Engineering Insurance Market Size

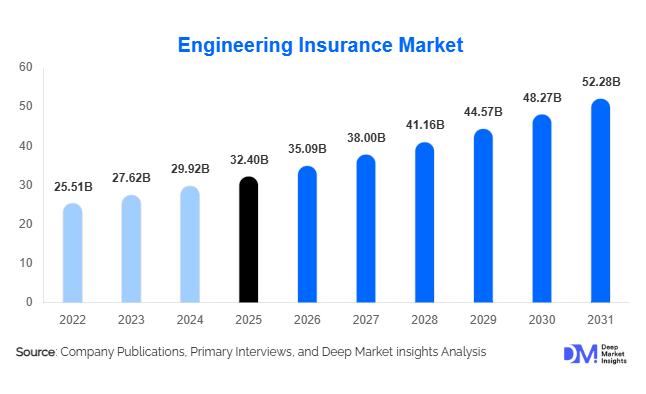

According to Deep Market Insights, the global engineering insurance market size was valued at USD 32.4 billion in 2025 and is projected to grow from USD 35.09 billion in 2026 to reach USD 52.28 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The engineering insurance market growth is primarily driven by rising investments in public infrastructure, increasing industrial automation, rapid renewable energy deployment, and growing demand for risk mitigation across large-scale construction and industrial projects.

Key Market Insights

- Contractors All Risk (CAR) insurance remains the dominant segment, supported by strong global infrastructure development and urban construction activities.

- Asia-Pacific dominates the engineering insurance market, led by China, India, Japan, and Southeast Asian economies investing heavily in transportation, industrial, and renewable energy infrastructure.

- Renewable energy engineering insurance is witnessing rapid growth, driven by increasing solar, wind, battery storage, and grid modernization projects globally.

- Digital underwriting and AI-based risk assessment technologies are reshaping the market, enabling insurers to improve claims forecasting, project monitoring, and premium pricing accuracy.

- Industrial automation and smart manufacturing expansion are accelerating demand for machinery breakdown and electronic equipment insurance products.

- Climate-related risks and catastrophic weather events are increasing the adoption of broader engineering insurance coverage and parametric risk protection solutions.

Engineering Insurance Market Latest Trends

Renewable Energy Infrastructure Insurance Expansion

The rapid global transition toward renewable energy is significantly influencing the engineering insurance market. Large-scale solar parks, offshore wind farms, battery storage facilities, hydrogen plants, and smart grid installations require highly specialized insurance solutions covering erection, commissioning, machinery breakdown, and delay-in-start-up risks. Engineering insurers are increasingly developing renewable energy-specific underwriting models to manage technical and climate-related exposures associated with these projects. Offshore wind projects, in particular, involve high-value components, marine transportation risks, and challenging installation conditions, resulting in strong demand for comprehensive engineering insurance coverage.

Governments across Europe, Asia-Pacific, and the Middle East are allocating substantial investments toward clean energy infrastructure, encouraging insurers to expand dedicated renewable energy portfolios. Engineering insurers are also integrating climate-risk modeling, predictive maintenance analytics, and satellite-based monitoring systems into renewable project underwriting. This trend is strengthening insurer capabilities while supporting long-term premium growth in sustainable infrastructure projects globally.

Digital Risk Assessment and Smart Underwriting

Engineering insurance providers are increasingly adopting advanced digital technologies to improve underwriting efficiency and project risk visibility. Artificial intelligence, IoT-enabled sensors, drones, satellite imagery, and predictive analytics are being integrated into engineering insurance workflows to monitor construction progress, detect equipment vulnerabilities, and forecast operational risks in real time.

Smart underwriting tools are helping insurers reduce claims frequency, improve loss prevention, and optimize pricing structures for complex infrastructure projects. Drone-based inspections are being widely used in transportation, mining, and renewable energy projects to assess construction quality and identify risk exposures without disrupting operations. Additionally, digital platforms are improving accessibility for mid-sized contractors and SMEs seeking faster engineering insurance policy issuance and claims management solutions.

