Luxury White Wine Market Size

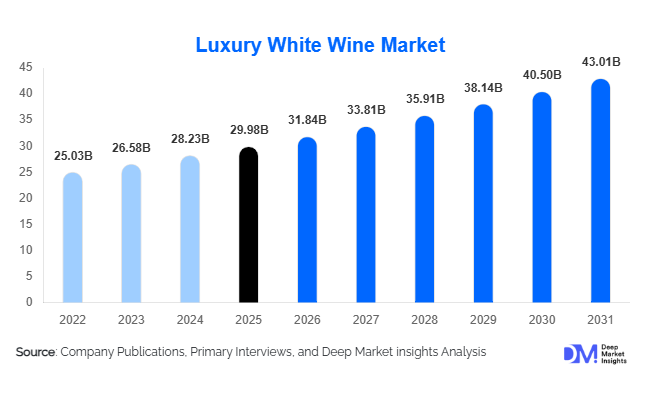

According to Deep Market Insights, the global luxury white wine market size was valued at USD 29.98 billion in 2025 and is projected to grow from USD 31.84 billion in 2026 to reach USD 43.01 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The luxury white wine market growth is primarily driven by rising global premiumization trends, increasing consumer preference for high-quality alcoholic beverages, expansion of luxury hospitality and fine dining establishments, and growing demand for premium white wine varietals such as Chardonnay, Sauvignon Blanc, Riesling, and Blanc de Blancs. The market is further supported by the expansion of affluent consumer populations across Asia-Pacific, increasing wine tourism activities, and the growing popularity of sustainable and biodynamic wine production methods.

Key Market Insights

- Luxury white wines are increasingly benefiting from premiumization trends, as consumers prioritize quality, provenance, exclusivity, and vineyard heritage over volume consumption.

- Chardonnay remains the dominant luxury white wine varietal globally, accounting for approximately 31% of market revenue due to strong demand from Burgundy, Napa Valley, and premium Australian producers.

- Europe dominates the luxury white wine market, supported by established wine-producing regions across France, Germany, Italy, and Spain, accounting for approximately 43% of global demand.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, luxury gifting culture, expanding wine education, and premium hospitality growth across China, India, Japan, and South Korea.

- Sustainability and biodynamic viticulture are becoming key purchasing criteria, particularly among affluent millennials and environmentally conscious wine consumers.

- Direct-to-consumer sales channels and premium wine e-commerce platforms are reshaping distribution, allowing wineries to improve margins while strengthening customer engagement and brand loyalty.

Luxury White Wine Market Latest Trends

Sustainable and Biodynamic Wine Production Gaining Momentum

Sustainability has become one of the most influential trends shaping the luxury white wine market. Consumers increasingly evaluate wineries based on environmental stewardship, carbon reduction initiatives, water conservation practices, and regenerative vineyard management. Biodynamic and organic luxury white wines are commanding premium prices in developed markets, particularly across Europe and North America. Leading producers are investing in renewable energy systems, precision irrigation technologies, and biodiversity conservation programs to strengthen their sustainability credentials. Premium wine buyers increasingly associate sustainability certifications with product quality, authenticity, and long-term brand value, making eco-conscious production a major competitive differentiator.

Growth of Direct-to-Consumer and Digital Wine Commerce

Luxury white wine producers are increasingly leveraging direct-to-consumer (DTC) channels to enhance customer relationships and improve profitability. Premium wineries are launching exclusive membership clubs, limited-edition allocations, virtual tasting experiences, and personalized subscription programs. Digital wine marketplaces are expanding access to high-net-worth consumers across emerging markets while providing enhanced product transparency and authenticity verification. Blockchain-enabled provenance tracking, AI-powered wine recommendations, and luxury wine investment platforms are further transforming the consumer experience. This trend is particularly strong among younger affluent consumers who seek convenience, exclusivity, and direct engagement with premium wine brands.

