Mango Edible Essence Market Size

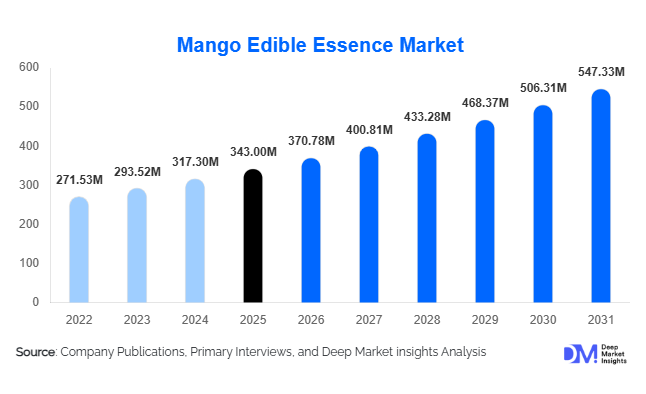

According to Deep Market Insights, the global mango edible essence market size was valued at USD 343 million in 2025 and is projected to grow from USD 370.78 million in 2026 to reach USD 547.33 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The mango edible essence market growth is primarily driven by rising demand for tropical fruit-based flavor systems, increasing adoption of clean-label ingredients across food and beverage applications, and growing utilization of natural flavor solutions in dairy, nutraceutical, confectionery, and pharmaceutical products. As consumers increasingly prefer authentic fruit-derived ingredients over synthetic alternatives, manufacturers are investing in advanced extraction, encapsulation, and flavor stabilization technologies to improve product quality, shelf life, and sensory performance. Expanding processed food production across emerging economies and growing exports of tropical-flavored products are further supporting market expansion globally.

Key Market Insights

- Natural mango edible essence accounts for more than 56% of global market revenue, supported by strong clean-label and natural ingredient demand.

- Beverages remain the largest application segment, contributing approximately 37% of total market demand due to increasing consumption of juices, flavored waters, and functional beverages.

- Asia-Pacific dominates the global market, accounting for nearly 41% of total revenue, driven by strong mango production and food processing industries.

- Nutraceutical and functional food applications represent the fastest-growing segment, with demand expanding at over 10% CAGR globally.

- Food and beverage manufacturers account for approximately 64% of total end-user demand, reflecting widespread adoption across industrial food production.

- Advanced extraction technologies and flavor encapsulation systems are increasingly being adopted to improve flavor consistency, stability, and shelf-life performance.

Mango Edible Essence Market Latest Trends

Growing Shift Toward Natural and Clean-Label Flavor Systems

Food manufacturers worldwide are increasingly replacing artificial flavor ingredients with natural fruit-derived alternatives. Mango edible essence has emerged as one of the most preferred tropical fruit flavors due to its broad consumer acceptance and compatibility across beverages, dairy products, bakery formulations, and confectionery applications. Regulatory authorities in North America and Europe continue to encourage transparency in ingredient labeling, prompting manufacturers to reformulate products using naturally sourced flavor solutions. Natural mango essence producers are investing heavily in sustainable sourcing programs, traceability systems, and advanced extraction technologies to meet growing customer requirements. This trend is expected to continue throughout the forecast period as consumers increasingly scrutinize ingredient lists and seek products containing recognizable natural ingredients.

Expansion of Functional Foods and Nutraceutical Applications

Mango edible essence is witnessing rapid adoption within the global functional foods and nutraceutical industries. Manufacturers of protein powders, gummy supplements, meal replacements, functional beverages, and wellness products are increasingly utilizing mango flavor systems to improve product palatability and consumer acceptance. Mango essence is particularly effective in masking bitterness associated with botanical extracts, vitamins, minerals, and plant proteins. The trend is further supported by rising health consciousness, increasing demand for personalized nutrition products, and strong growth within sports nutrition markets. Flavor houses are developing customized mango profiles specifically designed for nutraceutical applications, creating new growth avenues for industry participants.

