Hard Cider Market Size

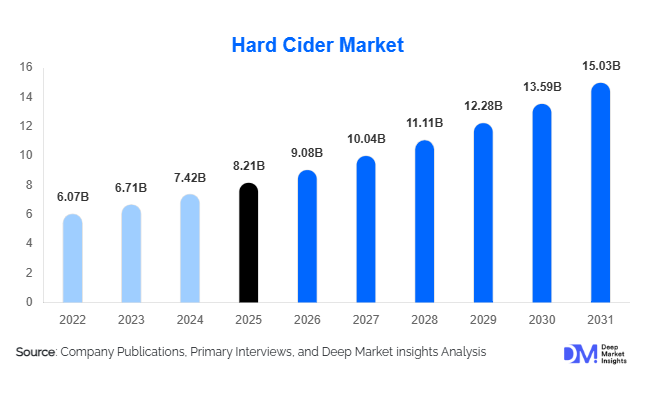

According to Deep Market Insights, the global hard cider market size was valued at USD 8.21 billion in 2025 and is projected to grow from USD 9.08 billion in 2026 to reach USD 15.03 billion by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The hard cider market growth is primarily driven by increasing consumer preference for flavored alcoholic beverages, rising demand for gluten-free alcohol alternatives, and expanding premium craft cider consumption across developed and emerging economies.

Key Market Insights

- Premium and craft hard cider products are witnessing strong global demand, supported by consumer preference for artisanal alcoholic beverages with natural ingredients and unique flavor profiles.

- Fruit-flavored hard cider continues to dominate product innovation, particularly berry, tropical, and citrus variants targeting millennials and Gen Z consumers.

- Europe dominates the global hard cider market, led by the U.K., France, and Spain due to established cider-drinking traditions and strong pub culture.

- Asia-Pacific is the fastest-growing regional market, driven by rising urbanization, westernized drinking habits, and expanding middle-class spending in China, India, Japan, and Australia.

- Off-trade retail channels account for the majority of global sales, supported by supermarkets, liquor chains, and rapidly growing online alcohol retail platforms.

- Technological advancements in fermentation, packaging, and flavor stabilization are improving product quality, shelf life, and manufacturing efficiency globally.

hard cider market latest trends

Premiumization and Craft Cider Expansion

The global hard cider industry is increasingly shifting toward premium and craft-based offerings as consumers seek authentic drinking experiences and differentiated flavor profiles. Craft cider manufacturers are introducing small-batch products made with specialty apple varieties, organic ingredients, and regional fermentation techniques. Premium hard cider products are also benefiting from growing demand for artisanal alcoholic beverages positioned as healthier and more natural alternatives to conventional beer. Barrel-aged ciders, botanical infusions, and limited-edition seasonal launches are becoming increasingly common across North America and Europe. Consumers are showing willingness to pay premium prices for locally sourced and sustainably produced products, enabling manufacturers to achieve higher profit margins and stronger brand loyalty.

Rising Popularity of Low-Alcohol and Health-Oriented Cider

Health-conscious drinking trends are significantly influencing product innovation in the hard cider market. Manufacturers are increasingly launching low-calorie, low-sugar, organic, and alcohol-free cider variants to attract consumers seeking moderation without compromising taste. Gluten-free positioning remains a major competitive advantage for hard cider compared to traditional beer products. Younger consumers are particularly attracted to clean-label alcoholic beverages with natural fruit ingredients and lower alcohol content. Companies are also investing in sustainable packaging solutions such as recyclable aluminum cans and lightweight bottles to align with environmentally conscious consumer preferences. Functional ingredients and botanical flavor enhancements are emerging as new areas of product differentiation globally.

hard cider market drivers

Growing Demand for Flavored Alcoholic Beverages

The increasing popularity of flavored alcoholic beverages is one of the primary drivers supporting hard cider market expansion globally. Consumers are increasingly shifting away from traditional beer and spirits toward fruit-based alcoholic drinks offering sweeter, lighter, and more refreshing taste profiles. Fruit-flavored hard cider products, particularly tropical, berry, and citrus variants, are gaining strong traction among younger demographics and casual alcohol consumers. Social drinking culture, premium ready-to-drink trends, and expanding product availability in bars and retail stores are further accelerating adoption. Beverage companies are continuously expanding flavor portfolios to improve consumer engagement and strengthen market differentiation.

