High Pressure Processing (HPP) Food Market Size

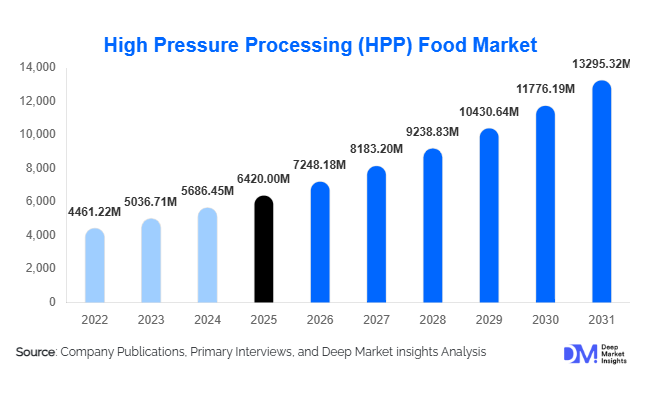

According to Deep Market Insights, the global high pressure processing (HPP) food market size was valued at USD 6,420 million in 2025 and is projected to grow from USD 7,248.18 million in 2026 to reach USD 13,295.32 million by 2031, expanding at a CAGR of 12.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for minimally processed, preservative-free food products, rising consumer preference for clean-label beverages and ready-to-eat meals, and technological advancements enabling extended shelf life without compromising nutritional quality.

Key Market Insights

- Clean-label food demand is accelerating HPP adoption, as the technology eliminates pathogens without chemical preservatives.

- Cold-pressed juices and functional beverages dominate applications, supported by premiumization trends and health-conscious consumers.

- North America leads global adoption due to strong infrastructure and early commercialization of HPP tolling services.

- Asia-Pacific is the fastest-growing region, driven by urbanization and expanding processed food consumption in China and India.

- Retail and foodservice sectors increasingly rely on HPP to improve shelf stability and reduce food waste.

- Automation and equipment innovation are lowering processing costs and expanding adoption among mid-sized food manufacturers.

What are the latest trends in the High Pressure Processing (HPP) food market?

Expansion of Clean-Label and Fresh-Like Foods

Consumers increasingly demand foods that maintain fresh taste, texture, and nutritional integrity while ensuring safety and longer shelf life. HPP technology aligns perfectly with these expectations by inactivating pathogens using pressure instead of heat. This has enabled manufacturers to launch preservative-free guacamole, dips, deli meats, dairy alternatives, and functional beverages. Retailers are prioritizing refrigerated premium foods with shorter ingredient lists, positioning HPP as a core processing method supporting transparency and health-focused consumption trends.

Rise of HPP Tolling and Shared Processing Facilities

The emergence of tolling service providers has significantly reduced capital barriers for small and medium food brands. Instead of investing in expensive HPP machinery, manufacturers outsource processing to specialized facilities, accelerating innovation cycles and new product launches. This business model is particularly impactful for startups producing cold-pressed juices, plant-based meals, and premium sauces. Expansion of contract processing hubs across North America and Europe is helping scale production while maintaining operational flexibility.

What are the key drivers in the High Pressure Processing food market?

Growing Demand for Food Safety and Shelf-Life Extension

Global food supply chains require technologies that ensure microbiological safety without degrading product quality. HPP significantly reduces pathogens such as Listeria and Salmonella while preserving sensory attributes. Food recalls and stricter safety regulations have encouraged processors to adopt non-thermal preservation technologies, strengthening HPP adoption across meat, seafood, and ready-meal categories.

Premiumization of Beverages and Functional Foods

Health-focused consumers increasingly prefer cold-pressed juices, probiotic drinks, and nutrient-rich smoothies. HPP enables preservation of vitamins, enzymes, and natural flavors, supporting premium product positioning and higher price realization. Beverage brands leveraging HPP technology typically achieve longer refrigerated shelf life, expanding distribution reach and export potential.

Retail Expansion of Refrigerated Convenience Foods

Urban lifestyles and demand for ready-to-eat meals have boosted refrigerated packaged food segments globally. HPP allows manufacturers to scale distribution without freezing or artificial preservatives, making it highly attractive for meal kits, deli proteins, and plant-based offerings.

What are the restraints for the global market?

High Equipment Capital Costs

HPP machinery requires significant upfront investment, often exceeding several million dollars per installation. This limits adoption among smaller processors in developing markets and increases dependency on tolling facilities.

Packaging Compatibility Constraints

Products processed through HPP must use flexible, water-resistant packaging materials capable of withstanding extreme pressure. Packaging redesign requirements add complexity and cost, particularly for legacy food brands transitioning to HPP.

What are the key opportunities in the HPP food industry?

Expansion into Emerging Asian Markets

Rapid urbanization and rising disposable incomes across Asia-Pacific present strong growth opportunities. Governments encouraging food safety modernization are supporting adoption of advanced preservation technologies, enabling new entrants to establish regional processing hubs.

