Online Food Delivery and Takeaway Market Size

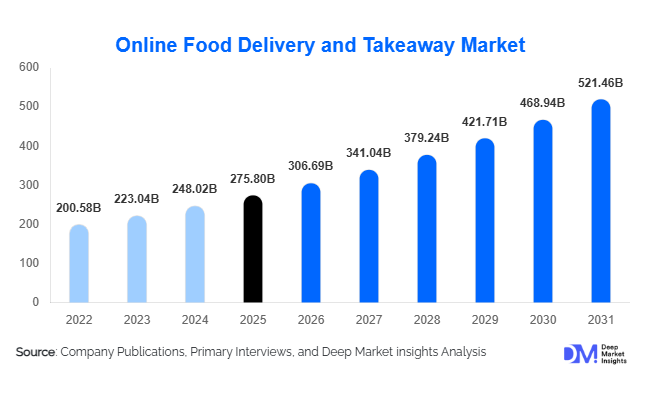

According to Deep Market Insights, the global online food delivery and takeaway market size was valued at USD 275.8 billion in 2025 and is projected to grow from USD 306.69 billion in 2026 to reach USD 521.46 billion by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). Market expansion is being driven by rapid digitalization of foodservice ecosystems, increasing smartphone penetration, evolving consumer lifestyles favoring convenience, and widespread adoption of app-based ordering platforms across both developed and emerging economies. The integration of AI-driven logistics, cloud kitchens, and real-time delivery tracking has significantly enhanced operational efficiency and consumer experience, further accelerating adoption globally.

Key Market Insights

- Convenience-led consumption behavior is reshaping global foodservice demand, with digital ordering becoming a default purchasing channel in urban markets.

- Cloud kitchens and virtual brands are expanding rapidly, enabling restaurants to scale delivery operations with lower capital expenditure.

- Asia-Pacific dominates market demand, supported by large urban populations and mobile-first consumer ecosystems.

- Subscription-based delivery models are improving customer retention and increasing order frequency worldwide.

- AI-powered logistics optimization is reducing delivery times and operational costs across platforms.

- Digital payments adoption continues to accelerate market penetration in emerging economies.

What are the latest trends in the online food delivery and takeaway market?

Rise of Cloud Kitchens and Delivery-Only Brands

Delivery-only kitchens are transforming the economics of foodservice operations. Restaurants increasingly adopt cloud kitchen models that eliminate expensive dine-in infrastructure while maximizing geographic reach through centralized production hubs. Multi-brand kitchens allow operators to serve multiple cuisines from a single facility, improving asset utilization and margins. Venture investments and franchise-based expansion models are accelerating adoption across Asia-Pacific, North America, and the Middle East. This trend also enables rapid experimentation with menus driven by customer analytics, allowing brands to respond quickly to changing consumption preferences.

AI, Automation, and Predictive Ordering

Artificial intelligence is increasingly embedded across ordering platforms. Predictive algorithms analyze consumer behavior, weather patterns, and time-of-day demand to recommend meals and optimize delivery routes. Automated dispatch systems, smart batching, and dynamic pricing models reduce idle delivery time and improve profitability. Robotics-assisted kitchens and automated packaging solutions are being piloted in high-volume urban centers, indicating a long-term shift toward tech-enabled food fulfillment ecosystems.

What are the key drivers in the online food delivery and takeaway market?

Urbanization and Changing Consumer Lifestyles

Rapid urbanization and longer working hours are driving demand for convenient meal solutions. Dual-income households and younger consumers increasingly prioritize time efficiency, leading to higher reliance on ready-to-eat meals delivered through mobile applications. Urban density also improves delivery economics by reducing last-mile costs and increasing order clustering efficiency.

Expansion of Digital Payment Infrastructure

The widespread adoption of digital wallets and real-time payment systems has removed friction from online ordering. Seamless checkout experiences encourage impulse purchases and higher order frequency. Emerging markets such as India, Indonesia, and Brazil are witnessing exponential growth due to government-backed fintech ecosystems and mobile-first banking adoption.

