Dry Champagne Market Size

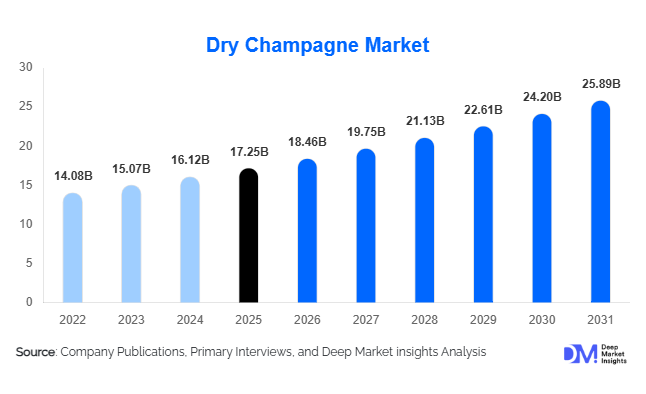

According to Deep Market Insights, the global dry champagne market size was valued at USD 17.25 billion in 2025 and is projected to grow from USD 18.46 billion in 2026 to reach USD 25.89 billion by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The dry champagne market growth is primarily driven by increasing premiumization across alcoholic beverages, rising demand for luxury experiences, expanding hospitality and tourism industries, and growing consumer preference for lower-sugar sparkling wines. Dry champagne varieties, including Brut Nature, Extra Brut, Brut, and Extra Dry, continue to dominate global champagne consumption due to their versatility, sophisticated flavor profile, and strong alignment with health-conscious drinking trends.

Key Market Insights

- Brut champagne remains the dominant category, accounting for approximately 68% of global dry champagne sales due to its broad consumer appeal and compatibility with food pairings.

- Europe leads global consumption and production, representing nearly 49% of market demand, supported by France's dominance in champagne production and established consumption habits across major European economies.

- The United States remains the largest single-country importer, contributing approximately 23% of global dry champagne demand through premium retail, hospitality, and gifting channels.

- Asia-Pacific is the fastest-growing regional market, driven by increasing disposable incomes, luxury consumption, and premium hospitality expansion across China, India, South Korea, and Southeast Asia.

- Sustainability initiatives are becoming critical competitive differentiators, with producers investing in organic viticulture, regenerative farming, lightweight packaging, and carbon-neutral operations.

- E-commerce and direct-to-consumer sales channels are transforming distribution, allowing premium producers to strengthen customer engagement while improving margins and brand visibility.

Dry Champagne Market Latest Trends

Premiumization Driving Category Expansion

The global dry champagne market continues to benefit from premiumization trends across the alcoholic beverage industry. Consumers are increasingly prioritizing quality, authenticity, and heritage over volume consumption, leading to stronger demand for premium and luxury champagne products. Prestige cuvées, limited-edition releases, vintage offerings, and grower champagnes are experiencing particularly strong growth among affluent consumers. Luxury hospitality establishments, fine dining restaurants, destination wedding venues, and premium event organizers are increasingly incorporating premium dry champagne into their beverage portfolios. This trend has allowed producers to maintain pricing power despite economic volatility while expanding profit margins through high-value product offerings.

Growing Demand for Sustainable and Low-Dosage Champagne

Consumer preferences are increasingly shifting toward environmentally responsible products and lower-sugar alcoholic beverages. Dry champagne styles such as Brut Nature and Extra Brut are benefiting from growing health-conscious consumption trends. Simultaneously, producers are investing heavily in sustainable vineyard management, organic certification programs, renewable energy adoption, and biodiversity preservation initiatives. Sustainability has evolved from a marketing attribute into a core purchasing consideration, particularly among younger consumers and premium buyers. Champagne houses are also introducing eco-friendly packaging formats, lightweight glass bottles, and transparent sourcing practices to strengthen brand loyalty and meet evolving consumer expectations.

Dry Champagne Market Drivers

Rising Global Premium Alcohol Consumption

The increasing consumer preference for premium alcoholic beverages remains one of the most significant drivers of dry champagne market growth. Affluent consumers are demonstrating a willingness to spend more on premium products that offer superior quality, heritage, and exclusivity. Champagne benefits from its strong luxury positioning and cultural association with celebration, achievement, and prestige. Premiumization trends are particularly evident in North America, Europe, China, Japan, and the Middle East, where consumers increasingly view champagne as a lifestyle product rather than simply an alcoholic beverage. The growing popularity of luxury gifting and corporate hospitality further supports premium dry champagne demand.

Expansion of Hospitality, Tourism, and Luxury Events

Global tourism recovery and rising investments in luxury hospitality continue to create substantial demand for dry champagne. Hotels, resorts, fine dining restaurants, cruise operators, airlines, and event management companies increasingly incorporate premium champagne into their service offerings. Destination weddings, corporate events, luxury travel experiences, and international tourism activities have become important demand drivers. Markets such as the UAE, Singapore, the United States, and Mediterranean tourism destinations have experienced particularly strong growth in premium champagne consumption through hospitality channels.

