Agriculture Technology Market Size

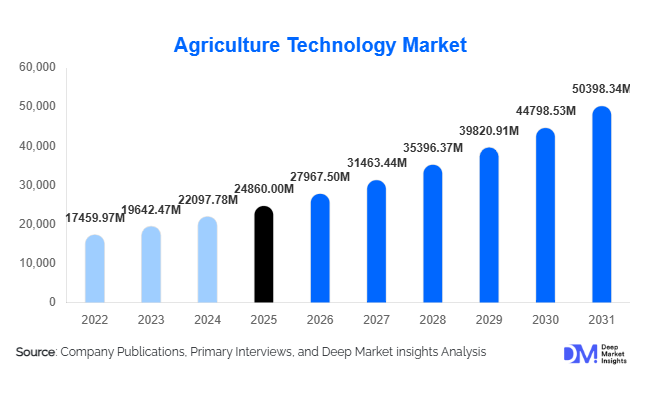

According to Deep Market Insights, the global agriculture technology market size was valued at USD 24,860 million in 2025 and is projected to grow from USD 27,967.50 million in 2026 to reach USD 50,398.34 million by 2031, expanding at a CAGR of 12.5% during the forecast period (2026–2031). Market growth is being driven by increasing global food demand, labor shortages in farming, climate variability, and the rapid digitalization of agricultural operations. Agriculture technology solutions—including precision farming tools, smart irrigation systems, robotics, AI-enabled analytics, and farm management platforms—are enabling farmers to improve productivity while optimizing resource utilization.

Governments and agribusinesses worldwide are accelerating investments in smart farming infrastructure to enhance yield efficiency and sustainability outcomes. Rising adoption of IoT-enabled sensors, satellite monitoring, and autonomous machinery is transforming traditional agriculture into data-driven operations. Emerging economies are witnessing strong adoption supported by subsidy programs and digital agriculture missions, while developed regions are advancing toward automation-led farming ecosystems. The agriculture technology market is increasingly transitioning from hardware-centric offerings toward integrated software ecosystems and analytics-driven decision-making platforms, reshaping value creation across the global agri-value chain.

Key Market Insights

- Precision agriculture technologies account for the largest revenue share, driven by demand for yield optimization and input cost reduction.

- Farm automation adoption is accelerating globally due to rising agricultural labor shortages and increasing wage pressures.

- North America leads global adoption supported by advanced mechanization and strong agri-tech investments.

- Asia-Pacific represents the fastest-growing region, fueled by digital agriculture initiatives in China and India.

- AI and data analytics integration are transforming farm decision-making and crop forecasting capabilities.

- Sustainability-focused farming practices are boosting adoption of smart irrigation and climate-resilient technologies.

What are the latest trends in the agriculture technology market?

Data-Driven Precision Farming Expansion

A major trend shaping the agriculture technology market is the shift toward data-centric farming ecosystems. Farmers increasingly rely on satellite imagery, soil sensors, and AI analytics platforms to monitor crop health, optimize fertilizer application, and reduce water consumption. Precision farming technologies allow variable-rate application of inputs, significantly improving productivity while lowering environmental impact. Cloud-based platforms now aggregate multi-source farm data, enabling predictive analytics for pest outbreaks and yield estimation. Agribusiness firms are integrating digital twins and predictive agronomy models, supporting proactive farm management decisions rather than reactive approaches.

Automation and Robotics in Agriculture

Agricultural robotics adoption is rising rapidly as farms seek operational efficiency and labor independence. Autonomous tractors, robotic harvesters, and drone-based spraying systems are increasingly deployed across large-scale farms. Robotics solutions are improving accuracy in planting, harvesting, and monitoring activities while reducing operational costs. Drone-enabled crop scouting and aerial analytics are becoming standard practices in high-value crop cultivation. The trend toward autonomous farming ecosystems is expected to redefine agricultural productivity benchmarks, particularly in developed markets facing aging farmer populations.

What are the key drivers in the agriculture technology market?

Rising Global Food Demand and Yield Optimization

Global population growth and changing dietary patterns are increasing pressure on agricultural output. Agriculture technology enables higher yields from limited arable land through optimized planting schedules, precision nutrient application, and climate monitoring. Governments and agricultural institutions are promoting digital farming solutions to ensure food security and improve farm profitability, making productivity enhancement a primary growth driver.

Labor Shortages and Mechanization Needs

Agricultural labor shortages across North America, Europe, and parts of Asia are accelerating automation adoption. Rising wages and workforce migration toward urban sectors have increased dependence on autonomous machinery and robotics. Smart mechanization solutions help farms maintain operational continuity while reducing long-term labor costs, driving sustained investment in agri-tech systems.

