Hydrogenated Fat Market Size

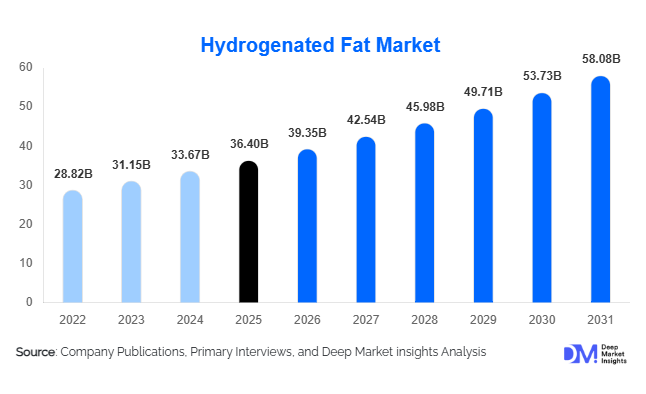

According to Deep Market Insights, the global hydrogenated fat market size was valued at USD 36.4 billion in 2025 and is projected to grow from USD 39.35 billion in 2026 to reach USD 58.08 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The hydrogenated fat market growth is primarily driven by rising consumption of processed foods, increasing demand for bakery and confectionery products, expansion of dairy alternatives, and growing utilization of specialty hydrogenated fats in personal care, pharmaceutical, and industrial applications. Despite regulatory restrictions on partially hydrogenated oils in several developed economies, manufacturers continue to benefit from growing adoption of fully hydrogenated and trans-fat-free fat systems that offer enhanced oxidative stability, longer shelf life, and improved product functionality.

Key Market Insights

- Fully hydrogenated fats account for nearly 48% of the global market, supported by regulatory-driven replacement of partially hydrogenated fats across developed economies.

- Palm oil-based hydrogenated fats dominate feedstock consumption, representing approximately 42% of total market demand due to cost competitiveness and abundant availability.

- Asia-Pacific leads the global hydrogenated fat market, accounting for nearly 38% of global consumption, driven by strong food manufacturing sectors in China, India, Indonesia, and Malaysia.

- Personal care and cosmetic applications are among the fastest-growing segments, supported by increasing demand for plant-based and sustainable ingredients.

- Food processing remains the largest end-use industry, contributing over 50% of global hydrogenated fat consumption.

- Investment in trans-fat-free technologies and specialty fat formulations is accelerating innovation and competitive differentiation among leading manufacturers.

Hydrogenated Fat Market Latest Trends

Transition Toward Trans-Fat-Free Fat Systems

One of the most significant trends shaping the hydrogenated fat market is the global transition toward trans-fat-free formulations. Regulatory authorities across North America, Europe, and parts of Asia have implemented stricter limits on industrial trans-fat consumption, encouraging manufacturers to replace partially hydrogenated oils with fully hydrogenated and interesterified fat systems. Food producers are increasingly investing in specialty fat formulations that provide similar texture, stability, and functionality without violating regulatory requirements. This trend is particularly evident in bakery shortenings, confectionery coatings, margarine formulations, and frying fats. As consumer awareness regarding cardiovascular health continues to rise, manufacturers are prioritizing cleaner formulations and reformulating existing product portfolios to comply with evolving nutritional standards.

Expansion of Specialty Fats for Non-Food Applications

Hydrogenated fats are increasingly being utilized beyond traditional food applications. The personal care, pharmaceutical, and oleochemical sectors are emerging as major consumers of specialty hydrogenated fats. Cosmetic manufacturers are incorporating hydrogenated vegetable fats into creams, lotions, lip balms, and skincare products due to their excellent emollient properties and oxidative stability. Similarly, pharmaceutical companies are using hydrogenated fats in controlled-release drug formulations and tablet coatings. The trend toward plant-based, sustainable, and naturally derived ingredients is further supporting demand from non-food industries. This diversification is enabling manufacturers to improve profitability by targeting higher-margin specialty applications rather than relying solely on food industry demand.

