Distilling Wine Market Size

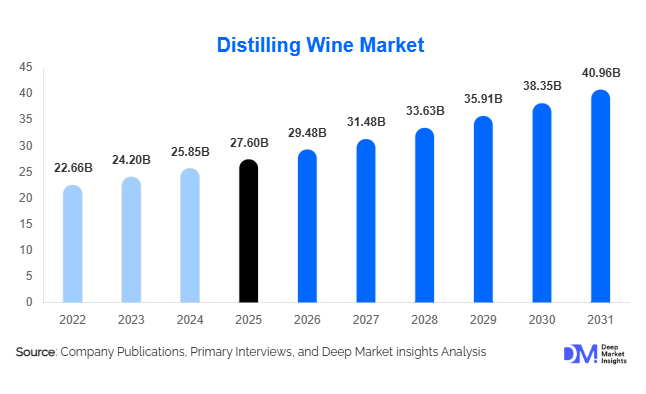

According to Deep Market Insights, the global distilling wine market size was valued at USD 27.6 billion in 2025 and is projected to grow from USD 29.48 billion in 2026 to reach USD 40.96 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The distilling wine market growth is primarily driven by rising premiumization across the global spirits industry, increasing consumer preference for aged and craft-produced brandies, expanding demand from emerging economies, and the growing popularity of luxury alcoholic beverages among affluent consumers. Wine-distilled spirits, including cognac, armagnac, grape brandy, and fruit brandy, continue to benefit from strong export demand and evolving consumption patterns that favor quality over volume.

Key Market Insights

- Premium and super-premium brandies are outpacing mainstream products, supported by consumer willingness to pay higher prices for aged spirits with authentic provenance and superior craftsmanship.

- Asia-Pacific is emerging as the fastest-growing consumption hub, driven by rising disposable incomes, urbanization, and increasing adoption of western drinking habits across China, India, Vietnam, and Southeast Asia.

- Europe remains the largest production and export center, led by France, Spain, and Italy, which collectively account for a significant share of global distilling wine exports.

- E-commerce and direct-to-consumer alcohol sales are reshaping distribution channels, enabling premium producers to reach consumers more efficiently and improve brand engagement.

- Craft distillation and small-batch production are gaining popularity, particularly among younger consumers seeking authenticity, exclusivity, and differentiated flavor profiles.

- Sustainability initiatives are increasingly influencing purchasing decisions, prompting producers to invest in renewable energy, recyclable packaging, water conservation, and vineyard sustainability programs.

Distilling Wine Market Latest Trends

Premiumization and Luxury Spirit Consumption Accelerating

The most significant trend shaping the distilling wine market is the rapid premiumization of alcoholic beverage consumption. Consumers are increasingly trading up from standard spirits to premium, super-premium, and luxury brandies. Aged products such as XO, Hors d'Age, and vintage brandies are witnessing robust demand growth, particularly among affluent consumers in North America, Europe, China, Japan, and the Gulf countries. Producers are responding by launching limited-edition releases, single-estate offerings, and collectible bottlings that command significantly higher margins. Luxury gifting trends, rising wealth accumulation, and growing interest in investment-grade spirits are further supporting demand for premium wine-distilled products.

Innovation Through Craft Distillation and Flavor Diversification

Distillers are increasingly focusing on innovation through small-batch production, fruit-based brandies, botanical infusions, and barrel-finishing techniques. Younger legal-age consumers are demonstrating greater openness to flavored and experimental spirits, encouraging manufacturers to diversify product portfolios. Craft distilleries are gaining market share by emphasizing local sourcing, artisanal production methods, and transparency throughout the production process. Additionally, ready-to-drink (RTD) cocktails incorporating premium brandy are emerging as a high-growth category, creating new consumption occasions beyond traditional neat or after-dinner drinking experiences.

Distilling Wine Market Drivers

Growing Global Demand for Premium Alcoholic Beverages

Premiumization remains one of the strongest growth drivers across the global spirits industry. Consumers increasingly prioritize quality, heritage, authenticity, and aging characteristics when selecting alcoholic beverages. Distilling wine products such as cognac, aged brandies, and premium fruit brandies align closely with these preferences. The growing population of affluent consumers, particularly in emerging economies, is accelerating demand for premium spirits. Luxury hotels, fine-dining establishments, and upscale retail channels are also expanding their premium brandy portfolios to cater to changing consumer expectations.

Expansion of Cocktail Culture and Modern Mixology

The increasing popularity of cocktail culture has significantly expanded the consumer base for wine-distilled spirits. Bartenders and mixologists are incorporating brandy into contemporary cocktail menus, helping reposition the category among younger consumers. Premium cocktail bars, luxury restaurants, and hospitality establishments are introducing innovative brandy-based beverages that appeal to consumers seeking unique drinking experiences. This trend is broadening brandy consumption beyond traditional demographics and creating new opportunities for product innovation and market expansion.

Strong Export Demand and International Trade Growth

International trade remains a major growth catalyst for the distilling wine market. France, Spain, Italy, South Africa, and several Eastern European countries continue to export substantial volumes of wine-distilled spirits to North America, Asia-Pacific, and Latin America. Export-oriented growth has enabled producers to diversify revenue streams and reduce dependence on domestic markets. Rising demand from China, India, Vietnam, and Southeast Asia is particularly supporting global trade flows and production expansion.

Distilling Wine Market Restraints

Regulatory Complexity and Taxation Challenges

The alcoholic beverage industry remains heavily regulated across most countries. Excise duties, import tariffs, advertising restrictions, health labeling requirements, and distribution regulations create significant compliance costs for producers. Frequent policy changes can impact pricing structures, profitability, and market accessibility, particularly for smaller producers seeking international expansion.

