Recirculating Aquaculture System Market Size

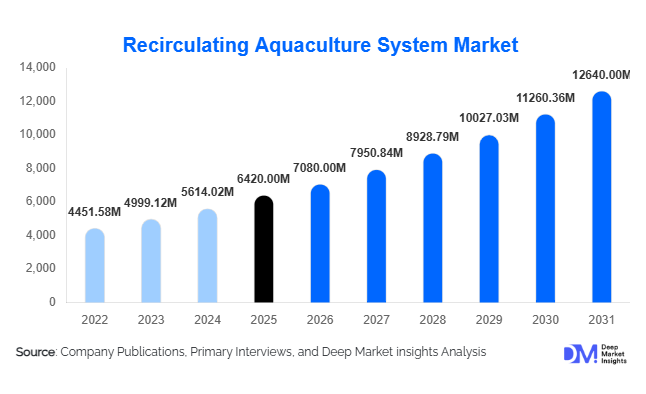

According to Deep Market Insights, the global recirculating aquaculture system (RAS) market size was valued at USD 6,420 million in 2025 and is projected to grow from USD 7,080 million in 2026 to reach approximately USD 12,640 million by 2031, expanding at a CAGR of 12.3% during the forecast period (2026–2031). Market expansion is driven by rising global seafood demand, tightening environmental regulations on open-water aquaculture, and increasing investments in land-based fish farming technologies. RAS solutions enable high-density fish production with reduced water usage, improved biosecurity, and year-round production cycles, making them increasingly attractive for commercial aquaculture operators.

Key Market Insights

- Land-based aquaculture adoption is accelerating globally, as governments push sustainable food production models.

- Salmon and high-value species farming dominate RAS deployment due to premium pricing and export demand.

- Europe leads technological adoption, supported by strict environmental regulations and innovation funding.

- Asia-Pacific represents the fastest-growing region, driven by seafood consumption growth in China, India, and Southeast Asia.

- Automation and AI-based water monitoring systems are improving operational efficiency and survival rates.

- Private equity investments and food security programs are accelerating large-scale commercial RAS projects worldwide.

What are the latest trends in the recirculating aquaculture system market?

Shift Toward Land-Based Sustainable Aquaculture

The aquaculture industry is transitioning from traditional open-net pens to controlled land-based systems to minimize environmental impact. RAS technology significantly reduces water discharge, prevents disease transmission from wild fish populations, and allows production near urban consumption centers. Governments across Europe and North America are promoting RAS farms to address overfishing concerns while maintaining seafood supply stability. Producers are increasingly locating facilities closer to major metropolitan markets to reduce logistics costs and carbon footprints.

Digitalization and Smart Aquaculture Systems

Technological integration is transforming RAS facilities into highly automated food production environments. IoT sensors, AI-driven feeding optimization, and real-time water chemistry monitoring are improving feed conversion ratios and reducing mortality rates. Predictive analytics tools are enabling farmers to anticipate disease outbreaks and optimize oxygen and filtration cycles. Robotics for cleaning tanks and automated grading systems are also becoming standard features in large-scale installations, improving labor efficiency and operational scalability.

What are the key drivers in the recirculating aquaculture system market?

Rising Global Seafood Consumption

Growing population levels and increasing protein consumption are driving seafood demand globally. Wild fisheries have reached sustainability limits, pushing governments and investors toward controlled aquaculture solutions. RAS systems enable consistent supply of premium fish species independent of seasonal or geographic limitations, making them critical to future seafood security.

Environmental Regulations and Biosecurity Requirements

Stricter environmental policies in regions such as the EU, Canada, and the United States are restricting traditional aquaculture expansion. RAS farms meet regulatory standards by reducing waste discharge and preventing ecological contamination. Biosecure indoor farming environments also reduce antibiotic use, aligning with global sustainability goals and consumer expectations.

