Fried Chicken Powder Market Size

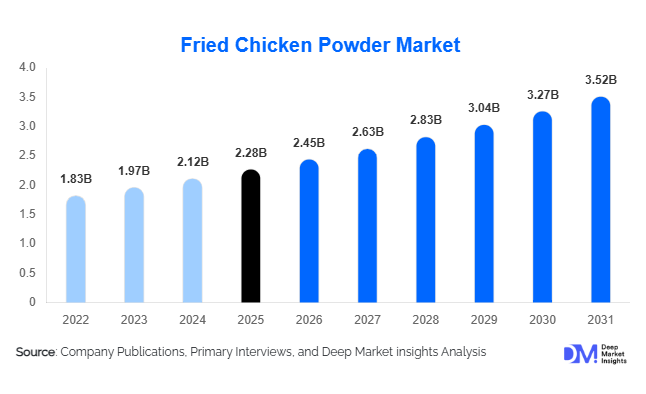

According to Deep Market Insights, the global fried chicken powder market size was valued at USD 2.28 billion in 2025 and is projected to grow from USD 2.45 billion in 2026 to reach USD 3.52 billion by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The fried chicken powder market growth is primarily driven by rising global consumption of fried poultry products, expansion of quick-service restaurant (QSR) chains, increasing production of frozen and ready-to-cook chicken products, and growing demand for standardized coating solutions among food processors. Fried chicken powders, including breading mixes, batter coatings, pre-dust formulations, and seasoning premixes, have become essential ingredients in commercial poultry preparation, enabling manufacturers and foodservice operators to deliver consistent texture, flavor, appearance, and crispness across high-volume production environments.

Key Market Insights

- Complete fried chicken coating premixes account for the largest product segment, representing approximately 34% of the global market due to operational simplicity and consistency advantages.

- Quick-service restaurants remain the largest end-user segment, contributing nearly 36% of total demand through large-scale fried chicken production.

- Asia-Pacific dominates the global market, accounting for approximately 34% of global revenue, supported by rapid urbanization and increasing poultry consumption.

- India is the fastest-growing major country market, projected to expand at over 10% CAGR through 2031 owing to strong QSR expansion and rising disposable incomes.

- Frozen poultry manufacturers are emerging as a major growth engine, driven by expanding retail demand for ready-to-cook and convenience food products.

- Advanced coating technologies, including low-oil absorption coatings, air-fryer-compatible formulations, and crispness-retention systems, are becoming major competitive differentiators.

Fried Chicken Powder Market Latest Trends

Growth of Air Fryer Compatible Coating Systems

The rapid adoption of air fryers across North America, Europe, and Asia-Pacific is reshaping product development strategies within the fried chicken powder industry. Manufacturers are introducing specialized coating systems designed to achieve traditional fried chicken texture and appearance while using significantly less oil. These coatings provide enhanced browning characteristics, improved adhesion, and prolonged crispness retention under alternative cooking methods. Food processors are increasingly incorporating air-fryer-compatible formulations into frozen chicken nuggets, tenders, wings, and ready-to-cook product portfolios. As consumers continue seeking healthier convenience foods, coating suppliers are investing heavily in R&D to optimize performance under air-frying conditions without compromising sensory attributes.

Rise of Customized Regional Flavor Profiles

Consumer demand for localized taste experiences is driving the development of region-specific fried chicken coating solutions. Suppliers are increasingly offering customized seasoning blends incorporating local spices, herbs, and flavor profiles tailored to specific markets. Spicy Korean-style coatings, Southeast Asian garlic-pepper blends, Middle Eastern spice mixes, and Latin American chili-based formulations are gaining traction among both foodservice operators and food manufacturers. Global restaurant chains are also leveraging localized flavor innovation to differentiate menus and increase customer engagement. This trend is expanding opportunities for ingredient suppliers capable of delivering customized formulations while maintaining consistency across large-scale production networks.

Fried Chicken Powder Market Drivers

Expansion of Global Quick-Service Restaurant Networks

The continued growth of international and regional fried chicken chains remains one of the strongest growth drivers for the market. Major brands are expanding aggressively across Asia-Pacific, Latin America, the Middle East, and Africa, creating sustained demand for industrial-scale coating systems. Standardized fried chicken powders enable restaurant operators to maintain consistent product quality across thousands of outlets while reducing preparation complexity and labor requirements. Emerging markets such as India, Indonesia, Vietnam, Saudi Arabia, and the Philippines are witnessing particularly strong outlet expansion, generating significant opportunities for coating suppliers.

Increasing Consumption of Frozen and Ready-to-Cook Poultry Products

The global shift toward convenience foods is fueling growth in frozen chicken nuggets, tenders, wings, strips, and popcorn chicken products. Food processors increasingly rely on advanced breading and batter systems to enhance product quality, optimize manufacturing efficiency, and improve shelf-life stability. The expansion of cold-chain infrastructure, particularly in developing economies, is further supporting demand for value-added poultry products that utilize fried chicken coating technologies.

