Malt Corn Syrup Market Size

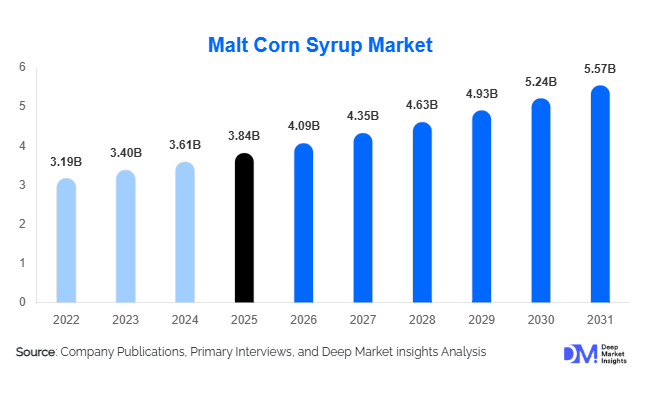

According to Deep Market Insights, the global malt corn syrup market size was valued at USD 3.84 billion in 2025 and is projected to grow from USD 4.09 billion in 2026 to reach USD 5.57 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The malt corn syrup market growth is primarily driven by rising consumption of processed foods, increasing utilization of corn-derived sweeteners in beverage manufacturing, and growing demand from brewing, fermentation, and industrial biotechnology applications. As manufacturers seek multifunctional ingredients that provide sweetness, texture enhancement, moisture retention, and fermentation support, malt corn syrup continues to gain importance across food and industrial value chains globally.

Key Market Insights

- Malt corn syrup remains a critical ingredient in processed food manufacturing, particularly across bakery, confectionery, dairy, and snack food applications.

- The beverage sector represents the fastest-growing demand segment, driven by expanding production of malt beverages, energy drinks, sports drinks, and alcoholic beverages.

- North America dominates the global market, supported by abundant corn production, mature starch processing infrastructure, and strong food manufacturing industries.

- Asia-Pacific is the fastest-growing regional market, led by increasing packaged food consumption and rapid industrialization in China and India.

- Demand for non-GMO and organic malt corn syrup products is rising, particularly in North America and Europe as food manufacturers adopt clean-label strategies.

- Industrial fermentation and biotechnology applications are emerging growth avenues, creating new demand streams beyond traditional food and beverage sectors.

Malt Corn Syrup Market Latest Trends

Growing Adoption of Clean-Label and Non-GMO Sweeteners

Food manufacturers are increasingly reformulating products to align with consumer demand for cleaner ingredient labels and greater transparency. This trend has accelerated investments in non-GMO and organic malt corn syrup production, particularly across North America and Europe. Large food brands are prioritizing traceability, sustainable sourcing, and certification programs to strengthen consumer confidence. As retailers expand shelf space dedicated to organic and natural foods, demand for premium malt corn syrup variants is expected to increase. Producers are also investing in identity-preserved corn supply chains and advanced quality assurance systems to capture higher-margin opportunities within specialty ingredient markets.

Expansion of Industrial Fermentation Applications

Malt corn syrup is increasingly being utilized as a carbohydrate substrate in fermentation-based manufacturing processes. The biotechnology industry is adopting corn-derived syrups for producing amino acids, enzymes, probiotics, organic acids, and specialty bio-based chemicals. Growing investments in sustainable industrial production and bioeconomy initiatives are supporting this trend. Manufacturers are developing customized syrup formulations with optimized maltose concentrations to improve fermentation efficiency and yield. As industrial biotechnology capacity expands globally, particularly in China, India, and the United States, fermentation applications are expected to become one of the fastest-growing segments within the malt corn syrup market.

Malt Corn Syrup Market Drivers

Increasing Demand for Processed and Convenience Foods

Urbanization, changing lifestyles, and rising disposable incomes continue to drive consumption of packaged and convenience foods globally. Malt corn syrup plays a crucial role in improving sweetness, texture, moisture retention, and shelf-life stability in bakery products, confectionery, cereals, dairy products, and processed foods. As food manufacturers expand production capacities to meet growing consumer demand, utilization of multifunctional sweeteners such as malt corn syrup continues to increase. Emerging economies in Asia-Pacific and Latin America are witnessing particularly strong growth in processed food consumption, creating sustained demand for corn-based sweeteners.

Growth of the Global Beverage Industry

The expanding beverage sector remains a major growth driver for the malt corn syrup market. Beverage manufacturers utilize malt corn syrup to enhance flavor profiles, improve mouthfeel, and support fermentation processes. Rising consumption of carbonated beverages, flavored malt drinks, sports beverages, energy drinks, and alcoholic beverages is increasing ingredient demand worldwide. The rapid expansion of premium beverage categories and craft brewing industries is further supporting adoption, particularly across Asia-Pacific and North America.