Mango Edible Essence Market Drivers

Rising Global Demand for Tropical Fruit Flavors

Consumer preferences continue to evolve toward exotic and tropical flavor experiences, particularly among younger demographics seeking differentiated food and beverage products. Mango remains one of the most universally accepted tropical fruit flavors globally, making it highly attractive for product developers. Beverage manufacturers, dairy producers, confectionery companies, and bakery brands are increasingly introducing mango-flavored product variants to capitalize on evolving taste preferences. This widespread adoption across multiple industries continues to drive demand for mango edible essence worldwide.

Growth of Processed Food and Beverage Manufacturing

The continued expansion of global processed food production remains a major growth driver for the mango edible essence market. Urbanization, changing lifestyles, and rising disposable incomes are supporting increased consumption of packaged foods, ready-to-drink beverages, frozen desserts, and convenience products. Manufacturers require consistent flavor systems capable of maintaining product quality across large-scale production environments, making mango edible essence an increasingly valuable ingredient. Rapid industrialization of food processing sectors in Asia-Pacific, Latin America, and the Middle East is further accelerating demand.

Increasing Adoption of Natural Ingredients

Growing consumer awareness regarding ingredient quality and health considerations has accelerated demand for natural flavor ingredients. Food brands increasingly use natural mango essence to support premium product positioning and meet clean-label objectives. Natural flavor systems also provide competitive differentiation in highly saturated consumer markets, encouraging widespread adoption among global manufacturers.

Mango Edible Essence Market Restraints

Volatility in Mango Raw Material Supply

The availability and pricing of mango raw materials remain heavily influenced by climatic conditions, seasonal harvest cycles, disease outbreaks, and agricultural productivity. Weather-related disruptions can significantly affect fruit quality and extraction yields, creating supply chain uncertainty for manufacturers. These fluctuations often increase procurement costs and reduce profit margins for producers of natural mango edible essence.

Stringent Regulatory and Labeling Requirements

Manufacturers operating across multiple geographies must comply with varying regulatory frameworks governing food flavor ingredients. Differences in labeling standards, natural flavor definitions, food safety regulations, and import requirements increase operational complexity and compliance costs. Regulatory approvals for new formulations can also extend product development timelines and delay commercialization activities.

Mango Edible Essence Industry Key Opportunities

Expansion of Functional Beverage Manufacturing

The rapid growth of functional beverages presents a substantial opportunity for mango edible essence suppliers. Categories including energy drinks, sports beverages, fortified juices, kombuchas, hydration products, and wellness drinks increasingly incorporate tropical fruit flavors to improve consumer appeal. Mango flavor profiles are particularly well suited for blending with vitamins, minerals, botanicals, and plant-based ingredients. As functional beverage manufacturers continue to expand globally, demand for specialized mango flavor solutions is expected to increase significantly.

Investment in Emerging Market Processing Infrastructure

Governments across major mango-producing countries such as India, Thailand, Vietnam, Indonesia, and Brazil are promoting value-added agricultural processing through financial incentives, export support programs, and industrial infrastructure development. These initiatives encourage local processing of mango-derived ingredients rather than exporting raw fruit. New extraction facilities, flavor manufacturing plants, and export-oriented food ingredient operations are creating long-term growth opportunities for both domestic and international market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 343.00 Million |

| Market Size in 2026 | USD 370.78 Million |

| Market Size in 2031 | USD 547.33 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Nature Insights

Natural mango edible essence dominates the global market with an estimated 56% share of total revenue, driven by accelerating consumer demand for clean-label, minimally processed, and naturally derived food ingredients. The expansion of premiumization trends across the food and beverage industry continues to reinforce the preference for natural mango flavor systems, particularly in applications where authenticity of taste and ingredient transparency play a critical role in brand positioning. Regulatory encouragement toward naturally sourced additives and the growing scrutiny of artificial flavoring agents further strengthen the dominance of this segment. Manufacturers are increasingly integrating natural mango essence into beverages, dairy formulations, frozen desserts, and confectionery products to enhance sensory appeal and product differentiation, while also aligning with evolving health-conscious consumption patterns. Nature-identical mango essence continues to play a supporting role in cost-sensitive formulations where flavor consistency, scalability, and affordability remain essential, particularly in mass-market beverage and processed food categories. Artificial mango essence, while still present in select emerging and price-driven markets, is experiencing gradual share erosion due to shifting consumer perceptions and tightening food safety regulations. Continued innovation in extraction technologies, including improved cold-press and solvent-free methods, along with the expansion of sustainable mango sourcing ecosystems, is expected to further consolidate the leadership position of natural mango edible essence over the forecast period.

