Liquid Butter Alternatives Market Size

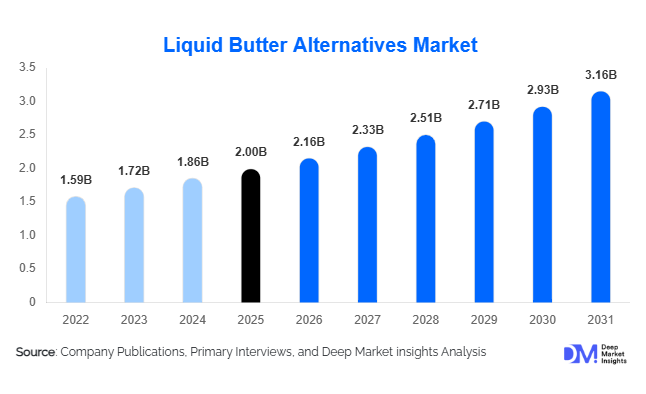

According to Deep Market Insights, the global liquid butter alternatives market size was valued at approximately USD 2.0 billion in 2025 and is projected to grow from USD 2.16 billion in 2026 to reach USD 3.16 billion by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The liquid butter alternatives market growth is primarily driven by increasing adoption across foodservice establishments, rising demand for cost-effective butter substitutes, growing consumption of processed and convenience foods, and expanding preference for plant-based and trans-fat-free formulations. Liquid butter alternatives provide superior operational efficiency, longer shelf life, consistent flavor delivery, and improved heat stability compared to conventional dairy butter, making them highly attractive for commercial kitchens and industrial food manufacturers.

Key Market Insights

- Foodservice operators are increasingly replacing traditional butter with liquid alternatives to reduce labor costs, improve consistency, and enhance kitchen efficiency.

- Plant-based liquid butter alternatives are witnessing strong adoption globally, supported by growing vegan, flexitarian, and health-conscious consumer populations.

- North America dominates the global market, accounting for nearly 35% of total demand due to its mature foodservice sector and extensive processed food industry.

- Asia-Pacific is the fastest-growing regional market, driven by rapid expansion of restaurant chains, food processing facilities, and organized foodservice infrastructure.

- Trans-fat-free and clean-label formulations are becoming industry standards, particularly across North America and Europe where regulatory scrutiny remains high.

- Technological innovation in flavor systems, emulsification, and oil blending is enabling manufacturers to closely replicate the taste and performance of dairy butter.

Liquid Butter Alternatives Market Latest Trends

Rapid Expansion of Plant-Based Butter Alternatives

The growing global shift toward plant-based food consumption is significantly influencing the liquid butter alternatives market. Manufacturers are increasingly developing formulations based on sunflower oil, canola oil, avocado oil, and coconut oil to meet evolving consumer preferences for dairy-free and vegan products. Foodservice operators and industrial food manufacturers are integrating these products into baked goods, snacks, sauces, and ready meals to align with clean-label and sustainability objectives. Premium plant-based products are also gaining traction among consumers seeking cholesterol-free alternatives without compromising flavor or cooking performance.

Clean-Label and Functional Ingredient Innovation

Consumers are demanding greater transparency in food ingredients, encouraging manufacturers to reformulate products with simpler ingredient lists and natural flavor systems. Clean-label liquid butter alternatives featuring non-GMO oils, natural emulsifiers, and allergen-free formulations are gaining popularity across developed markets. Simultaneously, ingredient suppliers are investing in advanced flavor encapsulation technologies and high-oleic oil blends that improve heat stability, oxidation resistance, and shelf life. These innovations are helping manufacturers differentiate products while addressing regulatory and consumer expectations.

Liquid Butter Alternatives Market Drivers

Growth of Global Foodservice and Quick-Service Restaurants

The rapid expansion of quick-service restaurants (QSRs), casual dining chains, institutional catering services, and cloud kitchens is creating substantial demand for liquid butter alternatives. These products eliminate the need for butter melting, improve operational consistency, and reduce ingredient waste. Major restaurant operators increasingly standardize liquid butter alternatives across locations to ensure uniform product quality and cost control. The continuing expansion of foodservice infrastructure in emerging economies is further accelerating adoption.

Increasing Focus on Cost Optimization in Food Manufacturing

Food manufacturers are under constant pressure to manage production costs while maintaining product quality. Volatility in global dairy prices has encouraged bakery, snack, frozen food, and ready-meal producers to adopt liquid butter alternatives as cost-efficient substitutes. These products provide predictable pricing, improved handling characteristics, and enhanced production efficiency, making them attractive ingredients for large-scale food manufacturing operations.