Technological Advancements in Starch Processing

Continuous improvements in enzymatic conversion technologies have enhanced production efficiency, reduced manufacturing costs, and improved product consistency. Modern starch hydrolysis systems enable manufacturers to produce tailored maltose concentrations for specific applications. Automation, process optimization, and energy-efficient manufacturing technologies are improving profitability while expanding application possibilities. These innovations are strengthening the competitiveness of malt corn syrup against alternative sweeteners and supporting long-term market growth.

Malt Corn Syrup Market Restraints

Volatility in Corn Prices and Agricultural Supply Chains

Corn represents the primary raw material used in malt corn syrup production. Agricultural disruptions caused by weather variability, biofuel demand fluctuations, trade restrictions, and geopolitical tensions can significantly impact corn prices. Such volatility directly affects production costs and profit margins, particularly for manufacturers operating under long-term supply contracts. Managing raw material procurement risks remains a key challenge across the industry.

Competition from Alternative Sweeteners

The growing popularity of alternative sweeteners such as stevia, monk fruit, agave syrup, and other natural sugar substitutes presents a competitive challenge. Consumer concerns regarding sugar consumption and ingredient perception are encouraging food manufacturers to diversify sweetener portfolios. While malt corn syrup continues to offer significant functional advantages, producers must invest in innovation, clean-label positioning, and product differentiation to maintain market competitiveness.

Malt Corn Syrup Industry Key Opportunities

Expansion of Functional and Malt-Based Beverage Manufacturing

The growing global market for functional beverages, sports nutrition products, flavored malt beverages, and low-alcohol drinks presents substantial opportunities for malt corn syrup suppliers. These beverage categories require ingredients that provide fermentability, sweetness balance, and texture enhancement. Emerging markets across Asia-Pacific, the Middle East, and Latin America are witnessing significant investments in beverage manufacturing, creating favorable conditions for long-term market expansion. Companies that develop customized formulations tailored to specific beverage applications are expected to benefit from premium pricing opportunities.

Growth of Industrial Biotechnology and Fermentation Markets

The rapid development of industrial biotechnology is creating new demand streams for malt corn syrup producers. Fermentation-based production of enzymes, amino acids, probiotics, organic acids, and bio-based chemicals increasingly relies on carbohydrate feedstocks. Governments worldwide are promoting sustainable manufacturing and bioeconomy initiatives, encouraging investments in fermentation infrastructure. This trend provides market participants with opportunities to diversify beyond traditional food and beverage applications while accessing high-growth industrial segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.84 Billion |

| Market Size in 2026 | USD 4.09 Billion |

| Market Size in 2031 | USD 5.57 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Conventional malt corn syrup accounted for approximately 41.8% of the global market in 2025, maintaining its position as the leading product category. The segment’s dominance is primarily attributed to its cost-effectiveness, widespread availability of corn feedstock, and extensive utilization across large-scale food and beverage manufacturing operations. Food processors continue to favor conventional variants due to their consistent performance, reliable supply chains, and compatibility with a broad range of formulations including bakery products, confectionery, beverages, and processed foods. The leading driver supporting this segment is the growing demand for affordable sweetening and texturizing ingredients among industrial food manufacturers seeking production efficiency and cost optimization. At the same time, non-GMO and organic malt corn syrup variants are witnessing robust growth as consumer preferences increasingly shift toward clean-label, natural, and sustainably sourced ingredients, particularly across North America and Europe. High maltose corn syrup products are also gaining significant traction in brewing, confectionery, and fermentation-based applications due to their enhanced fermentability, controlled sweetness profile, and superior functional performance. Manufacturers are increasingly introducing customized syrup formulations tailored to specific processing requirements, further expanding product diversification and application opportunities across food, beverage, pharmaceutical, and industrial sectors.

Physical Form Insights

Liquid malt corn syrup dominated the market with an estimated 67.2% share of global demand in 2025. The segment continues to benefit from widespread adoption across food and beverage manufacturing facilities where seamless integration into automated production systems is critical. The primary driver for the segment is the growing preference among manufacturers for ingredients that improve operational efficiency, reduce handling complexity, and enable precise dosing during large-scale production. Liquid formulations offer advantages including uniform mixing, ease of transportation through bulk handling systems, and enhanced process consistency, making them particularly attractive for bakery, confectionery, dairy, and beverage applications. Semi-concentrated variants continue to find demand in applications where transportation costs and storage efficiency are prioritized, while powdered malt corn syrup serves specialized applications requiring extended shelf life, simplified storage, and convenient blending with dry ingredients. Ongoing investments in liquid processing infrastructure, storage facilities, and bulk logistics networks are expected to further strengthen the dominance of liquid malt corn syrup throughout the forecast period.