Consumer Shift Toward Lower-Sugar Alcoholic Beverages

Health-conscious consumers are increasingly favoring beverages with lower sugar content. Dry champagne categories, especially Brut Nature and Extra Brut, align closely with this trend by offering sophisticated flavor profiles while maintaining relatively low residual sugar levels. Younger consumers are demonstrating growing interest in products that balance indulgence with wellness considerations, creating favorable conditions for long-term dry champagne market expansion.

Dry Champagne Market Restraints

Climate Change and Vineyard Production Risks

The dry champagne market remains highly dependent on grape production within the Champagne region of France. Climate-related challenges, including frost events, drought conditions, excessive rainfall, and temperature variability, can significantly affect grape yields and quality. These factors create supply uncertainties and contribute to production cost volatility. As climate risks intensify, producers may face increasing pressure to invest in adaptive vineyard management strategies while maintaining strict appellation standards.

High Product Pricing and Economic Sensitivity

Dry champagne remains a premium discretionary product, making it vulnerable to economic slowdowns and fluctuations in consumer confidence. Inflationary pressures, rising living costs, and periods of reduced discretionary spending can negatively impact premium alcohol purchases. While affluent consumers provide some demand stability, broader market expansion may be constrained during periods of economic uncertainty, particularly in emerging markets where luxury consumption remains highly sensitive to macroeconomic conditions.

Dry Champagne Industry Key Opportunities

Expansion Across Emerging Luxury Markets

Asia-Pacific presents one of the most attractive growth opportunities for dry champagne producers. Rising affluent populations in China, India, Vietnam, Indonesia, and Thailand are creating substantial demand for imported luxury beverages. Urbanization, growing exposure to international lifestyles, expanding premium retail networks, and increasing luxury tourism are driving champagne adoption among new consumer segments. Producers that establish strong brand awareness and localized distribution strategies in these markets are likely to secure significant long-term growth opportunities.

Sustainability-Led Product Differentiation

Sustainability represents a major opportunity for both established producers and emerging market participants. Consumers increasingly seek products aligned with environmental responsibility, ethical sourcing, and transparent production practices. Investments in organic viticulture, carbon-neutral production facilities, regenerative agriculture, and sustainable packaging can strengthen competitive positioning while supporting premium pricing strategies. Sustainability certifications are becoming particularly influential among younger consumers and premium hospitality buyers, creating opportunities for producers to enhance both brand equity and profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.25 Billion |

| Market Size in 2026 | USD 18.46 Billion |

| Market Size in 2031 | USD 25.89 Billion |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Sweetness Category Insights

Brut champagne remains the dominant sweetness category in the global dry champagne market, accounting for approximately 68% of total market revenue in 2025. Its leadership is supported by strong consumer preference for balanced dryness, versatility across food pairings, and widespread acceptance in both mature and emerging champagne-consuming markets. Brut varieties are extensively featured across fine dining establishments, luxury hospitality venues, corporate events, and celebratory occasions, reinforcing their position as the preferred choice among both retail consumers and commercial buyers. The segment further benefits from growing consumer awareness regarding lower sugar consumption, as Brut champagnes typically contain lower residual sugar levels than sweeter sparkling wine alternatives. Rising participation in wine education programs, sommelier-led tasting experiences, and premium dining culture continues to strengthen demand for Brut products globally.Extra Brut and Brut Nature categories are witnessing accelerated growth as health-conscious consumers increasingly seek ultra-low-dosage and lower-calorie alcoholic beverages. The growing influence of wellness-focused consumption patterns, clean-label preferences, and demand for authentic winemaking styles is encouraging producers to expand their offerings within these premium dry segments. Meanwhile, Extra Dry champagne continues to maintain stable demand among consumers seeking a slightly softer and fruit-forward taste profile while remaining within the broader dry champagne category. Ongoing product innovation, premiumization strategies, and the expansion of luxury sparkling wine consumption are expected to support growth across all sweetness categories throughout the forecast period, with Brut continuing to represent the largest and most commercially significant segment.

