Hydrogenated Olive Oil Market Size

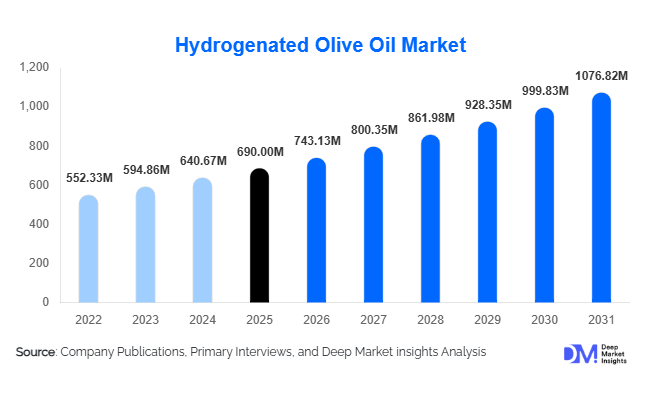

According to Deep Market Insights, the global hydrogenated olive oil market size was valued at USD 690 million in 2025 and is projected to grow from USD 743.13 million in 2026 to reach USD 1,076.82 million by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The hydrogenated olive oil market growth is primarily driven by increasing demand for natural and bio-based ingredients across cosmetics, pharmaceuticals, specialty food processing, and industrial applications. The ingredient’s superior oxidative stability, improved shelf life, enhanced texture-modifying properties, and compatibility with premium formulations have positioned it as a preferred alternative to conventional hydrogenated vegetable oils and synthetic emollients.Hydrogenated olive oil is increasingly being utilized as a structuring agent, emollient, pharmaceutical excipient, and specialty fat ingredient across high-value applications. Growing consumer preference for sustainable, plant-derived ingredients, coupled with regulatory pressure to reduce reliance on petroleum-derived compounds, is creating favorable market conditions. The cosmetics and personal care industry remains the largest consumer segment, while pharmaceutical applications are emerging as one of the fastest-growing areas due to increasing demand for lipid-based drug delivery systems and topical formulations.

Key Market Insights

- Cosmetics and personal care applications account for approximately 42% of global market demand, supported by rising adoption in skincare, haircare, lip care, and premium beauty formulations.

- Europe dominates the global hydrogenated olive oil market, benefiting from strong olive oil production capabilities, established cosmetic ingredient manufacturing, and advanced pharmaceutical industries.

- Asia-Pacific is the fastest-growing regional market, driven by expanding beauty product manufacturing, pharmaceutical production, and increasing demand for natural ingredients across China, India, Japan, and South Korea.

- Fully hydrogenated olive oil remains the leading product category, accounting for nearly 48% of global market revenue due to superior stability and compliance with trans-fat regulations.

- Pharmaceutical-grade hydrogenated olive oil adoption is accelerating, particularly in topical drug delivery systems, ointments, and controlled-release formulations.

- Sustainability certifications, traceability programs, and organic ingredient sourcing are becoming increasingly important purchasing criteria among global manufacturers.

Hydrogenated Olive Oil Market Latest Trends

Growing Adoption of Natural and Sustainable Cosmetic Ingredients

The global cosmetics industry is increasingly shifting toward plant-derived and sustainable ingredients, significantly benefiting the hydrogenated olive oil market. Major beauty brands are replacing petroleum-derived waxes, silicones, and synthetic emollients with bio-based alternatives that align with clean-label and environmentally responsible product positioning. Hydrogenated olive oil provides excellent moisturizing properties, formulation stability, and favorable sensory characteristics, making it highly attractive for premium skincare and cosmetic products. The trend is particularly strong across Europe, North America, Japan, and South Korea, where consumers actively seek vegan, cruelty-free, and sustainable beauty products. Manufacturers are increasingly investing in certified organic and traceable olive-derived ingredients to meet evolving consumer expectations and regulatory requirements.