Government Support for Digital Agriculture

Public policies promoting sustainable farming and digital transformation are supporting rapid market expansion. National programs encouraging smart irrigation, drone usage, and AI-based advisory systems are improving technology accessibility. Subsidies, grants, and public-private partnerships are enabling small and mid-sized farmers to adopt advanced technologies, particularly in emerging economies.

What are the restraints for the global market?

High Initial Capital Investment

The adoption of agriculture technology requires significant upfront investment in hardware, software integration, and training. Smallholder farmers, especially in developing regions, face affordability challenges despite long-term cost savings. Financing gaps remain a critical barrier to widespread adoption.

Digital Infrastructure and Skill Gaps

Limited rural connectivity and lack of technical expertise hinder technology deployment in several agricultural regions. Farmers often require training to interpret analytics platforms effectively. Infrastructure disparities between developed and developing markets slow uniform adoption rates.

What are the key opportunities in the agriculture technology industry?

AI-Powered Climate-Smart Agriculture

Climate variability is creating opportunities for AI-driven predictive agriculture solutions. Technologies capable of forecasting weather risks, disease outbreaks, and irrigation requirements are becoming essential tools for farmers managing climate uncertainty. Companies developing adaptive analytics platforms can capture significant market share as sustainability becomes central to agricultural policy frameworks.

Digital Platforms for Smallholder Farmers

Emerging markets present strong growth opportunities through scalable subscription-based farm management platforms. Mobile-first solutions offering crop advisory, financing access, and supply-chain connectivity are enabling smallholders to participate in digital agriculture ecosystems. Governments and fintech firms are collaborating to integrate agri-tech with rural financial inclusion initiatives.

Carbon Farming and Sustainability Monetization

The emergence of carbon credit markets is opening new revenue streams for agriculture technology providers. Technologies that measure soil carbon, monitor emissions, and verify sustainable practices are gaining traction. Farms adopting regenerative practices supported by agri-tech tools can monetize sustainability outcomes, creating long-term demand for monitoring technologies.

Product Type Insights

Precision agriculture technologies continue to dominate the agriculture technology market, accounting for approximately 34% of the global market share in 2025. Adoption is fueled not only by measurable returns on investment through reduced fertilizer and pesticide usage but also by the need for sustainable farming practices and environmental compliance. Advanced sensors, soil monitoring systems, and variable-rate technology allow farmers to precisely manage inputs, optimize water and nutrient use, and enhance crop yields while minimizing environmental impact. Smart irrigation systems are experiencing rapid growth due to increasing water scarcity across key agricultural regions. These systems integrate real-time weather data, soil moisture sensors, and AI algorithms to optimize irrigation schedules, conserve water, and reduce operational costs. Agricultural robotics, including autonomous tractors, harvesters, and crop-spraying drones, are gaining momentum particularly in developed markets with high labor costs. These technologies enhance efficiency, reduce manual labor dependency, and support continuous farm operations. Farm management software platforms are becoming critical as farms transition to fully integrated digital ecosystems, combining data from field sensors, machinery, and market analytics to drive operational decisions. Drone-based monitoring technologies are also expanding, driven by lower hardware costs, improved sensor capabilities, and favorable regulatory frameworks enabling broader aerial surveillance for crop health, pest detection, and yield estimation.

Application Insights

Crop monitoring and yield management applications maintain the largest share, approximately 29% of the global market. Adoption is driven by increasing demand for predictive analytics, remote sensing, and real-time insights to optimize crop management practices. Farmers are increasingly relying on satellite imagery, drones, and IoT-enabled devices to monitor crop growth, detect diseases early, and make informed decisions on irrigation and fertilization. Precision planting and fertilization applications are gaining traction as they allow farmers to maximize efficiency, reduce input costs, and minimize environmental impact. Livestock monitoring is emerging as a high-growth application, facilitated by wearable sensors, RFID tagging, and connected farm management systems that track animal health, reproduction cycles, and behavior patterns. Post-harvest analytics and supply chain optimization applications are growing as food safety, traceability, and waste reduction become critical priorities for agribusinesses. Advanced analytics help monitor storage conditions, detect spoilage risks, and improve logistics planning, ultimately enhancing profitability and reducing losses in perishable goods supply chains.

Deployment Model Insights

Cloud-based deployment leads the market with an estimated 57% share in 2025. Cloud solutions provide scalability, remote accessibility, centralized data management, and the ability to integrate with AI and machine learning tools for predictive farming insights. They also facilitate collaborative farming practices, enabling multiple stakeholders—farmers, agronomists, and supply chain partners—to access real-time data simultaneously. On-premise solutions remain relevant for large-scale agribusinesses that require data sovereignty, offline operation capabilities, and enhanced control over sensitive operational data. Hybrid deployment models are gaining adoption as broadband and mobile connectivity improve in rural regions, enabling farms to leverage cloud benefits while maintaining critical local infrastructure. These models are particularly attractive in developing markets where infrastructure constraints and cybersecurity concerns coexist.