Form Insights

Liquid mango edible essence remains the dominant form segment, accounting for approximately 61% of global demand, primarily due to its superior solubility, ease of integration, and operational efficiency in large-scale industrial food processing environments. The leading driver of this segment is the strong reliance of beverage manufacturers on liquid formulations, as they enable consistent flavor dispersion across juices, carbonated drinks, flavored waters, and dairy-based beverages while minimizing production complexity and processing time. The compatibility of liquid essence with automated dosing systems and high-throughput production lines further enhances its widespread adoption across global manufacturing facilities. Powdered and encapsulated mango essence formats are witnessing strong momentum, supported by rising demand from bakery, confectionery, nutraceutical, and instant food applications where shelf stability, flavor retention, and extended storage life are critical performance factors. These formats are increasingly preferred in dry mix formulations and health-focused products due to their ability to preserve volatile flavor compounds under varying temperature and humidity conditions. Emulsion-based and concentrated paste formats are also gaining traction in specialized applications that require intensified flavor profiles, improved heat stability, and controlled release characteristics, particularly in premium desserts and processed food innovations.

Application Insights

Beverages continue to represent the largest application segment, contributing nearly 37% of total global demand, supported by sustained innovation across fruit juices, functional beverages, flavored waters, carbonated drinks, and sports nutrition products. The primary growth driver in this segment is the increasing consumer shift toward refreshing, tropical, and functional flavor experiences, combined with the rapid expansion of ready-to-drink beverage formats across both developed and emerging markets. Dairy products form the second-largest application category, supported by strong consumption of flavored milk, yogurts, ice creams, and frozen desserts, where mango essence is widely used to enhance taste appeal and product variety. Confectionery and bakery applications continue to expand as manufacturers incorporate mango flavor systems into candies, gummies, pastries, cakes, and snack products to cater to evolving consumer preferences for exotic and fruit-based flavor profiles. Nutraceutical applications are emerging as a high-growth area, driven by the need for effective flavor masking solutions in protein powders, dietary supplements, and functional wellness formulations, where palatability significantly influences consumer adherence. Pharmaceutical applications are also steadily increasing, particularly in pediatric and oral care formulations, where mango flavoring is utilized to improve medication acceptance and patient compliance.

End-User Insights

Food and beverage manufacturers remain the dominant end-user segment, accounting for approximately 64% of total market demand, supported by continuous product innovation, rapid expansion of packaged food portfolios, and increasing introduction of tropical flavor variants across global markets. The leading driver for this segment is the growing emphasis on product differentiation and sensory enhancement, which encourages manufacturers to integrate mango essence into a wide range of new product launches. Dairy processors represent a significant secondary end-user group, driven by rising global consumption of flavored dairy products and increasing demand for indulgent yet natural taste experiences. Nutraceutical manufacturers are emerging as one of the fastest-growing end-user categories, fueled by the expansion of sports nutrition, dietary supplements, and functional health products where flavor masking plays a critical role in consumer acceptance. Pharmaceutical companies continue to adopt mango edible essence to improve the palatability of oral dosage forms, particularly in pediatric and geriatric segments where taste significantly impacts compliance. Foodservice operators and HORECA channels also contribute meaningfully to demand through the incorporation of mango flavor systems in desserts, beverages, and seasonal menu innovations aimed at enhancing customer experience.