Luxury White Wine Market Drivers

Global Premiumization of Alcoholic Beverage Consumption

Consumers worldwide are increasingly shifting from mass-market alcoholic beverages toward premium and luxury products. The growing willingness to spend on superior quality, limited-production wines, and prestigious wine labels is supporting strong value growth across the luxury white wine segment. Affluent consumers increasingly view luxury wine as both a lifestyle product and a status symbol, driving demand across established and emerging markets. Premiumization is particularly evident among millennials and Generation X consumers who prioritize quality, authenticity, and experiential consumption over quantity.

Expansion of Luxury Hospitality and Fine Dining Industries

The rapid growth of luxury hotels, Michelin-starred restaurants, premium resorts, and wine tourism destinations continues to strengthen demand for luxury white wines. Fine dining establishments increasingly feature premium white wines as part of curated tasting menus and food-pairing experiences. Hospitality operators are expanding premium wine selections to meet growing consumer expectations, while luxury travel experiences increasingly incorporate vineyard visits, private tastings, and wine-focused tourism packages. This expansion of experiential luxury consumption continues to support market growth globally.

Rising Preference for White Wine Consumption

Consumer tastes are gradually shifting toward white wines due to their versatility, food compatibility, lower tannin profiles, and year-round consumption appeal. Premium Chardonnay, Sauvignon Blanc, Riesling, and sparkling white wines are increasingly favored by younger consumers and female wine drinkers. The growing popularity of seafood cuisine, Mediterranean diets, and lighter culinary experiences is further contributing to the expansion of luxury white wine demand globally.

Luxury White Wine Market Restraints

Climate Change and Vineyard Production Risks

Luxury white wine production depends heavily on terroir-specific vineyards and favorable climate conditions. Extreme weather events, droughts, heatwaves, frost damage, and changing precipitation patterns increasingly threaten grape yields and quality. Climate-related production disruptions can lead to supply shortages, higher prices, and increased operational costs for producers. Many premium wine regions are investing heavily in climate adaptation strategies, yet long-term production uncertainty remains a significant challenge.

Regulatory and Taxation Challenges

The luxury white wine market remains exposed to alcohol taxation, import tariffs, labeling regulations, and advertising restrictions across numerous countries. Trade disputes, changing alcohol policies, and increasing excise duties can negatively impact profitability and market accessibility. Premium wines are particularly vulnerable to regulatory changes due to their higher price points and dependence on international trade flows.

Luxury White Wine Industry Key Opportunities

Asia-Pacific Premium Consumption Expansion

Asia-Pacific presents the largest growth opportunity for luxury white wine producers. Rising disposable incomes, expanding affluent populations, growing western dining adoption, and increasing awareness of wine culture are driving premium wine consumption across China, India, Japan, South Korea, Singapore, and Southeast Asia. Luxury gifting traditions and the expansion of premium hospitality sectors further support demand growth. Producers that establish strong distribution networks and localized marketing strategies are expected to benefit significantly from this long-term opportunity.

Sustainable Luxury Wine Positioning

The growing consumer preference for sustainable products creates significant opportunities for wineries investing in organic, biodynamic, and environmentally responsible production methods. Sustainability certifications increasingly influence purchasing decisions among affluent consumers, particularly in Europe and North America. Producers adopting regenerative agriculture, renewable energy systems, and carbon-neutral production practices can command pricing premiums while strengthening brand differentiation and customer loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 29.98 Billion |

| Market Size in 2026 | USD 31.84 Billion |

| Market Size in 2031 | USD 43.01 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Style Insights