Plant-Based and Alternative Protein Applications

The rise of plant-based diets creates opportunities for HPP-treated meat alternatives, dairy substitutes, and protein snacks. HPP enhances product safety while preserving texture, enabling premium positioning within fast-growing alternative protein markets.

Export-Oriented Fresh Food Supply Chains

HPP technology enables extended shelf life for refrigerated foods, allowing exporters to ship fresh products across continents without freezing. This supports cross-border trade in seafood, avocado products, sauces, and functional beverages, creating strong growth avenues for processors targeting international markets.

Product Type Insights

High Pressure Processing (HPP) product segmentation continues to evolve as food manufacturers increasingly prioritize clean-label preservation, extended refrigerated shelf life, and premium product differentiation. HPP beverages remain the leading product category, accounting for approximately 34% of the global market in 2025. Growth in this segment is primarily supported by accelerating consumer demand for minimally processed cold-pressed juices, plant-based beverages, probiotic drinks, and functional wellness formulations that require microbial safety without thermal degradation. The leading segment driver is the rising global preference for nutrient-retaining preservation technologies that maintain flavor authenticity, color stability, and vitamin integrity while eliminating artificial preservatives. Beverage brands are leveraging HPP to position products within premium health-focused retail categories, particularly across urban markets where consumers increasingly associate freshness with refrigerated distribution.Meat and poultry products represent the second-largest product category, supported by increasing regulatory scrutiny surrounding pathogen control and foodborne illness prevention. HPP enables processors to achieve validated pathogen reduction while maintaining raw-like texture and product quality, making it particularly valuable for ready-to-cook and marinated protein products. Adoption is further supported by export-oriented processors seeking compliance with international safety standards and extended logistics flexibility. The technology also allows manufacturers to reduce chemical preservatives while meeting retailer safety certifications, strengthening adoption across premium protein supply chains.

Seafood applications are expanding rapidly, especially in shellfish processing where HPP significantly improves product yield and operational efficiency. Pressure-assisted shucking reduces manual labor requirements while enhancing meat recovery rates and improving worker safety. This advantage has accelerated adoption among lobster, oyster, and crab processors supplying international markets. Additionally, HPP improves texture consistency and shelf-life stability, enabling exporters to reach distant markets without compromising freshness perception.Fruits and vegetable-based products, including guacamole, salsa, dips, and fresh purees, continue to gain market traction as retailers expand refrigerated clean-label offerings. The segment benefits from strong consumer demand for preservative-free convenience foods that retain fresh sensory characteristics. HPP supports oxidation control and microbial stability without thermal processing, allowing brands to maintain natural taste profiles while extending distribution reach. Growth in premium ready-to-eat snacking and refrigerated meal components continues to reinforce demand within this category.

Application Insights

From an application perspective, pathogen reduction remains the dominant use case, contributing nearly 41% of market share in 2025. The leading application driver is the increasing global emphasis on food safety compliance and risk mitigation across supply chains. Regulatory agencies and retailers are enforcing stricter microbial safety requirements, encouraging processors to adopt non-thermal technologies capable of eliminating pathogens such as Listeria, Salmonella, and E. coli while preserving product quality. HPP provides validated lethality performance without compromising sensory attributes, making it highly attractive across multiple food categories.Shelf-life extension applications are experiencing rapid expansion, particularly within refrigerated ready meals, meal kits, and fresh convenience foods. As modern retail formats shift toward fresh and minimally processed offerings, manufacturers require technologies that support longer distribution cycles without preservatives. HPP enables extended shelf life while maintaining fresh-like characteristics, reducing food waste and improving inventory efficiency for retailers and logistics operators. The growth of e-commerce grocery delivery and cross-border cold-chain distribution further amplifies this application demand.Texture modification applications are gaining prominence in seafood and premium protein processing, where pressure treatment enhances tenderness and improves consistency. The technology allows processors to optimize mouthfeel characteristics while maintaining raw product positioning. This capability is increasingly utilized in high-value seafood exports and gourmet protein products targeting foodservice and premium retail segments.Nutritional preservation applications are expanding across functional foods, nutraceutical beverages, and wellness-focused product formulations. Manufacturers increasingly adopt HPP to retain bioactive compounds, antioxidants, and heat-sensitive nutrients that are typically degraded during thermal pasteurization. As consumers prioritize health-driven consumption and ingredient transparency, nutritional preservation is emerging as a strategic application supporting premium product positioning.

Distribution Channel Insights

Direct B2B supply to food manufacturers remains the dominant distribution channel, accounting for over 52% of industry revenue. Long-term processing contracts between HPP equipment providers, toll processors, and large food manufacturers ensure operational continuity and capacity utilization. Large-scale beverage and ready-meal producers increasingly integrate HPP into centralized processing hubs to optimize economies of scale while maintaining consistent quality standards across product lines.Tolling service providers represent the fastest-growing distribution model as emerging brands and startups seek access to HPP capabilities without significant capital expenditure. The high upfront cost of pressure vessels encourages outsourcing, enabling smaller companies to launch premium refrigerated products while minimizing financial risk. This model has played a critical role in accelerating innovation within cold-pressed juices, plant-based foods, and specialty functional products.Retail private-label adoption is steadily increasing as supermarket chains expand preservative-free refrigerated portfolios. Retailers are partnering with contract processors to introduce clean-label store brands that compete directly with premium branded products. The expansion of private-label innovation reflects growing consumer trust in retailer-owned health-focused offerings and supports broader commercialization of HPP-enabled foods across mainstream markets.