Expansion of Pharmaceutical Excipient Applications

Hydrogenated olive oil is gaining prominence within pharmaceutical manufacturing due to its compatibility with active pharmaceutical ingredients and its ability to improve formulation stability. Pharmaceutical companies are increasingly incorporating the ingredient into ointments, creams, topical treatments, and controlled-release drug delivery systems. Growing demand for dermatological products, wound care treatments, and topical therapies is creating new opportunities for pharmaceutical-grade hydrogenated olive oil suppliers. Investments in GMP-compliant production facilities and specialty excipient development are further strengthening adoption. As healthcare expenditure and pharmaceutical production continue to expand globally, particularly across Asia-Pacific markets, this trend is expected to contribute significantly to long-term market growth.

Hydrogenated Olive Oil Market Drivers

Rising Demand from Cosmetics and Personal Care Industry

The rapid expansion of the global beauty and personal care industry is one of the most significant drivers supporting hydrogenated olive oil demand. The ingredient serves multiple functions including moisturization, texture enhancement, thickening, and stabilization. Premium skincare products increasingly incorporate hydrogenated olive oil due to its natural origin and compatibility with sensitive skin formulations. Growing consumer expenditure on anti-aging products, natural cosmetics, and premium skincare solutions continues to support sustained demand. The rise of clean beauty brands and growing preference for naturally sourced ingredients are further accelerating market penetration across developed and emerging economies.

Shift Toward Plant-Based Specialty Ingredients

Manufacturers across multiple industries are actively transitioning toward plant-based raw materials as sustainability initiatives gain momentum globally. Hydrogenated olive oil offers an attractive alternative to petroleum-derived ingredients and synthetic waxes while delivering comparable performance characteristics. This trend is particularly evident in personal care, pharmaceuticals, and specialty chemicals where sustainability objectives increasingly influence purchasing decisions. Corporate environmental commitments, consumer awareness regarding ingredient transparency, and stricter environmental regulations are collectively encouraging greater adoption of olive-derived specialty ingredients.

Hydrogenated Olive Oil Market Restraints

Volatility in Olive Oil Supply and Raw Material Pricing

The hydrogenated olive oil market remains heavily dependent on olive oil production across Mediterranean countries such as Spain, Italy, Greece, and Turkey. Climatic fluctuations, drought conditions, water shortages, and harvest disruptions can significantly impact olive oil availability and pricing. Raw material cost volatility directly affects manufacturer profitability and pricing competitiveness, particularly for smaller market participants operating under long-term supply agreements. Such uncertainties can constrain production planning and create challenges in maintaining stable supply chains.

Regulatory Scrutiny Surrounding Hydrogenated Oils

Although fully hydrogenated olive oil generally avoids trans-fat concerns associated with partially hydrogenated oils, regulatory scrutiny surrounding hydrogenated ingredients continues to influence market perception. Manufacturers must invest in product testing, quality certifications, ingredient transparency initiatives, and compliance programs to address customer concerns and meet evolving regulatory standards. Compliance costs can increase operational expenditures, particularly in highly regulated markets such as North America and Europe.

Hydrogenated Olive Oil Industry Key Opportunities

Expansion of Premium Clean Beauty Formulations

The clean beauty movement presents substantial growth opportunities for hydrogenated olive oil suppliers. Premium skincare manufacturers increasingly seek multifunctional natural ingredients capable of replacing synthetic alternatives while maintaining product performance. Hydrogenated olive oil offers strong positioning as a sustainable emollient, stabilizer, and texture-enhancing ingredient. Suppliers capable of offering COSMOS-certified, organic-certified, and sustainably sourced products are expected to capture significant premium-market opportunities. Growing demand for vegan and environmentally friendly cosmetics across Europe, North America, and Asia-Pacific further strengthens this opportunity.

Growth in Pharmaceutical Excipient Manufacturing

Expanding pharmaceutical production across emerging economies creates significant opportunities for pharmaceutical-grade hydrogenated olive oil. The ingredient's use in topical formulations, controlled-release systems, and specialty excipients continues to expand as pharmaceutical companies seek stable and biocompatible ingredients. Rapid growth in dermatological products, wound care applications, and advanced drug delivery systems is expected to drive future demand. Suppliers investing in GMP-compliant production capabilities and pharmaceutical certifications are likely to benefit from attractive margins and long-term customer relationships.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 690.00 Million |