Rising Demand for Health-Oriented Fat Solutions

Growing awareness of cardiovascular health and dietary wellness has increased demand for trans-fat-free and cholesterol-free ingredient solutions. Liquid butter alternatives formulated with canola, sunflower, and high-oleic vegetable oils offer improved nutritional profiles compared to traditional butter. Regulatory initiatives targeting trans fats and unhealthy ingredients are further supporting market adoption across foodservice and industrial food applications.

Liquid Butter Alternatives Market Restraints

Strong Consumer Preference for Traditional Dairy Butter

Despite functional and economic advantages, many consumers continue to perceive dairy butter as a premium and natural ingredient. Premium bakery products, artisanal food manufacturers, and certain foodservice establishments often emphasize authentic butter usage as a quality differentiator. This perception can limit substitution rates in high-end applications and premium consumer segments.

Raw Material Price Volatility and Regulatory Compliance

The market remains sensitive to fluctuations in vegetable oil prices, particularly soybean, sunflower, palm, and canola oils. Supply chain disruptions, geopolitical developments, and agricultural production variability can significantly impact manufacturing costs. In addition, evolving food labeling requirements, sustainability mandates, and ingredient regulations increase compliance costs and create reformulation challenges for manufacturers operating across multiple regions.

Liquid Butter Alternatives Industry Key Opportunities

Expansion Across Emerging Foodservice Markets

Emerging economies in Asia-Pacific, Latin America, and the Middle East present substantial growth opportunities for liquid butter alternative manufacturers. Rising urbanization, growing disposable incomes, and expanding restaurant networks are increasing demand for efficient cooking ingredients. Foodservice operators in these markets are increasingly seeking products that improve consistency while reducing operational costs. As organized foodservice continues to replace traditional food outlets, demand for liquid butter alternatives is expected to accelerate significantly.

Development of Premium and Specialty Formulations

Manufacturers have significant opportunities to develop differentiated products targeting premium foodservice and industrial applications. Organic, allergen-free, non-GMO, and high-oleic oil-based formulations can command premium pricing while addressing specific customer requirements. Specialty products optimized for baking, frying, popcorn coating, and frozen food manufacturing are gaining traction as food producers seek tailored ingredient solutions. Sustainability-focused products using responsibly sourced oils also offer significant growth potential, particularly in Europe and North America.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.00 Billion |

| Market Size in 2026 | USD 2.16 Billion |

| Market Size in 2031 | USD 3.16 Billion |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Liquid butter-flavored oils emerged as the leading product type segment, accounting for approximately 32% of global market revenue in 2025. The segment’s dominance is primarily driven by its superior versatility, cost-effectiveness, and operational efficiency across commercial kitchens, quick-service restaurants, institutional catering facilities, and industrial food processing operations. These products provide butter-like flavor characteristics while offering enhanced shelf stability, ease of handling, and improved heat performance compared to traditional butter, making them particularly attractive for large-scale food preparation. Growing demand for consistent flavor delivery, reduced food preparation costs, and improved production efficiency continues to strengthen adoption across the foodservice sector.Liquid margarine remains a significant category, particularly within bakery, confectionery, and processed food manufacturing applications where manufacturers require standardized fat functionality, reliable texture development, and production consistency. The segment benefits from its suitability for high-volume industrial operations and its ability to support product quality across diverse food formulations.Plant-based liquid butter alternatives represent the fastest-growing product category, supported by the rapid expansion of vegan, vegetarian, and flexitarian consumer populations worldwide. Increasing consumer preference for dairy-free ingredients, sustainability-focused food products, and allergen-friendly formulations is encouraging manufacturers to expand plant-based product portfolios. Additionally, flavored liquid butter alternatives incorporating garlic, herbs, cheese, and specialty seasoning profiles are gaining popularity among foodservice operators seeking value-added flavor enhancement solutions that improve menu differentiation and customer appeal.

Oil Base Insights

Soybean oil-based formulations accounted for approximately 29% of the global market in 2025, making them the largest oil-base segment. The segment’s leadership is driven by the widespread availability of soybean oil, well-established global supply chains, favorable pricing dynamics, and extensive utilization across food processing industries. Manufacturers continue to favor soybean oil due to its functional versatility, reliable supply, and compatibility with a broad range of foodservice and industrial applications.Canola oil-based products are experiencing growing demand owing to their favorable nutritional profile, lower saturated fat content, and excellent heat stability characteristics. The increasing emphasis on healthier cooking ingredients among foodservice operators and consumers continues to support segment growth. Sunflower oil-based alternatives are witnessing particularly strong adoption across Europe, where demand for non-GMO ingredients, clean-label products, and healthier edible oil options remains robust.Multi-oil blends are increasingly being utilized by manufacturers seeking to optimize functionality, flavor performance, nutritional characteristics, and cost efficiency simultaneously. These blended formulations allow producers to balance performance requirements while managing raw material price volatility. Premium formulations incorporating avocado oil, olive oil, and specialty vegetable oils continue to gain traction in premium foodservice, gourmet culinary applications, and clean-label product development as consumers increasingly prioritize ingredient transparency and perceived health benefits.