Engineering Insurance Market Drivers

Global Infrastructure Modernization and Urban Development

Rising government investments in transportation infrastructure, smart cities, airports, railways, industrial corridors, and urban development projects are significantly driving engineering insurance demand worldwide. Large infrastructure projects inherently involve risks associated with structural damage, machinery failures, project delays, fire incidents, and third-party liabilities, increasing the need for comprehensive Contractors All Risk (CAR) and Erection All Risk (EAR) insurance coverage.

Emerging economies such as India, Indonesia, Vietnam, Saudi Arabia, and Brazil are witnessing large-scale infrastructure expansion supported by public-private partnerships and long-term national development plans. Engineering insurance has become a mandatory component in many infrastructure financing agreements, strengthening market penetration globally.

Increasing Industrial Automation and Machinery Dependency

The expansion of Industry 4.0 technologies, robotics, industrial automation systems, and connected manufacturing facilities is accelerating demand for machinery breakdown and electronic equipment insurance. Manufacturing plants, semiconductor facilities, battery gigafactories, and logistics hubs increasingly depend on high-value automated machinery where unexpected failures can lead to substantial production losses and contractual penalties.

Engineering insurers are responding by developing predictive maintenance-linked insurance models that integrate IoT monitoring and operational analytics. The increasing use of precision manufacturing technologies across automotive, aerospace, electronics, and pharmaceutical industries is further strengthening demand for advanced engineering insurance solutions.

Global Market Restraints

Complex Underwriting and Catastrophic Risk Exposure

Engineering insurance underwriting has become increasingly complex due to rising project scale, supply chain interdependencies, geopolitical instability, and climate-related uncertainties. Mega infrastructure and industrial projects often involve multi-country contractors, sophisticated equipment, and long construction timelines, increasing underwriting complexity and reinsurance dependency.

Natural catastrophes such as floods, earthquakes, storms, and wildfires are also increasing claims exposure for engineering insurers. Climate-related losses have raised reinsurance costs globally, impacting insurer profitability and contributing to stricter underwriting standards in high-risk regions.

Pricing Pressure and Competitive Market Conditions

The engineering insurance market remains highly competitive, particularly in mature economies where global insurers aggressively compete for large infrastructure accounts. Pricing pressure is reducing underwriting margins in several regions, especially for low-risk projects with strong loss histories.

Contractors and infrastructure developers often prioritize cost optimization during project bidding processes, placing downward pressure on premium pricing. Additionally, fluctuating raw material costs and inflation in construction activities can increase insured asset values and claims severity, creating profitability challenges for engineering insurance providers.

Engineering Insurance Industry Key Opportunities

Smart Infrastructure and Cyber-Physical Risk Insurance

The increasing deployment of smart infrastructure systems presents a major opportunity for engineering insurers. Connected transportation networks, automated industrial facilities, digital utilities, and smart city projects are creating new forms of cyber-physical risks that traditional engineering policies may not fully address.

Insurers are developing hybrid engineering and cyber-risk insurance products covering operational technology failures, system disruptions, cyberattacks, and connected infrastructure vulnerabilities. As governments and industrial enterprises continue digitalizing critical infrastructure, demand for integrated engineering-cyber insurance solutions is expected to rise substantially.

Expansion in Emerging Infrastructure Economies

Emerging economies across Asia-Pacific, the Middle East, and Africa are generating strong opportunities for engineering insurance providers due to accelerating infrastructure investments. Countries such as India, Saudi Arabia, Indonesia, Vietnam, and the UAE are expanding transportation systems, industrial parks, logistics hubs, renewable energy projects, and urban infrastructure at a rapid pace.