Still luxury white wine remains the dominant product style segment, accounting for approximately 46% of global market revenue in 2025. The segment continues to benefit from strong consumer preference for premium still wines that offer versatility across both everyday luxury consumption and formal dining occasions. Premium Chardonnay remains the leading category within still luxury white wines, supported by sustained demand for high-end labels originating from Burgundy, Napa Valley, Sonoma, Margaret River, and other globally recognized wine-producing regions. The segment’s leadership is driven by increasing consumer appreciation for terroir-driven wines, growing participation in wine education and tasting experiences, and strong demand from fine dining establishments that prioritize premium white wine offerings. In addition, Sauvignon Blanc, Riesling, Chenin Blanc, and premium blends continue to expand their presence among affluent consumers seeking diversity in flavor profiles and regional authenticity.Dessert and fortified luxury white wines, including Sauternes, Ice Wine, Tokaji, and other limited-production offerings, maintain niche yet highly profitable positions within the market. Their exclusivity, aging potential, and collector appeal continue to attract wine enthusiasts, investors, and high-net-worth consumers. Limited production volumes, strict geographic indications, and strong auction performance support premium pricing and long-term value appreciation. Across all product styles, increasing consumer preference for food-friendly wines, premium dining experiences, and versatile consumption occasions continues to strengthen demand for luxury white wines worldwide.

Price Tier Insights

The Premium Luxury segment, comprising wines priced between USD 50 and USD 100 per bottle, accounts for approximately 34% of global market revenue, making it the largest price category within the luxury white wine industry. The segment benefits from its ability to balance exclusivity and affordability, allowing affluent consumers to access high-quality wines without entering ultra-premium pricing levels. The leading growth driver for this segment is the expanding global affluent middle-class population, particularly in Asia-Pacific and North America, coupled with increasing consumer willingness to trade up from standard premium wines to luxury offerings. Premium Luxury wines are frequently purchased for gifting, fine dining, personal consumption, and wine exploration, making them highly accessible across multiple consumption occasions.Prestige Luxury and Icon Wine categories priced above USD 250 per bottle remain concentrated among high-net-worth individuals, institutional collectors, luxury hospitality establishments, and investment-focused buyers. Although these segments account for lower sales volumes, they generate significant revenue due to exceptionally high average selling prices, limited availability, strong brand heritage, and growing participation in wine auctions and secondary trading markets.

Distribution Channel Insights

Off-trade retail channels remain the largest distribution segment, accounting for approximately 39% of global luxury white wine sales. Specialty wine retailers, premium liquor stores, and luxury beverage boutiques continue to serve as preferred purchasing destinations for affluent consumers seeking expert guidance, exclusive product selections, and access to limited-production wines. The segment’s leadership is primarily driven by consumer preference for personalized recommendations, product authenticity, and broader portfolio availability compared to mass retail channels.On-trade distribution channels, including fine dining restaurants, luxury hotels, private clubs, resorts, and premium wine bars, continue to play a critical role in market expansion. Luxury white wines remain integral to premium dining experiences, curated tasting menus, and hospitality-driven consumption. Increasing global tourism activity, expansion of luxury hotel infrastructure, and growing consumer spending on experiential dining continue to support demand through on-trade channels.Online retail represents the fastest-growing distribution channel, supported by the rapid digitalization of wine purchasing behavior and increasing adoption of direct-to-consumer sales models. Winery-operated platforms, premium wine marketplaces, subscription services, and authenticated luxury wine exchanges provide consumers with convenient access to rare releases and exclusive allocations. Advanced personalization tools, digital wine education content, and improved logistics infrastructure continue to strengthen consumer confidence in online luxury wine purchases.

Consumer Type Insights

Individual luxury consumers account for approximately 44% of total market demand, making them the largest consumer segment within the global luxury white wine market. The segment’s leadership is driven by rising disposable incomes, lifestyle premiumization trends, growing wine knowledge, and increasing participation in wine tourism and tasting experiences. Affluent consumers increasingly view luxury white wine as both a lifestyle product and a reflection of personal taste, supporting sustained demand across major developed and emerging markets.Wine collectors and investors represent one of the most valuable customer groups due to their focus on rare vintages, limited-production wines, and high-appreciation assets. White Burgundy, vintage Champagne, premium Riesling, and collectible dessert wines continue to attract significant investment interest as alternative asset classes gain broader acceptance among wealth managers and private investors.Corporate gifting buyers remain an important source of demand, particularly across Asia-Pacific and the Middle East, where luxury wines are increasingly incorporated into executive gifting, relationship management, and premium business entertainment practices. Simultaneously, hospitality buyers, including luxury hotels, fine dining establishments, resorts, and cruise operators, continue to expand purchases as premium wine programs become essential components of high-end guest experiences and brand differentiation strategies.