Application Insights

Frying applications accounted for approximately 27% of total market demand in 2025, making them the largest application segment globally. The segment’s dominance is primarily driven by the growing requirement for high-performance cooking fats capable of delivering superior heat stability, extended frying life, consistent flavor profiles, and reduced burning characteristics. Commercial kitchens, quick-service restaurants, and institutional foodservice operators increasingly prefer liquid butter alternatives for frying because they help improve operational efficiency, reduce waste, and maintain product consistency across high-volume food preparation environments.Baking remains one of the most important application areas, supported by strong demand from industrial bakeries, confectionery manufacturers, and packaged food producers requiring consistent fat functionality, texture enhancement, moisture retention, and flavor delivery. The ability of liquid butter alternatives to support large-scale automated production processes continues to drive adoption within commercial baking operations.Topping and finishing applications are expanding steadily across restaurant chains, catering services, and foodservice establishments seeking convenient flavor enhancement solutions. Furthermore, increasing utilization in popcorn coating, sauce preparation, snack manufacturing, frozen foods, and ready-to-eat meal production reflects the growing importance of liquid butter alternatives as multifunctional ingredients capable of enhancing taste, appearance, and processing efficiency across diverse food categories.

Distribution Channel Insights

Direct B2B sales accounted for approximately 38% of global market revenue in 2025, making them the leading distribution channel. The segment’s growth is primarily driven by long-term procurement contracts between manufacturers and large foodservice operators, restaurant chains, institutional catering organizations, and food processing companies. Direct sales channels provide customers with pricing advantages, customized product solutions, technical support, and reliable supply continuity, making them the preferred procurement model for high-volume purchasers.Foodservice distributors continue to play a critical role in market expansion by facilitating product access for restaurants, hotels, cafés, bakeries, and institutional kitchens across North America and Europe. Their extensive distribution networks enable manufacturers to efficiently serve fragmented customer bases while maintaining product availability.Modern retail channels and e-commerce platforms are experiencing steady growth as household consumers increasingly adopt liquid butter alternatives for home cooking, baking, and specialty culinary applications. The growing penetration of online grocery platforms, coupled with rising consumer awareness of alternative cooking fats, is creating additional growth opportunities. Specialty ingredient suppliers remain essential distribution partners for industrial food manufacturers requiring customized formulations, product development assistance, and technical expertise.

End-Use Insights

Restaurants and quick-service restaurants (QSRs) represented approximately 34% of global demand in 2025, making them the largest end-use segment. The primary growth driver for this segment is the increasing need for operational efficiency, cost control, and standardized food quality across high-volume foodservice environments. Liquid butter alternatives help restaurants streamline preparation processes, reduce ingredient waste, improve product consistency, and enhance flavor delivery while maintaining profitability, particularly amid rising labor and raw material costs.Bakery and confectionery manufacturers constitute another major demand center, benefiting from the products’ ability to support large-scale production, improve processing efficiency, and deliver consistent product quality. Demand from frozen food manufacturers, snack producers, and ready-meal companies continues to increase as these industries seek versatile ingredients capable of enhancing flavor while supporting industrial-scale manufacturing requirements.Institutional catering facilities, including schools, hospitals, universities, and corporate cafeterias, are emerging as important consumers due to the products’ extended shelf life, ease of storage, favorable economics, and suitability for large-scale meal preparation. Continued growth in contract catering and organized foodservice operations is expected to further support demand across this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Liquid Butter Alternatives Market Segmentations

