AgTech Ecosystem Market Size

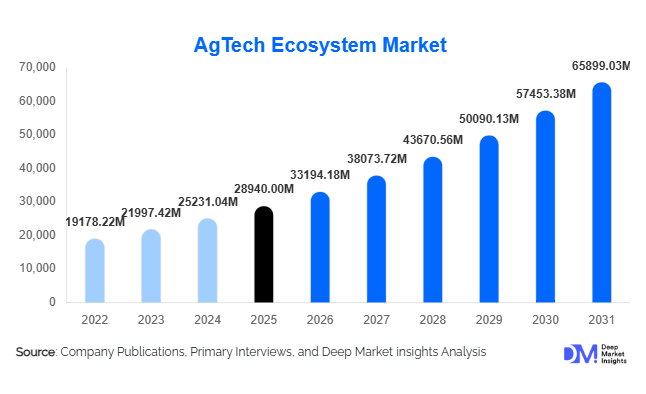

According to Deep Market Insights, the global AgTech ecosystem market size was valued at USD 28,940 million in 2025 and is projected to grow from USD 33,194.18 million in 2026 to reach approximately USD 65,899.03 million by 2031, expanding at a CAGR of 14.7% during the forecast period (2026–2031). The market expansion is driven by accelerating digital transformation in agriculture, increasing pressure to improve crop productivity amid climate variability, and rising adoption of precision farming technologies across developed and emerging economies. Governments and agribusinesses worldwide are investing heavily in smart farming infrastructure, AI-enabled analytics, robotics, and connected farm ecosystems to enhance yield efficiency while reducing resource consumption.

The AgTech ecosystem integrates hardware, software, services, data analytics, biotechnology, and financial platforms into a unified agricultural value chain. Farmers are increasingly shifting from traditional input-based farming toward data-driven decision-making supported by satellite imagery, IoT sensors, and predictive analytics. Rising food demand, labor shortages, water scarcity, and sustainability mandates are pushing stakeholders toward automation and precision agriculture solutions. Large commercial farms are early adopters, while smallholder farmers are entering the ecosystem through mobile-based advisory platforms and digital marketplaces. The market is also witnessing convergence between agriculture and fintech, logistics technology, and climate intelligence platforms, creating an interconnected ecosystem rather than standalone technologies. Over the next five years, AgTech adoption is expected to accelerate rapidly in Asia-Pacific and Latin America, where food security concerns and government-backed digitization initiatives are reshaping agricultural productivity models globally.

Key Market Insights

- Precision agriculture platforms represent the fastest adoption segment, enabling optimized fertilizer, irrigation, and crop monitoring decisions.

- AI and data analytics are becoming core farm management tools, transforming agriculture into a predictive and automated industry.

- North America leads global adoption due to large farm sizes and advanced mechanization infrastructure.

- Asia-Pacific is the fastest-growing regional market, supported by digital agriculture initiatives in India and China.

- Climate-smart agriculture solutions are emerging as key investment areas driven by sustainability regulations.

- Agri-fintech and digital marketplaces are expanding ecosystem participation among smallholder farmers.

What are the latest trends in the AgTech ecosystem market?

Data-Driven Farming and AI Integration

A major trend shaping the AgTech ecosystem is the rapid adoption of artificial intelligence and predictive analytics platforms. Farmers increasingly rely on AI-powered crop health monitoring, yield forecasting, pest prediction models, and automated farm recommendations. Satellite imagery combined with machine learning algorithms enables real-time field diagnostics, reducing crop losses and improving productivity. Agricultural enterprises are integrating multiple data streams—including weather, soil, and machinery performance—into unified dashboards that optimize farm operations. This shift toward data-centric agriculture is transforming farms into digitally managed production units.

Automation and Agricultural Robotics Expansion

Labor shortages and rising operational costs are accelerating the deployment of autonomous tractors, robotic harvesters, and drone-based spraying solutions. Robotics adoption is particularly strong in high-value crops such as fruits, vegetables, and vineyards where precision harvesting improves profitability. Autonomous machinery reduces dependency on seasonal labor while improving operational accuracy. The emergence of Robotics-as-a-Service (RaaS) models is also lowering entry barriers, enabling medium-sized farms to adopt automation without high capital expenditure.

