Agriculture ERP Market Size

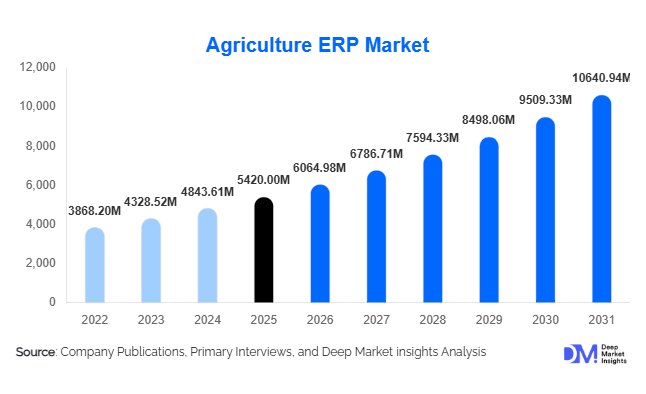

According to Deep Market Insights, the global agriculture ERP market size was valued at USD 5,420 million in 2025 and is projected to grow from USD 6,064.98 million in 2026 to reach approximately USD 10,640.94 million by 2031, expanding at a CAGR of 11.9% during the forecast period (2026–2031). Growth in the agriculture ERP market is being driven by rapid digital transformation across farming operations, increasing adoption of precision agriculture technologies, and the need for integrated farm-to-market data visibility. Agricultural enterprises are increasingly deploying ERP platforms to manage crop planning, inventory tracking, procurement, compliance reporting, and financial management within a unified digital ecosystem.

The market is experiencing strong momentum as agribusinesses shift from fragmented legacy systems toward cloud-based enterprise platforms capable of handling real-time analytics and predictive decision-making. Rising global food demand, climate variability, and supply chain volatility are pushing farmers and agribusiness companies to adopt technology-enabled operational planning. Governments worldwide are promoting smart agriculture initiatives and digital farming programs, accelerating ERP penetration across both developed and emerging markets. Additionally, integration of artificial intelligence, IoT-enabled sensors, satellite imaging, and blockchain-based traceability solutions is transforming ERP systems into strategic intelligence platforms rather than administrative tools. As agricultural value chains become increasingly globalized and compliance-intensive, agriculture ERP solutions are emerging as critical infrastructure supporting productivity, sustainability, and profitability across modern farming ecosystems.

Key Market Insights

- Cloud-based ERP deployments are dominating adoption, driven by scalability, remote farm management, and subscription pricing models.

- Large agribusiness enterprises lead demand, but SME farms are increasingly adopting modular ERP platforms.

- Asia-Pacific represents the fastest-growing region, supported by digital agriculture policies in India and China.

- Integration with precision agriculture technologies such as IoT sensors and satellite analytics is reshaping ERP functionality.

- Traceability and compliance management requirements across global food supply chains are accelerating ERP implementation.

- AI-driven forecasting and analytics are becoming standard features within next-generation agriculture ERP platforms.

What are the latest trends in the agriculture ERP market?

Shift Toward Intelligent Farm Management Platforms

Agriculture ERP systems are evolving beyond traditional enterprise resource planning toward intelligent farm management ecosystems. Modern platforms integrate crop analytics, weather forecasting, yield prediction, and automated input management into centralized dashboards. Farmers and agribusiness operators increasingly rely on predictive analytics to optimize irrigation schedules, fertilizer use, and harvesting timelines. These capabilities reduce operational inefficiencies while improving yield consistency. ERP vendors are embedding AI algorithms that analyze historical crop performance alongside real-time environmental data, enabling proactive decision-making. This transformation is positioning ERP platforms as operational command centers for digital agriculture.

Technology Integration Across the Agricultural Value Chain

ERP systems are increasingly integrating upstream and downstream supply chain functions, including seed suppliers, logistics providers, processors, and retailers. Blockchain-enabled traceability modules allow agribusinesses to monitor product origin, certification status, and transportation conditions, meeting rising consumer and regulatory transparency demands. Mobile-first ERP applications are also expanding adoption among field workers and smallholder farmers, allowing real-time data entry from farms. Integration with drones, remote sensing platforms, and machinery telemetry systems enables automated data collection, reducing manual reporting burdens while improving operational accuracy.

What are the key drivers in the agriculture ERP market?

