Gin Market Size

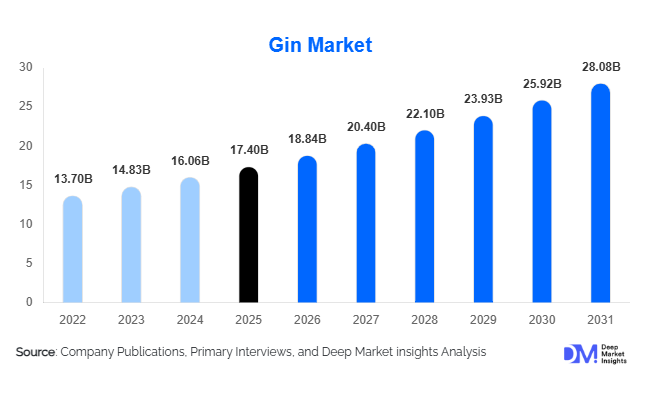

According to Deep Market Insights, the global gin market size was valued at USD 17.4 billion in 2025 and is projected to grow from USD 18.84 billion in 2026 to reach USD 28.08 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The gin market growth is primarily driven by increasing premium spirit consumption, the rapid expansion of cocktail culture, rising demand for flavored and craft gin variants, and the growing influence of experiential drinking trends among millennials and Gen Z consumers worldwide.

Key Market Insights

- Premium and super-premium gin categories are witnessing strong global demand, supported by rising consumer preference for artisanal and botanical alcoholic beverages.

- Flavored gin and pink gin are rapidly expanding, particularly among younger demographics seeking innovative and fruit-infused alcohol experiences.

- Europe dominates the global gin market, led by strong consumption and production across the U.K., Spain, Germany, and the Netherlands.

- Asia-Pacific is the fastest-growing regional market, supported by urbanization, rising disposable incomes, and westernized nightlife culture in India, China, Japan, and Southeast Asia.

- Off-trade retail and online alcohol sales channels are expanding rapidly, improving accessibility for premium and niche craft gin brands globally.

- Sustainability and innovation are reshaping the industry, with manufacturers investing in eco-friendly packaging, organic botanicals, and low-calorie formulations.

gin market latest trends

Premium and Craft Gin Expansion

The gin industry is increasingly shifting toward premium and craft-oriented offerings as consumers seek differentiated flavor experiences and artisanal authenticity. Craft distilleries are experimenting with localized botanicals, small-batch production methods, and limited-edition releases to create unique brand identities. Consumers are willing to pay premium prices for high-quality botanical blends, heritage branding, and luxury packaging formats. Premiumization has become especially prominent across Europe and North America, while emerging economies are witnessing rising demand for imported premium spirits. Distilleries are also investing in experiential tourism through tasting rooms, distillery tours, and cocktail workshops to strengthen consumer engagement and brand loyalty. The growing popularity of organic and sustainably sourced ingredients is further influencing premium gin positioning globally.

Flavored and Low-Calorie Gin Innovations

Manufacturers are aggressively expanding flavored gin portfolios to capture younger and health-conscious consumers. Fruit-infused, floral, herbal, and citrus-based gin products are becoming mainstream across global retail shelves and hospitality venues. Pink gin remains one of the fastest-growing sub-categories due to its visual appeal and sweeter flavor profile. At the same time, low-calorie and lower-ABV gin variants are gaining traction among consumers seeking moderation and wellness-oriented drinking habits. Ready-to-drink gin cocktails are also expanding rapidly, particularly in convenience retail and e-commerce channels. Digital marketing campaigns and social media-led branding strategies are accelerating consumer experimentation with innovative gin products, especially among millennials and Gen Z populations.

gin market drivers

Growth of Cocktail Culture and Urban Nightlife

The increasing popularity of cocktail culture globally is a major driver of gin market growth. Gin-based cocktails such as martinis, negronis, and gin & tonic beverages continue to gain popularity across bars, restaurants, luxury hotels, and nightlife venues. Urban consumers increasingly prefer premium cocktail experiences, encouraging hospitality operators to expand gin selections and introduce botanical mixology concepts. The expansion of luxury hospitality infrastructure, nightlife tourism, and premium dining experiences across Asia-Pacific, Europe, and North America is further accelerating demand for premium gin products. Additionally, social media-driven cocktail trends are improving product visibility and encouraging consumer experimentation with new gin flavors and serving styles.