Fried Chicken Powder Market Restraints

Volatility in Raw Material Prices

The market remains vulnerable to fluctuations in the prices of wheat flour, corn flour, starches, spices, seasonings, and edible oils. Supply chain disruptions, adverse weather conditions, and geopolitical uncertainties can significantly impact ingredient costs, creating pricing pressures for manufacturers. Margin compression remains a challenge for suppliers operating in highly competitive and price-sensitive markets.

Growing Health Concerns Regarding Fried Foods

Increasing consumer awareness regarding obesity, cardiovascular health, and calorie consumption presents a long-term challenge for fried food categories. Although fried chicken remains highly popular globally, some consumers are shifting toward healthier protein alternatives and lower-fat cooking methods. Manufacturers must continuously innovate through reduced-oil absorption coatings, clean-label formulations, and healthier ingredient alternatives to sustain long-term growth.

Fried Chicken Powder Industry Key Opportunities

Expansion Across Emerging Market Foodservice Channels

Rapid growth in organized foodservice across Asia-Pacific, the Middle East, and Africa presents significant opportunities for coating suppliers. The increasing penetration of international and domestic QSR brands is generating demand for customized breading and batter systems tailored to local consumer preferences. Countries such as India, Indonesia, Saudi Arabia, Vietnam, and Egypt are witnessing substantial growth in commercial fried chicken consumption. Companies capable of establishing local manufacturing capabilities and regional flavor development centers can secure long-term supply agreements with restaurant chains and food processors. The relatively low penetration of premium coating technologies in these markets further enhances growth potential.

Premiumization and Clean-Label Product Development

Consumers increasingly seek products containing natural ingredients, recognizable labels, and fewer artificial additives. This trend creates substantial opportunities for premium coating systems that deliver superior texture performance while meeting clean-label requirements. Manufacturers are introducing non-GMO formulations, gluten-free coatings, natural spice blends, and reduced-sodium products to capture evolving consumer demand. Premium coatings offering extended crispness retention and lower oil absorption command higher margins and create differentiation opportunities within mature markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.28 Billion |

| Market Size in 2026 | USD 2.45 Billion |

| Market Size in 2031 | USD 3.52 Billion |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The complete fried chicken coating premix segment dominated the global fried chicken powder market in 2025, accounting for approximately 34% of total demand. The segment’s leadership is primarily attributed to the growing preference among quick-service restaurants, foodservice operators, and poultry processors for integrated coating solutions that combine batter, breading, seasoning, and adhesion functionalities into a single formulation. These all-in-one systems help reduce preparation time, minimize formulation errors, improve product consistency, and enhance operational efficiency, making them particularly attractive for large-scale commercial food production. The increasing emphasis on standardization across restaurant chains and centralized food manufacturing facilities continues to reinforce demand for complete premix solutions.Batter mix powders continue to gain market traction as poultry processors increasingly adopt automated production systems and high-throughput manufacturing lines. These formulations provide superior coating adhesion, improved moisture retention, and consistent product appearance, making them essential for industrial-scale processing operations. The rising production of frozen ready-to-cook and ready-to-eat poultry products is further accelerating demand for advanced batter technologies.Marinade powders and pre-dust coatings remain important components within multi-stage coating systems, particularly in premium fried chicken applications. These products enhance flavor penetration, coating adhesion, and moisture retention while contributing to overall sensory performance. Growing consumer demand for restaurant-quality texture and flavor experiences is encouraging manufacturers to incorporate increasingly sophisticated pre-dust and marinade formulations into premium product offerings.

Flavor Profile Insights

Original and classic flavor formulations accounted for approximately 38% of global market demand in 2025, making them the leading flavor category. The segment's dominance is driven by the enduring popularity of traditional fried chicken recipes and the widespread presence of flagship menu offerings across major restaurant chains. Consumers continue to associate classic seasoning profiles with authenticity, familiarity, and consistent taste experiences, supporting stable long-term demand across foodservice and retail channels.Regional and ethnic flavor profiles are also experiencing significant growth as foodservice operators seek to localize menu offerings and strengthen consumer engagement. Asian-inspired seasonings, Latin American spice blends, Middle Eastern flavor profiles, and fusion concepts are becoming increasingly prominent across international markets. This trend is particularly evident in Asia-Pacific and Latin America, where localized taste preferences play a crucial role in product acceptance and brand differentiation.Customized proprietary seasoning blends developed for large foodservice operators and restaurant chains continue to expand in importance. These exclusive formulations enable brands to establish unique flavor identities, improve customer loyalty, and differentiate themselves within highly competitive fried chicken markets. The growing emphasis on menu innovation and brand exclusivity is expected to further stimulate demand for customized coating and seasoning systems.