Hydrogenated Fat Market Drivers

Growth of Processed and Convenience Food Consumption

Rapid urbanization, changing lifestyles, and increasing disposable incomes are driving global consumption of processed and convenience foods. Hydrogenated fats remain essential ingredients in numerous food products due to their ability to improve texture, enhance shelf life, and provide thermal stability. Bakery products, packaged snacks, ready-to-eat meals, and frozen foods continue to generate substantial demand for specialty fats. Emerging economies such as India, China, Indonesia, Vietnam, and Brazil are witnessing strong growth in packaged food manufacturing, further supporting market expansion. Food processors continue to rely on hydrogenated fats to maintain product consistency, optimize production efficiency, and reduce spoilage throughout distribution channels.

Expanding Bakery and Confectionery Industries

The global bakery and confectionery sectors remain the largest consumers of hydrogenated fats. These ingredients play a critical role in producing desired textures, aeration properties, mouthfeel characteristics, and shelf stability. Growing consumption of cookies, cakes, pastries, doughnuts, fillings, and confectionery coatings is increasing demand for customized hydrogenated fat formulations. Developing markets are experiencing rising demand for western-style bakery products, while mature markets continue to emphasize premium and functional bakery offerings. The increasing penetration of organized retail and convenience stores is further supporting bakery industry growth worldwide.

Hydrogenated Fat Market Restraints

Regulatory Restrictions on Partially Hydrogenated Oils

Government agencies across several countries continue implementing regulations aimed at reducing trans-fat consumption. Restrictions on partially hydrogenated oils have forced manufacturers to invest significantly in reformulation efforts and alternative fat technologies. Compliance with varying regional standards increases operational complexity and development costs for global manufacturers. While fully hydrogenated fats offer a viable replacement, transitioning production systems and obtaining regulatory approvals can require substantial investment, creating challenges particularly for smaller market participants.

Volatility in Vegetable Oil Feedstock Prices

The hydrogenated fat industry remains highly dependent on feedstocks such as palm oil, soybean oil, sunflower oil, rapeseed oil, and coconut oil. Price fluctuations caused by weather disruptions, geopolitical tensions, trade restrictions, biofuel policies, and supply chain bottlenecks can significantly affect manufacturing costs and profit margins. Producers often face challenges in passing increased raw material costs directly to customers, resulting in margin pressures. Feedstock price volatility remains one of the most significant operational risks impacting long-term profitability and investment planning across the industry.

Hydrogenated Fat Industry Key Opportunities

Expansion of Emerging Market Food Processing Industries

Rapid industrialization of food processing sectors across Asia-Pacific, Latin America, the Middle East, and Africa presents substantial opportunities for hydrogenated fat manufacturers. Countries such as India, Indonesia, Vietnam, Nigeria, Egypt, and Saudi Arabia are investing heavily in food manufacturing infrastructure to meet rising domestic demand. Expanding urban populations and increasing consumption of packaged foods are creating new growth avenues for suppliers of bakery fats, frying fats, confectionery fats, and dairy replacement systems. Establishing regional production facilities and local distribution networks can provide manufacturers with significant competitive advantages in these fast-growing markets.

Growth of Personal Care and Pharmaceutical Applications

The increasing use of hydrogenated vegetable fats in cosmetics, skincare products, pharmaceutical excipients, and specialty formulations offers a high-value growth opportunity. Demand for plant-derived ingredients continues to rise globally as consumers increasingly favor sustainable and naturally sourced products. Manufacturers capable of supplying high-purity hydrogenated fats for pharmaceutical and cosmetic applications can benefit from higher margins and reduced exposure to food industry pricing pressures. Product innovation targeting premium personal care formulations is expected to become an increasingly important revenue driver throughout the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36.40 Billion |