Digital Transformation of Agriculture Operations

The increasing digitization of agriculture is a primary growth driver. Farms are transitioning into data-driven enterprises requiring integrated financial, operational, and agronomic management systems. ERP solutions enable centralized visibility across crop production cycles, procurement activities, labor management, and inventory planning. Rising farm consolidation and commercialization globally have intensified the need for scalable enterprise software capable of managing multi-location agricultural operations.

Rising Compliance and Traceability Requirements

Global food safety regulations and sustainability certifications are driving ERP adoption. Export-oriented producers must comply with traceability standards, environmental reporting frameworks, and quality assurance requirements. ERP systems automate compliance documentation and audit readiness, reducing administrative costs while improving regulatory adherence. Increasing retailer and consumer demand for transparent sourcing is further accelerating implementation.

Growth of Precision Agriculture Technologies

The proliferation of IoT sensors, GPS-enabled machinery, and satellite monitoring tools is generating large volumes of farm data. ERP platforms serve as integration layers that convert raw data into actionable insights. Farmers adopting precision agriculture technologies increasingly require ERP systems to consolidate agronomic and financial analytics into a unified decision-support framework.

Market Restraints

Despite strong growth, adoption barriers remain. High implementation costs and customization complexity limit adoption among smallholder farmers, particularly in developing economies. Additionally, limited digital literacy and inconsistent rural connectivity infrastructure create operational challenges for cloud-based deployments. Data security concerns and resistance to organizational change also slow transition from traditional farm management systems.

What are the key opportunities in the agriculture ERP industry?

Expansion into Emerging Agricultural Economies

Emerging markets across Asia, Africa, and Latin America present substantial opportunities due to increasing agricultural modernization initiatives. Governments are promoting digital farm registries, subsidy digitization, and smart irrigation programs, creating favorable environments for ERP adoption. Vendors offering localized language interfaces and modular pricing models can capture large untapped farmer populations.

AI and Predictive Analytics Integration

Embedding artificial intelligence into ERP systems enables predictive yield modeling, automated pest detection alerts, and resource optimization recommendations. Companies investing in AI-powered ERP modules can differentiate through higher productivity outcomes for users. Predictive analytics also supports financial forecasting and commodity price risk management for agribusiness enterprises.

Sustainability and Carbon Tracking Solutions

Growing emphasis on sustainable agriculture and carbon accounting is opening new ERP application areas. Platforms capable of tracking emissions, soil health metrics, and regenerative agriculture practices are gaining demand among exporters and food manufacturers seeking ESG compliance. Carbon credit management modules represent an emerging revenue stream for ERP providers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5420 Million |

| Market Size in 2026 | USD 6064.98 Million |

| Market Size in 2031 | USD 10640.94 Million |

| CAGR | 11.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Deployment Model Insights

The deployment landscape of agriculture ERP solutions has undergone a significant transformation over the past decade, with cloud-based ERP platforms emerging as the dominant delivery model across global agricultural enterprises. Cloud-based ERP solutions lead the market with approximately 62% share of the 2025 market, primarily driven by their operational flexibility, lower upfront capital expenditure, and ability to provide real-time access to farm and enterprise data across geographically dispersed operations. Unlike traditional on-premise systems that require extensive IT infrastructure and ongoing maintenance, cloud deployments enable agribusinesses to rapidly implement enterprise-grade solutions without substantial hardware investments.The increasing digitalization of agriculture has accelerated demand for scalable systems capable of integrating farm operations, procurement, logistics, inventory, compliance, and financial management into a unified platform. Cloud ERP systems allow stakeholders-including farm managers, agronomists, distributors, and executives-to access centralized data through mobile devices and web interfaces, supporting faster decision-making and operational transparency. Continuous software updates delivered through subscription-based models ensure that users benefit from evolving analytics capabilities, cybersecurity enhancements, and regulatory compliance features without disruption.Another major driver behind cloud adoption is the growing reliance on data-intensive technologies such as IoT-enabled sensors, satellite imagery, drone monitoring, and AI-driven predictive analytics. Cloud infrastructure provides the computing scalability required to process large agricultural datasets in real time, enabling predictive crop planning, weather risk management, and yield optimization. Additionally, cloud ERP platforms facilitate integration with third-party agricultural technologies, creating interconnected digital ecosystems that improve operational coordination across the agricultural value chain.While cloud solutions dominate, hybrid deployment models are gaining traction among large enterprises operating in regions with varying connectivity infrastructure.