National development initiatives including “Make in India,” “Saudi Vision 2030,” and industrial modernization programs in Southeast Asia are increasing demand for engineering insurance products across public and private projects. Insurers entering these markets can benefit from rising policy penetration, long-term infrastructure pipelines, and expanding industrial investments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 32.40 Billion |

| Market Size in 2026 | USD 35.09 Billion |

| Market Size in 2031 | USD 52.28 Billion |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Insurance Type Insights

The Contractors All Risk (CAR) insurance segment continues to dominate the global engineering insurance market, accounting for nearly 31% of total revenue in 2025. The segment’s leadership is primarily driven by the rising number of large-scale infrastructure, industrial construction, transportation, and commercial development projects worldwide. CAR insurance provides comprehensive protection against accidental physical damage, project site risks, third-party liabilities, and unforeseen operational disruptions during the construction phase, making it indispensable for contractors, project developers, and engineering procurement construction (EPC) firms. Increasing investments in highways, metro rail systems, airports, ports, bridges, industrial corridors, and smart city projects are further accelerating demand for CAR coverage globally. Governments and private developers increasingly require comprehensive insurance protection as part of project financing and regulatory compliance frameworks, which continues to strengthen segment growth.Erection All Risk (EAR) insurance is emerging as one of the fastest-growing insurance categories due to expanding investments in industrial machinery installation, renewable energy projects, transmission infrastructure, power plants, and advanced manufacturing facilities. The rapid deployment of offshore wind farms, solar parks, battery storage systems, and industrial automation infrastructure is significantly increasing the need for coverage against installation failures, equipment damage, and commissioning risks. Machinery breakdown insurance is also witnessing substantial growth as industries adopt automation, robotics, predictive maintenance systems, and smart manufacturing technologies that rely heavily on uninterrupted machinery operations. Meanwhile, electronic equipment insurance is gaining traction across telecommunications, healthcare, IT infrastructure, and hyperscale data center projects where operational continuity and equipment reliability are critical. Delay in Start-Up (DSU) and Advance Loss of Profit (ALOP) insurance products are increasingly being adopted in mega engineering projects where construction delays, equipment failures, or supply chain disruptions can result in significant financial losses and contractual penalties.

Project Type Insights

Infrastructure projects remain the largest project category within the engineering insurance market due to sustained government spending on transportation modernization, urban infrastructure expansion, and public utility development. The dominance of this segment is supported by increasing investments in highways, bridges, tunnels, airports, seaports, railway corridors, metro systems, and urban mobility infrastructure across both developed and emerging economies. Governments worldwide are prioritizing infrastructure expansion to support economic growth, industrialization, urbanization, and population growth, creating long-term demand for engineering insurance solutions. Large public-private partnership (PPP) projects and international development financing programs are also driving the adoption of comprehensive risk management and insurance coverage across infrastructure developments.Energy and utilities projects are among the fastest-growing segments due to the rapid transition toward renewable energy and grid modernization initiatives globally. Investments in offshore wind farms, utility-scale solar projects, hydropower infrastructure, battery storage facilities, and electricity transmission networks are creating substantial opportunities for engineering insurers. Manufacturing and industrial projects continue to generate stable demand as companies modernize production facilities, integrate Industry 4.0 technologies, and expand advanced manufacturing operations. In addition, telecommunications infrastructure projects, particularly 5G deployment, fiber-optic expansion, and hyperscale data center construction, are emerging as high-growth areas requiring specialized engineering insurance products to protect sophisticated electronic systems and critical infrastructure assets.

