Herbal Liqueur Market Size

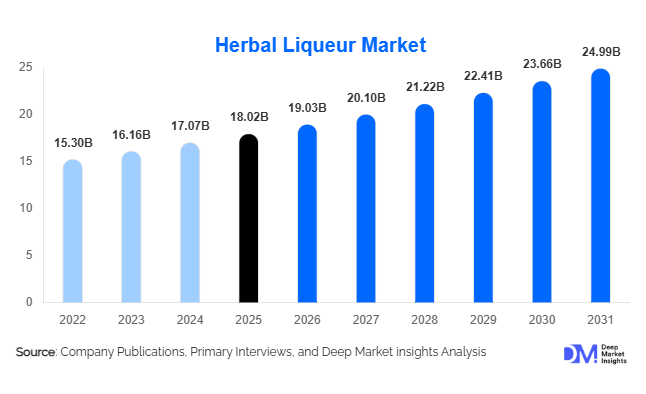

According to Deep Market Insights, the global herbal liqueur market size was valued at USD 18.02 billion in 2025 and is projected to grow from USD 19.03 billion in 2026 to reach USD 24.99 billion by 2031, expanding at a CAGR of 5.6% during the forecast period (2026–2031). The herbal liqueur market growth is primarily driven by rising premium spirits consumption, increasing consumer preference for botanical and natural flavor profiles, expanding cocktail culture worldwide, and growing demand for authentic heritage-based alcoholic beverages. Herbal liqueurs, traditionally consumed as digestifs and aperitifs, are increasingly being adopted across premium hospitality venues, craft cocktail bars, and luxury retail channels. Market expansion is further supported by innovation in botanical formulations, premium packaging, sustainable sourcing initiatives, and the growing popularity of low-sugar and artisanal alcoholic beverages among younger consumers.

Key Market Insights

- Premium and super-premium herbal liqueurs are gaining market share, supported by consumers seeking authentic botanical ingredients, craft production methods, and premium drinking experiences.

- Cocktail and mixology applications are emerging as the fastest-growing consumption segment, driving demand across bars, restaurants, hotels, and premium hospitality venues globally.

- Europe dominates the global herbal liqueur market, accounting for nearly 45% of total revenue due to strong consumption traditions in Germany, Italy, France, Austria, and Central Europe.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, urbanization, premium alcohol adoption, and growing cocktail culture across China, India, South Korea, and Southeast Asia.

- Off-trade retail channels remain the largest distribution network, benefiting from strong supermarket, liquor store, and specialty alcohol retail penetration.

- Botanical innovation and sustainable production technologies are reshaping product development strategies, with manufacturers focusing on organic ingredients, traceable sourcing, and environmentally responsible packaging solutions.

Herbal Liqueur Market Latest Trends

Premium Botanical Spirits Driving Consumer Demand

One of the most significant trends shaping the herbal liqueur market is the growing consumer preference for premium botanical spirits. Consumers are increasingly seeking beverages formulated with natural herbs, roots, spices, flowers, and fruit extracts rather than artificial flavoring systems. Premium herbal liqueurs featuring heritage recipes, small-batch production methods, and unique regional botanical blends are experiencing strong demand growth across Europe, North America, and Asia-Pacific. Manufacturers are responding by introducing limited-edition products, single-origin botanical formulations, and luxury packaging concepts. This premiumization trend has enabled producers to increase average selling prices while strengthening brand differentiation and consumer loyalty. Sustainable sourcing certifications, organic ingredients, and transparent ingredient labeling are becoming key purchasing criteria among younger consumer groups.

Expansion of Cocktail and Mixology Culture

The global resurgence of cocktail culture is significantly influencing herbal liqueur consumption patterns. Bartenders increasingly incorporate herbal liqueurs into signature cocktails, aperitif drinks, and contemporary mixology creations due to their complex flavor profiles and versatility. Premium hospitality operators are actively developing cocktail menus featuring herbal digestifs, bitters, and aperitifs to meet evolving consumer tastes. Social media platforms, craft cocktail competitions, and experiential drinking occasions are further driving awareness of herbal liqueur brands. In addition, ready-to-drink (RTD) cocktail innovations incorporating herbal liqueurs are creating new consumption occasions, particularly among younger consumers seeking convenience without compromising premium quality.