Enterprise Size Insights

Enterprise adoption patterns indicate that large enterprises account for nearly 54% of the global market share, reflecting the complex operational structures of multinational agribusiness organizations. Large agricultural corporations manage extensive supply chains spanning cultivation, storage, processing, export logistics, and retail distribution, necessitating integrated enterprise systems capable of coordinating multiple business units across regions. ERP solutions enable centralized governance while supporting localized operational workflows, making them indispensable for large-scale agricultural operations.The leading driver supporting large enterprise dominance is the need for supply chain visibility and operational standardization across international markets. Agribusiness conglomerates must comply with varying regulatory standards, sustainability reporting requirements, and traceability mandates, all of which require unified digital platforms capable of consolidating operational data. ERP systems allow enterprises to synchronize production forecasts with procurement strategies, manage commodity price volatility, and optimize transportation logistics in real time.At the same time, small and medium-sized enterprises (SMEs) are emerging as a rapidly expanding customer segment. Historically constrained by cost barriers, SMEs are increasingly adopting modular ERP platforms designed specifically for mid-sized farms, cooperatives, and agri-startups. Subscription pricing, mobile-first interfaces, and simplified implementation models have significantly reduced adoption complexity. These solutions allow smaller producers to digitize inventory management, crop planning, and financial tracking while gradually scaling functionality as operations grow.Government digital agriculture programs and financial incentives across developing economies are further encouraging SME adoption. Access to affordable cloud ERP platforms allows smaller farms to compete more effectively in export markets by meeting traceability and quality certification standards. As digital maturity increases globally, SME adoption is expected to contribute substantially to future market expansion.

Application Insights

Among application categories, farm management and crop planning solutions dominate with around 28% market share, driven primarily by the industry’s transition toward data-driven agricultural decision-making. Modern farming operations increasingly rely on predictive analytics to optimize planting schedules, irrigation planning, fertilizer usage, and harvesting timelines. ERP platforms integrate agronomic datasets with financial and operational planning tools, enabling producers to align cultivation strategies with market demand forecasts and profitability targets.The leading driver behind this segment’s growth is the rising need to improve agricultural productivity amid climate variability and resource constraints. Farmers are leveraging ERP-enabled analytics to monitor soil health, weather patterns, pest risks, and crop performance in real time. By combining agronomic intelligence with enterprise resource planning capabilities, organizations can reduce operational waste, improve yield consistency, and enhance resource utilization efficiency.Additionally, crop planning modules increasingly integrate satellite imagery and sensor data, allowing predictive modeling that supports precision agriculture practices. These capabilities help farmers make informed decisions regarding seed selection, irrigation intensity, and nutrient application, ultimately improving production outcomes while reducing environmental impact. Financial forecasting integration further strengthens adoption, as producers can evaluate cost projections and revenue expectations before planting cycles begin.Beyond crop management, ERP applications are expanding into livestock monitoring, greenhouse automation, supply chain coordination, and compliance management. Traceability applications are gaining importance as global food safety regulations require transparent tracking from farm to consumer. As agriculture evolves into a technology-driven industry, ERP applications are transitioning from administrative tools into strategic operational intelligence platforms.

Component Insights

Software solutions represent approximately 68% of total revenue, underscoring the central role of ERP platforms as the technological backbone of digital agriculture ecosystems. The leading driver for software dominance is the increasing demand for integrated platforms capable of consolidating operational data across cultivation, finance, procurement, logistics, and compliance management functions. Enterprises are prioritizing unified systems over fragmented legacy tools to achieve operational efficiency and data consistency.Subscription-based licensing models have significantly contributed to software revenue growth by enabling continuous innovation cycles. Vendors regularly introduce advanced analytics, artificial intelligence modules, and automation features that enhance productivity while improving user experience. Software platforms also support interoperability with agricultural equipment, IoT devices, and third-party analytics systems, expanding their functional value beyond traditional ERP capabilities.Despite software dominance, services remain a critical component of market growth. Implementation, customization, consulting, training, and system integration services are essential because agricultural operations vary widely based on crop type, climate conditions, regulatory environments, and regional farming practices. Enterprises often require tailored workflows and localized compliance configurations, creating sustained demand for professional services.Managed services are gaining importance as organizations outsource system maintenance and optimization to ERP providers, allowing agricultural operators to focus on core production activities. Over time, service offerings are evolving toward long-term digital transformation partnerships rather than one-time implementation engagements, strengthening vendor-client relationships and driving recurring revenue streams.

