Injectable Cocoa Fillings Market Size

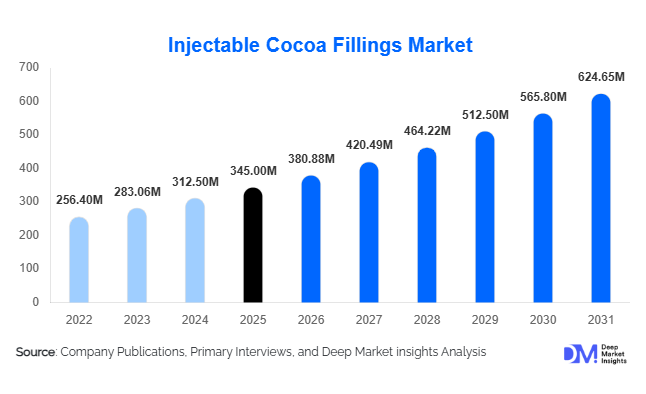

According to Deep Market Insights, the global injectable cocoa fillings market size was valued at approximately USD 345 million in 2025 and is projected to grow from USD 380.88 million in 2026 to reach USD 624.65 million by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The injectable cocoa fillings market growth is primarily driven by increasing demand for premium filled confectionery products, expansion of industrial bakery manufacturing, rising consumption of indulgent desserts, and growing adoption of automated filling technologies across food processing facilities. Injectable cocoa fillings are increasingly being used in chocolates, pastries, doughnuts, croissants, frozen desserts, and ready-to-eat snacks due to their superior texture, flavor consistency, and processing efficiency. Manufacturers are also introducing clean-label, low-sugar, organic, and plant-based cocoa filling formulations to align with evolving consumer preferences and regulatory requirements. As premiumization continues to influence global confectionery and bakery consumption, injectable cocoa fillings are becoming a critical ingredient category for product differentiation and value-added innovation.

Key Market Insights

- Chocolate confectionery remains the largest application segment, accounting for nearly 58% of global injectable cocoa fillings demand due to strong consumption of filled chocolates, pralines, and truffles.

- Industrial food manufacturers represent the largest end-user group, contributing approximately 47% of market demand through large-scale bakery and confectionery production.

- Europe dominates the global market, supported by established chocolate manufacturing industries in Germany, Belgium, Switzerland, France, and Italy.

- Asia-Pacific is the fastest-growing regional market, driven by rapid expansion of organized bakery chains, café culture, and premium confectionery consumption.

- Clean-label and vegan cocoa fillings are witnessing accelerated adoption, particularly in North America and Europe, as consumers seek healthier and more transparent ingredient formulations.

- Automation in bakery and confectionery manufacturing is increasing demand for highly stable injectable fillings compatible with high-speed filling systems.

- Premiumization trends in desserts and snack products are encouraging manufacturers to develop innovative cocoa filling textures, flavors, and nutritional profiles.

Injectable Cocoa Fillings Market Latest Trends

Premium Filled Confectionery Driving Product Innovation

The premium confectionery segment is becoming a major innovation hub within the injectable cocoa fillings market. Consumers are increasingly seeking indulgent chocolate products featuring multiple textures, rich cocoa flavors, and premium ingredient positioning. This has encouraged manufacturers to develop specialized injectable fillings with enhanced cocoa content, unique flavor combinations, and superior mouthfeel characteristics. Premium truffles, pralines, filled chocolate bars, and artisanal confectionery products are increasingly utilizing injectable cocoa fillings to create differentiated sensory experiences. Manufacturers are also introducing single-origin cocoa variants and gourmet flavor pairings such as cocoa-hazelnut, cocoa-caramel, and cocoa-fruit combinations to cater to evolving consumer preferences.

Clean-Label and Plant-Based Fillings Gaining Momentum

Growing demand for healthier indulgence is accelerating the adoption of clean-label and plant-based injectable cocoa fillings. Food manufacturers are reformulating products to eliminate artificial additives, synthetic emulsifiers, and excessive sugar content while maintaining desirable texture and shelf stability. Vegan cocoa fillings utilizing plant-derived ingredients are becoming increasingly popular across bakery and confectionery applications. Reduced-sugar formulations, organic certifications, and sustainability-focused sourcing programs are emerging as important differentiators. This trend is particularly strong in Europe and North America, where consumers increasingly scrutinize ingredient labels and seek transparency regarding sourcing and production practices.

