Food Security Technology Market Size

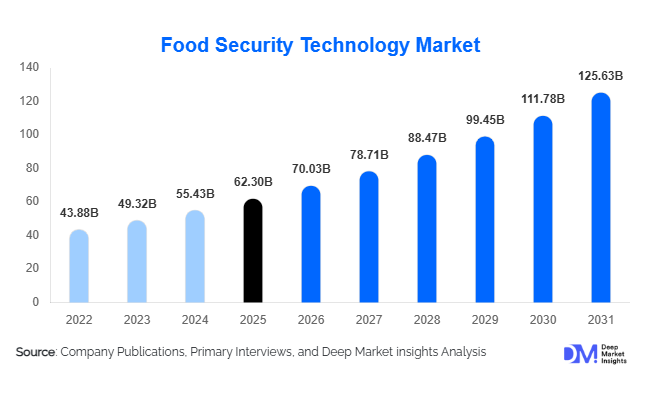

According to Deep Market Insights, the global food security technology market size was valued at USD 62.3 billion in 2025 and is projected to grow from USD 70.03 billion in 2026 to reach USD 125.63 billion by 2031, expanding at a CAGR of 12.4% during the forecast period (2026–2031). The food security technology market growth is primarily driven by increasing concerns surrounding global food shortages, climate variability, water scarcity, rising agricultural input costs, and the growing need for sustainable food production systems. Governments, agribusinesses, and food supply chain participants are increasingly investing in precision agriculture, smart irrigation systems, AI-powered farm analytics, controlled environment agriculture, and food traceability technologies to strengthen long-term food resilience.

Key Market Insights

- Precision agriculture technologies dominate the market, supported by rising adoption of IoT-enabled monitoring systems, smart irrigation, and automated crop management platforms.

- AI-powered predictive farming and analytics solutions are witnessing rapid adoption, helping farmers improve yield forecasting, pest detection, and resource optimization.

- North America remains the leading regional market, driven by advanced agricultural infrastructure, high mechanization rates, and strong agri-tech investments.

- Asia-Pacific is emerging as the fastest-growing region, fueled by food self-sufficiency initiatives, rising population pressure, and increasing digital agriculture investments in China and India.

- Controlled environment agriculture is gaining momentum globally, particularly vertical farming and hydroponics systems in urban and water-scarce regions.

- Food traceability and blockchain-enabled supply chain transparency technologies are expanding rapidly, driven by regulatory pressure and growing consumer demand for safe and sustainable food systems.

food security technology market latest trends

AI-Driven Precision Farming Expanding Rapidly

Artificial intelligence and advanced analytics are transforming agricultural decision-making across the food security technology market. AI-powered crop monitoring systems are enabling farmers to optimize planting schedules, identify nutrient deficiencies, detect pest infestations early, and improve overall productivity. Predictive analytics platforms integrated with weather intelligence systems are helping commercial farms reduce operational risks associated with climate volatility. Autonomous agricultural machinery, smart drones, and machine-learning-enabled irrigation management systems are also becoming increasingly mainstream. Large agribusinesses are deploying connected farming ecosystems that combine satellite imaging, sensor networks, and cloud-based analytics to maximize yield while minimizing water, fertilizer, and pesticide usage. The declining cost of IoT devices and cloud computing infrastructure is further accelerating technology adoption among medium-sized farms globally.

Controlled Environment Agriculture Gaining Strong Investment Momentum

Controlled environment agriculture (CEA), including vertical farming, hydroponics, aeroponics, and indoor cultivation systems, is becoming one of the fastest-growing trends within the food security technology market. Governments and private investors are increasingly funding indoor agriculture projects to reduce dependence on imported food and improve domestic food resilience. Countries with limited arable land and harsh climatic conditions, particularly Singapore, the UAE, Saudi Arabia, and Japan, are aggressively scaling urban farming infrastructure. Indoor farming operators are integrating LED grow lighting, climate control automation, and AI-driven nutrient optimization systems to improve year-round crop production efficiency. Retail chains and foodservice companies are also partnering with vertical farming operators to secure local fresh produce supply while reducing transportation-related food losses and carbon emissions.

food security technology market drivers

Rising Global Food Demand and Climate Challenges

Rapid population growth and increasing pressure on global food systems are significantly driving demand for advanced food security technologies. Rising urbanization and shrinking arable land availability are forcing governments and agricultural enterprises to improve productivity through precision farming and sustainable agricultural practices. Climate change has intensified concerns surrounding droughts, floods, unpredictable rainfall patterns, and soil degradation, creating urgent demand for climate-resilient farming technologies. Precision irrigation systems, AI-based crop monitoring, drought-resistant seed technologies, and soil analytics platforms are increasingly viewed as essential tools for maintaining food supply stability. Agricultural producers are prioritizing technology-driven efficiency improvements to maximize crop yields while reducing environmental impact.