| Market Size in 2026 | USD 39.35 Billion |

| Market Size in 2031 | USD 58.08 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fully hydrogenated fats constitute the largest product segment in the global hydrogenated fat market, accounting for approximately 48% of total revenue in 2025. The segment’s leadership is primarily driven by increasingly stringent regulations restricting the use of partially hydrogenated oils due to their trans-fat content, alongside growing consumer preference for healthier and cleaner-label food products. Fully hydrogenated fats provide excellent oxidative stability, longer shelf life, improved texture, and enhanced functionality while enabling manufacturers to formulate trans-fat-free products. Their widespread adoption across bakery, confectionery, margarine, shortening, dairy alternatives, and processed food applications continues to strengthen segment growth. Demand is particularly strong among multinational food manufacturers undertaking large-scale product reformulation initiatives to comply with global food safety regulations.Specialty hydrogenated fat blends represent the fastest-evolving product category, benefiting from growing demand for customized functionality across food and industrial applications. Manufacturers are increasingly developing tailored formulations for bakery shortenings, confectionery coatings, frying fats, filling fats, whipped toppings, dairy alternatives, and plant-based products. These specialty solutions offer precise melting profiles, improved texture, enhanced stability, and superior processing performance, making them highly attractive for premium product development and value-added food manufacturing.

Feedstock Source Insights

Palm oil-based hydrogenated fats dominate the feedstock landscape, accounting for approximately 42% of global consumption in 2025. The segment benefits from the abundant availability, cost competitiveness, high yield efficiency, and extensive production infrastructure associated with palm oil cultivation. Indonesia and Malaysia remain the primary suppliers of palm-derived feedstocks, supporting large-scale hydrogenated fat production and international trade. Palm oil’s favorable functional properties, including semi-solid characteristics and oxidative stability, further reinforce its position across bakery, confectionery, frying, and industrial applications.Rapeseed, sunflower, coconut, and cottonseed oils collectively contribute a significant share of specialty hydrogenated fat production. These feedstocks are increasingly utilized in premium food formulations, personal care products, pharmaceuticals, and specialty industrial applications where specific functional characteristics are required. Demand for non-palm alternatives is also growing among manufacturers seeking to diversify sourcing strategies and address evolving sustainability preferences.Animal-based hydrogenated fats, including tallow and lard derivatives, continue to serve niche markets within selected food, industrial, and oleochemical applications. Although substantially smaller than vegetable-based alternatives, these products remain relevant in specific formulations where unique performance attributes, cost considerations, or traditional consumption patterns support continued demand.

Application Insights

Food applications account for nearly 68% of global hydrogenated fat demand, making them the dominant application segment throughout the forecast period. The segment’s leadership is driven by the essential functional role hydrogenated fats play in improving texture, consistency, stability, mouthfeel, and shelf life across a wide range of food products. Growing consumption of packaged foods, convenience meals, snacks, and processed food products worldwide continues to support sustained demand from food manufacturers.Bakery products represent the single largest application area, supported by increasing global consumption of bread, cakes, pastries, biscuits, cookies, and other baked goods. Hydrogenated fats provide critical functionality by improving dough handling characteristics, enhancing product texture, extending freshness, and ensuring consistent manufacturing performance. Rising urbanization, changing dietary habits, and growing demand for convenience foods continue to strengthen bakery sector consumption.Non-food applications are expanding steadily as hydrogenated fats gain importance in cosmetics, pharmaceuticals, soaps, candles, lubricants, and oleochemical derivatives. Manufacturers are increasingly targeting these higher-margin specialty applications to diversify revenue streams and reduce exposure to commodity food markets. Growing demand for personal care products and specialty industrial formulations is expected to support long-term expansion within non-food segments.