Product Type Insights

Non-vintage dry champagne represents approximately 72% of global market demand, making it the largest product type segment. The segment benefits from consistent quality, year-round availability, greater production scalability, and comparatively accessible pricing relative to vintage offerings. Non-vintage champagnes serve as the foundation of many leading champagne houses’ portfolios and are widely distributed across retail stores, hospitality venues, restaurants, bars, and e-commerce platforms. Their broad consumer appeal and suitability for everyday celebrations, gifting occasions, and hospitality service continue to drive strong market penetration across developed and emerging economies.The primary driver supporting the dominance of the non-vintage segment is its ability to deliver a consistent taste profile and premium brand experience at a more affordable price point than vintage alternatives. Consumers increasingly seek premium yet accessible luxury beverages, making non-vintage products the preferred choice for both first-time champagne buyers and regular consumers. In addition, growing demand from hotels, restaurants, event venues, and airline hospitality programs further reinforces the segment’s leadership position.Vintage champagne continues to attract affluent consumers seeking exclusivity, exceptional quality, and unique harvest characteristics. These products often command premium pricing due to limited production volumes and the use of grapes sourced from exceptional growing seasons. Prestige cuvées represent the highest-value category within the market, benefiting from luxury branding, collector interest, and strong demand among high-net-worth consumers. At the same time, grower champagnes are gaining popularity among wine enthusiasts who value terroir expression, artisanal production techniques, authenticity, and vineyard-specific characteristics. Increasing consumer interest in provenance, craftsmanship, and boutique luxury products is expected to support continued growth across these premium categories.

Distribution Channel Insights

Off-trade channels account for approximately 55% of global dry champagne sales and remain the largest distribution segment. The category benefits from widespread availability through supermarkets, hypermarkets, specialty wine retailers, liquor stores, duty-free outlets, and online retail platforms. Consumers increasingly prefer purchasing champagne through off-trade channels due to greater product accessibility, competitive pricing, wider product selection, and convenience. The growing penetration of premium alcoholic beverages into organized retail networks has further strengthened sales volumes across this segment.The leading driver behind the dominance of the off-trade segment is the rapid expansion of e-commerce and direct-to-consumer wine sales, which provide consumers with enhanced convenience, product discovery opportunities, personalized recommendations, and access to premium and limited-edition labels. Digital transformation within the alcoholic beverage industry, coupled with rising smartphone adoption and online purchasing behavior, continues to accelerate growth across online sales channels.On-trade channels remain strategically important for brand building, premium positioning, and consumer engagement. Hotels, restaurants, bars, clubs, lounges, luxury resorts, and event venues serve as critical consumption points for premium and prestige champagne products. The recovery and expansion of global tourism, luxury hospitality investments, and experiential dining trends continue to support demand across on-trade establishments. Furthermore, premium champagne consumption during weddings, corporate events, social gatherings, and luxury entertainment experiences remains a key contributor to long-term channel growth.

End-Use Insights

Individual consumers account for approximately 62% of global dry champagne demand, making this the largest end-use segment. Household consumption continues to increase as consumers incorporate premium alcoholic beverages into celebrations, gifting occasions, festive gatherings, anniversaries, and personal milestones. The growing accessibility of premium champagne through retail and online channels has further expanded consumer adoption across a broader demographic base. Rising disposable incomes, increasing interest in luxury lifestyle experiences, and growing appreciation for premium sparkling wines continue to support segment expansion globally.The primary driver supporting the leadership of the individual consumer segment is the increasing trend toward premium at-home consumption and celebratory purchasing behavior. Consumers are increasingly willing to spend on premium alcoholic beverages to enhance personal experiences, social occasions, and gifting activities, creating sustained demand across both established and emerging markets.Commercial end-use sectors, including hotels, restaurants, bars, luxury resorts, airlines, cruise operators, and event management companies, represent one of the fastest-growing areas of demand. Premium champagne is increasingly utilized as a value-added offering to enhance customer experiences and reinforce luxury positioning. Growth in destination weddings, corporate hospitality programs, luxury tourism, international travel, and high-end entertainment events continues to generate incremental demand, particularly for premium vintage and prestige cuvée products.

Explore more data points, trends and opportunities Download Free Sample Report

Dry Champagne Market Segmentations

By Sweetness Category

- Brut Nature

- Extra Brut

- Brut

- Extra Dry

By Product Type

- Non-Vintage Dry Champagne

- Vintage Dry Champagne

- Prestige Cuvée Dry Champagne

- Grower Dry Champagne

By Color

- Blanc de Blancs

- Blanc de Noirs

- Traditional White Blend

- Rosé Dry Champagne

By Price Tier

- Entry-Level Premium

- Mid-Premium

- Super Premium

- Luxury

- Ultra-Luxury / Prestige

By Packaging Format

- Half Bottles (375 ml)

- Standard Bottles (750 ml)

- Magnum Bottles (1.5 L)

- Large Format Bottles

- Single-Serve & Mini Bottles

Regional Insights

North America

North America accounts for approximately 27% of global dry champagne demand, making it the second-largest regional market. The United States represents the world's largest individual import market for champagne and continues to drive the majority of regional consumption. Strong premiumization trends, a well-established luxury gifting culture, rising disposable incomes, and expanding demand for premium alcoholic beverages support market growth across both retail and hospitality channels. Champagne consumption has become increasingly associated with lifestyle-driven celebrations, corporate events, social gatherings, and luxury entertainment experiences. Canada also demonstrates strong per-capita consumption levels, supported by growing consumer appreciation for premium sparkling wines and high-end imported alcoholic beverages.Regional growth is primarily driven by increasing consumer willingness to spend on luxury experiences, expanding premium beverage portfolios across retail outlets, growing e-commerce penetration, and sustained investments in luxury hospitality, tourism, and fine dining sectors. The increasing popularity of experiential consumption and premium gifting occasions continues to create favorable market conditions throughout North America.

