Grape Brandy Market Size

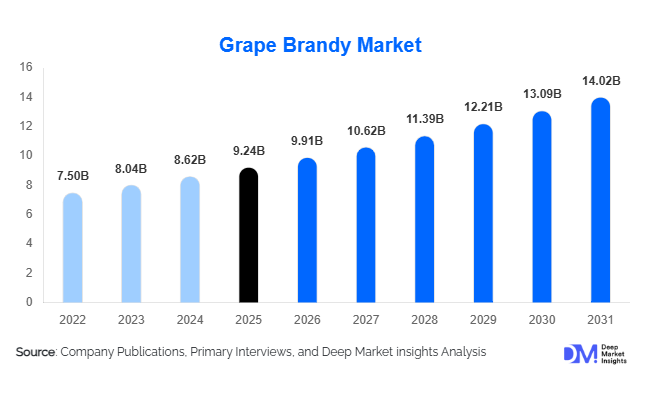

According to Deep Market Insights, the global grape brandy market size was valued at USD 9.24 billion in 2025 and is projected to grow from USD 9.91 billion in 2026 to reach USD 14.02 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The grape brandy market growth is primarily driven by rising premium spirits consumption, increasing consumer preference for aged alcoholic beverages, expanding cocktail culture, and growing demand for luxury and super-premium spirits across both developed and emerging economies. Strong heritage branding, premiumization trends, and increasing disposable incomes in Asia-Pacific and North America continue to support market expansion. In addition, travel retail growth, hospitality sector recovery, and increasing adoption of craft and artisanal spirits are creating favorable conditions for long-term demand growth in the global grape brandy industry.

Key Market Insights

- Premium and super-premium grape brandies are gaining significant market share, driven by consumers seeking higher-quality aged spirits and authentic production methods.

- Aged grape brandy remains the dominant product category, accounting for approximately 35% of global market revenue due to strong consumer preference for premium aged expressions.

- Europe dominates the global grape brandy market, supported by established production hubs in France and Spain and strong export demand worldwide.

- Asia-Pacific is the fastest-growing regional market, fueled by rising disposable incomes, premium alcohol consumption, and expanding middle-class populations.

- Cocktail and mixology applications are emerging as key growth drivers, particularly among younger consumers seeking innovative drinking experiences.

- Sustainability initiatives and vineyard traceability programs are becoming important competitive differentiators among leading producers.

Grape Brandy Market Latest Trends

Premiumization Reshaping Consumer Purchasing Behavior

The grape brandy market is experiencing a significant shift toward premium and luxury offerings. Consumers are increasingly willing to pay higher prices for products featuring longer aging periods, limited-edition releases, vineyard-specific sourcing, and traditional distillation methods. Premiumization is particularly evident in Asia-Pacific markets such as China, Japan, South Korea, and India, where affluent consumers increasingly view premium grape brandies as status symbols and gifting products. Producers are responding through expanded portfolios of XO, Extra Old, and reserve-aged products that command substantially higher margins than standard offerings. Luxury packaging, collectible bottles, and exclusive retail releases continue to strengthen premium positioning while supporting value growth across the industry.

Expansion of Cocktail and Mixology Applications

Modern cocktail culture is creating new consumption occasions for grape brandy. Premium bars, restaurants, and hospitality operators increasingly incorporate grape brandies into contemporary cocktail menus, broadening appeal beyond traditional neat consumption. Mixologists are utilizing grape brandy as a premium substitute for whiskey, rum, and cognac in both classic and innovative cocktails. Younger consumers are discovering grape brandy through these applications, helping producers attract demographics historically underrepresented within the category. Social media exposure, bartender education programs, and premium hospitality partnerships are accelerating adoption while supporting long-term market growth.

Grape Brandy Market Drivers

Growing Demand for Premium Spirits

The global shift toward premium alcoholic beverages remains one of the strongest growth drivers for the grape brandy market. Consumers increasingly prioritize quality, authenticity, and craftsmanship over volume consumption. Premium and super-premium grape brandies benefit from strong heritage narratives, aging credentials, and luxury positioning. As disposable incomes rise across major markets, consumers are trading up from standard spirits to aged and premium alternatives, creating substantial value growth opportunities for producers.