Coverage Scope Insights

Material damage coverage accounts for the largest share of the engineering insurance market, representing approximately 34% of total demand in 2025. The segment’s leadership is driven by the growing need to protect construction sites, industrial equipment, and engineering assets against risks such as fire, explosions, structural collapse, floods, storms, earthquakes, vandalism, and accidental damage. Construction firms, industrial operators, infrastructure developers, and project financiers increasingly prioritize material damage protection to minimize operational disruptions and financial losses associated with complex engineering projects. Rising climate-related risks and the increasing frequency of natural disasters are also strengthening demand for comprehensive material damage policies worldwide.Third-party liability coverage continues to play a critical role in the engineering insurance industry as contractors and infrastructure developers face growing legal and regulatory responsibilities associated with workplace accidents, environmental incidents, and public safety risks. Large transportation, industrial, and urban infrastructure projects particularly require extensive liability coverage due to the high potential for property damage and injury claims. Testing and commissioning coverage is becoming increasingly important for renewable energy projects, industrial automation systems, and advanced manufacturing facilities where technical failures during startup operations can lead to major operational and financial disruptions. In addition, natural catastrophe extensions are witnessing rapid growth as insurers and project developers respond to increasing exposure to extreme weather events, flooding, seismic activity, and climate-related construction delays.

Enterprise Size Insights

Large enterprises dominate the engineering insurance market with nearly 57% share of global demand, primarily due to the scale and complexity of projects managed by multinational EPC contractors, industrial conglomerates, infrastructure developers, and energy companies. These organizations typically operate across multiple geographies and require highly customized insurance programs that include integrated risk management solutions, broad liability protection, and substantial reinsurance support. The increasing number of cross-border infrastructure and energy projects is further driving demand for large-scale engineering insurance programs tailored to multinational operational requirements.Mid-sized enterprises are increasingly adopting engineering insurance as contractual obligations, lender requirements, and project financing conditions become more stringent across construction and industrial sectors. Growing awareness regarding operational risk management and business continuity is also contributing to higher insurance penetration among mid-sized firms. Small contractors and SMEs represent a rapidly emerging growth segment, particularly in developing economies where urbanization, infrastructure expansion, and industrial construction activities are accelerating. The growing availability of digital insurance platforms, simplified underwriting models, AI-driven risk assessment tools, and online policy issuance systems is improving accessibility and affordability for smaller engineering firms globally.

Distribution Channel Insights

Insurance brokers continue to dominate engineering insurance distribution, accounting for approximately 46% of the global market share in 2025. The segment’s dominance is largely attributed to the technical complexity of engineering and infrastructure risks, which often require specialized policy structuring, customized risk assessment, reinsurance negotiations, and claims management expertise. Brokers play an essential role in large infrastructure, industrial, and energy projects by helping clients design comprehensive coverage programs that align with contractual obligations and project-specific risk profiles. Increasing project complexity and rising demand for integrated risk advisory services continue to strengthen the role of brokers within the market.Direct insurers maintain a strong presence among government-backed infrastructure projects, large industrial clients, and established corporate accounts that require long-term insurer relationships and tailored underwriting solutions. Meanwhile, digital insurance platforms are witnessing rapid growth, particularly among SMEs and mid-sized contractors seeking faster policy approvals, simplified documentation, transparent pricing, and digital claims processing capabilities. The adoption of insurtech solutions, AI-powered underwriting systems, and cloud-based insurance platforms is further transforming engineering insurance distribution globally. Bancassurance is also gradually expanding in emerging economies where banks increasingly support infrastructure financing, industrial lending, and project development activities that require integrated insurance coverage.

End-Use Industry Insights

The construction industry remains the largest end-use segment within the engineering insurance market, accounting for approximately 35% of global demand in 2025. The segment’s leadership is driven by rising investments in residential developments, commercial real estate projects, industrial construction, and public infrastructure expansion worldwide. Rapid urbanization, population growth, and government-led infrastructure modernization initiatives continue to fuel demand for Contractors All Risk (CAR) insurance, liability coverage, and project risk management solutions across the construction sector. Increasing adoption of green building standards and smart infrastructure technologies is also creating additional opportunities for engineering insurers.The energy and power sector is among the fastest-growing end-use industries due to the global transition toward renewable energy generation and modernization of electricity infrastructure. Investments in solar energy, offshore wind, hydrogen projects, battery storage systems, and smart grids are significantly increasing demand for specialized engineering insurance products. Manufacturing industries are also expanding adoption of machinery breakdown insurance and electronic equipment coverage as automation, robotics, and smart factory technologies become increasingly integrated into industrial operations. In addition, telecommunications infrastructure, including 5G networks, fiber-optic systems, and hyperscale data centers, is emerging as a high-growth application area due to rising dependence on uninterrupted digital connectivity and advanced electronic infrastructure.