Restaurant Digitization and Omnichannel Strategy

Restaurants increasingly view delivery as a core revenue stream rather than a supplementary channel. Integration of POS systems, inventory analytics, and customer relationship tools allows restaurants to manage online demand efficiently. Hybrid dine-in and delivery strategies are strengthening revenue diversification and improving resilience against economic fluctuations.

What are the restraints for the global market?

Thin Profit Margins and High Logistics Costs

Despite strong demand growth, profitability remains a challenge due to delivery logistics expenses, promotional discounts, and platform commissions. Fuel costs, labor wages, and fleet management expenses continue to pressure margins, particularly in competitive urban markets.

Regulatory and Labor Compliance Challenges

Governments worldwide are introducing gig-worker regulations and food safety compliance standards. Classification of delivery riders as employees rather than contractors could increase operating costs for platforms. Additionally, data privacy laws and taxation policies create operational complexities for multinational delivery providers.

What are the key opportunities in the online food delivery and takeaway industry?

Expansion into Tier-II and Tier-III Cities

Untapped demand in smaller cities represents one of the largest growth opportunities. Rising disposable income, improved internet connectivity, and expanding logistics networks are enabling platforms to penetrate beyond metropolitan areas. Localization strategies, regional cuisine offerings, and lower delivery costs make these markets highly scalable.

Integration with Quick Commerce and Grocery Delivery

Platforms are diversifying into rapid grocery delivery and meal kits, leveraging existing logistics infrastructure. This convergence allows higher order density and improves delivery fleet utilization. Cross-category bundling is increasing average order value while strengthening customer loyalty ecosystems.

AI-Driven Personalization and Subscription Ecosystems

Subscription models offering free delivery and exclusive discounts are improving retention rates. Personalized recommendations driven by consumer data analytics enhance conversion rates and repeat purchases. Platforms investing in loyalty ecosystems are achieving stronger lifetime customer value.

Service Model Insights

The platform-to-consumer delivery model continues to dominate the global online food delivery ecosystem, accounting for approximately 58% of total global revenue in 2025. The leadership of this segment is primarily driven by the scalability and convenience offered by aggregated digital marketplaces that integrate multiple restaurants, payment gateways, and logistics systems within a single application environment. Consumers increasingly prefer unified platforms that enable price comparison, personalized recommendations powered by artificial intelligence, loyalty integrations, and real-time delivery tracking. The expansion of super-app ecosystems, subscription-based delivery programs, and algorithm-driven logistics optimization further strengthens platform-based delivery adoption across both developed and emerging economies. Additionally, aggressive promotional campaigns, bundled discounts, and dynamic pricing models enhance customer acquisition and retention, reinforcing this segment’s dominance.Restaurant-to-consumer delivery models maintain strong adoption, particularly among large quick-service restaurant (QSR) chains and premium food brands that operate proprietary mobile applications. These companies leverage direct ordering channels to maintain ownership of customer data, enhance brand loyalty, and minimize third-party commission expenses. The increasing emphasis on customer relationship management, personalized marketing, and subscription meal offerings has accelerated investments in in-house ordering ecosystems. Moreover, advancements in last-mile delivery software and route optimization technologies allow restaurants to operate efficient proprietary logistics networks.Hybrid fulfillment models are emerging as a strategic evolution within the market as restaurants increasingly combine third-party logistics providers with internal delivery fleets. This flexible approach allows businesses to manage peak demand efficiently while maintaining cost control during off-peak periods. Hybrid strategies are particularly beneficial in densely populated urban areas where delivery volumes fluctuate significantly throughout the day. The model also supports geographic expansion without heavy capital investment, enabling restaurants to balance operational efficiency with service quality.