End-Use Industry Insights

The food processing industry remains the largest end-use segment, accounting for approximately 53% of global hydrogenated fat consumption in 2025. The segment’s dominance is driven by rising global demand for processed foods, convenience products, packaged snacks, frozen meals, and ready-to-eat food categories. Large-scale food manufacturers rely on hydrogenated fats to deliver product consistency, improve processing efficiency, extend shelf life, and optimize product quality across diverse formulations.The bakery industry represents one of the most significant consumption sectors within the broader food processing landscape. Strong consumer demand for baked products across both developed and emerging economies continues to support extensive utilization of shortenings, specialty fats, and functional lipid systems. Expanding quick-service restaurant networks, café chains, and retail bakery operations further contribute to segment growth.Personal care and cosmetics represent one of the fastest-growing end-use industries, supported by increasing consumer spending on skincare, haircare, and beauty products worldwide. Hydrogenated fats are widely utilized in creams, lotions, emulsions, lip care products, and specialty cosmetic formulations due to their stability, texture-enhancing properties, and compatibility with various active ingredients.The chemical and oleochemical industries also contribute significantly to market expansion through applications involving surfactants, soaps, detergents, lubricants, candles, coatings, and industrial formulations. Rising demand for bio-based ingredients and sustainable industrial feedstocks is expected to further support consumption across these sectors.

Distribution Channel Insights

Direct business-to-business supply agreements account for the majority of global hydrogenated fat sales and remain the dominant distribution channel. Large food manufacturers, bakery chains, confectionery producers, pharmaceutical companies, and personal care manufacturers typically procure hydrogenated fats through long-term contracts with major producers to ensure stable supply, quality consistency, and cost efficiency. The increasing complexity of product formulations and the need for customized fat solutions further strengthen the importance of direct supplier relationships.Ingredient distributors play a critical role in serving medium-sized manufacturers, regional processors, and specialty product developers that require flexible procurement arrangements and technical support. These distribution networks help expand market reach while improving accessibility across geographically diverse customer bases.Commodity traders facilitate the international movement of vegetable oil feedstocks and finished hydrogenated fat products, particularly across Asia-Pacific, Europe, and North America. Their role remains essential in balancing global supply-demand dynamics and managing procurement risks associated with agricultural commodity markets.The growing adoption of digital procurement platforms, industrial sourcing networks, and supply chain management technologies is improving transaction efficiency, enhancing transparency, reducing procurement costs, and enabling manufacturers to optimize inventory management. Digitalization is expected to play an increasingly important role in shaping future distribution strategies across the hydrogenated fat value chain.

Explore more data points, trends and opportunities Download Free Sample Report

Hydrogenated Fat Market Segmentations

By Product Type

- Fully Hydrogenated Fats

- Partially Hydrogenated Fats

- Hydrogenated Fat Blends & Specialty Fat Systems

By Feedstock Source

- Palm Oil-Based Hydrogenated Fats

- Palm Kernel Oil-Based Hydrogenated Fats

- Soybean Oil-Based Hydrogenated Fats

- Sunflower Oil-Based Hydrogenated Fats

- Canola/Rapeseed Oil-Based Hydrogenated Fats

- Coconut Oil-Based Hydrogenated Fats

- Cottonseed Oil-Based Hydrogenated Fats

- Animal-Based Hydrogenated Fats

- Other Feedstock Sources

By Application

- Bakery Products

- Confectionery Products

- Margarine & Spreads

- Dairy Alternatives

- Snack Foods

- Processed & Convenience Foods

- Cosmetics & Personal Care Products

- Pharmaceutical Applications

- Industrial & Oleochemical Applications

By End-Use Industry

- Food Processing Industry

- Bakery Industry

- Confectionery Industry

- Dairy Alternative Industry

- Personal Care & Cosmetics Industry

- Pharmaceutical Industry

- Chemical & Oleochemical Industry

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global hydrogenated fat market, accounting for approximately 38% of total revenue in 2025. China remains the largest individual market, contributing nearly 12% of global demand, supported by its extensive food processing industry, large-scale bakery manufacturing sector, and rapidly expanding packaged food consumption. India accounts for approximately 8% of worldwide demand, driven by rising disposable incomes, urbanization, growing organized retail penetration, and increasing consumption of convenience foods. Indonesia and Malaysia benefit from highly integrated palm oil value chains, abundant feedstock availability, and substantial domestic refining and processing capacities. Japan and South Korea remain important consumers of specialty fats utilized in premium bakery, confectionery, and processed food applications.Regional growth is being driven by rapid urbanization, expanding middle-class populations, rising consumption of packaged and convenience foods, increasing investment in food processing infrastructure, growing quick-service restaurant penetration, expansion of modern retail channels, and strong availability of vegetable oil feedstocks. The region also benefits from increasing demand for bakery and confectionery products, accelerating industrialization, and continuous capacity expansions by major food ingredient manufacturers. As a result, Asia-Pacific is expected to remain the fastest-growing regional market throughout the forecast period.