Expansion of Hospitality and Travel Retail Industries

The recovery and expansion of global tourism, luxury hospitality, and travel retail sectors are supporting increased grape brandy consumption. Hotels, fine-dining restaurants, airport duty-free stores, and premium lounges remain important channels for premium grape brandy sales. International travelers frequently purchase premium grape brandies as gifts or collectible products, particularly in major travel hubs across Europe, the Middle East, and Asia-Pacific. The expansion of luxury tourism continues to strengthen demand for high-end spirits globally.

Grape Brandy Market Restraints

Stringent Alcohol Regulations and Taxation

Government regulations governing alcohol advertising, distribution, labeling, and taxation remain significant challenges for market participants. High excise duties and import tariffs increase product prices in several countries, potentially limiting market penetration. Compliance requirements also vary considerably between jurisdictions, creating operational complexity for multinational producers and exporters.

Competition from Alternative Premium Spirits

The growing popularity of premium whiskey, tequila, gin, and rum categories continues to intensify competition for consumer spending. Younger consumers often display stronger brand engagement with these categories, requiring grape brandy producers to invest heavily in brand modernization, product innovation, and digital marketing initiatives to remain competitive.

Grape Brandy Industry Key Opportunities

Rapid Growth Across Asia-Pacific Markets

Asia-Pacific represents the largest untapped growth opportunity within the global grape brandy market. Rising middle-class populations, urbanization, increasing disposable incomes, and premium alcohol consumption trends are driving substantial demand growth across China, India, Vietnam, Thailand, and Indonesia. International producers are increasingly investing in localized distribution networks, premium retail channels, and brand-building initiatives to capture expanding consumer demand. The region is expected to contribute the highest incremental revenue growth through 2031.

Craft and Artisanal Grape Brandy Expansion

The growing consumer preference for authenticity and small-batch production creates opportunities for craft grape brandy producers. Consumers increasingly seek products featuring vineyard traceability, organic grapes, traditional distillation techniques, and unique regional identities. Craft and artisanal grape brandies command premium pricing while attracting consumers interested in differentiated drinking experiences. Strategic partnerships with vineyards, tourism operators, and specialty retailers can further enhance growth prospects for new market entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.24 Billion |

| Market Size in 2026 | USD 9.91 Billion |

| Market Size in 2031 | USD 14.02 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The aged grape brandy segment dominated the global grape brandy market and accounted for approximately 35% of total market revenue in 2025. Its leadership is primarily attributed to strong consumer preference for premium spirits that offer greater flavor depth, refined aging characteristics, and authentic heritage-driven brand positioning. The growing popularity of VSOP, XO, Napoléon, and extra-aged variants continues to support revenue expansion as these products command significantly higher average selling prices and enjoy strong demand among affluent consumers, collectors, and connoisseurs. Rising premiumization trends across both developed and emerging economies have further accelerated demand for aged expressions, with consumers increasingly prioritizing product quality, craftsmanship, provenance, and exclusivity over volume-based consumption. In addition, the expansion of luxury gifting culture, particularly in Asia-Pacific and the Middle East, has strengthened sales of premium aged grape brandies. While aged products remain the dominant category, flavored grape brandies and craft-produced variants are gaining traction among younger legal-age consumers seeking innovative flavor profiles and differentiated drinking experiences. The growth of artisanal distilleries, experimental barrel-aging techniques, and limited-edition releases is also creating new opportunities for product diversification and market expansion.

Price Tier Insights

The premium segment emerged as the leading price category and accounted for approximately 32% of global grape brandy revenue in 2025. The segment’s dominance is primarily driven by the ongoing premiumization trend across the alcoholic beverages industry, as consumers increasingly seek superior quality, authenticity, and brand prestige. Rising disposable incomes, growing consumer awareness of aged spirits, and expanding gifting culture have encouraged consumers to trade up from standard products to premium offerings. Premium grape brandies benefit from a favorable balance between affordability and luxury appeal, making them accessible to a broader consumer base while maintaining strong profit margins for manufacturers. Furthermore, increasing demand for experiential consumption, premium hospitality experiences, and high-end social occasions continues to strengthen segment growth. Super-premium and luxury categories are witnessing particularly robust expansion among high-net-worth individuals and affluent urban consumers across China, the United States, South Korea, Japan, and Gulf Cooperation Council countries. Meanwhile, economy and mid-range products remain essential for driving volume sales in emerging markets, where growing urbanization, rising alcohol consumption, and expanding retail accessibility continue to support category penetration.