What are the key drivers in the AgTech ecosystem market?

Rising Global Food Demand and Yield Optimization

Growing global population and changing dietary patterns are increasing pressure on agricultural productivity. AgTech solutions enable precision input management, improving yields while minimizing waste. Governments and agribusinesses increasingly promote smart farming to ensure food security, making productivity enhancement a primary growth driver.

Climate Change and Resource Efficiency Requirements

Climate volatility has intensified demand for technologies that improve resilience against droughts, floods, and unpredictable weather patterns. Smart irrigation systems, climate analytics platforms, and soil monitoring sensors help farmers optimize water usage and mitigate environmental risks. Sustainability compliance and carbon reduction initiatives further accelerate adoption.

Digital Infrastructure Expansion in Rural Economies

Improved rural connectivity, cloud adoption, and smartphone penetration are enabling digital agriculture platforms to scale rapidly. Mobile advisory tools and farm management software are expanding access among smallholder farmers, particularly across Asia and Africa.

What are the restraints for the global market?

High Initial Investment Costs

Advanced AgTech systems require significant upfront investments in sensors, machinery, and software integration. Small and medium-scale farmers often face affordability challenges despite long-term productivity benefits, slowing adoption in developing regions.

Data Fragmentation and Interoperability Challenges

The AgTech ecosystem includes multiple platforms that often lack compatibility. Fragmented data standards create integration challenges between equipment manufacturers, analytics providers, and farm management systems, limiting seamless ecosystem scalability.

What are the key opportunities in the AgTech ecosystem industry?

Climate-Smart Agriculture Solutions

Climate resilience technologies represent a major opportunity for both startups and established agribusiness companies. Solutions focused on carbon monitoring, regenerative agriculture analytics, and sustainable input optimization are attracting strong investment from governments and ESG-focused funds. Carbon credit integration within farm platforms is expected to create new revenue streams for farmers.

Digital Agriculture in Emerging Economies

Countries across Asia, Africa, and Latin America are investing in digital agriculture programs to modernize farming practices. Mobile-based advisory services, fintech-enabled input financing, and marketplace platforms are expanding technology adoption among millions of smallholder farmers, creating massive untapped market potential.

Integration of Agri-Fintech and Supply Chain Platforms

The convergence of finance, logistics, and agricultural analytics offers opportunities to build end-to-end farm ecosystems. Digital lending platforms, crop insurance analytics, and traceability solutions are improving transparency across food supply chains, benefiting exporters and global food processors.

Segmental Analysis

The global AgTech ecosystem market demonstrates strong structural diversification across multiple segments, reflecting the evolving digital transformation of agriculture worldwide. Technological innovation, increasing pressure on food systems, climate variability, and the growing need for operational efficiency are collectively shaping adoption trends across solution types, technologies, deployment models, farm sizes, and application areas. Each segment contributes uniquely to market expansion, but leadership positions are largely defined by measurable productivity gains, scalability advantages, and the ability to deliver data-driven decision-making capabilities to farmers and agribusiness enterprises.

Solution Type: Precision farming solutions lead the global market, accounting for nearly 29% of the total market share in 2025. The dominance of this segment is primarily driven by the increasing demand for yield optimization and resource efficiency across modern agricultural operations. Precision farming integrates satellite positioning, advanced analytics, automated machinery, and predictive agronomic modeling to enable site-specific crop management. Farmers are increasingly shifting away from uniform field treatment toward variable-rate application of fertilizers, irrigation, and pesticides, allowing them to reduce operational costs while maximizing productivity. The rapid adoption of GPS-enabled tractors, autonomous equipment, and decision-support software platforms further strengthens segment growth. Additionally, rising environmental regulations encouraging efficient input utilization are accelerating investment in precision agriculture tools. Large agribusiness companies and commercial farms are particularly motivated to adopt precision farming technologies as they seek measurable improvements in profitability, sustainability compliance, and long-term soil health management. The integration of artificial intelligence into precision platforms is further enhancing predictive yield analytics, enabling farmers to anticipate weather risks, pest outbreaks, and nutrient deficiencies before they impact crop performance.