| Market Size in 2026 | USD 743.13 Million |

| Market Size in 2031 | USD 1076.82 Million |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global hydrogenated olive oil market is segmented into fully hydrogenated olive oil, interesterified hydrogenated olive oil, and hydrogenated olive oil blends. Among these, fully hydrogenated olive oil accounted for approximately 48% of global market revenue in 2025, making it the leading product segment. The segment’s dominance is primarily driven by its superior oxidative stability, enhanced resistance to rancidity, extended shelf life, and excellent functional performance across a broad range of industrial applications. Fully hydrogenated olive oil also aligns with increasingly stringent global trans-fat regulations, making it a preferred ingredient for manufacturers seeking stable and compliant formulations. Its widespread utilization in cosmetics, pharmaceuticals, specialty fats, and personal care formulations continues to strengthen market demand. In addition, the growing emphasis on formulation consistency, ingredient reliability, and long-term storage stability among manufacturers remains a key driver supporting segment growth. Interesterified hydrogenated olive oil is gaining significant traction in premium food and specialty nutrition applications due to its improved textural properties and favorable regulatory profile. Meanwhile, hydrogenated olive oil blends are witnessing steady adoption as manufacturers increasingly seek customized ingredient solutions that balance performance, cost efficiency, and application-specific functionality.

Purity Grade Insights

Based on purity grade, the market is categorized into high-purity hydrogenated olive oil (≥99%), standard purity grades, and industrial-grade variants. High-purity hydrogenated olive oil accounted for approximately 57% of global market revenue in 2025, establishing itself as the dominant segment. The segment benefits from increasing demand across pharmaceutical, dermaceutical, and premium cosmetic applications where stringent quality requirements, product uniformity, and regulatory compliance are critical purchasing criteria. The growing adoption of hydrogenated olive oil as an excipient, stabilizer, emollient, and formulation enhancer in pharmaceutical and personal care products continues to drive demand for high-purity grades. Furthermore, rising consumer preference for premium skincare products, clean-label formulations, and naturally derived ingredients is encouraging manufacturers to utilize higher-grade raw materials. Standard purity grades continue to maintain a substantial presence in food processing and specialty industrial applications where cost-performance balance remains important. Industrial-grade hydrogenated olive oil remains concentrated in lower-value chemical processing, lubricants, and specialty industrial formulations. However, the increasing global focus on product quality, traceability, and regulatory compliance is expected to further strengthen the market position of high-purity grades throughout the forecast period.

Physical Form Insights

The market is segmented by physical form into solid and wax forms, semi-solid butter forms, flakes, pellets, and other specialty formats. Solid and wax-form hydrogenated olive oil held approximately 45% of global market demand in 2025, making it the leading physical form segment. The segment's growth is driven by its excellent structuring capabilities, superior stability, and versatility across a wide range of cosmetic and personal care applications. Wax forms are extensively utilized in lip balms, creams, ointments, moisturizers, deodorants, and skincare products where consistency, texture enhancement, and long-lasting stability are essential. The increasing demand for premium beauty products and naturally derived formulation ingredients continues to support segment expansion. Semi-solid butter forms are witnessing rising adoption in luxury skincare and haircare applications owing to their rich sensory attributes and moisturizing properties. Meanwhile, flake and pellet formats are gaining popularity among industrial processors due to improved handling efficiency, simplified storage requirements, reduced processing losses, and enhanced formulation flexibility. Growing investments in advanced personal care formulations and specialty pharmaceutical products are expected to sustain strong demand across all physical form categories.

Application Insights

By application, the hydrogenated olive oil market is segmented into cosmetics and personal care, pharmaceuticals, food and beverages, and industrial applications. Cosmetics and personal care accounted for approximately 42% of total market value in 2025, making it the largest application segment. The segment’s leadership is driven by the increasing incorporation of naturally derived emollients, stabilizers, and texture-enhancing ingredients in skincare, haircare, anti-aging products, lip care formulations, and color cosmetics. Growing consumer preference for clean beauty products, sustainable ingredients, and premium skincare solutions continues to accelerate adoption across global beauty markets. The ingredient's ability to improve product texture, moisturization, stability, and shelf life further supports widespread utilization. Pharmaceutical applications represent the fastest-growing segment, supported by expanding use in ointments, topical drug delivery systems, controlled-release formulations, and medicinal creams. Food and beverage applications continue to generate considerable demand through bakery shortenings, confectionery fillings, specialty fats, and premium spreads where stability and functionality are critical. Industrial applications, including lubricants, candles, coatings, and oleochemical derivatives, provide additional opportunities as manufacturers increasingly seek renewable and plant-based alternatives to conventional ingredients.