Investment in Food Security Infrastructure

National food security initiatives are encouraging domestic seafood production. Governments are offering subsidies, grants, and low-interest financing for advanced aquaculture facilities. Institutional investors and sovereign funds are increasingly funding large-scale RAS salmon farms to stabilize protein supply chains and reduce reliance on imports.

What are the restraints for the global market?

High Initial Capital Investment

RAS facilities require substantial upfront investment for filtration systems, sensors, tanks, and climate control infrastructure. Capital intensity remains a major barrier for small and medium aquaculture operators, slowing adoption in developing markets.

Operational Complexity and Energy Consumption

Maintaining optimal water quality requires continuous monitoring and energy-intensive operations. Electricity costs and technical expertise requirements increase operating expenses, impacting profitability if production efficiencies are not optimized.

What are the key opportunities in the recirculating aquaculture system industry?

Urban and Nearshore Fish Farming

RAS enables fish farming close to consumption hubs, reducing transportation costs and ensuring fresher seafood supply. Urban aquaculture projects are gaining traction across Asia and Europe, creating opportunities for localized premium seafood brands.

Integration with Renewable Energy Systems

Energy costs represent a significant operational expense. Integration with solar, wind, and biogas systems is emerging as a strategic opportunity to reduce operating costs while improving sustainability credentials.

Expansion into New Species Cultivation

Beyond salmon, RAS adoption is expanding into shrimp, tilapia, barramundi, and ornamental fish farming. Species diversification improves revenue stability and allows producers to target regional consumer preferences and export markets.

System Component Insights

The global Recirculating Aquaculture Systems (RAS) market is fundamentally shaped by technological infrastructure, with water filtration and treatment systems emerging as the dominant system component, accounting for nearly 34% of the total market share in 2025. The leadership of this segment is primarily attributed to the critical role filtration plays in maintaining optimal aquatic environments, which directly influences fish survival, growth rates, and overall farm productivity. In RAS operations, water quality management determines operational success, making filtration technologies indispensable rather than optional investments.Modern aquaculture operations increasingly rely on advanced biological filtration, mechanical filtration, ultraviolet sterilization, degassing units, and oxygenation systems working together within integrated treatment frameworks. Biofilters enable the conversion of toxic ammonia into less harmful nitrates through microbial processes, significantly improving fish health and reducing mortality risks. Mechanical filtration systems remove suspended solids and organic waste, preventing pathogen growth and stabilizing water chemistry. As production densities increase within land-based aquaculture facilities, efficient filtration capacity becomes essential to sustain biomass levels without compromising environmental balance.The growing commercialization of high-density aquaculture has accelerated adoption of multi-stage filtration architectures capable of supporting continuous production cycles. Producers are increasingly investing in modular filtration systems that allow scalability and operational flexibility, enabling farms to expand output without rebuilding infrastructure. Furthermore, regulatory pressures surrounding wastewater discharge and environmental sustainability are encouraging adoption of advanced treatment technologies capable of minimizing ecological impact while maximizing water reuse efficiency.Technological innovation is also reshaping this segment through the integration of automated monitoring sensors that continuously assess dissolved oxygen, ammonia levels, pH balance, and turbidity. These real-time analytics systems allow predictive maintenance and early intervention, significantly reducing operational risks. As aquaculture operators transition toward precision aquaculture models, filtration systems evolve from passive infrastructure into intelligent ecosystem management platforms. Consequently, the leading driver for this segment remains the need for stable water quality in high-density aquaculture environments, which directly supports productivity, sustainability, and regulatory compliance across global markets.