Expansion of Craft Beverage Culture

The global rise of craft alcohol consumption is significantly boosting demand for artisanal hard cider products. Consumers increasingly value authenticity, local sourcing, and small-batch production methods, encouraging the growth of independent cider producers. Craft cider products are often perceived as premium alternatives with superior ingredient quality and innovative fermentation techniques. The trend is particularly strong in the United States, Canada, the United Kingdom, and Australia, where consumers actively seek locally produced alcoholic beverages. The expansion of taprooms, cider festivals, and direct-to-consumer sales channels is further strengthening market growth opportunities for craft producers.

global market restraints

Fluctuating Raw Material Prices

The hard cider industry remains highly dependent on apple production and specialty fruit concentrates, making it vulnerable to agricultural price volatility. Weather-related disruptions, crop disease, climate variability, and transportation costs can significantly impact raw material availability and production expenses. Rising costs for apples, packaging materials, and aluminum cans are pressuring profit margins, especially for small and medium-sized cider producers. Seasonal supply fluctuations can also create pricing instability within premium cider categories.

Alcohol Regulations and Taxation Challenges

Strict alcohol regulations and varying taxation frameworks across countries continue to restrain hard cider market expansion. Governments impose different licensing requirements, advertising restrictions, labeling regulations, and excise duties on alcoholic beverages, increasing operational complexity for global manufacturers. Marketing restrictions in certain regions limit brand promotion opportunities, while high alcohol taxes can reduce affordability and consumer demand. Regulatory uncertainty regarding online alcohol sales and cross-border distribution further complicates expansion strategies for international cider companies.

hard cider industry key opportunities

Expansion into Emerging Asia-Pacific Markets

Asia-Pacific presents substantial growth opportunities for hard cider manufacturers due to rising disposable incomes, urbanization, and changing consumer lifestyles. Countries such as China, India, Japan, and South Korea are witnessing increasing demand for premium flavored alcoholic beverages among younger urban populations. International beverage companies are expanding regional distribution partnerships and launching localized flavor variants tailored to regional preferences. Growth in organized retail, nightlife culture, and online alcohol delivery platforms is further supporting cider penetration across emerging economies. Early market entry strategies are expected to create long-term competitive advantages for global manufacturers.

Growth of Alcohol-Free and Functional Cider Products

The increasing popularity of alcohol moderation and wellness-oriented lifestyles is creating strong opportunities for alcohol-free and functional cider products. Consumers are seeking beverages that combine flavor, social consumption, and reduced alcohol intake. Manufacturers are introducing low-alcohol cider infused with botanical extracts, vitamins, and natural fruit ingredients to appeal to health-conscious buyers. This category is expected to gain significant traction in Europe and North America, where demand for non-alcoholic premium beverages is rising rapidly. The segment also offers opportunities for companies to expand beyond traditional alcohol consumers and access broader retail channels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.21 Billion |

| Market Size in 2026 | USD 9.08 Billion |

| Market Size in 2031 | USD 15.03 Billion |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fruit-flavored hard cider dominates the global market, accounting for the largest revenue share due to strong consumer preference for sweeter and more approachable alcoholic beverages. Berry, tropical, citrus, and mixed-fruit variants continue to witness rapid innovation and high consumer acceptance, particularly among millennials and Gen Z consumers. Traditional apple-based hard cider remains a strong category in Europe, especially in the U.K., France, and Spain, where cider consumption has deep cultural roots. Premium craft cider products are also expanding rapidly, supported by consumer demand for artisanal beverages with unique fermentation methods and locally sourced ingredients. Organic and low-calorie cider variants are gaining momentum globally as wellness-oriented drinking trends continue influencing purchasing decisions. Sparkling hard cider products are particularly popular in social and entertainment settings due to their refreshing taste profiles and premium packaging appeal.

Packaging Type Insights

Aluminum cans account for a substantial share of global hard cider packaging demand due to portability, convenience, sustainability, and strong preference in outdoor events and entertainment venues. Beverage companies are increasingly adopting slim-can premium packaging formats to improve brand differentiation and reduce transportation costs. Glass bottles remain highly popular in premium and artisanal cider categories, where traditional aesthetics and premium branding influence consumer purchasing behavior. Keg packaging continues to witness demand growth in bars, restaurants, and hospitality establishments due to increasing draft cider consumption. Sustainable and recyclable packaging solutions are becoming increasingly important purchasing considerations among environmentally conscious consumers, encouraging manufacturers to invest in eco-friendly materials and lightweight packaging technologies.

Distribution Channel Insights

Off-trade retail channels dominate global hard cider sales, contributing more than 60% of market revenues. Supermarkets, hypermarkets, liquor chains, and convenience stores continue expanding product visibility and accessibility for consumers worldwide. Online alcohol retail platforms are witnessing particularly strong growth due to convenience, broader product selection, and growing acceptance of digital alcohol purchasing. Direct-to-consumer channels are also gaining importance among craft cider manufacturers seeking stronger consumer engagement and higher margins. On-trade channels including bars, pubs, restaurants, breweries, and entertainment venues remain critical for premium product launches and experiential brand positioning. Social media marketing and influencer-driven alcohol promotion strategies are increasingly shaping purchasing behavior, particularly among younger demographics.