End-Use Industry Insights

Agribusiness corporations hold nearly 46% market share, reflecting their advanced digital maturity and strong investment capacity in enterprise technologies. The leading driver for this segment is the growing complexity of global agricultural supply chains, which require synchronized management of procurement, storage, processing, transportation, and distribution activities. ERP systems provide centralized platforms that enable real-time coordination between suppliers, production facilities, and distribution networks.Food processors are increasingly adopting agriculture ERP solutions to enhance supplier visibility and ensure compliance with food safety and traceability regulations. Integration between farming operations and processing facilities allows companies to monitor raw material quality, track inventory movement, and maintain transparency throughout production cycles. As consumer demand for ethically sourced and traceable food products increases, ERP adoption becomes essential for maintaining brand trust and regulatory compliance.Agri-input manufacturers-including seed, fertilizer, and agrochemical producers-are also deploying ERP systems to optimize demand forecasting and distribution planning. These organizations rely on ERP analytics to align production schedules with seasonal farming cycles, reducing inventory inefficiencies. Agricultural cooperatives represent another important user group, leveraging ERP platforms to coordinate collective procurement, manage shared storage facilities, and streamline financial reporting for member farmers.

End-Use Analysis

Demand for agriculture ERP solutions is expanding across diverse agricultural end-use segments as digital transformation reshapes the global farming industry. Large commercial farms and agribusiness conglomerates remain primary adopters due to their operational scale and export-oriented production models. These organizations face increasing pressure to enhance productivity while managing risks associated with climate change, labor shortages, and fluctuating commodity prices. ERP systems enable centralized monitoring of operations, improving efficiency and decision accuracy.Food processing companies represent one of the fastest-growing adoption segments, as ERP systems enable supplier traceability and production synchronization across multiple facilities. Real-time integration between farm output and processing capacity reduces supply disruptions while improving product consistency. Additionally, ERP analytics help processors forecast demand trends, optimize production schedules, and minimize waste.Agri-input manufacturers and cooperatives are increasingly deploying ERP solutions to manage distribution networks and inventory planning more efficiently. These organizations benefit from predictive demand modeling that aligns product availability with planting seasons and regional crop cycles. Export-driven agriculture markets-particularly grains, fruits, and specialty crops-are accelerating ERP investments to meet stringent international certification and quality requirements.Emerging agricultural models such as vertical farming, greenhouse cultivation, and precision livestock management are further expanding ERP adoption. These technologically advanced farming environments rely heavily on automated monitoring systems and sensor-driven analytics, which ERP platforms integrate into centralized operational dashboards. As agriculture transitions toward controlled-environment production systems, ERP solutions play a critical role in managing data-intensive operations and ensuring profitability.

Explore more data points, trends and opportunities Download Free Sample Report

Agriculture ERP Market Segmentations

By Deployment Type

- Cloud-Based Agriculture ERP

- On-Premise Agriculture ERP

- Hybrid ERP Solutions

By Component

- ERP Software Platforms

- Implementation & Integration Services

- Consulting Services

- Support & Maintenance Services

By Farm Type

- Crop Farming Operations

- Livestock & Dairy Farming

- Aquaculture & Fisheries

- Mixed Farming Enterprises

- Agribusiness & Plantation Management

By Enterprise Size

- Large Agricultural Enterprises

- Small & Medium Farms

By End Use

- Commercial Farms

- Agricultural Cooperatives

- Food Processing Companies

- Agri-Input Suppliers

- Agricultural Exporters & Traders

Regional Insights

North America

North America accounted for approximately 34% of the global market share in 2025, positioning the region as the leading adopter of agriculture ERP technologies. The United States and Canada benefit from highly mechanized farming systems, advanced IT infrastructure, and strong investment in agricultural innovation. One of the primary drivers of regional growth is the widespread adoption of precision agriculture technologies, including GPS-guided machinery, IoT-enabled sensors, and AI-powered analytics platforms that require integrated data management systems.Large agribusiness enterprises in the region are investing heavily in analytics-driven farm management platforms to improve yield forecasting and operational efficiency. The presence of major technology providers and agri-tech startups accelerates innovation and integration capabilities, enabling seamless connectivity between ERP platforms and digital farming tools. Additionally, strict food safety regulations and traceability requirements encourage companies to adopt ERP solutions for compliance management and supply chain transparency.Labor shortages in agricultural sectors further drive automation and digitalization initiatives, increasing reliance on ERP systems to optimize workforce planning and operational scheduling. Sustainability initiatives focused on reducing environmental impact and improving resource efficiency also contribute to ERP adoption, as organizations use digital platforms to track emissions, water usage, and input efficiency metrics.