Injectable Cocoa Fillings Market Drivers

Growing Demand for Premium Chocolate and Bakery Products

Global demand for premium confectionery and bakery products continues to rise as consumers seek indulgent food experiences and high-quality ingredients. Filled chocolates, gourmet pastries, artisanal doughnuts, and specialty desserts are increasingly incorporating injectable cocoa fillings to enhance product differentiation. Premium products command higher retail prices and generate stronger profit margins for manufacturers, encouraging greater adoption of advanced filling technologies and specialized cocoa formulations. Rising disposable incomes in emerging markets are further supporting premium confectionery consumption.

Expansion of Industrial Bakery Manufacturing

The rapid growth of industrial bakery production is significantly contributing to market expansion. Large-scale bakeries require fillings that can maintain consistency, stability, and processing efficiency under automated production conditions. Injectable cocoa fillings provide manufacturers with reliable solutions for high-volume production while ensuring uniform product quality. Increasing consumption of packaged bakery products, convenience foods, and ready-to-eat snacks continues to strengthen demand from industrial food manufacturers globally.

Growth of Foodservice and Café Chains

The expansion of café chains, quick-service restaurants, and foodservice operators has created additional demand for injectable cocoa fillings. Premium pastries, croissants, filled muffins, doughnuts, and dessert offerings have become important menu items for foodservice establishments seeking to increase customer spending and product differentiation. Emerging markets across Asia-Pacific, the Middle East, and Latin America are witnessing particularly strong growth in café culture, generating new demand opportunities for filling manufacturers.

Injectable Cocoa Fillings Market Restraints

Cocoa Price Volatility and Supply Risks

The injectable cocoa fillings industry remains vulnerable to fluctuations in cocoa bean prices. Production is highly dependent on cocoa supplies originating from major producing countries such as Côte d’Ivoire and Ghana. Weather disruptions, disease outbreaks, geopolitical developments, and supply chain challenges can significantly impact cocoa availability and pricing. Rising cocoa costs place pressure on manufacturers' margins and may limit product affordability in price-sensitive markets.

Competition from Alternative Filling Ingredients

Injectable cocoa fillings face competition from alternative filling categories including fruit fillings, caramel fillings, dairy creams, nut-based fillings, and flavored syrups. Food manufacturers often evaluate filling options based on cost, functionality, consumer preferences, and product positioning. In certain bakery and dessert applications, alternative fillings may provide more economical solutions, limiting cocoa filling penetration. Continuous innovation and value-added formulation development are therefore essential to maintain competitive advantage.

Injectable Cocoa Fillings Industry Key Opportunities

Expansion of Plant-Based and Functional Confectionery Products

The growing popularity of plant-based food products presents significant opportunities for injectable cocoa filling manufacturers. Vegan chocolates, dairy-free pastries, and functional snack products are gaining widespread consumer acceptance across developed and emerging markets. Manufacturers capable of developing high-performance plant-based cocoa fillings with clean-label attributes and enhanced nutritional profiles can capture growing demand from health-conscious consumers. Functional ingredients such as protein enrichment, fiber fortification, and sugar reduction technologies further expand product development opportunities.

Rapid Growth of Asia-Pacific Bakery and Café Industries

Asia-Pacific represents one of the most attractive growth opportunities for market participants. Countries including China, India, Indonesia, Vietnam, Thailand, and the Philippines are experiencing rapid growth in organized bakery chains, specialty cafés, and premium dessert consumption. Rising urbanization, increasing disposable incomes, and westernization of food preferences are creating favorable conditions for injectable cocoa filling adoption. Localized manufacturing facilities, technical application centers, and strategic partnerships with regional food producers can help suppliers capitalize on this expanding demand base.