Government Investments in Agricultural Modernization

Governments globally are increasing investments in agricultural modernization programs to strengthen national food resilience and reduce import dependency. Major economies such as China, India, the United States, and Saudi Arabia are deploying substantial funding toward smart irrigation systems, digital agriculture infrastructure, and sustainable farming initiatives. Government-backed subsidies for water-efficient irrigation, climate-smart agriculture, and rural digitization are accelerating market growth. National food security strategies introduced following global supply chain disruptions have also increased focus on domestic food production capabilities. Public-private partnerships aimed at improving rural connectivity and digital farming adoption are further supporting technology deployment across emerging agricultural economies.

global market restraints

High Initial Capital Investment Requirements

The implementation of advanced food security technologies often requires substantial upfront investment, creating barriers for smallholder farmers and agricultural cooperatives. Technologies such as autonomous machinery, vertical farming systems, robotics, and AI-powered farm analytics platforms involve significant equipment, infrastructure, and software costs. Financing limitations in developing economies continue to restrict adoption among resource-constrained farming communities. In many regions, insufficient access to agricultural credit and leasing mechanisms further slows technology penetration. Smaller farms often struggle to justify return on investment due to uncertain crop prices and fluctuating agricultural margins.

Limited Technical Expertise and Rural Infrastructure

Many agricultural regions continue to face shortages of skilled professionals capable of operating advanced digital farming systems and interpreting complex agricultural analytics. Limited digital literacy among farmers remains a major challenge, particularly across developing economies. Rural areas in emerging markets frequently suffer from poor internet connectivity, inconsistent electricity supply, and inadequate digital infrastructure, restricting deployment of IoT-enabled agricultural systems. Data interoperability issues between different technology providers and concerns surrounding agricultural data privacy also create operational complexities that can delay broader market adoption.

food security technology industry key opportunities

Expansion of Smart Irrigation and Water Management Solutions

Increasing global water scarcity is creating significant opportunities for smart irrigation and precision water management technologies. Governments and agricultural enterprises are prioritizing investments in drip irrigation systems, sensor-enabled irrigation controllers, water recycling technologies, and AI-based water optimization platforms. Water-stressed regions across the Middle East, Africa, Australia, and India are expected to become major growth centers for smart irrigation technologies over the coming years. Companies offering integrated water efficiency solutions that combine analytics, automation, and predictive irrigation scheduling are likely to gain substantial market traction as sustainable water management becomes critical for long-term agricultural productivity.

Digital Food Traceability and Supply Chain Transparency

Growing concerns surrounding food safety, contamination risks, and supply chain disruptions are accelerating demand for digital food traceability technologies. Blockchain-enabled food tracking systems, IoT-based cold chain monitoring platforms, and RFID-enabled logistics solutions are helping food manufacturers and retailers improve transparency across the food value chain. Regulatory pressure regarding food safety compliance in Europe and North America is encouraging broader adoption of traceability infrastructure. Export-oriented agricultural economies are also investing heavily in food traceability technologies to meet international standards and improve access to premium export markets. The growing importance of ESG reporting and sustainability compliance is expected to create long-term opportunities for food security technology providers focused on supply chain visibility.

Technology Type Insights

Precision agriculture technologies account for the largest share of the food security technology market, representing nearly 28% of total market revenue in 2025. Adoption is strongest among large commercial farms seeking to optimize yield efficiency and reduce input costs through smart irrigation, variable rate technology, and satellite-based crop monitoring systems. IoT-enabled field sensors and drone-based analytics platforms are becoming increasingly common across North America and Europe. Controlled environment agriculture is emerging as one of the fastest-growing technology categories due to rising investments in vertical farming and hydroponics systems. Biotechnology and climate-resilient seed technologies are also gaining traction as agricultural producers seek solutions capable of improving productivity under increasingly volatile climate conditions.

Application Insights

Crop production remains the leading application segment within the food security technology market, accounting for approximately 39% of total market share in 2025. Rising global demand for grains, fruits, vegetables, and oilseeds is driving adoption of precision farming systems, automated irrigation platforms, and predictive crop analytics tools. Livestock management technologies are witnessing strong growth due to increasing deployment of smart feeding systems, livestock monitoring wearables, and AI-based disease detection platforms. Food storage and cold chain monitoring applications are also expanding rapidly as food manufacturers and retailers seek to reduce post-harvest losses and improve supply chain efficiency. Fisheries and aquaculture technologies are emerging as an additional growth area supported by increasing global protein demand and sustainable seafood production initiatives.

Component Insights

Hardware components currently dominate the food security technology market, accounting for nearly 48% of total market revenue in 2025. Strong demand for sensors, drones, smart irrigation systems, monitoring devices, and agricultural robotics continues to support hardware segment growth. Precision irrigation infrastructure and autonomous farming equipment remain major investment categories among commercial agricultural enterprises. Software platforms, however, are expected to witness the fastest growth over the forecast period as cloud-based farm management systems and AI-driven analytics solutions become central to agricultural operations. Services such as system integration, consulting, predictive maintenance, and managed analytics are also gaining importance as farms increasingly adopt connected agricultural ecosystems requiring long-term technical support.