Distribution Channel Insights

The market is distributed through direct business-to-business (B2B) sales channels, specialty ingredient distributors, contract manufacturing partnerships, and digital procurement platforms. Direct B2B supply channels accounted for nearly 61% of global hydrogenated olive oil sales in 2025, making them the leading distribution channel. The segment’s dominance is attributed to the highly technical nature of hydrogenated olive oil applications, which often require customized specifications, quality assurance protocols, and long-term procurement agreements. Large pharmaceutical, cosmetic, and food manufacturers typically prefer direct sourcing relationships to ensure consistent supply, regulatory compliance, and product traceability. The growing demand for customized ingredient solutions and strategic supplier partnerships continues to strengthen direct procurement channels globally. Specialty ingredient distributors remain essential for reaching regional manufacturers and small-to-medium formulation companies that require flexible purchasing arrangements and technical support. Contract manufacturing partnerships are expanding as brands increasingly outsource production activities to improve operational efficiency and accelerate product development. Additionally, digital procurement platforms are emerging as supplementary sourcing channels, particularly among mid-sized industrial buyers seeking greater transparency, supply chain efficiency, and streamlined purchasing processes.

End-Use Industry Insights

Based on end-use industry, the market is segmented into cosmetics and personal care manufacturers, pharmaceutical manufacturers, food processing companies, and specialty chemical producers. Cosmetics and personal care manufacturers represented approximately 40% of overall market demand in 2025, making them the largest end-use industry segment. Growth within the segment is primarily driven by the global shift toward sustainable, naturally derived, and plant-based ingredients in beauty and personal care formulations. Rising consumer spending on premium skincare products, anti-aging solutions, and clean-label cosmetics continues to create strong demand for hydrogenated olive oil across international markets. The ingredient’s multifunctional properties, including emolliency, stabilization, and texture enhancement, further reinforce its widespread adoption among cosmetic manufacturers. Pharmaceutical manufacturers constitute the fastest-growing end-use segment, with forecast growth exceeding 8.5% annually through 2031. Increasing pharmaceutical research activities, expanding topical drug production, and rising healthcare expenditures are supporting demand across this sector. Food processing companies continue utilizing hydrogenated olive oil in specialty fat formulations and premium food products, while specialty chemical manufacturers employ the ingredient in niche industrial applications. Furthermore, export-oriented beauty product manufacturers across South Korea, Japan, Europe, and North America are contributing significantly to global market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Hydrogenated Olive Oil Market Segmentations

By Product Type

- Fully Hydrogenated Olive Oil

- Partially Hydrogenated Olive Oil

- Interesterified Hydrogenated Olive Oil

- Hydrogenated Olive Oil Blends

By Purity Grade

- High Purity

- Standard Purity

- Industrial Grade

By Physical Form

- Solid/Wax Form

- Semi-Solid Butter Form

- Flake/Pellet Form

- Liquid Modified Form

By Application

- Cosmetics & Personal Care

- Pharmaceuticals

- Food & Beverage

- Industrial Applications

By Distribution Channel

- Direct B2B Supply

- Specialty Ingredient Distributors

- Contract Manufacturers

- Online Industrial Procurement Platforms

Regional Insights

Europe

Europe accounted for approximately 39% of global hydrogenated olive oil demand in 2025, making it the largest regional market. The region benefits from a well-established olive oil value chain, advanced specialty ingredient manufacturing capabilities, and a strong presence of leading cosmetics, pharmaceutical, and food processing companies. Spain alone contributes nearly 15% of global market consumption, supported by its dominant position in olive cultivation, olive oil production, and downstream ingredient processing. Italy, Germany, France, and the United Kingdom remain major consumption centers due to robust demand from premium cosmetics, nutraceuticals, pharmaceuticals, and specialty food manufacturers. Regional growth is increasingly supported by stringent environmental regulations, sustainability initiatives, and growing demand for renewable plant-based ingredients. The expansion of clean-label food products, natural cosmetic formulations, and bio-based industrial materials continues to stimulate market development. In addition, strong consumer preference for premium personal care products, increasing investments in green chemistry, and regulatory support for sustainable sourcing practices are expected to reinforce Europe’s market leadership throughout the forecast period.