By Product Type

- Liquid Butter-Flavored Oils

- Liquid Margarine

- Liquid Shortening

- Plant-Based Liquid Butter Alternatives

- Blended Butter-Oil Alternatives

- Flavored Liquid Butter Alternatives

- Clean-Label Liquid Butter Alternatives

- Reduced-Fat Liquid Butter Alternatives

By Oil Base

- Soybean Oil-Based

- Canola/Rapeseed Oil-Based

- Sunflower Oil-Based

- Palm Oil-Based

- Coconut Oil-Based

- Olive Oil-Based

- Avocado Oil-Based

- Multi-Oil Blends

By Functional Application

- Frying

- Grilling & Sautéing

- Baking

- Topping & Finishing

- Popcorn Coating

- Sauce Preparation

- Ready-to-Eat Food Preparation

- Industrial Food Processing

By Formulation Type

- Conventional

- Non-Hydrogenated

- Trans-Fat-Free

- Organic

- Non-GMO

- Allergen-Free

By Distribution Channel

- Direct B2B Sales

- Foodservice Distributors

- Cash & Carry/Wholesale

- Modern Retail

- Convenience Retail

- E-Commerce

- Specialty Ingredient Suppliers

Regional Insights

North America

North America accounted for approximately 35% of global market revenue in 2025, making it the largest regional market. The United States represented nearly 29% of total global demand, supported by a mature foodservice industry, extensive quick-service restaurant networks, and a highly developed processed food manufacturing sector. Canada also contributes significantly through its bakery, institutional catering, and food processing industries.Regional market growth is primarily driven by the continued expansion of restaurant chains, increasing consumption of convenience foods, rising demand for cost-effective butter substitutes, and strong adoption of value-added cooking ingredients across commercial foodservice operations. The growing popularity of plant-based diets, clean-label food products, and trans-fat-free formulations is encouraging manufacturers to introduce healthier product variants. Furthermore, ongoing investments in food processing automation, menu innovation within quick-service restaurants, and consumer demand for consistent flavor experiences continue to strengthen market growth across North America.

Europe

Europe represented approximately 27% of global market share in 2025. Germany, the United Kingdom, France, Italy, and the Netherlands remain among the region’s largest consumers of liquid butter alternatives. The market benefits from a highly developed food processing sector, strong bakery traditions, and widespread adoption of specialty food ingredients.Growth across Europe is being driven by stringent food safety and nutritional regulations, increasing consumer preference for plant-based and sustainable food products, and growing demand for clean-label formulations. Food manufacturers throughout the region are actively reformulating products to reduce saturated fats and improve nutritional profiles while maintaining taste and functionality. Additionally, rising environmental awareness, expanding vegan food markets, and increasing investment in sustainable ingredient sourcing are supporting long-term demand for innovative liquid butter alternative products.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global demand in 2025 and is projected to be the fastest-growing regional market through 2031. China remains the largest consumer within the region, supported by rapid expansion of food processing, quick-service restaurants, and organized retail sectors. India is expected to record the highest growth rate globally, exceeding 10% CAGR, driven by increasing urbanization, rising disposable incomes, and rapid development of organized foodservice. Japan, South Korea, Australia, and Southeast Asian countries continue to generate stable demand across bakery, snack, and convenience food applications.The region’s growth is primarily fueled by rising consumption of processed and convenience foods, increasing westernization of dietary habits, rapid expansion of foodservice chains, and growing investments in food manufacturing infrastructure. Expanding middle-class populations, changing consumer lifestyles, and increasing demand for affordable flavor-enhancing ingredients are creating substantial opportunities for market participants. Additionally, the growth of modern retail channels and e-commerce food distribution platforms is further accelerating product penetration across emerging economies.

Latin America

Latin America accounted for approximately 7% of global market revenue in 2025. Brazil dominates regional demand due to its large food processing sector, extensive bakery industry, and strong domestic consumption of processed food products. Mexico continues to experience growth in restaurant chains, snack manufacturing, and processed food production, supporting increased adoption of liquid butter alternatives.Regional market expansion is being driven by increasing urbanization, rising demand for packaged and convenience foods, growth in quick-service restaurant networks, and ongoing modernization of food manufacturing operations. Cost optimization remains a critical purchasing factor for food producers, encouraging the adoption of liquid butter alternatives that provide functional and economic advantages over traditional dairy-based ingredients. Growing export-oriented food production activities across several Latin American countries are also contributing to market development.

Middle East & Africa

The Middle East and Africa region represented approximately 7% of global demand in 2025. GCC countries, including Saudi Arabia and the UAE, are leading regional growth through continued expansion of hospitality, tourism, retail foodservice, and institutional catering sectors. South Africa remains an important manufacturing and distribution hub for the broader African market.Market growth across the region is being supported by rising investments in food production infrastructure, increasing demand for processed and convenience foods, and expanding tourism-related foodservice activities. Government initiatives aimed at improving food security and enhancing domestic food manufacturing capabilities are encouraging greater utilization of value-added food ingredients. Additionally, population growth, rising disposable incomes, and increasing penetration of international restaurant brands are expected to generate sustained demand for liquid butter alternatives throughout the forecast period.

Key Players in the Liquid Butter Alternatives Market

- Cargill

- Bunge

- AAK

- Wilmar International

- Ventura Foods

- Upfield

- Conagra Brands

- Associated British Foods

- Fuji Oil Holdings

- Richardson International

- Peerless Foods

- Puratos

- Kerry Group

- Vandemoortele

- ADM