Distribution Channel Insights

Off-trade retail channels represented approximately 55% of global grape brandy sales in 2025, making them the largest distribution segment worldwide. The segment’s leadership is primarily supported by widespread consumer preference for convenient purchasing options, competitive pricing, and broad product availability across supermarkets, hypermarkets, specialty liquor stores, convenience stores, and duty-free outlets. Consumers increasingly favor retail purchases for home consumption, gifting purposes, and personal collections, particularly within premium and aged product categories. The expansion of organized retail networks in emerging markets and the growing presence of premium spirits sections within modern retail formats have further enhanced market accessibility. Additionally, the rapid growth of online alcohol retailing is transforming purchasing behavior, supported by expanding digital commerce infrastructure, improved delivery logistics, and increasing consumer acceptance of e-commerce platforms. Although off-trade remains dominant, on-trade channels such as hotels, bars, restaurants, clubs, and premium lounges continue to play a critical role in product discovery, brand visibility, and premium brand positioning. The rising popularity of craft cocktails, luxury hospitality experiences, and premium dining establishments continues to support demand through on-premise consumption channels.

End-Use Insights

Direct consumption remained the largest end-use segment, accounting for approximately 60% of global grape brandy demand in 2025. The segment’s dominance is driven by strong consumer preference for enjoying grape brandy neat, on the rocks, or with minimal dilution in order to fully appreciate its aroma, flavor complexity, and aging characteristics. This consumption pattern is particularly prominent across Europe and North America, where established brandy-drinking traditions and mature premium spirits markets continue to support demand. The increasing availability of aged and premium products has further encouraged consumers to view grape brandy as a sipping spirit rather than a mixing ingredient. Meanwhile, cocktail and mixology applications represent the fastest-growing end-use category, supported by the expansion of premium bars, luxury hospitality venues, and evolving consumer interest in innovative craft cocktails. The growing influence of mixologists and premium cocktail culture is introducing grape brandy to younger consumer demographics and new consumption occasions. Culinary applications, including desserts, confectionery products, sauces, gourmet cooking, and food flavoring, continue to generate stable demand, while gifting, collecting, and investment-oriented purchases remain important contributors to the luxury and ultra-premium market segments.

Consumer Group Insights

Individual consumers accounted for approximately 64% of global grape brandy demand in 2025, making them the largest consumer group within the market. The segment’s leadership is primarily driven by increasing household consumption, rising interest in premium alcoholic beverages, and growing consumer appreciation for aged spirits. Personal purchases for leisure consumption, gifting occasions, celebrations, and private collections continue to support sustained demand growth across both developed and emerging markets. Rising disposable incomes, expanding urban populations, and greater exposure to premium beverage culture through social media and experiential marketing are further strengthening consumer participation. Hospitality buyers, including hotels, restaurants, bars, resorts, and entertainment venues, represent the second-largest consumer group and remain highly influential in driving product visibility, trial, and premium brand perception. Additionally, corporate gifting programs, institutional procurement, luxury event organizers, and travel retail operators contribute incremental demand, particularly during festive seasons, business events, and high-value social occasions.

Explore more data points, trends and opportunities Download Free Sample Report

Grape Brandy Market Segmentations

By Product Type

- Standard Grape Brandy

- Aged Grape Brandy

- Premium & Super-Premium Grape Brandy

- Craft / Artisanal Grape Brandy

- Flavored Grape Brandy

By Price Tier

- Economy

- Mid-Range

- Premium

- Super-Premium

- Luxury / Ultra-Premium

By Production Method

- Pot-Still Grape Brandy

- Column-Still Grape Brandy

- Blended Grape Brandy

- Single-Origin / Estate-Produced Grape Brandy

By Distribution Channel

- On-Trade

- Off-Trade

- Online Retail / E-Commerce

By Consumer Group

- Individual Consumers

- Hospitality Buyers

- Corporate / Institutional Buyers

- Travel Retail Consumers

Regional Insights

North America

North America accounted for approximately 18% of the global grape brandy market in 2025, with the United States representing the largest market across the region. Market growth is being driven by rising premium spirits consumption, expanding consumer interest in aged and craft alcoholic beverages, and the continued evolution of cocktail culture. Increasing consumer willingness to explore premium and artisanal products has encouraged demand for high-quality grape brandies across both retail and hospitality channels. The region also benefits from a well-developed distribution infrastructure, strong purchasing power, and growing adoption of e-commerce alcohol sales platforms. The rapid expansion of craft distilleries, premium hospitality establishments, luxury dining venues, and experiential beverage consumption trends continues to create favorable conditions for market growth. Canada contributes significantly through stable retail networks, growing premium alcohol consumption, and increasing demand for imported premium spirits.