Explore more data points, trends and opportunities Download Free Sample Report

Engineering Insurance Market Segmentations

By Insurance Type

- Contractors All Risk (CAR) Insurance

- Erection All Risk (EAR) Insurance

- Machinery Breakdown Insurance

- Electronic Equipment Insurance

- Boiler and Pressure Plant Insurance

- Contractor’s Plant and Machinery (CPM) Insurance

- Delay in Start-Up (DSU) / Advance Loss of Profit Insurance

- Comprehensive Engineering Insurance Solutions

By Project Type

- Infrastructure Projects

- Building & Construction Projects

- Energy & Utilities Projects

- Oil & Gas Projects

- Manufacturing & Industrial Projects

- Telecommunications Infrastructure Projects

- Mining & Metals Projects

- Water & Wastewater Projects

- Smart City & Urban Infrastructure Projects

By Coverage Scope

- Material Damage Coverage

- Third-Party Liability Coverage

- Testing & Commissioning Coverage

- Transit & Storage Coverage

- Natural Catastrophe Coverage

- Equipment Failure Coverage

- Delay in Completion Coverage

- Cyber-Physical Risk Extensions

By Distribution Channel

- Insurance Brokers

- Direct Insurers

- Bancassurance

- Digital Insurance Platforms

- Reinsurance Arrangements

By End-Use Industry

- Construction

- Energy & Power

- Manufacturing

- Oil & Gas

- Mining

- Transportation & Logistics

- Telecommunications

- Healthcare Infrastructure

- Government & Public Infrastructure

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global engineering insurance market with nearly 38% market share in 2025, supported by rapid infrastructure development, industrialization, urban expansion, and renewable energy investments across major economies including China, India, Japan, South Korea, and Southeast Asia. The region’s dominance is primarily driven by large-scale government infrastructure programs, rising foreign direct investments, expanding manufacturing activities, and increasing public-private partnership projects. China remains the largest engineering insurance market globally due to extensive spending on transportation infrastructure, industrial modernization, renewable energy deployment, smart city initiatives, and high-speed railway expansion. The country’s continued investments in megaprojects and industrial automation are generating substantial demand for CAR, EAR, machinery breakdown, and liability insurance products.India is among the fastest-growing engineering insurance markets owing to rapid metro rail expansion, industrial corridor development, renewable energy investments, airport modernization, highway construction, and public infrastructure initiatives under programs such as “Make in India,” Bharatmala, and Smart Cities Mission. Increasing infrastructure financing activities and rising awareness regarding project risk management are further supporting market growth. Southeast Asian economies including Indonesia, Vietnam, Thailand, and the Philippines are also witnessing strong demand growth driven by urbanization, manufacturing relocation trends, logistics infrastructure expansion, and rising investments in industrial parks and energy infrastructure. Additionally, increasing climate-related risks across the region are encouraging broader adoption of comprehensive engineering insurance coverage.