Fish Species Insights

Among cultivated species, salmon farming dominates the global RAS market, accounting for approximately 28% of total market share in 2025. The leadership of salmon is strongly linked to its premium global demand, high export value, and well-established international supply chains. Salmon remains one of the most commercially valuable aquaculture species, making it an ideal candidate for capital-intensive RAS facilities where operational control and production predictability justify higher investment costs.Land-based salmon farming has gained significant traction in Europe and North America, where environmental regulations and concerns over ocean-based aquaculture—such as sea lice infestations, disease transmission, and ecosystem degradation—have encouraged alternative production methods. RAS technology enables producers to maintain precise control over temperature, salinity, and feeding conditions, resulting in consistent product quality and year-round harvest cycles. This operational reliability enhances supply stability for retailers and foodservice companies seeking dependable seafood sourcing.The expansion of inland salmon farms closer to consumer markets also reduces transportation costs and carbon emissions associated with long-distance seafood imports. Producers benefit from improved logistics efficiency and fresher product delivery, aligning with growing consumer preference for locally produced and sustainably farmed seafood. Moreover, advances in selective breeding and feed optimization have improved feed conversion ratios, further enhancing profitability within RAS salmon operations.Investment flows into large-scale salmon RAS facilities continue to increase as institutional investors recognize aquaculture’s potential to address global protein shortages. Government incentives supporting domestic seafood production and food security initiatives are also accelerating deployment. Therefore, the primary growth driver for this segment is the high economic value and global demand stability of salmon combined with the operational control enabled by land-based RAS farming, positioning it as the cornerstone species driving industry expansion.

System Type Insights

In terms of system configuration, closed-loop RAS systems dominate the industry, holding approximately 61% market share. Their leadership stems from unmatched water reuse efficiency and their ability to operate independently of natural water bodies. Closed-loop systems can recycle up to 99% of water, dramatically reducing freshwater consumption while maintaining consistent environmental conditions essential for intensive aquaculture.The increasing global focus on sustainable food production has significantly strengthened adoption of closed-loop systems. Regions facing water scarcity, climate variability, or strict environmental regulations increasingly prefer systems that minimize resource dependency. Unlike open or flow-through aquaculture models, closed-loop RAS facilities limit external contamination risks and provide biosecure environments that reduce disease outbreaks. This controlled production environment enhances yield predictability and lowers long-term operational risks.Additionally, closed-loop systems enable geographic flexibility, allowing aquaculture farms to operate far from coastal regions. This capability is transforming aquaculture into an urban-adjacent food production industry, supporting localized seafood supply chains and reducing import dependence. Technological advancements such as energy-efficient pumps, heat recovery systems, and integrated waste management solutions further enhance economic feasibility.As governments implement stricter environmental standards and carbon reduction goals, producers increasingly transition toward closed-loop infrastructure to meet compliance requirements. The leading driver behind this segment’s dominance is the growing need for water efficiency, environmental compliance, and biosecure aquaculture production systems, making closed-loop RAS the preferred architecture for future aquaculture expansion.

Farm Size Insights

Large-scale commercial farms account for nearly 52% of global RAS installations, reflecting the industrialization of aquaculture production. The transition from small experimental facilities to commercial-scale operations is driven by rising seafood demand, investor confidence, and technological maturity within the sector. Large farms benefit from economies of scale, allowing operators to optimize feed procurement, energy consumption, labor utilization, and distribution logistics.Vertically integrated seafood companies are increasingly adopting RAS technology to control the entire value chain—from hatchery operations to processing and distribution. This integration improves traceability, ensures consistent quality standards, and enhances brand positioning within premium seafood markets. Large-scale farms also attract institutional funding due to predictable revenue models supported by long-term supply agreements with retailers and foodservice providers.Automation and digital monitoring technologies further favor large installations by enabling centralized control over multiple production units. Advanced analytics optimize feeding schedules, growth monitoring, and environmental management, improving productivity while reducing human error. Governments supporting domestic seafood production through subsidies and infrastructure incentives are also encouraging expansion of industrial-scale RAS projects.The primary driver for this segment is the economic efficiency achieved through scale combined with increasing demand for reliable, export-quality seafood production, positioning large commercial farms as the backbone of global RAS capacity growth.