Europe

Europe remained the largest regional market, accounting for approximately 42% of global grape brandy revenue in 2025. The region’s dominance is supported by its centuries-old brandy-making heritage, extensive vineyard resources, and strong consumer preference for premium aged spirits. France and Spain continue to lead both production and consumption due to their established grape-growing industries, globally recognized brandy appellations, and strong export capabilities. The presence of premium and luxury heritage brands further reinforces Europe's leadership position within the global market. Germany, Italy, and the United Kingdom also contribute substantial demand, particularly for premium, aged, and imported grape brandy products. Regional growth is additionally supported by high per-capita alcohol consumption, strong tourism activity, mature hospitality industries, and continued demand for premium spirits across domestic and international markets. Europe's sophisticated premium spirits ecosystem, established regulatory frameworks, and extensive global distribution networks continue to strengthen its market position.

Asia-Pacific

Asia-Pacific accounted for approximately 28% of global market share in 2025 and represents the fastest-growing regional market, with annual growth exceeding 8.5%. Rapid urbanization, rising disposable incomes, expanding middle-class populations, and accelerating premiumization trends are driving substantial market expansion throughout the region. China remains the largest regional market, supported by strong gifting traditions, increasing demand for imported luxury spirits, and growing consumer preference for premium alcoholic beverages. India is emerging as one of the fastest-growing markets globally due to increasing purchasing power, expanding young adult populations, rising exposure to international spirits brands, and growing demand for premium products in metropolitan areas. Japan and South Korea continue to generate robust demand for aged and luxury grape brandies, supported by sophisticated premium beverage cultures and strong appreciation for craftsmanship and quality. Additionally, Southeast Asian markets including Thailand, Vietnam, Indonesia, Malaysia, and the Philippines offer significant long-term growth potential due to increasing urbanization, expanding tourism industries, rising disposable incomes, and growing penetration of organized retail and e-commerce channels.

Latin America

Latin America represented approximately 7% of global grape brandy demand in 2025. Brazil and Mexico remain the region’s largest consuming markets, supported by expanding urban populations, improving economic conditions, and growing consumer interest in premium alcoholic beverages. Increasing exposure to international spirits brands through tourism, digital marketing, and global retail channels is encouraging greater product adoption among younger consumers and affluent urban households. The expansion of modern retail infrastructure, rising middle-class incomes, and the gradual premiumization of alcohol consumption patterns are further supporting market growth. Additionally, the development of hospitality, tourism, and entertainment sectors across major metropolitan centers is expected to create new opportunities for premium grape brandy sales throughout the forecast period.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5% of global market share in 2025. South Africa remains the region’s leading producer and consumer, benefiting from a well-established wine and spirits industry, favorable grape-growing conditions, and a strong domestic production base. Market growth across the region is increasingly supported by rising premium beverage consumption, expanding tourism activity, and growing investment in luxury hospitality infrastructure. Demand in the United Arab Emirates, Saudi Arabia, Qatar, and other Gulf countries is particularly driven by affluent consumers, international tourism, luxury hotels, fine dining establishments, and travel retail channels. The increasing presence of premium beverage retailers, expanding expatriate populations, and growing demand for high-end gifting products are also contributing to market development. Furthermore, improving distribution networks, urbanization trends, and the gradual expansion of premium consumer segments across key African economies are expected to support long-term market growth.

Key Players in the Grape Brandy Market

- Rémy Cointreau

- Pernod Ricard

- Emperador Inc.

- Diageo plc

- E. & J. Gallo Winery

- Bacardi Limited

- Davide Campari-Milano N.V.

- Torres Brandy

- Osborne Group

- Yantai Changyu Pioneer Wine Co.

- Distell Group

- Sazerac Company

- Stock Spirits Group

- Mohan Meakin Limited

- Radico Khaitan Limited