Business Model Insights

Aggregator platforms lead the business model landscape, capturing nearly 46% of market share in 2025. The leading position of aggregators is supported by strong network effects, where increasing restaurant participation attracts more consumers, and higher consumer traffic incentivizes additional restaurant onboarding. Advanced analytics capabilities, targeted advertising solutions for restaurants, and integrated logistics infrastructure further enhance platform competitiveness. Aggregators also benefit from diversified revenue streams including delivery fees, commission structures, advertising placements, and subscription memberships, allowing sustained profitability despite competitive pricing pressures.Cloud kitchen operators represent the fastest-growing business model segment, driven by the industry’s shift toward asset-light expansion strategies. The leading growth driver for this segment is the ability to operate delivery-only kitchens without expensive dine-in infrastructure, significantly reducing capital expenditure and enabling rapid geographic scaling. Data-driven menu optimization, shared kitchen facilities, and demand forecasting technologies allow operators to maximize kitchen utilization and respond quickly to changing consumer preferences. Venture capital investment and partnerships with delivery platforms continue accelerating the global proliferation of cloud kitchens.Direct restaurant ordering platforms are gaining momentum among premium and established food brands seeking higher margins and stronger control over customer engagement. These platforms allow restaurants to bypass intermediary commissions while building long-term consumer relationships through loyalty programs, customized promotions, and subscription meal plans. Increasing digital transformation across the restaurant industry and the integration of omnichannel ordering systems are expected to further expand this segment.

Order Type Insights

Meal delivery orders remain the leading segment, accounting for approximately 64% of global transactions. The primary driver behind this dominance is the growing consumer preference for complete ready-to-eat meals that eliminate cooking time and support busy urban lifestyles. Rising dual-income households, extended working hours, and increasing reliance on convenience-driven consumption patterns continue to strengthen demand. Restaurants are also expanding menu diversity, including healthy meals, international cuisines, and dietary-specific offerings, further supporting segment leadership.Quick snacks and beverage orders are witnessing rapid expansion, fueled by changing consumption habits among younger demographics and the rise of late-night ordering culture. The proliferation of convenience-focused delivery options, including desserts, coffee, and quick-service snack brands, is increasing order frequency throughout the day. Integration with quick-commerce logistics and reduced delivery times enhances impulse purchasing behavior, accelerating growth in this category.Catering and group ordering segments are experiencing renewed growth following the normalization of workplace activity and hybrid office environments. Organizations increasingly utilize digital platforms for scheduled meal deliveries, corporate events, and team gatherings. Enhanced bulk-order management tools and subscription catering solutions enable seamless coordination for large-volume orders, strengthening long-term growth prospects.

Payment Method Insights

Digital payments accounted for nearly 72% of global transactions in 2025, making them the dominant payment method across online food delivery platforms. The leading driver for this segment is the rapid adoption of mobile wallets, unified payment interfaces, and contactless transaction technologies that provide speed, security, and convenience. Governments and financial institutions across multiple regions are promoting cashless ecosystems, while fintech integration enables instant refunds, subscription billing, and reward-based payment incentives. The expansion of embedded finance solutions within delivery applications further streamlines the consumer checkout experience.Cash-on-delivery transactions continue to decline globally as digital banking penetration expands; however, they remain relevant in certain emerging economies where trust in online payments is still evolving. In these markets, hybrid payment options help platforms onboard first-time digital consumers, gradually transitioning them toward electronic payment adoption.

End-Use Insights

Individual consumers represent the largest end-use segment, contributing nearly 78% of total orders. The leading driver of this segment is the widespread shift toward convenience-oriented consumption supported by urban lifestyles, increased smartphone usage, and the growing preference for on-demand services. Personalized recommendations, loyalty rewards, and subscription-based delivery memberships further increase ordering frequency among individual users. The integration of health-focused menus, customizable meal options, and dietary tracking features also enhances consumer engagement.Corporate and institutional ordering is emerging as the fastest-growing end-use category as organizations increasingly outsource employee meal programs and catering operations to digital platforms. Businesses adopt centralized ordering solutions to improve employee convenience, manage food budgets efficiently, and support hybrid work environments. Scheduled delivery systems and bulk ordering capabilities are strengthening adoption across technology companies, co-working spaces, and educational institutions.Hospitality partnerships, including hotels and co-working operators, are becoming important demand contributors by integrating delivery platforms into guest and tenant service offerings. Additionally, global expansion of international restaurant brands indirectly drives export-oriented demand, as delivery platforms enable rapid cross-border brand scaling without traditional physical expansion constraints.