End-Use Industry Insights

The beverage industry leads end-use demand, accounting for nearly 36% market share, supported by continuous innovation in premium juices, plant-based beverages, and functional drinks. The leading segment driver is the global shift toward health-oriented consumption patterns combined with consumer preference for minimally processed beverages that retain natural taste and nutritional value. Beverage manufacturers increasingly rely on HPP to differentiate products through freshness claims and clean-label positioning while meeting food safety standards.Ready-to-eat food manufacturers represent the fastest-growing end-use segment, expanding at double-digit rates as urbanization and busy lifestyles accelerate demand for convenient refrigerated meals. HPP enables extended shelf life without compromising quality, allowing producers to scale distribution across regional and international markets. Growth in meal subscription services and fresh prepared foods further strengthens adoption.Seafood exporters are increasingly integrating HPP into processing operations to enhance yield, improve product safety, and extend export shelf life. The technology supports global trade by enabling longer transit durations while maintaining premium product quality, particularly for high-value shellfish and fresh seafood products destined for distant consumer markets.Foodservice operators and meal kit companies are emerging end users, leveraging HPP to maintain ingredient freshness throughout complex distribution networks. As restaurant chains and delivery platforms expand centralized production models, HPP offers a scalable solution to ensure consistent product safety and quality across multiple locations.

| By Product Type | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 38% of the global market in 2025, supported by highly advanced food processing infrastructure and early commercialization of HPP technology. The United States leads regional adoption due to strong consumer demand for clean-label refrigerated foods and widespread availability of cold-chain logistics. A key regional growth driver is stringent food safety enforcement combined with retailer requirements for pathogen control validation, which encourages processors to adopt non-thermal preservation technologies. The expansion of premium juice brands, ready-to-eat meal providers, and private-label refrigerated foods continues to stimulate equipment installations. Canada is witnessing rising adoption in seafood and meat export industries, where HPP enhances compliance with international safety standards while improving export shelf stability.

Europe

Europe holds around 27% market share, driven by strong adoption across Germany, France, Spain, and the United Kingdom. Regional growth is primarily supported by strict regulatory frameworks governing food safety and labeling transparency, which encourage adoption of preservative-free processing technologies. Increasing consumer preference for organic, minimally processed foods and premium chilled ready meals further accelerates demand. Southern European countries, particularly Spain, play a significant role due to strong fruit processing and juice manufacturing industries. Additionally, sustainability initiatives promoting food waste reduction are encouraging processors to adopt HPP for shelf-life extension without chemical additives.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, led by China, Japan, South Korea, and India. Rapid urbanization, expanding middle-class populations, and rising consumption of packaged fresh foods are key regional growth drivers. Governments across the region are investing heavily in food safety modernization programs following heightened consumer awareness regarding food contamination risks. Increasing penetration of modern retail formats and cold-chain infrastructure is enabling wider commercialization of HPP-enabled products. Japan and South Korea demonstrate strong adoption in premium convenience foods, while China and India are witnessing growing investments in advanced food processing technologies to support domestic consumption and export competitiveness.

Latin America

Latin America is emerging as a strategically important region, with strong adoption in Mexico, Chile, and Brazil. Regional growth is largely driven by export-oriented agricultural industries, particularly avocado products, tropical fruit preparations, and seafood destined for North American markets. HPP enables exporters to meet stringent import safety standards while maintaining product freshness during long-distance transportation. Increasing investments in food processing modernization and value-added agricultural exports are encouraging regional processors to adopt advanced preservation technologies.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but steady growth, led by the United Arab Emirates, Saudi Arabia, and South Africa. A major regional driver is rising dependence on imported premium packaged foods combined with government investments in food security and domestic processing capabilities. Expansion of modern retail infrastructure and demand for high-quality refrigerated products are encouraging adoption of HPP technologies. Additionally, hospitality sector growth and premium foodservice expansion are increasing demand for extended shelf-life fresh products suitable for complex distribution environments across climatic conditions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the High Pressure Processing (HPP) Food Market

- JBT Corporation

- Hiperbaric

- Avure Technologies

- Universal Pure

- HPP Italia

- Next HPP

- American Pasteurization Company

- SafePac Pasteurization

- Cold Pressure Council Members (Processing Operators)

- Stansted Fluid Power

- Kobe Steel Ltd.

- Bertuzzi Food Processing

- Multivac Group

- Espuna (HPP Meat Processing)

- Hormel Foods Corporation