Rising Demand for Premium Alcoholic Beverages

Global consumers are increasingly prioritizing quality, authenticity, and premium experiences over high-volume alcohol consumption. This trend has significantly benefited the gin market, particularly the super-premium and craft gin segments. Consumers are willing to spend more on artisanal spirits with unique botanical compositions, sustainable sourcing, and premium packaging. Distillers are leveraging this shift by introducing limited-edition releases, aged gin variants, and region-specific botanical blends. Emerging middle-class populations in Asia-Pacific and Latin America are also increasingly adopting premium western alcoholic beverages, creating new growth opportunities for international gin manufacturers.

global market restraints

Regulatory and Taxation Pressures

The gin industry faces increasing regulatory scrutiny related to alcohol marketing, advertising restrictions, excise duties, and public health policies. Several countries are implementing stricter alcohol labeling requirements and higher taxes on spirits consumption, which can impact pricing competitiveness and consumption growth. Advertising limitations on digital and broadcast platforms also reduce promotional flexibility for brands. These regulatory complexities vary across regions, making international market expansion increasingly challenging for both established and emerging players.

Raw Material and Supply Chain Volatility

Gin production depends heavily on grains, botanicals, glass packaging, and imported flavor ingredients, all of which are exposed to supply chain disruptions and inflationary pressures. Rising agricultural input costs, energy prices, transportation expenses, and packaging shortages have increased operational costs for manufacturers. Smaller craft distillers are particularly vulnerable due to limited procurement scale and weaker pricing power. Climate-related disruptions affecting botanical crop availability are also creating supply inconsistencies, especially for premium and specialty gin formulations.

gin industry key opportunities

Expansion in Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East present significant growth opportunities for gin manufacturers. Countries such as India, China, Vietnam, Thailand, and the UAE are witnessing rising disposable incomes, expanding urban nightlife, and increasing exposure to western drinking culture. International brands are actively expanding premium portfolios in these regions through strategic distribution partnerships, hospitality collaborations, and localized marketing campaigns. Premium gin is increasingly viewed as a lifestyle product among younger urban consumers in emerging economies, creating long-term demand potential for global spirits companies.

Digital Retail and Direct-to-Consumer Growth

The rapid expansion of online alcohol retailing and direct-to-consumer platforms is reshaping the global gin market. Consumers increasingly prefer digital purchasing channels that offer convenience, product variety, transparent pricing, and personalized recommendations. Premium and craft gin brands are leveraging e-commerce platforms, subscription clubs, and virtual tasting experiences to strengthen direct customer engagement. Social commerce and influencer-led marketing are also driving online visibility for niche and artisanal brands. This digital transformation allows smaller distillers to compete more effectively against multinational companies by accessing broader global consumer bases without relying solely on traditional retail distribution networks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.40 Billion |

| Market Size in 2026 | USD 18.84 Billion |

| Market Size in 2031 | USD 28.08 Billion |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

London Dry Gin dominates the global market, accounting for nearly 34% of overall revenue due to its widespread consumer familiarity, versatility in cocktails, and strong presence across both premium and mainstream alcohol portfolios. Premium and super-premium variants continue to drive value growth within this segment, particularly across Europe and North America. Flavored gin, including fruit-infused, citrus, floral, and spice-based variants, is emerging as one of the fastest-growing categories, supported by rising experimentation among younger consumers. Pink gin has become especially popular among millennials and female consumers due to its sweeter profile and visual appeal. Craft and artisanal gin products are also gaining strong momentum as consumers increasingly seek small-batch authenticity, localized botanicals, and premium drinking experiences.

Application Insights

Household consumption represents a significant share of global gin demand, supported by rising home cocktail culture and growing online alcohol retail penetration. The hospitality industry remains the dominant commercial application segment, with bars, restaurants, hotels, and luxury resorts driving substantial premium gin consumption globally. Cocktail and mixology applications are expanding rapidly as consumers increasingly seek premium gin-based beverages in social settings. Travel retail and duty-free channels are also recovering strongly due to international tourism growth, particularly for luxury and gifting-oriented gin products. Corporate events, premium catering, and experiential nightlife venues continue to create additional demand for premium and limited-edition gin variants.

Distribution Channel Insights

Off-trade channels account for the majority of global gin sales, supported by supermarkets, specialty liquor stores, and expanding e-commerce platforms. Online alcohol retailing has emerged as a major growth driver due to changing consumer purchasing behavior and improved home delivery infrastructure. Premium and craft gin brands increasingly rely on direct-to-consumer sales channels to improve margins and strengthen customer engagement. On-trade channels, including bars, pubs, restaurants, and luxury hospitality venues, remain critical for brand visibility and premium positioning. Cocktail culture expansion and nightlife tourism recovery are supporting strong rebound growth in on-trade gin consumption across major urban markets.