Herbal Liqueur Market Drivers

Growing Global Premium Spirits Consumption

The premiumization of alcoholic beverages continues to be one of the strongest growth drivers for the herbal liqueur market. Consumers across developed and emerging economies are increasingly shifting from volume-based alcohol consumption toward quality-focused drinking experiences. Herbal liqueurs benefit from their heritage positioning, distinctive botanical formulations, and premium brand narratives, enabling manufacturers to capture higher-value consumer segments. Premium products account for nearly 39% of global herbal liqueur revenue, reflecting strong willingness among consumers to pay higher prices for authenticity, craftsmanship, and unique flavor profiles. The growing number of premium hospitality establishments, luxury bars, and upscale dining venues further supports demand for high-end herbal liqueur offerings.

Increasing Preference for Natural and Botanical Ingredients

Consumer awareness regarding ingredient transparency and natural product formulations is positively impacting demand for herbal liqueurs. Unlike many flavored spirits that rely heavily on synthetic additives, herbal liqueurs derive their flavor characteristics from botanicals such as gentian root, mint, angelica, cardamom, fennel, citrus peel, saffron, and numerous traditional herbs. This botanical heritage resonates strongly with consumers seeking authentic ingredients and premium beverage experiences. Producers are increasingly emphasizing ingredient traceability, organic cultivation, and sustainable sourcing practices to strengthen market positioning and appeal to health-conscious consumers.

Expansion of Global Hospitality and Cocktail Industries

The rapid growth of cocktail bars, premium restaurants, luxury hotels, and experiential hospitality venues is creating substantial opportunities for herbal liqueur manufacturers. Cocktail and mixology applications currently represent approximately 35% of total market demand and continue to expand as bartenders experiment with increasingly sophisticated flavor combinations. International tourism recovery, rising foodservice spending, and growth in premium nightlife venues are contributing to broader herbal liqueur adoption across both mature and emerging markets. The hospitality sector's focus on differentiated beverage offerings further reinforces long-term consumption growth.

Herbal Liqueur Market Restraints

Regulatory and Taxation Challenges

Alcoholic beverage regulations vary considerably across countries, creating operational complexities for herbal liqueur manufacturers. Producers must comply with differing excise tax structures, labeling requirements, advertising restrictions, ingredient disclosure standards, and import regulations. These compliance requirements increase administrative costs and can slow international market expansion. Regulatory tightening related to alcohol marketing and public health initiatives may also limit promotional opportunities in certain jurisdictions.

Volatility in Botanical Raw Material Prices

Herbal liqueur production depends on a wide range of agricultural ingredients, including herbs, roots, spices, flowers, and citrus fruits. Supply chain disruptions, adverse weather conditions, climate change impacts, and inflationary pressures can significantly affect raw material availability and pricing. Ingredients such as gentian root, saffron, cardamom, and specialty botanicals are particularly susceptible to supply fluctuations. Rising input costs can pressure manufacturer margins, particularly among smaller craft producers with limited purchasing scale.

Herbal Liqueur Industry Key Opportunities

Expansion Across High-Growth Asia-Pacific Markets

Asia-Pacific presents one of the most attractive growth opportunities for herbal liqueur manufacturers. Rising middle-class populations, increasing disposable incomes, premium alcohol adoption, and growing urban cocktail culture are creating favorable market conditions across China, India, South Korea, Vietnam, Thailand, and Indonesia. International brands are expanding distribution partnerships, investing in localized marketing initiatives, and developing region-specific product offerings tailored to evolving consumer preferences. China alone is expected to register CAGR above 8% through 2031, making it one of the most attractive growth markets globally.