Europe

Europe remains the largest regional market, accounting for approximately 49% of global dry champagne consumption in 2025. France dominates both production and domestic consumption, while the United Kingdom, Germany, Italy, and Spain collectively contribute substantial demand across the region. Champagne enjoys deep cultural integration throughout Europe, supported by longstanding consumption traditions, mature distribution networks, extensive tourism activity, and widespread consumer familiarity with premium sparkling wines. The region also benefits from a strong concentration of leading champagne producers, advanced vineyard management practices, and established export infrastructure.Regional growth is supported by strong cultural acceptance of champagne, continuous premiumization across alcoholic beverage categories, rising demand for sustainable and organic production practices, and ongoing investments in vineyard modernization and production efficiency. In addition, Europe's thriving tourism sector, luxury hospitality industry, and growing demand for premium dining experiences continue to sustain long-term market stability and value growth.

Asia-Pacific

Asia-Pacific accounts for approximately 15% of global dry champagne demand and is projected to be the fastest-growing regional market throughout the forecast period. China remains the largest consumer market within the region, supported by rising luxury spending, increasing wealth accumulation, expanding middle-class populations, and strong corporate gifting demand. Japan continues to represent a mature premium market characterized by sophisticated consumer preferences and strong appreciation for high-quality champagne products. India is emerging as one of the most attractive growth opportunities due to increasing disposable incomes, rapid urbanization, expanding affluent consumer groups, and significant investments in luxury hospitality infrastructure. Australia and South Korea further contribute to regional demand through growing premium wine consumption and evolving lifestyle preferences.The primary drivers of regional growth include rising disposable incomes, expanding luxury consumer populations, increasing westernization of consumption habits, growth in premium retail networks, and rapid development of luxury hospitality and tourism sectors. Growing exposure to international wine culture, higher spending on experiential luxury products, and increasing demand for premium gifting and celebration beverages are expected to significantly accelerate market expansion across the region.

Latin America

Latin America accounts for approximately 4% of global dry champagne demand, with Brazil, Mexico, and Argentina representing the largest consumption markets. The region is witnessing gradual expansion in premium alcoholic beverage consumption as economic development improves purchasing power among affluent and upper-middle-income consumers. Luxury retail infrastructure, premium hospitality establishments, and high-end dining venues are increasingly introducing imported champagne offerings to meet evolving consumer preferences. Although champagne consumption remains concentrated among affluent consumers, awareness and accessibility continue to improve across key metropolitan markets.Regional growth is being driven by increasing urbanization, rising disposable incomes among high-income households, expanding luxury retail and hospitality sectors, growing international tourism, and greater consumer exposure to premium imported beverages. The continued development of luxury lifestyle markets is expected to create substantial long-term growth opportunities throughout the region.

Middle East & Africa

The Middle East and Africa region contributes approximately 5% of global dry champagne demand. The United Arab Emirates remains the largest market within the region, benefiting from strong luxury tourism activity, high-income consumer demographics, and significant investments in premium hospitality infrastructure. Saudi Arabia is emerging as an increasingly important market as tourism diversification initiatives and large-scale hospitality developments create new opportunities for premium beverage consumption. South Africa serves as a key regional consumption hub, supported by tourism activity, luxury retail expansion, and growing demand for premium imported alcoholic beverages.Regional growth is primarily driven by rapid expansion of luxury tourism, increasing investments in premium hotels and resorts, rising concentrations of affluent consumers, and large-scale hospitality and entertainment developments. Government-led tourism diversification programs, particularly across Gulf countries, coupled with growing demand for luxury lifestyle experiences, continue to create favorable conditions for premium champagne consumption throughout the Middle East and Africa.

Key Players in the Dry Champagne Market

- LVMH Moët Hennessy Louis Vuitton

- Laurent-Perrier Group

- Vranken-Pommery Monopole

- Nicolas Feuillatte

- Taittinger

- Bollinger

- Louis Roederer

- Piper-Heidsieck

- Lanson-BCC

- Pol Roger

- Charles Heidsieck

- Deutz

- Duval-Leroy

- Gosset

- Palmer & Co