Europe

Europe accounts for approximately 24% of global hydrogenated fat demand and represents one of the most mature markets worldwide. Germany, France, the United Kingdom, Italy, Spain, and the Netherlands constitute the region’s primary consumption centers. Strict regulatory requirements regarding trans fats have accelerated the adoption of fully hydrogenated fats and specialty fat systems across European food manufacturing industries. The region also demonstrates strong emphasis on sustainability, traceability, and certified vegetable oil sourcing practices.Growth across Europe is primarily supported by continuous product reformulation initiatives, increasing demand for premium bakery and confectionery products, expanding dairy alternative consumption, rising adoption of plant-based foods, and strong investment in specialty ingredient innovation. Additionally, consumer preference for clean-label products, sustainable sourcing standards, and premium food experiences continues to create opportunities for advanced specialty fat formulations across the region.

North America

North America holds approximately 22% of the global hydrogenated fat market. The United States alone contributes nearly 18% of worldwide demand due to its extensive processed food industry, large snack food sector, developed bakery market, and significant foodservice industry presence. Canada supports regional demand through bakery manufacturing, specialty food production, and premium packaged food consumption, while Mexico benefits from expanding food processing investments and growing demand for convenience food products.Regional growth is driven by ongoing product reformulation efforts to comply with trans-fat regulations, increasing demand for functional specialty fats, strong consumption of processed and convenience foods, expansion of plant-based food categories, and continued innovation within bakery and confectionery applications. Advanced manufacturing capabilities, established distribution networks, and rising demand for clean-label formulations further support market development across North America.

Latin America

Latin America accounts for approximately 9% of global hydrogenated fat consumption. Brazil represents the largest market in the region, supported by its extensive food processing industry, large domestic consumer base, and strong soybean oil production capabilities. Argentina and Mexico continue to contribute significantly through growing packaged food industries, expanding urban populations, and increasing investment in food manufacturing infrastructure.Regional growth is supported by rising disposable incomes, increasing urbanization, expanding modern retail networks, growing consumption of bakery and confectionery products, and continued development of local food processing industries. Abundant agricultural resources, particularly soybean production, provide a strong feedstock foundation that supports both domestic consumption and export-oriented manufacturing activities.

Middle East & Africa

The Middle East and Africa account for approximately 7% of global hydrogenated fat consumption and represent one of the fastest-growing regional markets. Saudi Arabia, the UAE, Egypt, and South Africa serve as major demand centers, supported by population growth, increasing food imports, and expanding domestic food manufacturing activities. Governments across the region are actively investing in food security initiatives, industrial diversification programs, and local production capabilities, creating favorable conditions for market expansion.Growth in the region is being driven by rapid population expansion, increasing per-capita food consumption, rising demand for packaged and convenience foods, growth in hospitality and foodservice sectors, expanding retail infrastructure, and increasing investments in local food processing facilities. Additionally, rising consumer spending on personal care and cosmetic products, particularly across Gulf Cooperation Council countries, is supporting demand for specialty hydrogenated fats used in non-food applications. Continued industrial development and economic diversification initiatives are expected to sustain strong market growth over the forecast period.

Key Players in the Hydrogenated Fat Market

- Wilmar International

- Cargill Incorporated

- Bunge Global SA

- AAK AB

- Fuji Oil Holdings Inc.

- IFFCO Group

- Musim Mas Holdings

- Intercontinental Specialty Fats

- Mewah International Inc.

- Olenex

- 3F Industries Ltd.

- Archer Daniels Midland (ADM)

- Nisshin Oillio Group Ltd.

- IOI Corporation Berhad

- Vandemoortele NV