Cyber Security Market Size

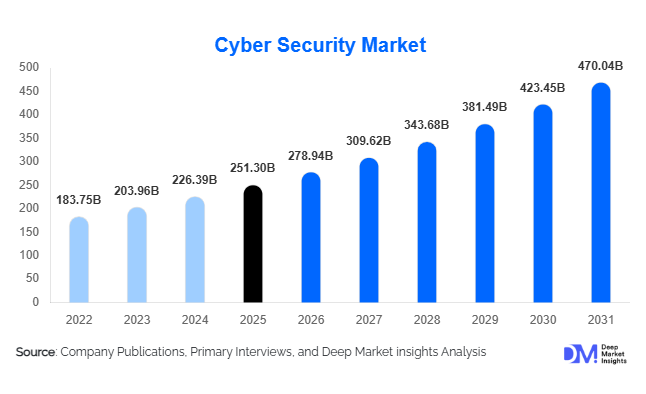

According to Deep Market Insights, the global cyber security market size was valued at USD 251.30 billion in 2025 and is projected to grow from USD 278.94 billion in 2026 to reach USD 470.04 billion by 2031, expanding at a CAGR of 11.0% during the forecast period (2026–2031). The cyber security market growth is primarily driven by the rapid rise in ransomware attacks, increasing cloud migration across enterprises, growing digital transformation initiatives, and stricter global data protection regulations. Organizations worldwide are significantly increasing investments in identity management, endpoint protection, cloud workload security, and AI-powered threat intelligence platforms to strengthen digital resilience.

The expansion of hybrid work environments, industrial IoT deployment, and 5G-enabled infrastructure has widened the cyber threat landscape globally, accelerating demand for integrated security architectures. Enterprises are increasingly transitioning from traditional perimeter-based defense models toward zero-trust frameworks and cloud-native security ecosystems. Industries such as BFSI, healthcare, manufacturing, telecom, government, and energy remain major adopters due to high exposure to data breaches and operational disruptions.

Managed security services are gaining strong momentum as organizations struggle with shortages of skilled cyber security professionals. Small and medium enterprises are also accelerating adoption of subscription-based security solutions due to rising phishing and malware attacks. Additionally, governments across North America, Europe, Asia-Pacific, and the Middle East are increasing national cyber defense investments to secure critical infrastructure, public digital services, and strategic defense systems. The integration of artificial intelligence, behavioral analytics, automation, and extended detection and response (XDR) technologies is expected to reshape the competitive landscape over the forecast period.

Key Market Insights

- Cloud security and identity-centric protection frameworks are rapidly becoming core enterprise priorities, driven by hybrid work adoption and expanding multi-cloud infrastructure.

- AI-driven threat intelligence and automated incident response platforms are transforming cyber defense operations, reducing breach response times and improving real-time threat detection capabilities.

- North America dominates the global cyber security market, supported by extensive enterprise digitization, strong regulatory frameworks, and high cyber defense spending.

- Asia-Pacific is the fastest-growing regional market, fueled by rapid digital transformation, expansion of fintech ecosystems, and increasing ransomware incidents.

- Managed security services are witnessing strong demand among SMEs, as organizations increasingly outsource security operations due to skill shortages and cost optimization requirements.

- Zero-trust architecture and XDR platforms are emerging as major technology trends, replacing fragmented legacy security systems with unified security ecosystems.

Cyber Security Market Latest Trends

Rapid Adoption of Zero-Trust Security Architecture

Organizations worldwide are increasingly adopting zero-trust security frameworks to strengthen digital resilience against evolving cyber threats. Traditional perimeter-based models are becoming ineffective due to widespread cloud adoption, hybrid work environments, and increasing device connectivity. Zero-trust models enforce continuous authentication, strict identity verification, and least-privilege access policies across enterprise networks. Governments, financial institutions, healthcare providers, and large enterprises are prioritizing zero-trust deployment to secure distributed digital infrastructure and prevent lateral movement during cyberattacks. Vendors are integrating zero-trust capabilities with identity governance, endpoint protection, and cloud security platforms to deliver comprehensive enterprise-grade security ecosystems.

AI-Driven Threat Detection and Security Automation

Artificial intelligence and machine learning technologies are increasingly reshaping cyber security operations globally. Enterprises are deploying AI-powered analytics to identify anomalous user behavior, predict emerging attack patterns, and automate incident response workflows. Security Operations Centers are leveraging AI-enabled SIEM and XDR platforms to reduce false positives and accelerate breach remediation timelines. Automated orchestration tools are helping organizations manage large-scale threat environments with reduced dependence on manual intervention. Generative AI is also being adopted to enhance phishing detection, malware analysis, and vulnerability management. As cyberattacks become more sophisticated, AI-assisted security frameworks are expected to become a fundamental component of enterprise cyber defense strategies.