Functionality Insights

Sweetening applications represented the largest functionality segment, accounting for approximately 44.7% of the global market. The segment’s leadership is driven by the increasing use of malt corn syrup as a versatile sweetening ingredient across confectionery, bakery, dairy, beverage, and processed food products. The leading growth driver is the rising demand for multifunctional sweeteners that provide not only sweetness but also texture enhancement, moisture retention, and improved product stability. Manufacturers increasingly utilize malt corn syrup to achieve balanced sweetness profiles while supporting desirable sensory characteristics. Beyond sweetening, moisture retention and texture enhancement functions contribute significantly to market demand by helping maintain softness, freshness, and consistency in baked goods and confectionery products. Shelf-life extension capabilities further enhance the ingredient’s value proposition by reducing product degradation during storage and distribution. In addition, fermentation-related applications are experiencing accelerated growth as biotechnology, brewing, and industrial fermentation industries expand globally, creating new opportunities for specialized malt corn syrup formulations.

Application Insights

Food and beverage applications collectively accounted for approximately 72.4% of total market demand, making them the largest application category in the global malt corn syrup market. The primary driver behind this dominance is the continuous growth of processed food consumption and the increasing demand for functional ingredients that improve product quality, taste, texture, and shelf stability. Bakery products remain the largest application segment due to malt corn syrup’s ability to enhance moisture retention, improve texture, prevent staling, and maintain product freshness over extended periods. Confectionery manufacturers extensively utilize malt corn syrup to control sugar crystallization, improve consistency, and enhance mouthfeel. Beverage applications are witnessing strong growth as producers increasingly adopt malt corn syrup to support sweetness management, fermentation efficiency, and flavor development in both alcoholic and non-alcoholic beverages. Beyond traditional food and beverage applications, industrial sectors including pharmaceuticals, nutraceuticals, animal nutrition, and biotechnology are emerging as important demand centers, providing manufacturers with opportunities to diversify revenue streams and expand into higher-value applications.

End-Use Industry Insights

The food processing industry remained the largest end-use segment, accounting for approximately 38.6% of the global market in 2025. The segment’s growth is primarily supported by rising production volumes of packaged foods, bakery products, confectionery items, ready-to-eat meals, and convenience foods worldwide. The leading driver is the increasing consumer demand for processed and convenience food products, particularly in urban markets where changing lifestyles continue to reshape consumption patterns. Food processors rely on malt corn syrup for its multifunctional properties, including sweetening, moisture retention, texture improvement, and shelf-life enhancement. Meanwhile, beverage manufacturing is emerging as the fastest-growing end-use segment, supported by increasing consumption of flavored beverages, energy drinks, sports drinks, malt-based beverages, and alcoholic products. Brewing and distilling industries continue to expand utilization due to the ingredient’s favorable fermentability characteristics and process efficiency benefits. Furthermore, biotechnology, pharmaceutical, and nutraceutical industries are creating new growth opportunities as fermentation-based manufacturing technologies gain increasing commercial relevance across global markets.

Distribution Channel Insights

Direct industrial sales dominated the market with approximately 61.9% share of global revenues. The segment’s leadership is primarily driven by the procurement preferences of large food and beverage manufacturers that require consistent quality, long-term supply agreements, and competitive pricing structures. The leading driver is the growing emphasis on supply chain reliability and strategic sourcing among major industrial buyers. Direct procurement arrangements enable manufacturers to secure stable raw material supplies while improving cost management and quality control. Ingredient distributors continue to play a critical role in serving medium-sized and regional manufacturers that require greater purchasing flexibility and technical support. Food ingredient traders facilitate international market access and support cross-border supply chains, particularly in emerging markets. Additionally, online B2B procurement platforms are steadily gaining traction as digital transformation accelerates across the ingredient industry. Enhanced transparency, real-time pricing visibility, and streamlined procurement processes are expected to strengthen digital distribution channels and improve overall market accessibility during the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Malt Corn Syrup Market Segmentations

By Product Type

- High Maltose Corn Syrup (HMCS)