Premiumization and Artisanal Product Development

Artisanal bakers, specialty chocolatiers, and premium dessert manufacturers are increasingly seeking differentiated ingredient solutions that enhance product quality and brand positioning. Injectable cocoa fillings designed for gourmet applications offer manufacturers opportunities to capture higher margins while addressing growing demand for premium food experiences. Custom flavor development, sustainable cocoa sourcing, and texture innovation are expected to play key roles in future market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 345.00 Million |

| Market Size in 2026 | USD 380.88 Million |

| Market Size in 2031 | USD 624.65 Million |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Liquid injectable cocoa fillings account for approximately 54% of global market demand, making them the leading product form segment within the injectable cocoa fillings market. Their dominant position is primarily driven by superior flowability, consistent viscosity characteristics, and seamless compatibility with high-speed automated production lines used across large-scale confectionery, bakery, and dessert manufacturing facilities. Food processors increasingly favor liquid formulations because they enable precise dosing, reduce production waste, improve operational efficiency, and ensure uniform product quality across large production batches. The growing adoption of industrial automation and advanced filling technologies across the global food processing sector continues to strengthen demand for liquid injectable cocoa fillings.Paste-based injectable cocoa fillings remain particularly important in premium confectionery applications where richer texture profiles, higher cocoa concentrations, and differentiated sensory attributes are desired. Premium chocolate manufacturers increasingly utilize paste formulations to create luxurious filled chocolates, pralines, and specialty confectionery products that command higher margins. Meanwhile, aerated, mousse-like, and ganache-style injectable fillings are witnessing increasing adoption among artisanal chocolatiers and premium dessert producers seeking to differentiate their offerings through innovative textures and premium flavor experiences. Continuous investments in rheology optimization, ingredient functionality enhancement, and filling stability technologies are further expanding application opportunities across all product forms.

Cocoa Composition Insights

Milk cocoa fillings represent the largest composition segment, accounting for approximately 39% of the global market. The segment's leadership is primarily driven by broad consumer acceptance, balanced flavor characteristics, and extensive applicability across chocolates, pastries, cakes, biscuits, frozen desserts, and snack products. Milk cocoa fillings provide the familiar taste profile preferred by a large proportion of consumers globally, making them the preferred choice for mass-market and premium product manufacturers alike. Their versatility across multiple food categories continues to reinforce segment dominance.White cocoa fillings continue to maintain strong demand within specialty confectionery applications, seasonal product launches, and premium bakery offerings where visual appeal and flavor differentiation are important. Additionally, blended formulations that combine milk and dark chocolate characteristics are gaining traction among manufacturers seeking customized taste profiles and broader consumer appeal. High-cocoa solids fillings are also benefiting from rising demand for premium, authentic, and gourmet chocolate products, further contributing to market diversification and innovation.

Application Insights

Chocolate confectionery remains the largest application segment, accounting for nearly 58% of global injectable cocoa fillings consumption. The segment's leadership is primarily driven by sustained consumer demand for premium filled chocolates, pralines, truffles, chocolate bars, bonbons, and specialty confectionery products. Injectable cocoa fillings enable manufacturers to create differentiated flavor combinations, premium textures, and value-added product offerings, making them a critical ingredient within modern chocolate manufacturing. Growing consumer willingness to pay premium prices for indulgent and innovative confectionery products continues to support segment expansion.Bakery applications represent the second-largest market segment and continue to experience strong growth due to increasing demand for filled doughnuts, croissants, pastries, muffins, cakes, cookies, and other premium baked goods. The rapid expansion of café chains, specialty bakeries, and convenience-oriented bakery formats globally is creating substantial opportunities for injectable cocoa filling suppliers. Manufacturers increasingly utilize advanced filling technologies to enhance product freshness, improve flavor consistency, and create premium bakery experiences.Dairy desserts, including ice cream, frozen desserts, yogurt products, mousses, and puddings, are increasingly incorporating injectable cocoa fillings to improve taste, visual appeal, and texture differentiation. The growing popularity of indulgent desserts and premium dairy innovations continues to stimulate demand in this segment. Additionally, snack products, ready-to-eat desserts, and convenience-oriented food offerings are emerging as high-growth applications as food manufacturers respond to changing consumer lifestyles and increasing demand for portable indulgent products.