Explore more data points, trends and opportunities Download Free Sample Report

Mango Edible Essence Market Segmentations

By Nature

- Natural Mango Edible Essence

- Nature-Identical Mango Edible Essence

- Artificial/Synthetic Mango Edible Essence

By Form

- Liquid Mango Edible Essence

- Powder Mango Edible Essence

- Emulsion-Based Mango Essence

- Encapsulated Mango Essence

- Concentrated Paste Essence

By Flavor Profile

- Alphonso Mango Profile

- Totapuri Mango Profile

- Kent Mango Profile

- Tommy Atkins Mango Profile

- Mixed Tropical Mango Profile

By Application

- Beverages

- Dairy Products

- Bakery Products

- Confectionery

- Snacks & Savory Products

- Nutraceuticals & Dietary Supplements

- Pharmaceutical Applications

- Foodservice & HORECA

By End User

- Food & Beverage Manufacturers

- Dairy Processors

- Bakery & Confectionery Manufacturers

- Nutraceutical Companies

- Pharmaceutical Companies

- Foodservice Operators

Regional Insights

Asia-Pacific

Asia-Pacific leads the global mango edible essence market with approximately 41% of total revenue in 2025, supported by strong agricultural base, extensive mango cultivation, and a rapidly expanding food processing industry. The primary growth driver in the region is the deep cultural and culinary integration of mango-based flavors, combined with the rapid industrialization of beverage and dairy manufacturing sectors. India plays a pivotal role as both a leading producer and consumer, benefiting from abundant raw material availability and a well-established flavor extraction ecosystem. China continues to witness robust demand growth driven by urbanization, rising disposable incomes, and strong expansion in packaged beverage and dairy categories. Southeast Asian countries such as Thailand, Indonesia, and Vietnam contribute significantly due to strong tropical fruit consumption patterns and export-oriented food processing industries, while Japan and South Korea drive premium demand through innovation in functional beverages and high-value confectionery products. Government initiatives supporting food processing infrastructure development and export-oriented value-added agriculture further reinforce the region’s dominant position in the global market.

North America

North America accounts for approximately 24% of global market revenue, with the United States representing the largest share of regional demand. The key growth driver in this region is the rising consumer preference for natural, clean-label, and exotic flavor experiences, particularly within the premium beverage and functional food categories. Strong innovation in ready-to-drink beverages, dairy alternatives, and health-oriented food products continues to accelerate adoption of mango edible essence. The expansion of wellness-focused consumption trends and increasing demand for natural fruit-based flavor systems further support market penetration. Canada also demonstrates steady growth, driven by rising awareness of natural ingredients and increasing incorporation of tropical flavors into mainstream food and beverage products.

Europe

Europe represents approximately 21% of global demand, supported by strong regulatory frameworks that favor natural ingredients and a highly discerning consumer base that prioritizes ingredient transparency and product quality. The key growth driver in the region is the strict regulatory environment surrounding artificial additives, which has significantly accelerated the shift toward natural mango edible essence across multiple food categories. Germany, the United Kingdom, France, Italy, and Spain are leading markets, driven by strong demand in premium confectionery, bakery, dairy, and functional nutrition segments. European manufacturers continue to invest in product reformulation and clean-label innovation strategies, which further support long-term demand growth for natural fruit-based flavor systems.

Latin America

Latin America contributes approximately 8% of global market revenue, with growth primarily driven by expanding food processing capabilities and increasing consumption of processed beverages and dairy products. The leading growth driver in the region is the strong availability of tropical fruits combined with the rapid expansion of domestic beverage manufacturing industries. Brazil dominates the regional market due to its well-established fruit processing sector and growing demand for flavored beverages, while Mexico and Argentina are experiencing rising adoption of mango flavor systems in packaged food and drink applications. Export-oriented food production and increasing investment in food processing infrastructure continue to support regional market expansion.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of global demand, with growth driven by increasing urbanization, rising disposable incomes, and expanding food and beverage manufacturing capabilities. The primary growth driver is the rising consumption of flavored beverages and dairy products in rapidly urbanizing economies, supported by a growing preference for tropical and exotic taste profiles. GCC countries are investing heavily in food processing and import substitution strategies, which is strengthening regional production capacity and increasing demand for flavor ingredients. South Africa remains the largest market in the region due to its developed food manufacturing base, while Egypt is emerging as a key growth hub supported by expanding beverage and dairy sectors. Overall, increasing modernization of retail food systems and rising consumer exposure to global flavor trends are expected to sustain long-term growth across the region.

Key Players in the Mango Edible Essence Market

- IFF

- Givaudan

- dsm-firmenich

- Symrise

- Sensient Technologies

- ADM

- Takasago International Corporation

- MANE

- Flavorchem Corporation

- Bell Flavors & Fragrances

- T. Hasegawa Co., Ltd.

- Kerry Group

- Synergy Flavors

- Huabao International Holdings

- Keva Flavours