Cyber Security Market Drivers

Growing Frequency of Ransomware and Advanced Cyberattacks

The increasing frequency and sophistication of ransomware attacks, phishing campaigns, and advanced persistent threats are major drivers accelerating cyber security spending globally. Enterprises across BFSI, healthcare, manufacturing, telecom, and government sectors are experiencing rising financial losses associated with operational downtime, reputational damage, and regulatory penalties following data breaches. Nation-state cyber warfare activities and supply chain attacks are further intensifying enterprise investment in threat intelligence, endpoint security, and real-time monitoring systems. Organizations are prioritizing proactive security frameworks capable of detecting and mitigating attacks before operational disruption occurs.

Expansion of Cloud Computing and Hybrid Work Environments

Rapid migration toward public, hybrid, and multi-cloud environments is significantly increasing demand for cloud-native security solutions. Enterprises are deploying cloud workload protection, identity management, secure access systems, and API security platforms to secure distributed digital assets. The widespread adoption of hybrid work environments has expanded organizational attack surfaces, creating strong demand for secure remote access solutions and identity-centric protection frameworks. Increasing SaaS adoption and interconnected enterprise ecosystems are also contributing to long-term cyber security market expansion globally.

Global Market Restraints

Shortage of Skilled Cyber Security Professionals

The global shortage of qualified cyber security professionals remains one of the most significant restraints affecting market expansion. Organizations are struggling to recruit skilled security analysts, incident response specialists, ethical hackers, and cloud security architects capable of managing complex digital threat environments. This talent gap increases operational costs, slows incident response efficiency, and limits the ability of enterprises to fully utilize advanced cyber security platforms. Small and medium enterprises are particularly vulnerable due to limited access to specialized expertise and budgetary constraints.

High Deployment and Integration Costs

Advanced cyber security infrastructure often involves substantial implementation, maintenance, and integration expenses. Large-scale deployment of SIEM, XDR, cloud security, and identity governance platforms requires continuous software updates, infrastructure upgrades, and specialized workforce training. Legacy IT environments further complicate integration processes, especially in developing economies where digital modernization remains uneven. High operational costs continue to challenge adoption among small enterprises and organizations with limited technology budgets.

Cyber Security Industry Key Opportunities

Critical Infrastructure and National Cyber Defense Investments

Governments worldwide are increasing investments in cyber defense modernization to protect critical infrastructure, digital public services, telecommunications networks, and military systems. National cyber resilience initiatives across the United States, Europe, India, China, Japan, and Gulf countries are creating significant growth opportunities for industrial cyber security providers. Smart city infrastructure, connected transportation systems, energy grids, and industrial automation environments require advanced OT and SCADA protection frameworks. Vendors specializing in sovereign cloud security, industrial cyber defense, and AI-driven monitoring systems are expected to benefit substantially from long-term government infrastructure spending.

Managed Security Services Expansion Among SMEs

Small and medium enterprises are increasingly adopting managed security services due to growing cyber risks and lack of internal security expertise. Subscription-based managed detection and response (MDR), cloud security monitoring, and endpoint protection services are gaining rapid adoption due to scalability and cost efficiency. Emerging economies such as India, Brazil, Indonesia, and Vietnam are witnessing strong demand for outsourced cyber security services as digitalization accelerates among SMEs. Vendors capable of delivering integrated security solutions with simplified deployment and recurring subscription models are expected to gain strong competitive advantages over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 251.30 Billion |

| Market Size in 2026 | USD 278.94 Billion |

| Market Size in 2031 | USD 470.04 Billion |

| CAGR | 11% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Security Type Insights

Cloud security represents the leading segment within the cyber security market, accounting for nearly 21% of the global market in 2025. The growing shift toward hybrid cloud infrastructure, SaaS adoption, and distributed workforce models is significantly increasing enterprise demand for cloud-native security platforms. Identity and access management solutions are also witnessing strong growth due to rising zero-trust adoption and stricter regulatory compliance requirements. Endpoint detection and response solutions continue gaining traction as organizations strengthen defenses against ransomware attacks targeting employee devices and connected enterprise endpoints. Operational technology and industrial cyber security are emerging as high-growth segments due to increasing deployment of Industry 4.0 systems, smart manufacturing infrastructure, and connected industrial control environments.

Deployment Mode Insights

Cloud-based deployment dominates the global cyber security market, accounting for approximately 58% of the total market share in 2025. Organizations increasingly prefer cloud-delivered security solutions due to scalability, remote accessibility, reduced infrastructure requirements, and faster deployment capabilities. Hybrid deployment models are also gaining popularity among enterprises operating across legacy infrastructure and modern cloud environments, enabling flexible integration while maintaining compliance and operational control. On-premise deployment remains relevant in highly regulated industries such as defense, government, and critical infrastructure where strict data sovereignty requirements necessitate localized security environments.

Enterprise Size Insights

Large enterprises account for nearly 63% of the global cyber security market due to their extensive digital infrastructure, high-value data assets, and elevated exposure to sophisticated cyber threats. These organizations continue investing heavily in AI-powered analytics, zero-trust architecture, and integrated security ecosystems to secure global operations. Medium-sized enterprises are rapidly increasing cyber security investments as cloud adoption and remote workforce models expand. Small enterprises are emerging as an important growth segment due to increasing cyberattack frequency and rising availability of affordable subscription-based security services tailored for SME environments.