Distribution Channel Insights

Direct B2B sales dominate the injectable cocoa fillings market and account for approximately 68% of total market revenues. The leading position of this distribution channel is driven by the industry's highly specialized procurement structure, where large food manufacturers establish long-term supply agreements with ingredient producers to ensure consistent product quality, formulation customization, technical support, and supply chain reliability. Direct procurement arrangements also enable manufacturers to optimize production efficiency, maintain strict quality standards, and secure stable ingredient availability.Ingredient distributors play a critical role in expanding market penetration, particularly among small and medium-sized food manufacturers that may not procure directly from large ingredient suppliers. These distributors provide technical expertise, localized inventory management, and broader product accessibility across regional markets. Foodservice suppliers further support market growth by serving bakery chains, restaurants, cafés, hotels, and dessert operators requiring specialized filling solutions tailored to specific applications.The emergence of digital ingredient procurement platforms and e-commerce channels is gradually transforming market accessibility. Online ingredient marketplaces provide artisanal bakers, specialty chocolatiers, and smaller food businesses with convenient access to premium injectable cocoa fillings, product specifications, formulation guidance, and technical documentation, thereby supporting broader market participation and innovation.

End-User Insights

Industrial food manufacturers account for approximately 47% of global market demand, making them the largest end-user segment in the injectable cocoa fillings market. The segment's dominance is primarily driven by large-scale production requirements across confectionery, bakery, frozen dessert, snack, and convenience food categories. These manufacturers rely heavily on injectable cocoa fillings to improve product differentiation, enhance sensory appeal, and develop innovative premium offerings while maintaining production efficiency and consistency across extensive manufacturing operations.Bakery chains represent one of the fastest-growing end-user categories as café culture, premium bakery concepts, and on-the-go consumption trends continue expanding worldwide. Artisanal bakers and specialty chocolatiers are increasingly utilizing customized injectable fillings to create handcrafted premium products that cater to consumers seeking unique and high-quality indulgent experiences. Foodservice operators, quick-service restaurants, hotels, and dessert chains are also incorporating filled pastries, cakes, and desserts into their menus, further supporting market growth across commercial foodservice channels.

Explore more data points, trends and opportunities Download Free Sample Report

Injectable Cocoa Fillings Market Segmentations

By Product Form

- Liquid Injectable Cocoa Fillings

- Semi-Liquid Cocoa Cream Fillings

- Paste-Based Cocoa Fillings

- Aerated Cocoa Fillings

- Ganache-Type Injectable Fillings

By Cocoa Composition

- Dark Cocoa Fillings

- Milk Cocoa Fillings

- White Cocoa Fillings

- Blended Cocoa Fillings

- High-Cocoa Solids Fillings

By Functional Characteristics

- Standard Fillings

- Bake-Stable Fillings

- Freeze-Thaw Stable Fillings

- Heat-Resistant Fillings

- Low-Sugar Fillings

- Sugar-Free Fillings

- Organic Fillings

- Clean-Label Fillings

- Vegan Fillings

By Application

- Chocolate Confectionery

- Bakery Products

- Dairy Desserts

- Snack Products

- Ready-to-Eat Desserts

By End User

- Industrial Food Manufacturers

- Bakery Chains

- Chocolate Manufacturers

- Artisanal Bakers & Chocolatiers

- Foodservice Operators

- Quick-Service Restaurants (QSRs)

Regional Insights

Europe

Europe accounts for approximately 36% of the global injectable cocoa fillings market, making it the largest regional market worldwide. Germany, Belgium, France, Italy, Switzerland, and the Netherlands serve as major production and consumption centers due to their long-established chocolate manufacturing traditions, advanced bakery industries, and strong presence of leading confectionery brands. The region benefits from a mature premium chocolate culture, high per-capita confectionery consumption, and continuous product innovation across both artisanal and industrial food sectors. Belgium alone contributes nearly 8% of global demand, reflecting its strategic importance within the global chocolate industry.Regional growth is primarily driven by increasing demand for premium and gourmet confectionery products, rising consumer preference for filled chocolates and specialty desserts, ongoing innovation in bakery and snack categories, and strong adoption of premium cocoa-based ingredients. Additionally, growing consumer interest in artisanal products, clean-label formulations, premium indulgence, and high-cocoa-content confectionery continues to create opportunities for advanced injectable filling solutions throughout the region.