Farm Size Insights

Large commercial farms represent the dominant farm size segment within the food security technology market, accounting for approximately 46% of market share in 2025. These operators possess greater financial resources to invest in precision agriculture systems, autonomous machinery, and advanced analytics infrastructure. Large-scale farming enterprises are prioritizing digital transformation to improve operational efficiency, sustainability compliance, and profitability amid rising labor and input costs. Medium-sized farms are increasingly adopting cloud-based farm management platforms and smart irrigation systems as technology costs decline. Smallholder farms remain an important long-term growth opportunity, particularly in Asia-Pacific and Africa, where governments and NGOs are promoting affordable digital agriculture solutions and financing programs to improve food productivity and rural incomes.

End-Use Insights

Commercial agriculture enterprises account for the largest end-use share of the food security technology market, contributing approximately 41% of total revenue in 2025. Large agribusinesses are aggressively investing in smart farming systems, supply chain visibility platforms, and AI-driven agricultural analytics to improve productivity and sustainability performance. Government agencies and public-sector institutions are among the fastest-growing end-use segments due to increasing investments in national food resilience programs, climate-smart agriculture infrastructure, and rural digitization initiatives. Food processing companies are also expanding adoption of blockchain traceability systems, cold chain monitoring solutions, and automated food safety infrastructure to comply with increasingly stringent regulatory standards. Agricultural cooperatives and research institutions continue to play a key role in technology adoption, particularly within emerging markets.

| By Technology Type | By Application | By Component | By Farm Size | By Deployment Model |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 32% of the global food security technology market in 2025, making it the largest regional market. The United States dominates regional demand due to advanced agricultural infrastructure, high adoption of precision farming systems, and strong investment activity in agri-tech innovation. Commercial farms across the U.S. are increasingly deploying AI-powered analytics, autonomous tractors, and IoT-enabled irrigation systems to improve operational efficiency and sustainability. Canada is also witnessing rising adoption of smart agriculture technologies, particularly within grain production and greenhouse farming sectors. Government support for climate-smart agriculture and sustainable water management is further accelerating market growth across the region.

Europe

Europe represents approximately 24% of the global market and remains a major hub for sustainable agriculture technologies and food traceability systems. Germany, France, the Netherlands, and the United Kingdom are leading adopters of AI-based farm analytics, precision irrigation systems, and low-carbon agricultural technologies. Strict environmental regulations and sustainability mandates are encouraging widespread deployment of resource-efficient farming systems across Europe. The Netherlands continues to lead globally in greenhouse farming innovation and controlled environment agriculture infrastructure. Increasing focus on reducing agricultural emissions and improving food traceability is expected to sustain long-term regional market growth.

Asia-Pacific

Asia-Pacific accounted for approximately 29% of global market share in 2025 and is projected to be the fastest-growing regional market through 2031, supported by a CAGR exceeding 14%. China remains one of the largest growth contributors due to large-scale investments in smart farming, agricultural drones, and domestic food production modernization. India is witnessing rapid expansion in precision irrigation, digital agriculture platforms, and agri-fintech ecosystems supported by government-led agricultural digitization programs. Japan and Singapore are heavily investing in vertical farming and indoor agriculture technologies to improve domestic food resilience amid limited land availability. Rising population pressure and food demand continue to support long-term market expansion across the region.

Latin America

Latin America is emerging as a promising market for food security technologies led by Brazil, Argentina, and Mexico. Brazil is among the world’s largest adopters of precision agriculture systems due to its large-scale soybean, sugarcane, and grain production industries. Agricultural exporters across the region are increasingly investing in smart irrigation, yield monitoring systems, and supply chain traceability technologies to improve productivity and maintain export competitiveness. Growing mechanization and rising investment in agricultural infrastructure are expected to accelerate technology adoption throughout Latin America over the forecast period.

Middle East & Africa

The Middle East & Africa region is witnessing increasing investments in controlled environment agriculture, water-efficient irrigation systems, and desalination-supported farming technologies. Saudi Arabia and the UAE are aggressively scaling vertical farming infrastructure to reduce food import dependence and strengthen domestic food production capabilities. African countries including Kenya, Nigeria, and South Africa are gradually adopting digital farming systems, climate-smart agriculture technologies, and mobile-based farm advisory platforms to improve agricultural productivity and food accessibility. Water scarcity concerns and food import vulnerability remain major drivers of regional market demand.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Food Security Technology Market

- John Deere

- Trimble Inc.

- Bayer AG

- Corteva Agriscience

- Syngenta Group

- AGCO Corporation

- CNH Industrial

- Kubota Corporation

- Topcon Positioning Systems

- Yara International

- Nutrien Ltd.

- Netafim

- Valmont Industries

- AeroFarms

- Plenty Unlimited