Technology Type: IoT-based agricultural monitoring dominates the technology segment with approximately 24% market share, supported by widespread deployment of connected sensors and real-time monitoring infrastructure. The leading driver behind this segment is the growing requirement for continuous field intelligence and data visibility across agricultural operations. IoT devices collect granular data related to soil moisture levels, microclimatic conditions, crop growth patterns, irrigation efficiency, and livestock health parameters. This real-time data enables farmers to make informed decisions that minimize waste and enhance productivity. Advances in low-power wide-area networks and improved rural connectivity are making sensor deployment more economically viable, even in developing agricultural regions. The increasing affordability of sensor hardware combined with cloud analytics platforms allows farms of varying scales to adopt smart monitoring systems. Moreover, integration between IoT platforms and automated irrigation or fertilization systems creates closed-loop agricultural ecosystems where decisions are executed automatically based on live data inputs. As climate uncertainty increases globally, farmers rely more heavily on predictive monitoring technologies to manage risks associated with droughts, floods, and temperature fluctuations, further strengthening the adoption of IoT-driven agriculture.

Deployment Mode: Cloud-based platforms hold around 61% market share, making them the dominant deployment model within the AgTech ecosystem. The leading driver for cloud adoption is scalability combined with remote accessibility, allowing stakeholders to access farm intelligence from any location through centralized dashboards. Cloud deployment eliminates the need for expensive on-premise infrastructure while enabling seamless data storage, analytics processing, and software updates. Subscription-based pricing models also reduce upfront investment barriers, making advanced digital farming tools more accessible to agribusinesses and cooperatives. Cloud platforms facilitate integration between multiple agricultural technologies such as drones, sensors, machinery, and satellite imaging systems, creating unified data ecosystems. Furthermore, collaborative farming models benefit from cloud architecture by allowing advisors, agronomists, suppliers, and farmers to share insights in real time. As agricultural supply chains become increasingly digitized, cloud solutions play a critical role in enabling traceability, compliance reporting, and predictive logistics planning. The expansion of edge computing capabilities alongside cloud infrastructure further enhances performance by allowing localized data processing while maintaining centralized analytics oversight.

Farm Size: Large commercial farms represent nearly 46% share of technology adoption, primarily driven by their financial capacity and operational complexity. The leading driver in this segment is the strong return on investment achievable through large-scale technology deployment. Commercial farms manage extensive land areas where even small efficiency improvements translate into significant cost savings and yield gains. These farms often operate integrated supply chains, requiring sophisticated planning tools, automation technologies, and predictive analytics platforms. Labor shortages in many agricultural economies also encourage large farms to adopt robotics, autonomous machinery, and digital monitoring systems that reduce dependency on manual labor. Additionally, large farms serve as early adopters and testing grounds for innovative technologies, accelerating commercialization and wider market diffusion. Financial institutions and technology providers frequently prioritize large-scale farms for pilot deployments due to their ability to generate measurable performance data. As sustainability reporting becomes increasingly important for global food buyers, large farms are leveraging AgTech systems to document environmental performance metrics such as water usage, carbon emissions, and soil health indicators.

Application: Crop management applications account for approximately 34% of global demand, reflecting agriculture’s fundamental focus on productivity optimization. The leading driver behind this segment is the need to enhance crop yield consistency while reducing input waste and environmental impact. Crop management platforms combine agronomic modeling, satellite imagery, pest forecasting, nutrient analysis, and weather intelligence into integrated decision-support systems. Farmers increasingly rely on these applications to determine optimal planting schedules, irrigation timing, fertilization strategies, and harvest planning. The rising global demand for food security places pressure on producers to maximize output from limited arable land, making data-driven crop management essential. Furthermore, regulatory requirements for pesticide usage and traceability encourage adoption of digital crop monitoring tools that provide documentation and compliance tracking. Integration with drone-based imaging and AI-powered disease detection technologies is further expanding application capabilities, enabling early intervention and minimizing crop losses. As agricultural digitization progresses, crop management systems are evolving into comprehensive farm operating platforms that unify agronomic planning with financial and logistical management.

