Herbal Tea Market Size

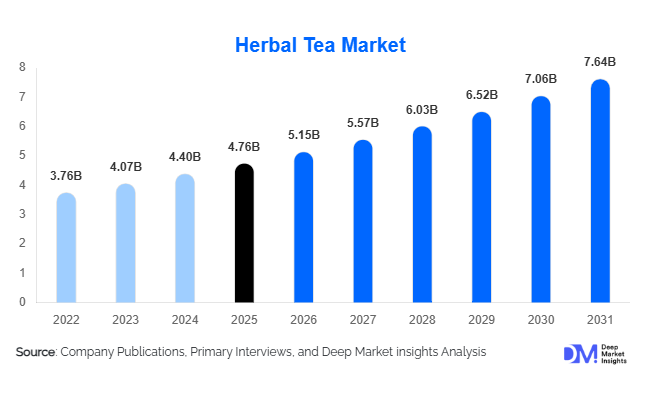

According to Deep Market Insights, the global herbal tea market size was valued at USD 4.76 billion in 2025 and is projected to grow from USD 5.15 billion in 2026 to reach USD 7.64 billion by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The herbal tea market growth is primarily driven by increasing consumer preference for natural and functional beverages, rising awareness regarding preventive healthcare, growing adoption of plant-based wellness products, and expanding demand for caffeine-free alternatives to conventional tea and coffee. The market is also benefiting from premiumization trends, organic product adoption, and the growing influence of traditional medicinal systems such as Ayurveda, Traditional Chinese Medicine (TCM), and herbal wellness practices across developed and emerging economies.

Key Market Insights

- Functional herbal teas are becoming mainstream wellness products, with consumers increasingly seeking formulations that support immunity, digestion, sleep quality, stress management, and detoxification.

- Organic herbal tea demand continues to accelerate globally, driven by clean-label preferences, sustainability concerns, and increasing willingness among consumers to pay premium prices for certified products.

- Asia-Pacific dominates the global herbal tea market, supported by strong herbal medicine traditions, extensive botanical cultivation, and growing domestic consumption in China and India.

- North America remains one of the fastest-growing premium consumption markets, driven by rising health consciousness and strong adoption of functional beverages.

- E-commerce and direct-to-consumer channels are transforming distribution, allowing brands to access global consumers and introduce specialized herbal formulations.

- Innovation in adaptogens, botanicals, and personalized wellness products is creating new revenue streams and enabling manufacturers to differentiate within a highly competitive marketplace.

Herbal Tea Market Latest Trends

Functional Wellness Formulations Driving Product Innovation

The herbal tea industry is witnessing a significant shift toward functional formulations that target specific health and wellness outcomes. Consumers increasingly prefer herbal blends containing ingredients such as turmeric, ginger, chamomile, ashwagandha, echinacea, moringa, peppermint, and tulsi due to their perceived health benefits. Manufacturers are developing scientifically backed products that support immunity, digestive health, sleep enhancement, stress reduction, weight management, and cognitive wellness. Premium wellness teas are gaining shelf space in supermarkets, pharmacies, specialty wellness stores, and online marketplaces. Companies are also introducing adaptogenic herbal blends designed to help consumers manage stress and improve resilience, reflecting broader consumer interest in holistic health and preventive healthcare solutions.

Sustainability and Organic Certification Becoming Key Purchasing Factors

Sustainability is becoming a major differentiator within the herbal tea market. Consumers increasingly seek products sourced through environmentally responsible cultivation practices and transparent supply chains. Organic certification, Fair Trade sourcing, biodegradable tea bags, recyclable packaging, and carbon-neutral production methods are becoming important purchase drivers. Leading manufacturers are investing in regenerative agriculture programs and direct sourcing partnerships with growers to improve supply security while meeting sustainability expectations. Premium brands are further strengthening consumer trust through traceability initiatives that provide visibility into ingredient origin, cultivation practices, and quality assurance processes. These trends are particularly prominent across North America and Europe, where sustainability considerations strongly influence purchasing behavior.

Herbal Tea Market Drivers

Growing Consumer Focus on Preventive Healthcare

The increasing emphasis on preventive healthcare is one of the strongest growth drivers for the herbal tea market. Consumers are actively incorporating herbal beverages into daily routines as part of broader wellness strategies aimed at supporting immunity, digestive health, stress reduction, and overall well-being. Rising awareness regarding lifestyle diseases, aging populations, and healthcare costs has encouraged greater adoption of natural remedies and functional foods. Herbal teas are increasingly viewed as convenient, affordable, and accessible wellness solutions, driving demand across both developed and emerging markets.

Expansion of the Global Functional Beverage Industry

The rapid growth of the functional beverage sector is creating significant opportunities for herbal tea manufacturers. Consumers are increasingly replacing sugary soft drinks, carbonated beverages, and energy drinks with healthier alternatives offering functional benefits. Herbal teas align closely with evolving consumer preferences for clean-label products, natural ingredients, and low-calorie beverages. Product innovation focused on immunity support, detoxification, metabolism enhancement, and relaxation continues to attract health-conscious consumers. The market is also benefiting from increasing integration of herbal teas into broader wellness ecosystems that include nutraceuticals, dietary supplements, and functional foods.