Application Insights

Bone-in fried chicken remained the largest application segment in 2025, accounting for approximately 31% of global demand. The segment’s leadership is driven by the continued popularity of traditional fried chicken products across quick-service restaurants, casual dining establishments, and independent foodservice outlets. Strong consumer preference for authentic fried chicken experiences, combined with the widespread availability of bone-in menu offerings, continues to support substantial demand for breading, batter, and seasoning solutions specifically designed for this category.Frozen ready-to-cook and ready-to-eat chicken products constitute one of the fastest-growing application areas. Growth is supported by expanding retail distribution networks, rising consumer preference for convenient meal solutions, and increasing demand for products that offer restaurant-quality experiences at home. Manufacturers are increasingly investing in advanced coating technologies that maintain crispiness and sensory performance after freezing, storage, and reheating.Plant-based chicken alternatives remain a relatively small but rapidly expanding application segment. Manufacturers are utilizing innovative coating systems to replicate the texture, appearance, and eating characteristics of conventional fried chicken products. Rising consumer interest in alternative proteins, flexitarian diets, and sustainable food options is expected to create new growth opportunities for coating ingredient suppliers serving this emerging category.

Distribution Channel Insights

Direct industrial sales dominated the global market in 2025, accounting for approximately 44% of total revenue. The segment’s leadership is largely driven by procurement practices among large poultry processors, multinational restaurant chains, and frozen food manufacturers that require consistent product quality, technical support, and reliable supply arrangements. Long-term supply agreements enable buyers to secure formulation consistency while allowing suppliers to maintain stable production volumes and strategic customer relationships.Foodservice distributors continue to play a critical role in market development by serving regional restaurant chains, independent foodservice operators, catering companies, and institutional kitchens. These distribution networks provide access to a broad range of coating solutions while facilitating inventory management and logistics support for customers that may not purchase directly from manufacturers.Cash-and-carry wholesale channels remain important for small and medium-sized foodservice establishments that require flexible purchasing volumes and immediate product availability. The segment benefits from the growing number of independent restaurants and local foodservice businesses across emerging economies.Modern retail and e-commerce channels are gradually expanding their presence within the market as household consumers increasingly seek professional-grade coating products for home preparation. Digital procurement platforms are also transforming business-to-business purchasing by improving order visibility, streamlining supply chain management, reducing transaction costs, and enhancing overall procurement efficiency throughout the industry.

End-Use Insights

Quick-service restaurants (QSRs) represented the largest end-use segment in 2025, accounting for approximately 36% of global demand. The segment’s dominance is driven by the rapid expansion of fried chicken chains, increasing consumer preference for convenient dining options, and the need for highly standardized food preparation processes. QSR operators rely heavily on advanced coating systems to ensure consistent flavor, texture, appearance, and cooking performance across large restaurant networks, making them major purchasers of industrial breading and batter solutions.Frozen food manufacturers are projected to be the fastest-growing end-use category during the forecast period. Rising consumer demand for convenience foods, busy lifestyles, increasing freezer penetration, and expanding retail distribution of ready-to-cook poultry products are collectively driving growth. Manufacturers are increasingly adopting specialized coating technologies that preserve product quality throughout freezing, transportation, and reheating processes.Independent restaurants, catering operators, institutional kitchens, and household consumers continue to generate stable demand across both developed and emerging markets. Growing interest in home cooking, restaurant-inspired meal preparation, and premium packaged coating products is further contributing to the expansion of retail-oriented demand.

