Keto Flour Market Size

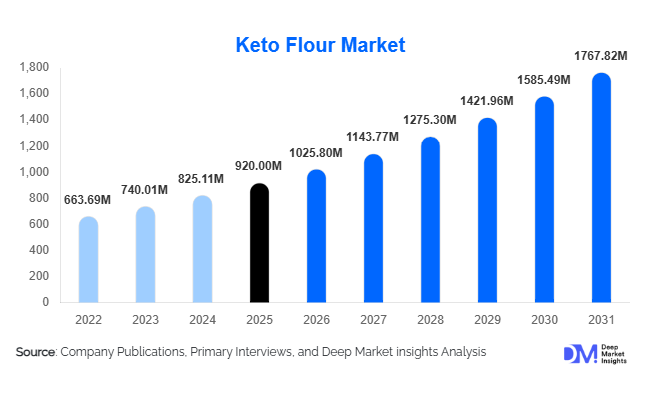

According to Deep Market Insights, the global keto flour market size was valued at approximately USD 920 million in 2025 and is projected to grow from USD 1,025.80 million in 2026 to reach USD 1767.82 million by 2031, expanding at a CAGR of 11.5% during the forecast period (2026–2031). The keto flour market growth is being driven by increasing adoption of ketogenic and low-carbohydrate diets, rising demand for gluten-free and grain-free food ingredients, and growing consumer preference for functional nutrition products that support weight management, blood sugar control, and overall metabolic health. Food manufacturers are increasingly incorporating keto flour into bakery products, snacks, meal replacements, and protein-enriched formulations to address evolving dietary preferences. Growing awareness of preventive healthcare and clean-label ingredients is further accelerating market expansion across both developed and emerging economies.

Key Market Insights

- Almond flour remains the dominant product segment, accounting for nearly 38% of global market revenue due to its superior baking functionality and consumer acceptance.

- Commercial food manufacturers are increasingly adopting keto flour blends to develop low-carbohydrate bakery products, snacks, and meal replacement solutions.

- North America dominates the global market, representing approximately 42% of total demand due to widespread keto diet adoption and advanced health-food retail infrastructure.

- Asia-Pacific is the fastest-growing regional market, supported by rising health awareness, increasing disposable incomes, and growing demand for premium nutritional foods.

- Online retail channels continue gaining market share, enabling direct-to-consumer sales and wider availability of specialty keto flour products.

- Innovation in multi-ingredient keto flour blends is improving texture, moisture retention, and protein content, expanding adoption among commercial bakeries and food manufacturers.

Keto Flour Market Latest Trends

Growing Adoption of Functional and High-Protein Flour Blends

Manufacturers are increasingly developing advanced keto flour formulations that combine almond flour, coconut flour, lupin flour, flaxseed flour, and plant-based proteins to improve nutritional value and baking performance. These blends offer enhanced protein content, improved texture, greater moisture retention, and better shelf stability compared to single-ingredient alternatives. Food manufacturers are actively seeking flour solutions that can replicate traditional wheat flour functionality while maintaining low carbohydrate levels. As a result, demand for customized keto flour blends is rising across commercial bakeries, packaged food manufacturers, and nutritional product developers. Premium blended products are also commanding higher margins and creating differentiation opportunities for suppliers operating within the rapidly evolving functional ingredients market.

Expansion of Clean-Label and Organic Keto Products

Consumer demand for transparency in food ingredients is driving significant growth in clean-label and organic keto flour products. Buyers increasingly prefer minimally processed ingredients that are free from artificial additives, preservatives, and genetically modified organisms. Organic almond flour, organic coconut flour, and certified non-GMO keto flour blends are gaining popularity among health-conscious consumers seeking natural dietary solutions. Retailers are responding by expanding shelf space dedicated to premium wellness products, while manufacturers are investing in organic certification and sustainable sourcing programs. This trend is particularly pronounced in North America and Europe, where consumers increasingly associate clean-label foods with superior quality, nutritional value, and environmental sustainability.

Keto Flour Market Drivers

Rising Popularity of Ketogenic and Low-Carbohydrate Diets

The growing global adoption of ketogenic diets remains the most significant driver of keto flour market growth. Consumers seeking effective weight-management solutions, improved metabolic health, and blood sugar regulation are increasingly incorporating keto-friendly products into their daily diets. Keto flour serves as a direct substitute for traditional grain-based flour in numerous food applications, enabling consumers to maintain dietary compliance without sacrificing food variety. Social media influence, nutrition-focused communities, and increasing healthcare awareness continue to accelerate consumer interest in low-carbohydrate lifestyles worldwide.