Technology Insights

Technological innovation plays a transformative role in the RAS ecosystem, with automated monitoring and control technologies accounting for approximately 31% of total market revenue. Automation is rapidly becoming essential as aquaculture operations grow more complex and production densities increase. Modern RAS facilities depend on interconnected sensors, artificial intelligence analytics, and cloud-based monitoring platforms to maintain precise environmental control.Automated systems continuously track parameters such as dissolved oxygen, temperature, pH, salinity, and nutrient concentrations. Real-time data analysis enables predictive decision-making, allowing operators to adjust feeding rates or water conditions before stress impacts fish populations. This proactive management approach significantly reduces mortality rates and improves feed efficiency, which represents one of the largest cost components in aquaculture production.Labor shortages in developed markets have also accelerated automation adoption, as digital technologies reduce reliance on manual monitoring and skilled technicians. Remote farm management capabilities allow operators to supervise multiple facilities simultaneously, improving operational scalability. Integration of machine learning algorithms further enhances performance optimization by identifying patterns in fish behavior and growth cycles.The leading growth driver for this segment is the industry-wide shift toward precision aquaculture aimed at improving productivity while minimizing labor dependency and operational risk. Automation technologies are expected to remain central to future RAS innovation and competitive differentiation.

End-Use Analysis

The food production industry remains the dominant end-use segment within the global RAS market, supported by increasing seafood consumption and rising consumer demand for traceable, antibiotic-free protein sources. Commercial aquaculture operations represent more than 70% of total demand, reflecting the growing role of controlled-environment fish farming in addressing global food security challenges. As wild fish stocks face overexploitation and climate-related disruptions, RAS facilities offer a stable alternative capable of delivering consistent production volumes independent of natural ecosystem fluctuations.Retail chains and foodservice companies increasingly prioritize supply transparency and sustainability certifications, encouraging producers to adopt land-based aquaculture systems that enable full traceability. Consumers are showing stronger preference for responsibly farmed seafood, particularly in North America and Europe, where sustainability labeling influences purchasing decisions. RAS technology supports these expectations by minimizing antibiotic usage and environmental discharge while ensuring uniform product quality.Research institutes and hatcheries represent a growing secondary end-use segment, utilizing RAS environments for breeding optimization, genetic improvement programs, and disease research. Controlled systems allow scientists to test feeding regimes and environmental conditions with precision, accelerating innovation across aquaculture species. Meanwhile, export-oriented seafood processing industries continue to expand, growing at approximately 6–7% annually, reinforcing demand for stable upstream fish supply supported by RAS production.Emerging applications such as pharmaceutical-grade fish oil extraction and premium ornamental fish farming are creating niche opportunities with higher profit margins. These specialized applications leverage RAS capabilities for contamination control and consistent product characteristics. Collectively, expanding global seafood demand and the need for sustainable protein production remain the overarching drivers strengthening end-use adoption worldwide.

| By System Component | By Fish Species | By System Type | By Farm Size | By Technology |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for nearly 24% of the global RAS market in 2025, led by the United States and Canada. Regional growth is strongly supported by rising consumer demand for sustainably sourced seafood and increasing investment in land-based aquaculture infrastructure. Governments and private investors are funding large-scale salmon farming projects aimed at reducing dependence on imported seafood while strengthening domestic production capacity.Regulatory scrutiny surrounding offshore aquaculture has accelerated adoption of land-based systems, particularly in Canada, where environmental policies encourage reduced ecological impact. Technological innovation hubs across the region foster collaboration between aquaculture companies, engineering firms, and research institutions, enabling rapid commercialization of advanced RAS solutions. Additionally, proximity to major consumer markets lowers transportation costs and improves product freshness, enhancing competitiveness against imported seafood.The key regional growth driver in North America is the combination of sustainability-driven consumer demand, regulatory pressure on ocean farming, and strong investment in domestic seafood production infrastructure, which collectively supports continued RAS expansion.