| By Service Model | By Order Type | By Business Model | By Payment Mode | By End User |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific held approximately 41% of global market share in 2025, making it the largest regional market for online food delivery services. Regional growth is primarily driven by dense urban populations, widespread smartphone penetration, and the dominance of super-app ecosystems that integrate food delivery with payments, mobility, and e-commerce services. China remains the largest single-country market due to advanced logistics infrastructure, high digital payment adoption, and strong consumer reliance on app-based daily services. India represents the fastest-growing major market, expanding at over 15% annually, supported by increasing internet accessibility, rising middle-class income levels, and government initiatives promoting digital payments. Southeast Asian economies benefit from youthful demographics, rapid urbanization, and expanding gig-economy workforces, which collectively strengthen delivery network scalability and market penetration.

North America

North America accounted for nearly 24% of global revenue, driven primarily by the United States and Canada. Regional growth is supported by high disposable incomes, advanced digital infrastructure, and strong consumer familiarity with subscription-based service models. The widespread adoption of delivery memberships significantly increases order frequency and customer retention rates. Additionally, deep integration between QSR chains and delivery platforms, coupled with technological innovations such as AI-driven demand forecasting and automated fulfillment systems, enhances operational efficiency. Increasing demand for premium dining delivery, health-conscious meal options, and convenience-focused lifestyles further reinforces market expansion.

Europe

Europe demonstrates steady and sustainable growth led by the United Kingdom, Germany, and France. Regional expansion is driven by increasing demand for premium restaurant delivery experiences and heightened consumer awareness regarding sustainability practices. The adoption of eco-friendly packaging solutions, electric delivery fleets, and carbon-neutral logistics initiatives supports long-term industry development. Regulatory frameworks emphasizing gig-worker protections and labor standardization are reshaping operational models, encouraging platforms to invest in workforce stability, service quality improvements, and transparent pricing structures. Urban densification and strong restaurant digitization across Western Europe continue to support market maturity.

Middle East & Africa

The Middle East & Africa region is witnessing accelerating adoption, led by the United Arab Emirates and Saudi Arabia. Regional growth drivers include high smartphone penetration, strong consumer spending on foodservice, and digitally connected urban populations. Government-led smart city initiatives and investments in logistics infrastructure enhance delivery efficiency across major metropolitan areas. In Africa, markets such as South Africa and Nigeria are gradually expanding as fintech ecosystems mature and mobile payment adoption increases. Rising urban middle-class populations and improving internet connectivity are expected to unlock long-term growth opportunities across the continent.

Latin America

Latin America is experiencing strong growth momentum, with Brazil and Mexico dominating regional demand. Market expansion is driven by rapid urban population growth, increasing workforce participation among younger consumers, and strong adoption of mobile-first digital services. Investments in localized logistics networks, dark stores, and last-mile delivery optimization are improving service reliability across major cities. Additionally, partnerships between delivery platforms and local restaurants are expanding cuisine diversity and improving platform penetration. Economic digitization initiatives and expanding fintech adoption continue to accelerate the transition toward app-based food ordering throughout the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Online Food Delivery and Takeaway Market

- DoorDash Inc.

- Uber Technologies Inc.

- Meituan

- Delivery Hero SE

- Just Eat Takeaway.com N.V.

- Prosus N.V.

- Domino’s Pizza Inc.

- Yum! Brands Inc.

- McDonald’s Corporation

- Restaurant Brands International Inc.

- Starbucks Corporation

- Chipotle Mexican Grill Inc.

- Wingstop Inc.

- Papa John’s International Inc.

- Shake Shack Inc.