End-Use Analysis

Commercial farming enterprises remain the dominant end users within the AgTech ecosystem, contributing over 40% of global market demand. The expansion of industrial-scale agriculture has created strong demand for integrated analytics, automation platforms, and operational intelligence systems capable of managing large cultivation areas efficiently. Agribusiness companies increasingly deploy digital platforms to optimize planting cycles, monitor resource consumption, and enhance supply-chain coordination. These enterprises view AgTech not merely as a productivity tool but as a strategic investment that improves profitability, risk management, and long-term sustainability performance.Food processing companies represent a rapidly expanding end-use segment driven by increasing global emphasis on food safety, traceability, and quality assurance. Processors require transparent supply chains capable of verifying crop origin, cultivation practices, and sustainability metrics. AgTech platforms provide end-to-end visibility from farm to processing facilities, enabling compliance with international export standards and certification requirements. Digital traceability systems also reduce supply disruptions by improving forecasting accuracy and inventory management.Export-oriented agriculture plays a critical role in accelerating adoption, particularly for high-value crops such as fruits, vegetables, grains, and specialty commodities. Producers targeting international markets must meet strict quality and documentation standards, encouraging investment in digital monitoring tools and analytics platforms. Predictive yield modeling enhances export planning by enabling producers to align harvest volumes with global demand cycles, reducing price volatility risks.Agricultural cooperatives and government-backed farming initiatives are increasingly deploying shared digital infrastructure to support smallholder farmers. Cooperative-based technology adoption allows farmers to access advanced analytics and advisory services without bearing full ownership costs. Governments worldwide are integrating AgTech solutions into rural modernization programs aimed at improving productivity, climate resilience, and farmer income stability. These initiatives significantly expand technology penetration in emerging economies.The growth of controlled-environment agriculture and vertical farming further diversifies end-use opportunities. Urban agriculture systems rely heavily on automation, environmental sensors, and AI-driven optimization platforms to manage lighting, nutrients, and climate conditions. As urban populations expand and local food production gains importance, technology-driven farming environments are creating new revenue streams and accelerating innovation within the broader AgTech ecosystem.

| By Solution Type | By Deployment Model | By Farm Type | By End-Use Industry | By Technology Layer |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 36% of the global market share in 2025, maintaining its leadership position due to advanced agricultural infrastructure and high technology readiness. The United States represents the primary growth engine within the region, characterized by large farm sizes, high mechanization levels, and strong integration between agriculture and digital innovation ecosystems. Farmers in the region increasingly adopt autonomous tractors, AI-powered analytics platforms, and satellite-based monitoring systems to enhance operational efficiency.One of the strongest regional growth drivers is the availability of venture capital funding supporting AgTech startups and innovation hubs. Collaboration between technology companies, research institutions, and farming enterprises accelerates commercialization of emerging solutions. Labor shortages across agricultural sectors also encourage rapid automation adoption, including robotics and smart machinery. Additionally, data-driven crop insurance programs incentivize farmers to deploy monitoring technologies that improve risk assessment accuracy.Canada contributes to regional expansion through climate-focused agricultural programs promoting sustainable farming practices. Precision irrigation systems, carbon monitoring technologies, and climate-resilient crop analytics are gaining traction as policymakers emphasize environmental sustainability. Government incentives and digital infrastructure investments further strengthen adoption rates, ensuring continued regional dominance.