Asia-Pacific

Asia-Pacific represented approximately 28% of global market demand in 2025 and is projected to be the fastest-growing regional market, expanding at a CAGR of approximately 9.1% through 2031. Rapid industrialization, expanding manufacturing capabilities, and increasing consumer expenditure on personal care and healthcare products are driving regional growth. China remains the largest market within the region due to its extensive cosmetic, pharmaceutical, and specialty chemical manufacturing sectors. South Korea and Japan continue to drive premium demand through globally recognized beauty and skincare industries that increasingly utilize naturally derived ingredients. India is emerging as one of the fastest-growing national markets, supported by expanding pharmaceutical production, rising disposable incomes, increasing domestic personal care consumption, and growing awareness of clean-label products. Additional growth drivers include urbanization, the rapid expansion of e-commerce beauty channels, increasing foreign investment in specialty ingredients, and rising demand for premium skincare products among middle-class consumers. These factors collectively position Asia-Pacific as the primary growth engine for the global hydrogenated olive oil market.

North America

North America accounted for approximately 22% of global market demand in 2025. The United States represents the largest market in the region, supported by advanced cosmetic manufacturing infrastructure, a highly developed pharmaceutical sector, and strong consumer preference for natural and sustainable ingredients. Demand continues to increase across premium skincare products, clean beauty formulations, organic personal care products, and topical pharmaceutical applications. The growing popularity of plant-based ingredients and increasing regulatory scrutiny surrounding synthetic additives are encouraging manufacturers to incorporate naturally derived alternatives such as hydrogenated olive oil into product formulations. Canada contributes additional demand through specialty personal care products, pharmaceutical manufacturing, and nutraceutical applications. The region also benefits from strong research and development activities, increasing investments in innovative beauty formulations, and expanding consumer awareness regarding ingredient transparency, all of which are expected to support continued market growth.

Middle East & Africa

The Middle East and Africa accounted for approximately 6% of global market demand in 2025. Turkey serves as the region’s largest producer and consumer due to its extensive olive cultivation industry, established edible oil sector, and growing specialty ingredient manufacturing capabilities. Gulf Cooperation Council (GCC) countries continue to increase imports of premium cosmetic and personal care ingredients as demand for high-end beauty products expands. South Africa contributes through pharmaceutical production, personal care manufacturing, and growing adoption of naturally derived formulation ingredients. Regional growth is supported by rising disposable incomes, expanding urban populations, increasing consumer interest in premium skincare products, and growing investments in local cosmetics manufacturing. Furthermore, government-led economic diversification initiatives across several Gulf countries are encouraging investments in value-added consumer goods industries, creating additional opportunities for specialty ingredient suppliers.

Latin America

Latin America accounted for approximately 5% of global hydrogenated olive oil demand in 2025. Brazil and Mexico represent the largest regional markets due to their expanding personal care, cosmetics, and pharmaceutical industries. Increasing consumer awareness regarding natural ingredients, rising demand for premium beauty products, and growing adoption of clean-label formulations are contributing to market growth. Regional manufacturers are increasingly incorporating plant-derived ingredients into skincare and haircare products to align with evolving consumer preferences and international product standards. The pharmaceutical sector is also experiencing gradual expansion, supporting additional demand for high-quality excipients and formulation ingredients. Continued urbanization, rising middle-class purchasing power, increasing retail penetration of premium personal care products, and growing investments by multinational beauty brands are expected to support steady market expansion across the region over the forecast period.

Key Players in the Hydrogenated Olive Oil Market

- Hallstar

- AAK AB

- BASF

- Croda International

- Evonik Industries

- Nisshin Oillio Group

- Berg + Schmidt

- Givaudan Active Beauty

- Vantage Specialty Ingredients

- Res Pharma

- Sophim

- A&A Fratelli Parodi

- Industrial Quimica Lasem

- Olvea Group

- Gustav Heess