Consumer Demographic Insights

Millennials represent the largest consumer demographic in the hard cider market, driven by preference for flavored alcoholic beverages, premium experiences, and experimentation with alternative alcohol products. Gen Z consumers are rapidly emerging as a high-growth segment due to increasing interest in low-alcohol beverages, sustainable products, and innovative flavor combinations. Health-conscious consumers are significantly influencing demand for gluten-free, organic, and low-calorie cider variants. Premium adult consumers continue driving growth within the craft and super-premium categories, particularly in North America and Europe. Occasional alcohol consumers are also contributing to market expansion due to cider’s lighter flavor profile and perceived accessibility compared to beer and spirits.

Explore more data points, trends and opportunities Download Free Sample Report

Hard Cider Market Segmentations

By Product Type

- Traditional Hard Cider

- Fruit-Flavored Hard Cider

- Dry Hard Cider

- Semi-Dry Hard Cider

- Sweet Hard Cider

- Sparkling Hard Cider

- Still Hard Cider

- Organic Hard Cider

- Craft / Artisanal Hard Cider

- Low-Alcohol Hard Cider

- Alcohol-Free / Non-Alcoholic Cider

By Flavor Profile

- Apple-Dominant

- Pear Cider (Perry)

- Mixed Fruit Blend

- Spiced Cider

- Botanical / Herb-Infused

- Barrel-Aged / Oak-Aged

By Alcohol Content

- Below 3% ABV

- 3%–5% ABV

- 5%–7% ABV

- Above 7% ABV

By Packaging Type

- Glass Bottles

- Aluminum Cans

- PET Bottles

- Kegs

- Tetra Packs

By Distribution Channel

- On-Trade

- Bars & Pubs

- Restaurants

- Hotels

- Breweries & Taprooms

- Off-Trade

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Liquor Stores

- Online Retail

- Direct-to-Consumer Sales

Regional Insights

North America

North America accounts for nearly 31% of the global hard cider market, led primarily by the United States. The region continues benefiting from strong craft alcohol culture, premiumization trends, and increasing consumer preference for gluten-free alcoholic beverages. U.S. consumers are increasingly adopting flavored and canned cider products, particularly within younger demographics seeking alternatives to beer. Canada is also witnessing steady growth supported by premium imports and local craft cider production. Strong retail infrastructure, expanding e-commerce alcohol sales, and high consumer spending on premium beverages continue supporting regional market expansion.

Europe

Europe remains the dominant regional market, accounting for approximately 42% of global hard cider revenues in 2025. The United Kingdom represents the largest individual market globally due to established cider-drinking traditions and widespread pub consumption culture. France and Spain maintain strong artisanal cider industries supported by regional production heritage and tourism demand. Germany and Sweden are witnessing rising demand for craft cider and flavored alcoholic beverages among younger urban consumers. Europe also leads innovation in premium cider, organic production methods, and sustainable packaging technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 13% through 2031. Australia currently leads regional cider consumption due to high premium beverage spending and established cider-drinking culture. China and India represent major long-term growth opportunities driven by rising middle-class incomes, westernized drinking preferences, and rapid urbanization. Japan and South Korea are witnessing increasing demand for fruit-flavored alcoholic beverages among younger consumers. Expanding nightlife culture, organized retail development, and digital alcohol delivery services are significantly supporting regional market growth.

Latin America

Latin America is gradually emerging as a promising market for hard cider products, particularly in Brazil, Argentina, and Chile. Rising demand for fruit-based alcoholic beverages and increasing penetration of organized retail infrastructure are supporting consumption growth. Premium imported cider brands are gaining popularity among urban consumers seeking differentiated alcoholic beverage experiences. International manufacturers are increasingly targeting the region through localized marketing strategies and partnerships with beverage distributors.

Middle East & Africa

The Middle East & Africa region currently represents a smaller share of global hard cider demand but offers long-term growth potential in tourism-driven hospitality markets. South Africa remains the largest regional producer and consumer due to its developed alcoholic beverage industry and fruit production capabilities. Premium imported cider products are gaining visibility in the UAE and Saudi Arabia, particularly within hotels, restaurants, and entertainment venues catering to expatriate populations and international tourists. Increasing hospitality investments and expanding premium alcohol retail infrastructure are expected to support future market expansion.

Key Players in the Hard Cider Market

- Heineken N.V.

- C&C Group plc

- Carlsberg Group

- Asahi Group Holdings

- The Boston Beer Company

- Aston Manor Cider

- Thatchers Cider

- Molson Coors Beverage Company

- AB InBev

- Kopparbergs Bryggeri

- Carlton & United Breweries

- Suntory Holdings

- Vermont Cider Company

- Halewood Artisanal Spirits

- Ace Cider