North America

North America accounted for nearly 24% of the global engineering insurance market share in 2025, driven by infrastructure modernization initiatives, renewable energy investments, industrial automation, and advanced manufacturing expansion. The United States remains the leading regional market due to increasing federal infrastructure spending, modernization of transportation networks, expansion of logistics and warehousing infrastructure, and rising investments in energy transition projects. The implementation of smart infrastructure technologies, data centers, semiconductor manufacturing facilities, and industrial digitization initiatives is significantly increasing demand for engineering insurance products across the country.Canada is witnessing stable growth supported by mining projects, renewable energy developments, transportation infrastructure investments, and industrial modernization programs. The region is also experiencing rising adoption of cyber-integrated engineering insurance products as industrial facilities become increasingly connected through IoT, AI-driven automation, and digital monitoring systems. Furthermore, stricter regulatory standards related to workplace safety, environmental risk management, and infrastructure resilience are encouraging businesses to adopt broader and more sophisticated engineering insurance coverage solutions across North America.

Europe

Europe remains a technologically advanced engineering insurance market supported by strong industrial manufacturing capabilities, transportation infrastructure modernization, renewable energy deployment, and stringent regulatory standards. Germany leads the regional market due to its highly developed industrial base, advanced engineering sector, and significant demand for machinery breakdown and industrial risk insurance products. The country’s emphasis on Industry 4.0 adoption, factory automation, and precision manufacturing continues to support sustained market growth.The United Kingdom, France, Italy, and the Nordic countries also contribute significantly to regional demand due to ongoing investments in rail infrastructure, smart city development, renewable energy projects, and industrial modernization. Offshore wind energy expansion in Northern Europe is creating substantial opportunities for EAR, DSU, and marine-related engineering insurance products. Additionally, ESG compliance requirements, sustainability initiatives, and climate-risk management practices are becoming increasingly integrated into engineering underwriting across Europe. Rising investments in hydrogen infrastructure, electric vehicle manufacturing facilities, and green energy projects are further driving regional market expansion.

Latin America

Latin America represents an emerging engineering insurance market supported by infrastructure modernization, industrial development, mining activities, and renewable energy investments. Brazil accounts for the largest regional share due to extensive transportation projects, industrial expansion, energy infrastructure development, and large-scale construction activities. Increasing government initiatives focused on logistics modernization, urban transportation systems, and energy diversification are strengthening engineering insurance demand across the country.Mexico is witnessing rising market growth driven by manufacturing investments, automotive production expansion, logistics infrastructure development, and nearshoring trends that are encouraging multinational companies to establish industrial operations closer to North American supply chains. Mining investments across Chile and Peru, combined with renewable energy developments throughout the region, are also contributing to higher demand for engineering insurance solutions. Furthermore, increasing participation of international insurers and reinsurers is improving market penetration and expanding product availability across Latin America.

Middle East & Africa

The Middle East & Africa region is witnessing strong engineering insurance growth supported by mega infrastructure developments, industrial diversification strategies, tourism infrastructure projects, and large-scale energy investments. Saudi Arabia and the United Arab Emirates lead regional demand due to extensive smart city developments, transportation infrastructure expansion, airport projects, industrial zones, renewable energy investments, and giga-projects linked to Vision 2030 economic diversification programs. Large-scale construction activities associated with tourism, entertainment, logistics, and urban development are significantly increasing demand for CAR, EAR, liability, and project delay insurance products across the Gulf region.South Africa remains a key African market supported by mining operations, transportation infrastructure investments, industrial projects, and energy sector modernization. Other African economies are gradually increasing engineering insurance adoption as governments focus on improving roads, ports, power generation capacity, and urban infrastructure. Infrastructure financing initiatives, sovereign development programs, and growing public-private partnerships are further supporting market penetration across the region. Additionally, rising awareness regarding climate risks, project delays, and operational disruptions is encouraging broader adoption of engineering insurance coverage among contractors and infrastructure developers throughout the Middle East & Africa.

Key Players in the Engineering Insurance Market

- Allianz SE

- Zurich Insurance Group

- AXA SA

- Chubb Limited

- Munich Re

- Swiss Re

- Tokio Marine Holdings

- AIG (American International Group)

- HDI Global SE

- Generali Group

- Sompo Holdings

- Liberty Mutual Insurance

- MAPFRE

- QBE Insurance Group

- CNA Financial Corporation