Low-Sugar and Wellness-Oriented Product Innovation

Although herbal liqueurs remain alcoholic beverages, manufacturers are increasingly exploring lower-sugar formulations, reduced-alcohol variants, and products emphasizing natural botanical ingredients. Consumers are seeking beverages that align with broader wellness and moderation trends while still delivering premium taste experiences. This presents opportunities for producers to innovate through functional botanicals, organic ingredients, and cleaner-label formulations. Products positioned around authenticity, ingredient transparency, and sustainability are expected to attract younger demographics and premium consumers alike.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.02 Billion |

| Market Size in 2026 | USD 19.03 Billion |

| Market Size in 2031 | USD 24.99 Billion |

| CAGR | 5.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bitter herbal liqueurs dominate the global market, accounting for approximately 42% of total revenue in 2025. Their leadership position is supported by strong consumption across cocktail applications, digestif occasions, and premium hospitality venues. Popular categories such as amaro, fernet, and herbal bitters continue to experience strong demand, particularly across European and North American markets. Digestif herbal liqueurs represent the second-largest segment due to longstanding consumption traditions in Europe and Latin America. Aperitif herbal liqueurs are gaining momentum as consumers increasingly embrace pre-meal drinking occasions and cocktail culture. Premium botanical herbal liqueurs are among the fastest-growing product categories, benefiting from premiumization trends and increasing consumer interest in artisanal spirits.

Botanical Ingredient Insights

Mixed botanical formulations represent the largest ingredient segment, accounting for nearly 48% of global herbal liqueur revenue. These products typically combine dozens of herbs, roots, spices, flowers, and citrus ingredients, creating highly differentiated flavor profiles and strong brand identities. Root-based formulations, including gentian and angelica-derived products, remain particularly important in traditional European herbal liqueurs. Herb-based and spice-based formulations are gaining popularity among craft producers seeking innovative flavor combinations. Citrus and floral botanical variants are increasingly utilized in premium cocktail applications, where lighter flavor profiles appeal to modern consumers seeking more versatile drinking experiences.

Distribution Channel Insights

Off-trade distribution channels account for approximately 61% of total market revenue, making them the dominant route to market globally. Supermarkets, liquor stores, specialty alcohol retailers, and duty-free outlets continue to drive volume sales due to their extensive geographic reach and consumer accessibility. On-trade channels, including bars, restaurants, hotels, and nightclubs, remain critically important for premium brand development and consumer trial. Cocktail culture expansion is particularly benefiting on-trade sales growth. Online retail channels are experiencing accelerated adoption, supported by digital alcohol platforms, direct-to-consumer sales strategies, and evolving consumer purchasing behavior. Brand-owned e-commerce platforms are increasingly becoming important tools for premium customer engagement and product differentiation.

Consumer Group Insights

Millennials account for approximately 36% of global herbal liqueur consumption and represent the largest consumer segment. This demographic is highly receptive to premium spirits, cocktail experimentation, and authentic botanical ingredients. Generation Z consumers are increasingly entering the category through cocktail culture, social media influence, and premium RTD beverage innovations. Generation X remains a significant contributor to premium and luxury herbal liqueur sales due to strong purchasing power and established consumption habits. High-net-worth consumers continue driving demand for super-premium and limited-edition herbal liqueur products, particularly within gifting and luxury hospitality applications.

End-Use Insights

Direct consumption remains the largest end-use category, accounting for roughly 40% of total market demand. However, cocktail and mixology applications represent the fastest-growing segment, contributing approximately 35% of global consumption and expanding at a rate exceeding overall market growth. Hospitality and foodservice applications continue benefiting from premium beverage menu development and tourism recovery. Cultural and traditional ceremonies remain important consumption channels in several European and Latin American markets. Premium gifting and collector-oriented consumption are emerging as high-value applications, particularly within luxury spirits categories. The growing use of herbal liqueurs in RTD cocktails and experiential hospitality offerings is expected to create additional demand opportunities throughout the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Herbal Liqueur Market Segmentations