Europe

Europe holds approximately 31% market share, making it the largest regional market for RAS adoption. Countries such as Norway, Denmark, and the Netherlands lead installations due to longstanding aquaculture expertise and stringent environmental regulations promoting closed production systems. Norway represents a particularly significant contributor, accounting for a substantial portion of global land-based salmon investments.European Union sustainability policies and carbon reduction goals strongly favor water-efficient aquaculture technologies. Producers are transitioning toward RAS facilities to minimize marine ecosystem impacts while maintaining export competitiveness. High seafood consumption rates and established export networks further strengthen regional demand for technologically advanced aquaculture systems.Innovation funding programs and collaboration between universities and private companies continue to drive technological advancements, including energy-efficient system designs and digital monitoring solutions. The primary regional growth driver is the regulatory push toward environmentally sustainable aquaculture combined with Europe’s leadership in high-value salmon production.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, fueled by rapid population growth, rising income levels, and increasing seafood consumption. China, India, Vietnam, and Japan are actively expanding RAS infrastructure to secure reliable domestic protein supplies and reduce pressure on declining wild fisheries. Governments across the region are integrating aquaculture development into national food security strategies.China is investing heavily in large-scale RAS facilities to stabilize seafood supply chains and modernize aquaculture production. India is witnessing growing investment in shrimp RAS farms targeting export markets, supported by improving cold-chain logistics and processing capabilities. Urbanization trends and limited access to clean coastal waters are encouraging adoption of indoor aquaculture systems capable of operating near metropolitan consumption centers.Technological cost reductions and increasing availability of skilled aquaculture professionals further accelerate regional adoption. The leading growth driver in Asia-Pacific is the need to meet rapidly expanding seafood demand while ensuring food security through controlled and scalable aquaculture production.

Middle East & Africa

The Middle East is emerging as a strategic adopter of RAS technology due to severe water scarcity and heavy reliance on seafood imports. Countries such as the United Arab Emirates and Saudi Arabia are investing in indoor aquaculture facilities designed to support national food security initiatives. Controlled-environment systems allow fish production in arid climates where traditional aquaculture is not feasible.Government-backed investment programs and sovereign wealth funding are accelerating deployment of technologically advanced aquaculture infrastructure. Energy-efficient desalination integration and climate-controlled facilities enable consistent production despite extreme environmental conditions. In Africa, adoption remains at an early stage but shows strong potential in countries such as South Africa and Egypt, where aquaculture is expanding to address protein shortages and employment opportunities.The primary regional growth driver is the urgent need for food security solutions and sustainable water-efficient protein production in water-constrained environments.

Latin America

Latin America is witnessing gradual expansion of RAS adoption, led by Chile and Brazil. The region’s established salmon export industry is encouraging exploration of land-based aquaculture systems to mitigate disease risks and environmental challenges associated with ocean farming. Producers are increasingly evaluating RAS as a complementary production model capable of improving biosecurity and stabilizing output.Rising international seafood demand and export diversification strategies are encouraging investment in advanced aquaculture technologies. Governments and private operators are collaborating to modernize aquaculture infrastructure while improving sustainability standards required by global import markets. The region benefits from strong aquaculture expertise and favorable climatic conditions that support hybrid production approaches combining traditional and recirculating systems.The leading growth driver in Latin America is the need to enhance export reliability and reduce biological risks within established seafood industries through controlled land-based aquaculture production, positioning RAS as a strategic long-term investment across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Recirculating Aquaculture System Market

- AquaMaof Aquaculture Technologies Ltd.

- AKVA Group ASA

- Veolia Water Technologies

- Xylem Inc.

- Pentair plc

- Billund Aquaculture A/S

- Skretting

- PR Aqua

- MAT-KULING

- Aquacare Environment Inc.

- RAS Baltic

- Clewer Aquaculture Ltd.

- Fish Farm Solutions Ltd.

- BioFishency Ltd.

- Aquafarm Equipment AS