Herbal Tea Market Restraints

Raw Material Price Volatility and Agricultural Risks

The herbal tea industry remains highly dependent on agricultural production, making it vulnerable to fluctuations in raw material availability and pricing. Climate change, droughts, floods, pest infestations, and changing weather patterns can significantly impact yields of key herbs such as chamomile, peppermint, hibiscus, ginger, and lemongrass. Supply disruptions often result in increased procurement costs and margin pressure for manufacturers. The growing demand for organic ingredients further intensifies sourcing challenges, as certified organic cultivation requires stricter agricultural practices and longer production cycles.

Regulatory and Health Claim Compliance Challenges

Regulatory complexity remains a key challenge for herbal tea manufacturers operating across multiple jurisdictions. Requirements related to product labeling, ingredient approvals, health claims, organic certification, and food safety standards vary significantly between countries. Companies must invest substantial resources in regulatory compliance, testing, and certification processes to maintain market access. Restrictions on therapeutic claims can also limit marketing flexibility, particularly for products positioned around specific health benefits, creating barriers for smaller market participants seeking international expansion.

Herbal Tea Industry Key Opportunities

Expansion of Functional and Medicinal Herbal Tea Categories

Functional herbal teas represent one of the most attractive opportunities for industry participants. Demand is growing rapidly for products targeting specific health outcomes such as immunity enhancement, digestive support, stress management, sleep improvement, weight control, and women's health. Companies that successfully combine traditional herbal knowledge with scientific validation can achieve premium positioning and stronger customer loyalty. The increasing convergence of herbal teas and nutraceuticals is expected to create substantial value creation opportunities over the coming decade.

Emerging Market Expansion and Digital Commerce Growth

Rapid urbanization, rising disposable incomes, and increasing health awareness are creating new demand opportunities across emerging markets including India, China, Indonesia, Vietnam, Brazil, Saudi Arabia, and the UAE. Simultaneously, digital commerce platforms are enabling manufacturers to reach consumers directly without extensive investments in traditional retail infrastructure. Subscription models, personalized tea recommendations, wellness-focused marketplaces, and direct-to-consumer channels are improving customer acquisition and retention while supporting premium product sales. These developments are expected to accelerate market penetration and unlock new growth opportunities for both established brands and new entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.76 Billion |

| Market Size in 2026 | USD 5.15 Billion |

| Market Size in 2031 | USD 7.64 Billion |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mixed herbal blends represent the largest product segment, accounting for approximately 28% of the global herbal tea market in 2025. Consumers increasingly prefer multifunctional products that combine ingredients such as chamomile, ginger, peppermint, hibiscus, turmeric, and lemongrass to deliver multiple wellness benefits within a single beverage. Chamomile tea remains one of the most widely consumed single-herb products due to its association with relaxation and sleep support, while ginger and turmeric teas continue to gain popularity because of their anti-inflammatory positioning. Hibiscus and rooibos teas are experiencing growing demand among consumers seeking antioxidant-rich alternatives, while moringa and adaptogenic herbal teas are emerging as premium niche categories. Continuous product innovation and botanical ingredient diversification are expected to sustain strong growth across multiple herbal tea categories.

Functional Benefit Insights

General wellness teas account for approximately 26% of total market revenue, making them the leading functional category. These products appeal to a broad consumer base by supporting overall health without targeting specific medical conditions. Immunity-support teas have experienced significant growth due to increased health awareness and rising interest in preventive healthcare. Digestive health teas containing peppermint, fennel, ginger, and licorice continue to perform strongly across global markets. Relaxation and sleep-support formulations featuring chamomile, lavender, and valerian are also expanding rapidly as consumers seek natural stress management solutions. Detoxification, weight management, cognitive wellness, and energy-support formulations are increasingly attracting younger health-conscious consumers seeking personalized wellness products.

Nature and Form Insights

Conventional herbal tea continues to dominate the market, accounting for nearly 76% of global sales in 2025, primarily due to broader availability and affordability. However, organic herbal tea remains the fastest-growing category as consumers increasingly prioritize clean-label products and sustainable sourcing practices. In terms of product form, tea bags account for approximately 58% of global demand, supported by convenience, standardized brewing, and widespread retail availability. Loose-leaf herbal teas continue to attract premium consumers who value authenticity and flavor quality. Meanwhile, ready-to-drink (RTD) herbal tea beverages are emerging as a high-growth segment, particularly among younger consumers seeking convenient wellness beverages suitable for on-the-go consumption.