Europe

Europe represents nearly 26% market share, supported by strong regulatory frameworks and sustainability-focused agricultural policies. Countries such as Germany, France, the Netherlands, and Spain are leading adopters due to their advanced agricultural export industries and cooperative farming structures. A major driver of regional growth is the European Union’s emphasis on digital agriculture and sustainability reporting under environmental policies and subsidy programs.Farm subsidy digitization initiatives require accurate data collection and reporting, encouraging farmers and cooperatives to deploy ERP systems capable of managing compliance documentation efficiently. European agriculture also places strong emphasis on traceability, organic certification, and environmental accountability, all of which benefit from integrated ERP platforms that consolidate operational and compliance data.The region’s strong cooperative farming culture further accelerates ERP adoption, as shared digital platforms enable collective resource planning and financial management. Additionally, increasing consumer demand for transparent food sourcing encourages producers and exporters to implement ERP-driven traceability solutions that track products throughout the supply chain. Investments in smart farming technologies across Western and Northern Europe continue to strengthen market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at over 14% CAGR during the forecast period. Rapid population growth, rising food demand, and government-led agricultural modernization programs are key drivers supporting regional expansion. China and India lead adoption through national smart agriculture initiatives aimed at improving productivity, farm income stability, and food security.Government subsidies promoting farm mechanization and digital infrastructure development are accelerating ERP implementation among large farms and agricultural cooperatives. Increasing smartphone penetration and mobile connectivity enable cloud-based ERP adoption even in rural farming communities, allowing farmers to access operational data remotely. The shift toward organized agricultural supply chains and export-oriented production further strengthens demand for integrated enterprise systems.Australia and Japan demonstrate strong adoption in high-value crop farming and technologically advanced agricultural operations. These markets prioritize efficiency, automation, and resource optimization, encouraging ERP deployment for precision farming management. Rising investments in agri-tech startups across Southeast Asia also contribute to regional growth, as digital platforms become essential tools for modern agricultural ecosystems.

Latin America

Latin America is emerging as a significant growth market, with Brazil and Argentina dominating regional demand due to their large-scale agricultural exports. The leading driver of ERP adoption in the region is the expansion of commercial farming operations focused on soybean, corn, and grain exports. Plantation operators increasingly rely on ERP platforms to manage logistics optimization, inventory tracking, and yield monitoring across vast cultivation areas.Export competitiveness requires adherence to international quality standards and traceability requirements, encouraging producers to digitize operational workflows. ERP systems help agricultural enterprises manage fluctuating commodity prices by improving financial forecasting and cost control. Additionally, improvements in rural connectivity and increasing investment in agricultural technology infrastructure are enabling broader adoption among mid-sized farms.Government initiatives promoting agricultural productivity and sustainability practices are further supporting digital transformation across the region. As agribusiness companies expand global trade partnerships, ERP platforms become essential for coordinating supply chains and maintaining operational transparency.

Middle East & Africa

The Middle East and Africa region is witnessing steady adoption of agriculture ERP solutions, driven primarily by the need to improve food security and optimize resource utilization in challenging climatic conditions. Countries such as Israel, South Africa, and the United Arab Emirates are leading regional adoption through investments in smart irrigation, greenhouse farming, and controlled-environment agriculture.A key growth driver is the increasing focus on water-efficient agricultural practices. ERP platforms enable monitoring of irrigation schedules, resource consumption, and crop performance, helping farmers maximize productivity while conserving scarce resources. Government-backed digital agriculture initiatives across African nations are encouraging modernization of farming operations through technology adoption and training programs.Greenhouse farming expansion and hydroponic cultivation systems require integrated operational management tools, further supporting ERP demand. Additionally, international development programs and private investments aimed at strengthening agricultural supply chains are accelerating ERP deployment across emerging markets. As digital infrastructure improves across the region, adoption is expected to expand significantly over the forecast period.

Key Players in the Agriculture ERP Market

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Trimble Inc.

- Deere & Company

- Ag Leader Technology

- FarmERP

- Aptean Inc.

- NetSuite (Oracle NetSuite ERP)

- Epicor Software Corporation

- IFS AB

- Sage Group plc

- Unit4

- Blue Yonder Group