By Product Type

- Bitter Herbal Liqueurs

- Digestif Herbal Liqueurs

- Aperitif Herbal Liqueurs

- Sweet Herbal Liqueurs

- Semi-Sweet Herbal Liqueurs

- Herbal Cream Liqueurs

- Traditional Regional Herbal Liqueurs

- Premium Botanical Herbal Liqueurs

By Botanical Ingredient Base

- Root-Based (Gentian, Angelica, Licorice Root)

- Herb-Based (Mint, Sage, Thyme, Rosemary)

- Spice-Based (Cardamom, Cinnamon, Clove, Star Anise)

- Citrus Botanical-Based

- Floral Botanical-Based

- Mixed Botanical Formulations

By Alcohol Content

- Below 20% ABV

- 20%–30% ABV

- 30%–40% ABV

- Above 40% ABV

By Price Category

- Economy

- Mid-Premium

- Premium

- Super Premium & Luxury

By Distribution Channel

-

On-Trade

- Bars

- Restaurants

- Hotels

- Nightclubs

-

Off-Trade

- Supermarkets & Hypermarkets

- Liquor Stores

- Specialty Beverage Stores

- Duty-Free Retail

-

Online Retail

- Brand-Owned Platforms

- E-Commerce Marketplaces

Regional Insights

Europe

Europe remains the largest regional market, accounting for approximately 45% of global herbal liqueur revenue in 2025. Germany leads regional demand with nearly 12% of global consumption, supported by strong cultural acceptance of herbal digestifs and premium bitters. Italy contributes approximately 9% of global revenue through its extensive amaro consumption tradition. France, Austria, Switzerland, and the Czech Republic also represent significant markets due to established herbal spirits cultures. Premiumization, cocktail innovation, and tourism-driven demand continue supporting regional growth.

North America

North America accounts for approximately 27% of global market revenue, led overwhelmingly by the United States. The U.S. contributes nearly 23% of total global herbal liqueur consumption, benefiting from sophisticated cocktail culture, premium spirits adoption, and strong hospitality industry demand. Canada continues to demonstrate steady growth through premium alcohol retail channels and expanding consumer interest in botanical beverages. Craft cocktail bars and mixology-focused establishments remain important growth drivers across the region.

Asia-Pacific

Asia-Pacific represents approximately 17% of global market revenue and is the fastest-growing regional market. China is the largest regional consumer and contributes nearly 5% of global demand. Rising disposable incomes, urbanization, and increasing exposure to international beverage trends are accelerating herbal liqueur adoption. India is emerging as an important growth market due to premium alcohol consumption growth and expanding hospitality infrastructure. Japan, South Korea, and Australia continue to exhibit strong demand for premium imported herbal spirits and cocktail-focused products.

Latin America

Latin America accounts for approximately 8% of global market revenue. Brazil and Mexico represent the largest regional markets, supported by growing premium alcohol consumption and expanding hospitality industries. Argentina and Chile are also experiencing rising demand for imported herbal liqueurs, particularly within premium urban consumer segments. Tourism-driven consumption and increasing cocktail culture adoption continue supporting regional market development.

Middle East & Africa

The Middle East & Africa region contributes approximately 3% of global herbal liqueur revenue. South Africa remains the largest market due to its developed hospitality sector and premium alcohol consumption patterns. The UAE serves as an important regional hub for luxury spirits consumption, supported by tourism and high-income consumer groups. Morocco and selected North African markets are also demonstrating gradual demand growth. Premium hospitality development and tourism investments remain key long-term growth catalysts across the region.

Key Players in the Herbal Liqueur Market

- Mast-Jägermeister SE

- Pernod Ricard

- Davide Campari-Milano N.V.

- The Liquor Barn

- Chartreuse Diffusion

- Gruppo Montenegro

- Stock Spirits Group

- Underberg AG

- Zwack Unicum Nyrt.

- Luxardo S.p.A.

- Becherovka

- Distillerie Bonollo

- Lucas Bols N.V.

- Maison Dolin

- Gammel Dansk Spirits