Farm Size Insights

Large commercial farms account for nearly 46% of total market demand, driven by capital-intensive investments in precision agriculture, robotics, and AI-based analytics that generate measurable efficiency gains. Medium-sized farms are increasingly adopting modular and scalable solutions, supported by financial instruments, subsidies, and digital agriculture programs aimed at promoting modernization. Smallholder farms represent the fastest-growing adoption segment, leveraging mobile platforms, low-cost sensors, and government or NGO-backed smart farming initiatives. Mobile-first technology adoption enables smallholders to access weather forecasts, crop recommendations, and market insights, bridging the digital divide and improving productivity. These trends are reshaping farm operations globally, with data-driven decision-making becoming a standard practice across farm sizes.

| By Product Type | By Application | By Deployment Model | By Farm Size |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America held approximately 32% of global market share in 2025, with the United States and Canada as leading contributors. The region’s growth is driven by high mechanization, robust agricultural research, and strong venture capital funding in agri-tech startups. Adoption of AI-driven analytics, autonomous machinery, and integrated farm management platforms is accelerating efficiency and reducing labor dependency. U.S. farmers are increasingly using machine learning models for predictive pest and disease management, while Canada focuses on precision irrigation, greenhouse automation, and climate-smart technologies to optimize crop production under varying weather conditions. Government programs, innovation grants, and collaboration with technology providers are key growth enablers, while growing awareness of sustainability and carbon reduction goals is prompting adoption of emission-monitoring and resource-efficient solutions.

Europe

Europe accounts for nearly 24% of global demand. Growth is supported by regulatory frameworks that incentivize sustainable farming, including subsidies for precision agriculture and environmental compliance. Germany, France, and the Netherlands are leaders in deploying smart greenhouse systems, robotic farm equipment, and advanced farm management software to optimize energy and input usage. EU policies, such as the Common Agricultural Policy (CAP), encourage adoption of low-emission technologies, soil health monitoring, and water-use efficiency solutions. Additionally, strong collaboration between universities, research institutes, and agri-tech companies fosters innovation and accelerates adoption of precision agriculture practices across commercial and smallholder farms. Consumer demand for sustainably produced food further reinforces the adoption of traceability and post-harvest optimization technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing market, driven by large agricultural economies including China, India, Japan, and Australia. China’s government-led digital agriculture modernization initiatives focus on AI-assisted crop management, IoT-based soil and water monitoring, and precision fertilization systems. India is witnessing rapid adoption among smallholders through mobile-based platforms, startup-led agri-tech solutions, and government-backed smart farming programs targeting yield improvement and resource efficiency. Australia and Japan are increasingly deploying robotics and autonomous machinery to address labor shortages and improve operational efficiency. Population growth, rising food demand, and government initiatives promoting technology adoption and rural connectivity are further driving regional expansion. Strategic investments by multinational agri-tech providers are also supporting technology penetration in emerging markets.

Latin America

Latin America’s growth is driven by large-scale commercial farming in Brazil and Argentina, where soybean, corn, and sugarcane production dominate. Precision agriculture adoption is expanding to increase yields, optimize input use, and enhance export competitiveness. Farm consolidation, mechanization, and access to technology financing are further enabling adoption of satellite monitoring, GPS-guided machinery, and precision fertilization solutions. Government programs promoting sustainable and climate-smart agriculture, alongside international investment in agri-tech, are key growth enablers. Additionally, the region’s focus on food exports and demand for consistent crop quality is driving deployment of post-harvest monitoring, storage optimization, and supply chain traceability solutions.

Middle East & Africa

The Middle East & Africa region is witnessing growing adoption of smart irrigation and controlled-environment agriculture technologies due to acute water scarcity, arid climates, and food security priorities. Israel and the UAE are pioneering greenhouse automation, hydroponics, and precision irrigation, making them hubs of innovation in the region. South Africa is increasingly implementing farm management platforms, data-driven decision support systems, and IoT-based monitoring to enhance productivity and optimize input efficiency. Regional growth is supported by government-led initiatives, private sector investment, and partnerships with agri-tech startups focused on sustainable, resource-efficient farming solutions. Water conservation, climate resilience, and export-oriented agriculture are driving technology adoption across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Agriculture Technology Market

- Deere & Company

- Trimble Inc.

- AGCO Corporation

- CNH Industrial N.V.

- Kubota Corporation

- Topcon Positioning Systems

- Raven Industries

- Bayer AG

- Corteva Agriscience

- Syngenta Group

- Valmont Industries

- Yara International

- Climate LLC

- Hexagon AB

- DJI Agriculture