North America

North America represents approximately 27% of global market demand, with the United States accounting for nearly 22% of worldwide consumption. The region maintains a strong market position due to its highly developed confectionery, bakery, snack, and convenience food industries. Demand for premium bakery products, filled snack items, gourmet desserts, and innovative confectionery products continues to support market expansion across both retail and foodservice sectors.Key growth drivers in North America include increasing consumer preference for premium indulgent foods, growing demand for innovative chocolate-filled snacks, expansion of specialty bakery chains, rising consumption of ready-to-eat desserts, and continued investment in food product innovation. Clean-label product development, premium chocolate consumption, and demand for customized flavor experiences are further encouraging manufacturers to incorporate advanced injectable cocoa filling solutions into new product launches. Canada contributes additional growth through its specialty confectionery manufacturing sector and expanding premium bakery market.

Asia-Pacific

Asia-Pacific accounts for approximately 25% of the global market and represents the fastest-growing regional segment, with forecast growth exceeding 12% annually. China, India, Japan, South Korea, Indonesia, Thailand, and other emerging economies are witnessing rapid expansion in confectionery and bakery consumption as urbanization, rising disposable incomes, and changing dietary preferences reshape regional food markets. China contributes nearly 9% of global demand, while India is emerging as one of the fastest-growing national markets due to rapid expansion of organized bakery chains, cafés, and premium dessert outlets.Regional growth is being driven by expanding middle-class populations, increasing westernization of food consumption habits, rising demand for premium confectionery products, growing penetration of international bakery and café brands, and rapid development of modern retail infrastructure. Furthermore, increasing consumer exposure to global dessert trends through social media, rising demand for convenience foods, and expanding investments by multinational food manufacturers are accelerating adoption of injectable cocoa fillings across diverse applications throughout the region.

Latin America

Latin America contributes approximately 7% of global market revenues, led by Brazil and Mexico. The region is benefiting from steady expansion of the bakery and confectionery sectors, increasing urbanization, and growing consumer demand for packaged food products. Rising availability of premium chocolate products and greater penetration of modern retail channels are creating favorable conditions for market growth.Key regional growth drivers include expanding middle-class populations, increasing consumption of packaged confectionery and baked goods, growing investment in food manufacturing capacity, and rising demand for affordable premium food products. The strengthening presence of international ingredient suppliers and confectionery manufacturers, coupled with expanding distribution networks and product innovation activities, is further supporting market development across Latin America.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of global market demand. The United Arab Emirates, Saudi Arabia, South Africa, and Egypt represent key consumption markets supported by growing retail modernization and increasing demand for premium food products. Although currently representing a smaller share of global demand, the region offers significant long-term growth potential due to improving consumer purchasing power and evolving food consumption patterns.Regional growth is primarily driven by increasing premium confectionery imports, rapid expansion of modern retail formats, rising investments in foodservice and hospitality sectors, growing tourism activity, and increasing demand for premium bakery and dessert products. Gulf Cooperation Council countries remain particularly attractive due to high disposable incomes, strong gifting culture associated with premium chocolates, and continued development of luxury retail and foodservice infrastructure. In Africa, expanding urban populations, improving retail access, and increasing investment in food processing industries are expected to create additional opportunities for injectable cocoa filling manufacturers over the forecast period.

Key Players in the Injectable Cocoa Fillings Market

- Barry Callebaut

- Puratos

- Cargill

- ADM

- AAK

- AGRANA

- Zentis

- Dawn Foods

- Irca Group

- Fuji Oil

- Ingredion

- Tate & Lyle

- Bunge

- Alpezzi

- Norte Eurocao