Distribution Channel Insights

Supermarkets and hypermarkets remain the largest distribution channel, accounting for approximately 37% of global herbal tea sales. Their extensive product selection, strong brand visibility, and widespread consumer reach continue to support channel dominance. Specialty tea stores and health-focused retailers play a critical role in premium and organic product sales, particularly in developed markets. Pharmacies and wellness stores are increasingly important channels for functional and medicinal herbal tea formulations. Online retail and direct-to-consumer channels represent the fastest-growing distribution segment, benefiting from expanding digital adoption, subscription services, and personalized shopping experiences. E-commerce platforms enable brands to introduce niche products, educate consumers, and expand internationally without substantial investments in traditional retail infrastructure.

End-Use Insights

Household consumption remains the dominant end-use segment, representing approximately 68% of global herbal tea demand. Growing awareness of wellness benefits, increasing home-based beverage consumption, and the incorporation of herbal teas into daily health routines continue to support strong household demand. The hospitality sector, including hotels, resorts, cafés, and restaurants, remains an important contributor to market growth, particularly within premium herbal tea categories. Wellness centers, spas, healthcare facilities, and corporate offices are emerging as high-growth end-use segments as organizations increasingly promote employee wellness and customer well-being. Airlines and travel catering operators are also expanding herbal tea offerings to meet growing consumer demand for healthier beverage alternatives during travel.

Explore more data points, trends and opportunities Download Free Sample Report

Herbal Tea Market Segmentations

By Product Type

- Chamomile Tea

- Peppermint Tea

- Ginger Tea

- Hibiscus Tea

- Rooibos Tea

- Turmeric Tea

- Lavender Tea

- Lemongrass Tea

- Echinacea Tea

- Dandelion Tea

- Moringa Tea

- Cinnamon Tea

- Sage Tea

- Fennel Tea

- Mixed Herbal Blends

- Other Herbal Teas

By Functional Benefit

- Digestive Health Teas

- Immunity Support Teas

- Relaxation & Sleep Support Teas

- Detox & Cleansing Teas

- Weight Management Teas

- Energy & Vitality Teas

- Women's Health Teas

- Respiratory Health Teas

- Cognitive Wellness Teas

- General Wellness Teas

By Nature

- Conventional Herbal Tea

- Organic Herbal Tea

By Form

- Tea Bags

- Loose Leaf Herbal Tea

- Instant Herbal Tea Powder

- Ready-to-Drink (RTD) Herbal Tea

- Herbal Tea Concentrates

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Tea Stores

- Pharmacies & Health Stores

- Online Retail/E-Commerce

- Direct-to-Consumer (DTC)

- Foodservice Distributors

egional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 38% of global herbal tea market revenue in 2025, making it the largest regional market. China and India represent the primary demand centers due to longstanding herbal medicine traditions and extensive botanical cultivation. China remains both a major producer and consumer of herbal teas, supported by Traditional Chinese Medicine practices and increasing wellness-focused consumption. India continues to experience strong demand growth driven by Ayurveda-based formulations, rising disposable incomes, and expanding health awareness. Japan, South Korea, and Australia contribute significantly through premium consumption and growing demand for functional wellness beverages. Asia-Pacific is expected to remain the fastest-growing regional market throughout the forecast period.

Europe

Europe accounted for approximately 31% of global market demand in 2025, supported by strong consumer acceptance of herbal remedies and high organic product adoption. Germany remains the largest European herbal tea market, benefiting from a well-established herbal medicine culture and significant demand for chamomile, peppermint, and medicinal herbal blends. The United Kingdom, France, Italy, and Spain also represent major consumption centers. Sustainability, organic certification, and premium wellness positioning continue to drive growth across the region, with consumers demonstrating strong willingness to pay higher prices for ethically sourced products.

North America

North America represents approximately 22% of global herbal tea consumption, with the United States accounting for the majority of regional demand. The region benefits from growing consumer interest in functional beverages, preventive healthcare, and clean-label nutrition. Premium organic herbal teas, adaptogenic formulations, and specialty wellness products continue to gain traction among health-conscious consumers. Canada also contributes significantly to regional demand, supported by strong adoption of natural health products and sustainable consumer preferences.

Latin America

Latin America accounts for approximately 5% of global herbal tea demand, led by Brazil and Mexico. Growing urbanization, rising health awareness, and increasing middle-class purchasing power are supporting market expansion across the region. Consumers increasingly view herbal teas as healthier alternatives to sugary beverages, creating opportunities for both domestic and international brands.

Middle East & Africa

The Middle East & Africa region represents approximately 4% of global demand but offers significant long-term growth potential. The UAE and Saudi Arabia are emerging as key premium consumption markets due to rising disposable incomes and increasing health-conscious lifestyles. South Africa and Egypt remain important regional markets, supported by growing wellness trends and expanding retail distribution. Increasing consumer awareness regarding herbal wellness products is expected to accelerate market growth across the region over the forecast period.

Key Players in the Herbal Tea Market

- Unilever

- Associated British Foods (Twinings)

- Tata Consumer Products

- Hain Celestial Group

- Bigelow Tea

- Traditional Medicinals

- Yogi Tea

- Celestial Seasonings

- The Republic of Tea

- Numi Organic Tea

- Harney & Sons

- Stash Tea

- Rishi Tea & Botanicals

- Dilmah Tea

- Teekanne