Growing Demand for Gluten-Free and Grain-Free Foods

The global gluten-free food industry continues to expand beyond individuals diagnosed with celiac disease. Consumers increasingly perceive gluten-free and grain-free products as healthier alternatives that support digestive wellness and overall health. Most keto flour products are naturally gluten-free, allowing manufacturers to benefit from overlapping consumer demand trends. This convergence between keto, paleo, gluten-free, and clean-eating lifestyles is creating a broader addressable market for alternative flour products and supporting long-term category growth.

Expansion of Functional Foods and Preventive Nutrition

Consumers are increasingly adopting preventive healthcare approaches that emphasize nutrition as a means of reducing long-term health risks. Keto flour aligns strongly with this trend by offering high-protein, high-fiber, low-glycemic alternatives suitable for diabetic-friendly, weight-management, and sports nutrition applications. Food manufacturers continue to launch innovative products targeting specific health outcomes, creating sustained demand for specialized flour ingredients capable of supporting functional nutrition claims.

Keto Flour Market Restraints

Volatility in Raw Material Prices

The market remains highly dependent on agricultural commodities such as almonds, coconuts, flaxseed, and specialty seeds. Weather-related disruptions, crop yield fluctuations, transportation costs, and regional supply shortages can significantly affect raw material availability and pricing. These factors contribute to higher production costs and create profitability challenges for manufacturers, particularly during periods of agricultural uncertainty.

Functional Limitations Compared to Conventional Flour

Despite significant technological improvements, many keto flours still present challenges in replicating the elasticity, structure, and texture of wheat flour. Commercial food manufacturers often require specialized formulations, binders, and processing techniques to achieve desired product quality. These additional formulation complexities increase production costs and can limit adoption among mainstream food manufacturers seeking simple ingredient substitutions.

Keto Flour Industry Key Opportunities

Expansion into Medical Nutrition and Diabetic-Friendly Foods

Increasing global prevalence of diabetes, obesity, and metabolic disorders is creating substantial opportunities for keto flour manufacturers. Healthcare professionals increasingly recommend low-glycemic dietary solutions to support blood sugar management and weight control. Keto flour is being incorporated into diabetic bakery products, meal replacement formulations, and therapeutic nutrition products designed for long-term health management. Companies capable of developing clinically supported ingredient solutions can access premium healthcare-oriented market segments with higher profit margins and stronger customer retention.

Rapid Growth Across Emerging Asia-Pacific Markets

Asia-Pacific represents one of the most attractive growth opportunities for keto flour manufacturers. Rising disposable incomes, urbanization, increasing obesity concerns, and growing consumer awareness of preventive healthcare are driving demand for premium nutritional ingredients across China, India, Australia, Japan, and Southeast Asia. Market penetration remains relatively low compared to North America and Europe, creating significant expansion potential for both domestic and international suppliers. Localized formulations using regionally preferred ingredients are expected to further accelerate adoption across the region.

Industrial Adoption of Advanced Keto Flour Blends

Commercial bakeries and packaged food manufacturers increasingly require keto flour solutions capable of delivering functionality similar to traditional wheat flour. This creates opportunities for suppliers investing in advanced flour blending technologies, texture optimization, protein enrichment, and moisture-retention improvements. Customized ingredient systems designed for industrial-scale production can command premium pricing while establishing long-term supply relationships with large food manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 920 Million |

| Market Size in 2026 | USD 1025.80 Million |

| Market Size in 2031 | USD 1767.82 Million |

| CAGR | 11.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Almond flour continues to dominate the global keto flour market, contributing approximately 38% of total revenue in 2025, driven primarily by its superior baking performance, neutral flavor profile, and strong compatibility with mainstream and specialty bakery formulations. Its leadership is further reinforced by the growing global shift toward gluten-free and low-carbohydrate diets, where almond flour serves as a direct functional replacement for wheat flour without compromising texture or sensory appeal. Coconut flour holds the second-largest share, supported by its affordability, high dietary fiber content, and strong moisture-absorbing properties, making it especially valuable in dense baked goods and clean-label formulations. Flaxseed flour is gaining traction as a functional ingredient driven by rising demand for omega-3-rich and digestive-health-oriented foods, particularly in wellness-focused product lines. Lupin flour is emerging rapidly as a high-growth specialty ingredient due to its exceptionally high protein content and strong alignment with plant-based nutrition trends, especially in premium keto bakery applications. Multi-ingredient keto flour blends are expanding at an accelerated pace as manufacturers increasingly prioritize formulation stability, improved texture, and scalability in commercial production, positioning blends as a key innovation driver in industrial keto food development.