Explore more data points, trends and opportunities Download Free Sample Report

Fried Chicken Powder Market Segmentations

By Product Type

- Fried Chicken Breading Powder

- Fried Chicken Batter Mix Powder

- Complete Fried Chicken Coating Premix

- Marinade & Pre-Dust Powder

By Flavor Profile

- Original/Classic Flavor

- Spicy Flavor

- Hot & Crispy Flavor

- Garlic Flavor

- Pepper Flavor

- BBQ Flavor

- Regional/Ethnic Flavor Variants

- Customized Proprietary Blends

By Ingredient Category

- Wheat-Based Powder

- Corn-Based Powder

- Rice-Based Powder

- Multi-Grain Based Powder

- Gluten-Free Formulations

- Clean Label/Natural Ingredient Formulations

By Functional Performance

- Standard Frying Coatings

- Low Oil Absorption Coatings

- High Crispness Retention Coatings

- Freeze-Thaw Stable Coatings

- Air Fryer Compatible Coatings

- Oven-Bake Compatible Coatings

By Application

- Bone-In Fried Chicken

- Chicken Fillets

- Chicken Nuggets

- Chicken Tenders/Strips

- Popcorn Chicken

- Chicken Wings

- Ready-to-Cook Fried Chicken Products

- Plant-Based Chicken Alternatives

Regional Insights

North America

North America accounted for approximately 31% of global market revenue in 2025, positioning it among the largest regional markets for fried chicken powder. The United States represented nearly 27% of global demand, supported by high per-capita poultry consumption, widespread quick-service restaurant penetration, and a highly developed frozen food industry. Strong demand from major fried chicken restaurant chains and large poultry processors continues to drive consumption of industrial breading, batter, and seasoning systems.Regional growth is being supported by increasing consumer demand for premium fried chicken products, continuous menu innovation among restaurant chains, growing consumption of frozen convenience foods, and expanding adoption of air-fryer-compatible coating technologies. The region is also witnessing rising demand for clean-label formulations, reduced-additive ingredients, and gluten-free coating systems as health-conscious consumers seek products with improved ingredient transparency. Canada contributes additional market growth through ongoing expansion in food processing activities, investments in poultry production, and increasing consumption of value-added poultry products.

Asia-Pacific

Asia-Pacific led the global market with approximately 34% market share in 2025 and remains the fastest-growing regional market. China represents the largest country market within the region, accounting for nearly 12% of global demand due to strong poultry consumption, rapid expansion of foodservice establishments, and increasing adoption of western-style dining concepts. India is projected to be the fastest-growing major market, supported by rising disposable incomes, accelerating urbanization, growing youth demographics, and double-digit expansion of organized foodservice networks.Regional growth is being driven by rapid urban population expansion, increasing consumption of convenience foods, growing penetration of international and domestic quick-service restaurant chains, rising household incomes, and changing dietary preferences toward protein-rich foods. The popularity of fried chicken among younger consumers, combined with increasing investments in food processing infrastructure and cold-chain logistics, is creating substantial opportunities for coating ingredient suppliers. Countries such as Indonesia, Thailand, Vietnam, and the Philippines are witnessing strong growth as westernized eating habits continue to gain acceptance while local flavor customization drives product innovation.

Europe

Europe accounted for approximately 22% of global market revenue in 2025. Major demand centers include the United Kingdom, Germany, France, Spain, Poland, and the Netherlands. The region benefits from a mature food processing industry, strong frozen poultry production capabilities, and increasing demand for premium convenience foods. Manufacturers are increasingly focusing on innovative coating technologies that align with consumer expectations regarding quality, texture, and ingredient transparency.Regional growth is supported by rising demand for ready-to-cook poultry products, increasing consumption of convenience meals, growing preference for premium and artisanal food offerings, and continued expansion of private-label frozen food categories. Clean-label trends, demand for gluten-free formulations, and growing interest in healthier preparation methods are encouraging innovation in coating ingredient development. Poland has emerged as a strategically important poultry processing hub, while Western European markets continue to drive demand for high-performance and value-added coating solutions.

Latin America

Latin America is primarily led by Brazil and Mexico, both of which benefit from large poultry industries and steadily increasing consumption of fried chicken products. Brazil’s position as one of the world's leading poultry producers and exporters generates significant demand for industrial coating systems used in value-added poultry processing. Mexico continues to experience strong growth in quick-service restaurant penetration, urban food consumption, and frozen food demand.Regional market expansion is being driven by rising urbanization, improving disposable incomes, increasing consumer preference for affordable protein sources, and ongoing growth of international restaurant chains. Expanding investments in poultry processing infrastructure and greater availability of convenience food products are further supporting demand. Additionally, the growing influence of local flavor preferences is encouraging manufacturers to develop region-specific seasoning and coating formulations that cater to evolving consumer tastes.

Middle East & Africa

The Middle East and Africa region represents an emerging growth market for fried chicken powder, supported by expanding foodservice sectors and rising poultry consumption. Saudi Arabia and the United Arab Emirates constitute the largest demand centers, benefiting from strong consumer spending, high restaurant density, and significant presence of international quick-service restaurant brands. South Africa and Egypt also contribute substantially to regional demand through expanding food manufacturing and poultry processing activities.Regional growth is being driven by rapid population growth, increasing urbanization, rising disposable incomes, growing tourism activity, and expanding investments in food manufacturing infrastructure. The increasing popularity of western-style fast food, improving cold-chain logistics, and rising demand for convenience-oriented meal solutions are creating favorable conditions for market expansion. Furthermore, government initiatives aimed at strengthening domestic food production and food security are encouraging investments in poultry processing capacity, supporting long-term demand for advanced coating and seasoning systems throughout the region.

Key Players in the Fried Chicken Powder Market

- Kerry Group

- Newly Weds Foods

- Bowman Ingredients

- Blendex Company

- Breading & Coating Ltd

- House-Autry Mills

- Showa Sangyo

- Associated British Foods

- McCormick & Company

- Ajinomoto

- BRATA Produktions

- Thai Nisshin Technomic

- Arcadia Foods

- Bunge

- Shimakyu