Industry Vertical Insights

BFSI remains the leading industry vertical, accounting for approximately 19% of the global cyber security market in 2025. Financial institutions face persistent threats targeting digital payment systems, customer databases, and online banking platforms, driving strong investments in fraud detection, identity management, and encryption technologies. Healthcare is among the fastest-growing verticals due to rapid digitization of patient records and connected medical devices. Manufacturing companies are increasingly investing in industrial cyber security to protect smart factories and operational technology systems from ransomware and supply chain attacks. Government and defense sectors also remain major adopters due to rising geopolitical cyber warfare risks and national infrastructure protection requirements.

End-Use Insights

Commercial enterprises remain the largest end-use segment for cyber security solutions globally, driven by rapid digital transformation and increasing cloud adoption across industries. Enterprises are prioritizing investments in endpoint security, identity governance, and cloud workload protection to strengthen operational resilience. Government organizations and defense institutions represent one of the fastest-growing end-use segments due to rising cyber warfare threats and increasing public infrastructure digitization. Healthcare providers, telecom operators, and critical infrastructure organizations are also accelerating cyber security spending as connected systems and IoT-enabled environments expand globally.

Explore more data points, trends and opportunities Download Free Sample Report

Cyber Security Market Segmentations

By Security Type

- Network Security

- Endpoint & Device Security

- Cloud Security

- Identity & Access Management

- Application Security

- Data Security

- Security Analytics & Intelligence

- Operational Technology (OT) & Industrial Cybersecurity

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid Deployment

By Enterprise Size

- Large Enterprises

- Medium Enterprises

- Small Enterprises

By Solution Component

- Solutions

- Managed Security Services

- Professional Services

- Incident Response Services

By Threat Type

- Malware & Ransomware

- Phishing & Social Engineering

- Advanced Persistent Threats (APT)

- Insider Threats

- Zero-Day Exploits

- Supply Chain Attacks

- Cryptojacking

- Nation-State Cyberattacks

By Industry Vertical

- BFSI

- Healthcare & Life Sciences

- Government & Defense

- IT & Telecom

- Retail & E-Commerce

- Manufacturing

- Energy & Utilities

- Transportation & Logistics

- Education

Regional Insights

North America

North America accounted for approximately 38% of the global cyber security market share in 2025, led primarily by the United States. High enterprise digitalization, strong cloud adoption, extensive federal cyber defense spending, and frequent large-scale cyberattacks continue driving regional demand. The United States remains the largest national market globally due to strong investments across BFSI, healthcare, telecom, and defense sectors. Canada is also witnessing robust growth supported by increasing investments in banking cyber resilience and critical infrastructure modernization initiatives.

Europe

Europe represents nearly 24% of the global cyber security market, supported by stringent data protection regulations and expanding digital sovereignty initiatives. Germany dominates regional demand due to extensive industrial automation and manufacturing digitalization. The United Kingdom continues to witness strong cyber security spending across financial services and cloud infrastructure. France, the Netherlands, and Nordic countries are increasingly investing in public-sector cyber resilience and telecom infrastructure security. GDPR compliance requirements continue to significantly influence enterprise cyber security procurement decisions across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and accounted for approximately 27% of global revenue in 2025. China remains a major contributor due to extensive smart manufacturing deployment and state-backed cyber defense programs. India is emerging as one of the fastest-growing cyber security markets globally, driven by fintech expansion, digital payments growth, and increasing enterprise cloud adoption. Japan and South Korea continue investing heavily in industrial IoT security, automotive cyber protection, and smart factory security frameworks. Southeast Asian economies are also witnessing strong cyber security adoption as e-commerce and digital banking penetration accelerate.

Latin America

Latin America is gradually strengthening its cyber security ecosystem, led by Brazil and Mexico. Increasing e-commerce penetration, rising digital banking adoption, and growing cyber fraud incidents are encouraging enterprises to enhance security infrastructure investments. Governments across the region are also introducing stronger data protection regulations to improve national cyber resilience and strengthen digital trust among businesses and consumers.

Middle East & Africa

The Middle East & Africa region is witnessing growing cyber security investments driven by smart city initiatives, energy infrastructure modernization, and digital transformation strategies. Saudi Arabia and the UAE are investing heavily in cloud security, national cyber resilience, and public-sector digital infrastructure. Israel remains a global innovation hub for advanced cyber security technologies and start-up ecosystems. African economies are gradually increasing investments in telecom security, fintech protection, and digital public infrastructure as internet penetration and mobile financial services expand across the region.

Key Players in the Cyber Security Market

- Palo Alto Networks

- Cisco Systems

- Fortinet

- CrowdStrike

- Microsoft

- Check Point Software Technologies

- Trend Micro

- Broadcom

- IBM

- Zscaler

- Okta

- SentinelOne

- Sophos

- Rapid7

- CyberArk