Nature Insights

Conventional keto flour products account for approximately 78% of total market revenue, primarily driven by cost efficiency, large-scale availability, and established supply chains that support mass food manufacturing. Their dominance is reinforced by their suitability for high-volume production environments where consistency and affordability remain critical purchasing factors for industrial buyers. Organic keto flour, however, is witnessing significantly faster growth, supported by rising consumer demand for clean-label, non-GMO, and sustainably sourced food ingredients. The expansion of organic certification frameworks and increasing retail penetration of certified organic almond and coconut flour products are further strengthening this segment. Growth is particularly strong in North America and Europe, where consumers demonstrate a higher willingness to pay premium prices for organic verification and transparency in sourcing, making organic positioning a key long-term differentiation strategy for manufacturers.

Application Insights

Bread and bakery applications remain the dominant segment, accounting for approximately 34% of global demand in 2025, primarily driven by the strong consumer shift toward low-carbohydrate alternatives to traditional wheat-based bread. The growth of ketogenic and gluten-free diets has significantly increased demand for keto-compatible baking ingredients that replicate the structure and elasticity of conventional baked goods while maintaining nutritional compliance. Cookies, biscuits, cakes, and pastries are also experiencing steady expansion as manufacturers diversify product portfolios to include indulgent yet health-oriented offerings. Meal replacement products and sports nutrition formulations are among the fastest-growing application areas, driven by rising demand for convenient, protein-rich, and low-glycemic nutrition solutions that support active lifestyles and weight management goals. Additional growth opportunities are emerging in snack foods, breakfast products, coatings, and culinary applications where keto flour functions as a versatile ingredient that enhances both nutritional profile and product functionality.

Distribution Channel Insights

Supermarkets and hypermarkets continue to lead the distribution landscape, accounting for approximately 36% of global sales, supported by strong consumer trust, extensive product visibility, and the ability to offer diverse brand assortments under a single retail environment. Their dominance is further reinforced by increasing shelf space allocation for health-focused and specialty food categories. Specialty health food stores maintain strong relevance, particularly for premium, organic, and niche keto flour products, as they cater to highly informed consumers seeking curated wellness-oriented selections. Online retail channels are experiencing the fastest growth, driven by expanding digital adoption, convenience-driven purchasing behavior, and access to a wider range of specialty and international brands that are often unavailable in physical stores. Direct-to-consumer channels are also gaining momentum as manufacturers leverage digital platforms to strengthen brand loyalty, improve margin structures, and collect real-time consumer insights, making digital commerce a critical growth enabler for emerging keto flour brands.

End User Insights

Household consumers represent approximately 45% of global keto flour demand, supported by increasing adoption of home baking, personalized nutrition trends, and rising awareness of low-carbohydrate diets. This segment’s growth is largely driven by consumers seeking control over ingredient quality and dietary composition in everyday meals. Commercial bakeries remain a major institutional driver, fueled by the widespread integration of keto-friendly bread, cookies, and pastries into mainstream retail bakery offerings. Packaged food manufacturers are increasingly incorporating keto flour into snacks, frozen foods, and meal replacement products as part of broader product innovation strategies targeting health-conscious consumers. Foodservice operators are also expanding keto menu options to meet evolving dietary preferences, while health and nutrition product manufacturers represent one of the fastest-growing end-user categories, driven by strong demand for diabetic-friendly, sports nutrition, and functional wellness formulations that emphasize protein enrichment and metabolic health support.