- Malt Corn Syrup Blends

- Organic Malt Corn Syrup

- Non-GMO Malt Corn Syrup

- Conventional Malt Corn Syrup

By Physical Form

- Liquid Malt Corn Syrup

- Semi-Concentrated Malt Corn Syrup

- Dry Malt Corn Syrup Powder

By Functionality

- Sweetening Agent

- Bulking Agent

- Moisture Retention Agent

- Texture & Mouthfeel Enhancer

- Fermentation Substrate

- Shelf-Life Extension Ingredient

By Application

- Bakery Products

- Confectionery Products

- Dairy Products

- Frozen Desserts

- Breakfast Cereals

- Processed Foods

- Sauces & Dressings

- Snack Foods

- Carbonated Soft Drinks

- Energy & Sports Drinks

- Malt-Based Beverages

- Alcoholic Beverages

- Functional Beverages

- Syrups & Beverage Concentrates

- Pharmaceutical Formulations

- Nutraceutical Products

- Personal Care & Cosmetics

- Animal Feed Applications

- Fermentation & Biotechnology

By End-Use Industry

- Food Processing Industry

- Beverage Manufacturing Industry

- Brewing & Distilling Industry

- Pharmaceutical Industry

- Nutraceutical Industry

- Personal Care Industry

- Feed Industry

- Biotechnology Industry

Regional Insights

North America

North America accounted for approximately 34.5% of the global malt corn syrup market in 2025, making it the largest regional market. The United States dominates regional demand due to its extensive corn production capacity, advanced starch processing infrastructure, and highly developed food and beverage manufacturing sector. Strong consumption of processed foods, bakery products, confectionery, dairy products, and soft drinks continues to support market expansion. Canada contributes through its established food processing, brewing, and specialty ingredient industries, while Mexico is emerging as an important manufacturing hub serving both domestic and export markets. The primary driver for regional growth is the abundant availability of corn feedstock combined with the continued expansion of value-added food processing activities. Rising demand for clean-label ingredients, ongoing product innovation, and increasing investments in functional food formulations are further supporting market development across the region.

Europe

Europe represented approximately 23.8% of global market demand in 2025, supported by a mature food processing ecosystem and growing demand for specialty sweeteners and functional ingredients. Germany remains the largest regional market owing to its strong bakery, confectionery, brewing, and industrial food manufacturing sectors. France, the United Kingdom, Italy, and Spain also contribute substantially to regional consumption. Demand for organic, sustainable, traceable, and non-GMO ingredient solutions continues to rise, encouraging manufacturers to expand premium malt corn syrup product portfolios. The key driver of regional growth is the increasing adoption of specialty food ingredients that align with evolving consumer preferences for clean-label and high-quality food products. In addition, stringent food safety regulations, emphasis on supply chain transparency, and ongoing innovation in premium food and beverage formulations are expected to support long-term market expansion throughout Europe.

Asia-Pacific

Asia-Pacific accounted for approximately 31.2% of global demand in 2025 and is expected to remain the fastest-growing regional market, with a projected CAGR exceeding 7.5% through 2031. China leads regional consumption due to its large-scale food processing industry, expanding beverage sector, and rapidly growing biotechnology industry. India is emerging as one of the fastest-growing markets globally, supported by rising disposable incomes, increasing packaged food consumption, rapid urbanization, and expanding beverage production capacity. Japan and South Korea represent technologically advanced markets characterized by strong demand for high-performance specialty ingredients and premium food products. Southeast Asian countries including Indonesia, Thailand, Vietnam, and the Philippines are witnessing increasing adoption across food manufacturing and beverage industries. The primary driver for regional growth is the rapid expansion of processed food and beverage consumption driven by urbanization, changing dietary preferences, and a growing middle-class population. Continued industrialization of food production and investments in modern manufacturing infrastructure are expected to further accelerate demand across the region.

Latin America

Latin America accounted for approximately 5.1% of global market revenues in 2025. Brazil remains the dominant market owing to its large food and beverage manufacturing sector and expanding processed food industry. Argentina, Chile, Colombia, and other regional economies are witnessing growing adoption of corn-derived sweeteners as consumer demand for packaged foods and convenience products continues to rise. Investments in food processing infrastructure, modernization of manufacturing facilities, and increasing exports of processed food products are supporting regional market development. The leading driver for growth in Latin America is the expanding processed food industry coupled with rising consumer demand for affordable packaged food and beverage products. Furthermore, improving industrial capabilities and growing integration into global food supply chains are expected to strengthen regional demand over the forecast period.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5.4% of global demand in 2025. Saudi Arabia and the United Arab Emirates lead regional consumption due to ongoing investments in food processing, beverage manufacturing, and food security initiatives. South Africa remains the most developed market in Sub-Saharan Africa, supported by a well-established food production industry and growing demand for processed food products. Other countries across the region are increasingly investing in domestic food manufacturing capabilities to reduce import dependence and improve supply chain resilience. The primary driver of regional growth is the rapid expansion of urban populations and the corresponding increase in demand for packaged, convenient, and shelf-stable food products. Rising investments in food processing infrastructure, economic diversification strategies, and expanding retail distribution networks are expected to create favorable conditions for sustained market growth across the Middle East and Africa.

Key Players in the Malt Corn Syrup Market

- Cargill

- Archer Daniels Midland (ADM)

- Ingredion

- Tate & Lyle

- Roquette

- Tereos

- AGRANA

- Xiwang Group

- Zhucheng Dongxiao Biotechnology

- Kent Corporation

- San Soon Seng Food Industries

- Malt Products Corporation

- Gulshan Polyols

- Global Sweeteners Holdings

- COFCO Biochemical