Production Method Insights

Conventional premium viticulture remains the dominant production method, accounting for approximately 57% of global market revenue. The segment benefits from established vineyard infrastructure, production consistency, broad consumer familiarity, and the ability to maintain reliable quality across large-scale premium wine operations. The leading driver supporting segment leadership is the extensive global availability of conventionally produced luxury wines across renowned wine regions, ensuring stable supply and widespread market penetration.However, organic, biodynamic, and sustainability-certified luxury white wines are expanding at a significantly faster pace than the broader market. Rising environmental awareness, increasing scrutiny of agricultural practices, and growing consumer preference for authenticity and transparency are encouraging producers to adopt sustainable vineyard management techniques. Premium consumers increasingly associate environmentally responsible production with superior quality, terroir expression, and long-term brand value.Natural luxury wines are also gaining visibility among younger affluent consumers and wine enthusiasts seeking minimal-intervention production methods and distinctive flavor characteristics. Although the segment remains relatively small, increasing experimentation among premium wineries and growing interest from specialty retailers continue to support future growth opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Luxury White Wine Market Segmentations

By Product Style

- Still Luxury White Wine

- Sparkling Luxury White Wine

- Dessert & Fortified Luxury White Wine

By Grape Variety

- Chardonnay

- Sauvignon Blanc

- Riesling

- Pinot Grigio/Pinot Gris

- Chenin Blanc

- Semillon

- Albariño

- Viognier

- Gewürztraminer

- Other Luxury White Varietals

By Production Method

- Conventional Premium Viticulture

- Organic Luxury White Wine

- Biodynamic Luxury White Wine

- Sustainable-Certified Luxury White Wine

- Natural Luxury White Wine

By Distribution Channel

- Fine Dining Restaurants

- Luxury Hotels & Resorts

- Wine Bars

- Specialty Wine Retailers

- Premium Liquor Stores

- Duty-Free Retail

- Winery Direct-to-Consumer

- Premium Wine E-Commerce

- Wine Subscription Clubs

By Consumer Type

- Individual Luxury Consumers

- Wine Collectors & Investors

- Corporate & Gifting Buyers

- Hospitality Buyers

- Institutional Luxury Beverage Buyers

Regional Insights

Europe

Europe remains the largest luxury white wine market globally, accounting for approximately 43% of market share in 2025. France represents the largest individual country market with approximately 18% global share, supported by world-renowned production regions including Burgundy, Champagne, Loire Valley, and Alsace. Germany maintains leadership in premium Riesling production and consumption, while Italy continues to expand its presence through premium Pinot Grigio, Soave, and luxury sparkling wine offerings. The United Kingdom remains one of the world's largest import destinations for luxury white wines, supported by a sophisticated consumer base and mature fine wine market.Regional growth is primarily driven by Europe's unparalleled concentration of prestigious appellations, strong export performance, increasing premiumization across domestic consumption markets, and continued growth in wine tourism. Established vineyard infrastructure, centuries-old winemaking traditions, robust geographical indication protections, and sustained demand from international collectors further reinforce Europe's leadership position. The region also benefits from expanding demand for organic and biodynamic luxury wines, particularly in France, Germany, and Italy, where sustainability initiatives are increasingly influencing purchasing decisions.