Explore more data points, trends and opportunities Download Free Sample Report

Keto Flour Market Segmentations

By Product Type

- Almond Flour

- Coconut Flour

- Flaxseed Flour

- Sunflower Seed Flour

- Lupin Flour

- Pecan Flour

- Hazelnut Flour

- Walnut Flour

- Sesame Flour

- Chia Flour

- Pumpkin Seed Flour

- Mixed Keto Flour Blends

- Other Specialty Keto Flours

By Nature

- Conventional Keto Flour

- Organic Keto Flour

By Functional Attribute

- Gluten-Free Keto Flour

- High-Protein Keto Flour

- High-Fiber Keto Flour

- Clean-Label Keto Flour

- Non-GMO Keto Flour

- Fortified/Functional Keto Flour

By Application

- Bread & Bakery Products

- Cakes & Pastries

- Cookies & Biscuits

- Pizza Crusts & Flatbreads

- Snacks & Crackers

- Breakfast Products

- Meal Replacements & Nutrition Products

- Sauces, Coatings & Culinary Applications

- Others

By End User

- Household Consumers

- Commercial Bakeries

- Packaged Food Manufacturers

- Foodservice & Restaurants

- Health & Nutrition Product Manufacturers

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 42% of global revenue in 2025, with growth primarily driven by widespread adoption of ketogenic and low-carbohydrate diets, a highly mature functional food ecosystem, and strong consumer awareness of nutritional wellness. The United States leads regional demand due to its advanced packaged food industry, strong presence of health-focused brands, and continuous product innovation in keto-friendly bakery and snack categories. The region’s growth is further supported by rising obesity rates, increasing participation in fitness-oriented lifestyles, and strong penetration of e-commerce and direct-to-consumer health food brands, all of which contribute to sustained demand for keto flour ingredients across both retail and industrial channels. Canada also contributes meaningfully, supported by growing consumer interest in gluten-free, clean-label, and natural food products.

Europe

Europe accounts for approximately 28% of global market demand, with growth driven by strong consumer preference for organic, clean-label, and allergen-free food products, alongside a well-established regulatory framework that emphasizes ingredient transparency and food safety. Countries such as Germany, the United Kingdom, France, Italy, Spain, and the Netherlands lead regional consumption, supported by high awareness of preventive healthcare and increasing adoption of plant-based and low-carb dietary lifestyles. The region’s growth is also reinforced by premiumization trends, where consumers are willing to pay higher prices for certified organic and sustainably sourced keto flour products. Germany and the United Kingdom collectively account for a significant share of regional demand due to their strong health food retail infrastructure and early adoption of functional nutrition trends.

Asia-Pacific

Asia-Pacific holds approximately 18% of global market share and is the fastest-growing regional market, with projected growth exceeding 14% annually, driven by rapid urbanization, rising disposable incomes, and increasing awareness of diet-related health issues such as obesity and diabetes. Countries including China, India, Japan, South Korea, and Australia are key contributors to regional expansion, supported by growing exposure to Western dietary patterns and the rapid development of e-commerce-based food retail ecosystems. India is expected to emerge as the fastest-growing market due to increasing health consciousness among urban populations and rising demand for low-carbohydrate alternatives, while China continues to expand rapidly through premium health food consumption and strong digital retail penetration. The region’s growth is further supported by localized product innovation tailored to diverse culinary preferences and nutritional needs.

Latin America

Latin America represents approximately 7% of global demand, with growth primarily driven by increasing urbanization, expanding middle-class populations, and rising awareness of functional and health-oriented nutrition. Brazil and Mexico serve as the primary markets, supported by growing investments in modern retail infrastructure and increasing availability of premium health food products. The region’s expansion is further supported by rising demand for weight management solutions and improved dietary awareness among younger consumers, which is gradually shifting consumption patterns toward low-carb and nutrient-dense food alternatives. Premium bakery products and functional food innovations are emerging as key growth avenues across urban centers.

Middle East & Africa

The Middle East and Africa region accounts for approximately 5% of global market demand, with growth strongly influenced by rising prevalence of lifestyle-related diseases such as diabetes and obesity, particularly in Gulf Cooperation Council countries. The United Arab Emirates, Saudi Arabia, and South Africa represent the largest contributors to regional consumption, supported by increasing demand for premium imported health foods and expanding retail modernization. Growth is also driven by increasing consumer preference for clean-label and halal-certified products that align with regional dietary and cultural requirements. Expanding supermarket chains, growing health awareness, and government-led wellness initiatives are expected to further strengthen long-term demand for keto flour products across the region.

Key Players in the Keto Flour Market

- Blue Diamond Growers

- Bob's Red Mill Natural Foods

- King Arthur Baking Company

- BetterBody Foods

- Nature's Eats

- Otto's Naturals

- Anthony's Goods

- Nutiva

- Swerve

- Ardent Mills

- LiveKuna

- Healthworks

- Honeyville

- Terrasoul Superfoods

- Bajo Foods