Consumer Demographic Insights

Millennials represent the leading consumer demographic in the global gin market, accounting for nearly 37% of total consumption value. This segment is strongly influenced by cocktail culture, social media trends, premium experiences, and flavored spirit experimentation. Generation Z consumers are increasingly contributing to flavored gin and ready-to-drink product demand, particularly through digital retail channels. High-income urban consumers remain key drivers of premium and super-premium gin growth globally. Female consumers are also becoming increasingly important within flavored and pink gin categories, while older demographics continue to support traditional London Dry and premium botanical gin consumption.

Packaging Type Insights

Glass bottle packaging dominates the gin market with more than 82% share due to its premium aesthetic appeal, product preservation benefits, and strong association with luxury spirits. Manufacturers increasingly utilize customized bottle designs, embossed branding, and premium labeling to differentiate products within competitive retail environments. Sustainable and refillable packaging formats are gaining traction as environmental concerns influence purchasing decisions. Aluminum cans and ready-to-drink packaging solutions are also expanding rapidly, particularly within convenience retail and outdoor consumption applications. Eco-friendly packaging innovation is expected to become a major competitive differentiator among premium gin brands over the coming years.

Explore more data points, trends and opportunities Download Free Sample Report

Gin Market Segmentations

By Product Type

- London Dry Gin

- Plymouth Gin

- Old Tom Gin

- Genever Gin

- New Western / Contemporary Gin

- Navy Strength Gin

- Flavored Gin

- Pink Gin

- Barrel-Aged Gin

- Organic & Craft Gin

- Non-Alcoholic Gin Alternatives

By Price Category

- Economy Gin

- Mid-Range Gin

- Premium Gin

- Super-Premium Gin

- Ultra-Premium & Luxury Gin

By Alcohol Content

- Below 35% ABV

- 35%–40% ABV

- 40%–45% ABV

- Above 45% ABV

By Distribution Channel

- On-Trade

- Off-Trade

- Supermarkets & Hypermarkets

- Specialty Liquor Stores

- Convenience Stores

- Online Retail & E-Commerce

- Direct-to-Consumer Channels

By Consumer Demographics

- Millennials

- Generation Z

- Generation X

- Baby Boomers

- High-Income Consumers

- Urban Consumers

- Cocktail Enthusiasts

- Health-Conscious Consumers

Regional Insights

North America

North America accounts for approximately 26% of the global gin market, led primarily by the United States. The region benefits from strong cocktail culture, rising premium spirit consumption, and rapid growth of craft distilleries. U.S. consumers increasingly prefer botanical and artisanal gin products, while luxury hospitality and nightlife sectors continue to stimulate premium demand. Canada is also witnessing growing demand for flavored and craft gin variants, supported by rising consumer experimentation and premium alcohol spending.

Europe

Europe remains the largest regional market, representing nearly 41% of global revenue in 2025. The United Kingdom dominates global gin production and consumption due to its strong heritage, extensive craft distillery ecosystem, and high consumer familiarity with gin-based cocktails. Spain remains one of the largest per-capita gin consumption markets globally, driven by premium gin-and-tonic culture. Germany, France, Italy, and the Netherlands continue to support strong premium spirit demand due to tourism, urban nightlife expansion, and growing consumer preference for botanical alcoholic beverages.

Asia-Pacific

Asia-Pacific is projected to register the fastest growth rate during the forecast period, with CAGR exceeding 10%. India and China are emerging as major consumption centers due to rising disposable income, westernized drinking patterns, and expanding hospitality industries. Australia and Japan remain mature premium gin markets with strong craft distillation ecosystems and growing demand for artisanal products. Southeast Asian countries including Thailand, Vietnam, and Singapore are witnessing increasing premium alcohol adoption driven by tourism growth and urban nightlife development.

Latin America

Latin America is gradually emerging as a growth market for premium gin products. Brazil remains the leading regional consumer due to rising urbanization, premium spirit adoption, and expanding nightlife culture. Argentina and Chile are also witnessing increasing demand for imported flavored and botanical gin products among younger consumers. International brands are strengthening regional distribution partnerships to capitalize on growing premium alcohol demand across major urban centers.

Middle East & Africa

The Middle East & Africa market is expanding steadily due to luxury tourism, expatriate populations, and premium hospitality investments. The UAE remains the largest premium spirits market in the region, supported by tourism and luxury nightlife infrastructure. South Africa continues to strengthen its domestic craft gin production industry while also expanding exports to international markets. Rising tourism investments across Saudi Arabia and other Gulf economies are expected to support long-term premium spirit demand growth.

Key Players in the Gin Market

- Diageo

- Pernod Ricard

- Bacardi Limited

- William Grant & Sons

- Beam Suntory

- Brown-Forman

- Davide Campari-Milano

- Rémy Cointreau

- Lucas Bols

- Sazerac Company

- Stock Spirits Group

- Inver House Distillers

- San Miguel Corporation

- Langley Distillery

- The East India Company Spirits