North America

North America accounts for approximately 28% of global luxury white wine demand, led overwhelmingly by the United States. American consumers demonstrate strong demand for premium Chardonnay, Sauvignon Blanc, Riesling, and imported European luxury wines. Napa Valley and Sonoma remain major production centers for premium white wines, while Canada contributes additional market growth through luxury imports and globally recognized Ice Wine production.The region's growth is being driven by rising consumer spending on premium alcoholic beverages, increasing participation in wine tourism, and expanding interest in wine education and tasting experiences. Growth in direct-to-consumer sales channels, digital wine platforms, and subscription-based wine services continues to improve market accessibility. Furthermore, growing consumer preference for sustainable, organic, and premium-quality wines supports ongoing premiumization across the region. Strong demand from luxury restaurants, hospitality operators, and affluent millennial consumers further accelerates market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market and is forecast to expand at a CAGR exceeding 8.5% through 2031. China accounts for approximately 6% of global market demand and remains the region's largest luxury white wine consumer. Japan contributes approximately 3% of global demand, supported by strong food-pairing traditions and consistent consumption of imported premium wines. India is emerging as one of the fastest-growing luxury white wine markets globally due to expanding affluent populations, rising luxury consumption, and increasing exposure to global wine culture. South Korea, Singapore, Australia, and Hong Kong continue to contribute substantial premium wine demand across the region.Regional growth is primarily driven by rapid wealth creation, urbanization, expanding middle- and upper-income consumer groups, and increasing acceptance of wine as a status-oriented lifestyle product. Growth in luxury hospitality infrastructure, international tourism, premium dining culture, and corporate gifting practices continues to stimulate demand. The rising influence of digital commerce, wine education programs, and international wine events is further accelerating consumer awareness and market penetration. In addition, younger affluent consumers increasingly view luxury wines as premium lifestyle and investment products, creating long-term growth opportunities across the region.

Latin America

Latin America accounts for approximately 6% of global luxury white wine demand. Brazil remains the largest consumer market within the region, supported by a growing affluent population, increasing exposure to international luxury brands, and rising participation in premium dining experiences. Mexico, Argentina, and Chile continue contributing to market growth through expanding hospitality sectors, growing imports of luxury wines, and increasing consumer interest in premium alcoholic beverages.Regional growth is supported by rising disposable incomes among upper-income urban consumers, expansion of luxury retail infrastructure, and increasing influence of global wine culture. Growth in international tourism, premium restaurants, and luxury hotel developments is strengthening demand for imported luxury white wines. Additionally, local wine-producing countries such as Argentina and Chile are increasingly investing in premium white wine production and export-oriented strategies, contributing to broader market development across the region.

Middle East & Africa

The Middle East and Africa region accounts for approximately 4% of global market revenue. The United Arab Emirates remains the dominant luxury wine consumption hub due to its thriving hospitality industry, strong international tourism sector, and concentration of high-income consumers. Qatar and selected luxury hospitality channels across Saudi Arabia contribute additional demand through premium tourism and luxury dining activities. South Africa remains the region's leading producer and exporter of premium white wines, benefiting from strong international recognition and favorable production economics.Regional growth is being driven by expanding luxury hospitality investments, rising international visitor arrivals, and increasing demand for premium dining experiences across major tourism destinations. The continued development of luxury hotels, resorts, fine dining establishments, and entertainment venues in Gulf Cooperation Council countries supports consumption of high-end wines through licensed hospitality channels. In Africa, growing international demand for South African premium wines, increasing export opportunities, and investments in vineyard modernization continue to strengthen the region's position within the global luxury white wine industry.

Key Players in the Luxury White Wine Market

- Treasury Wine Estates

- LVMH Wines & Spirits

- Constellation Brands

- Pernod Ricard

- E. & J. Gallo Winery

- Jackson Family Wines

- Duckhorn Portfolio

- Champagne Taittinger

- Louis Jadot

- Trinchero Family Estates

- Banfi Vintners

- Marchesi Antinori

- Beringer Vineyards

- Villa Maria Estate

- Gonzalez Byass