Europe

Europe holds nearly 24% market share, supported by strong regulatory frameworks promoting sustainable agriculture and environmental accountability. Countries such as Germany, France, and the Netherlands lead adoption due to technologically advanced farming systems and strong government support mechanisms. European farmers increasingly deploy precision agriculture technologies to comply with stringent environmental standards and optimize resource utilization.A key regional growth driver is the European Union’s sustainability agenda, which includes subsidies encouraging adoption of digital farming solutions that reduce fertilizer runoff, water consumption, and carbon emissions. Traceability requirements across food supply chains also accelerate investment in farm data management platforms. Carbon reduction mandates and climate-smart agriculture initiatives push farmers toward analytics-driven decision-making systems.Additionally, Europe’s strong cooperative farming structure facilitates shared technology adoption, allowing smaller farms to access advanced solutions collectively. Research collaborations between universities and AgTech companies foster continuous innovation, particularly in robotics, greenhouse automation, and regenerative agriculture practices.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market, projected to expand at a CAGR exceeding 17% during the forecast period. Rapid population growth, rising food demand, and increasing government support for agricultural modernization are central drivers of regional expansion. China leads investment through large-scale smart agriculture initiatives focused on digital monitoring, AI-powered analytics, and automated farming equipment deployment.India is experiencing significant growth driven by expanding digital advisory platforms, mobile-based farm management applications, and drone-enabled crop monitoring solutions. Government programs promoting precision farming, combined with rising smartphone penetration among farmers, are accelerating technology adoption. The need to improve productivity across fragmented landholdings further strengthens demand for affordable digital solutions.Japan and Australia contribute through advanced robotics and automation technologies designed to address labor shortages and improve operational efficiency. In Japan, aging farmer populations accelerate adoption of autonomous machinery, while Australia focuses on climate-resilient farming technologies to manage water scarcity and extreme weather variability. Increasing agritech investments across Southeast Asia further enhance regional growth prospects.

Middle East & Africa

The Middle East and Africa region is witnessing steady adoption of AgTech solutions driven primarily by food security concerns and harsh climatic conditions. Water scarcity acts as a major catalyst for smart irrigation technologies, precision water management systems, and controlled-environment agriculture. Governments across the region are prioritizing agricultural innovation to reduce reliance on food imports.Israel serves as a global innovation hub for agricultural technology, contributing advanced irrigation systems, sensor technologies, and greenhouse automation solutions. Meanwhile, the United Arab Emirates and Saudi Arabia are investing heavily in vertical farming and hydroponic systems to enable domestic food production in desert environments. Public-private partnerships and sovereign investment funds are accelerating commercialization of advanced farming technologies.In Africa, digital advisory platforms and mobile-based agricultural services are expanding access to farming intelligence for smallholder communities. International development programs supporting climate-resilient agriculture further drive technology adoption, particularly in irrigation optimization and crop monitoring solutions.

Latin America

Latin America is emerging as a significant growth region, led by Brazil and Argentina, where large-scale soybean and corn production drives demand for advanced agricultural technologies. Export-oriented farming models require yield predictability, operational efficiency, and compliance with global trade standards, encouraging adoption of analytics platforms and traceability systems.Brazil represents the fastest-growing country in the region due to rapid digitalization of agribusiness operations and increasing investment in precision agriculture tools. Large farm sizes create favorable conditions for automation and data-driven management systems. Expansion of agricultural exports to international markets further strengthens demand for technology solutions that enhance transparency and productivity.Regional growth is also supported by improving rural connectivity and rising collaboration between agricultural cooperatives and technology providers. As sustainability reporting becomes increasingly important for global commodity buyers, Latin American producers are investing in AgTech platforms to monitor environmental performance and maintain competitiveness in international markets.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Global AgTech Ecosystem Market

- Deere & Company

- Bayer AG

- Corteva Agriscience

- Trimble Inc.

- AGCO Corporation

- CNH Industrial N.V.

- Syngenta Group

- Raven Industries

- Climate LLC

- Topcon Agriculture

- Farmers Edge Inc.

- Granular Inc.

- IBM Corporation

- Microsoft Corporation

- Yara International ASA