Intensifying Competition from Alternative Spirits

The distilling wine market faces increasing competition from whiskey, tequila, rum, gin, and ready-to-drink alcoholic beverages. Many younger consumers are experimenting with diverse spirit categories, intensifying competition for market share. Premium tequila and whiskey segments have particularly attracted consumer attention in recent years, creating pressure for brandy producers to innovate and differentiate their offerings.

Distilling Wine Industry Key Opportunities

Premium Product Expansion Across Emerging Markets

Emerging economies present significant opportunities for premium and super-premium brandy manufacturers. Rising disposable incomes, urbanization, and expanding middle-class populations are increasing demand for luxury alcoholic beverages. China, India, Vietnam, Indonesia, and the Philippines are expected to contribute a substantial portion of incremental market growth during the forecast period. Companies that establish strong premium positioning and localized marketing strategies are likely to capture significant market share.

Growth of Ready-to-Drink and Cocktail-Based Offerings

The expanding ready-to-drink alcoholic beverage segment creates opportunities for distilling wine producers to diversify their portfolios. Brandy-based canned cocktails, premium mixed beverages, and convenient consumption formats appeal to younger consumers seeking accessibility and convenience. This category enables producers to reach new customer segments while creating additional consumption occasions beyond traditional spirits drinking.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 27.60 Billion |

| Market Size in 2026 | USD 29.48 Billion |

| Market Size in 2031 | USD 40.96 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The grape-based distilled spirits segment remains the leading product category in the global distilling wine market, accounting for approximately 52% of total market value. Its dominance is primarily attributed to the strong global reputation of cognac, armagnac, and premium grape brandies, which benefit from established heritage, protected geographical indications, extensive international distribution networks, and strong consumer trust. The segment continues to gain momentum from increasing premiumization trends, rising demand for aged spirits, and growing consumer preference for authentic products with historical provenance. Premium grape-based offerings also benefit from their strong positioning within luxury gifting, fine dining, and collectible spirits categories, enabling manufacturers to maintain higher profit margins and sustained revenue growth.Fruit-based distilled spirits, including apple, plum, pear, cherry, and other specialty fruit brandies, continue to witness healthy expansion as consumers increasingly seek diversified flavor profiles and regionally distinctive alcoholic beverages. Growing interest in craft spirits and local production traditions has strengthened demand for fruit-based alternatives across both mature and emerging markets. In addition, innovation in flavor development, premium packaging, and artisanal production techniques is enhancing consumer appeal across younger demographic groups.The specialty segment, encompassing organic brandy, craft-distilled wine spirits, small-batch products, and limited-edition releases, is emerging as one of the fastest-growing categories within the market. Growth is being driven by increasing consumer emphasis on sustainability, transparency, traceability, and artisanal craftsmanship. Consumers are increasingly willing to pay premium prices for products perceived as authentic, environmentally responsible, and locally sourced. Furthermore, premium aged variants continue to outperform standard offerings in terms of revenue growth, reflecting a broader global shift toward higher-value alcoholic beverages and luxury consumption experiences.

Quality Category Insights

The XO and Extra Old category represents the leading value-generating segment within the distilling wine market, accounting for approximately 21% of global market revenue despite contributing a comparatively smaller share of overall consumption volume. The segment’s leadership is primarily driven by its significantly higher average selling prices, growing consumer preference for ultra-premium spirits, and increasing demand from gifting, luxury hospitality, and investment-oriented buyers. Rising affluence among consumers in North America, Europe, and Asia-Pacific continues to strengthen demand for aged products that offer superior complexity, craftsmanship, and exclusivity.VSOP products maintain broad market appeal by offering an attractive balance between quality, affordability, and accessibility. Their versatility across both personal consumption and social occasions enables them to attract a wide consumer base while serving as an entry point into premium brandy consumption. Vintage, reserve, and limited-edition expressions are increasingly attracting collectors and enthusiasts seeking rarity and long-term value appreciation, particularly in developed markets where premium spirits have emerged as alternative luxury assets.Meanwhile, non-aged and entry-level categories continue to generate substantial sales volumes, particularly across developing economies where affordability remains a key purchasing consideration. Although these products contribute significantly to market penetration and consumer accessibility, revenue growth remains concentrated within premium aging categories due to stronger pricing power and rising consumer willingness to trade up to higher-quality offerings.

Distribution Channel Insights

The off-trade channel remains the dominant distribution segment, accounting for approximately 63% of global distilling wine sales. Its leadership is driven by widespread consumer preference for at-home consumption, broader product availability, competitive pricing, and increasing convenience across purchasing platforms. Supermarkets, hypermarkets, specialty liquor retailers, online alcohol marketplaces, and duty-free outlets collectively play a critical role in supporting product accessibility across domestic and international markets. The continued expansion of organized retail infrastructure and improvements in alcohol e-commerce regulations are further strengthening off-trade sales performance globally.Online retail is emerging as one of the fastest-growing sales channels as digital adoption accelerates across both developed and emerging economies. Enhanced direct-to-consumer capabilities, personalized product recommendations, subscription models, and premium product accessibility are encouraging greater consumer engagement through digital platforms. Additionally, premium and luxury producers increasingly leverage online channels to strengthen brand visibility and expand international reach.On-trade channels, including hotels, restaurants, bars, lounges, and nightclubs, are experiencing renewed growth as global tourism, hospitality, and entertainment industries continue to recover. Premium and ultra-premium products particularly benefit from on-trade exposure, where curated tasting experiences, mixology programs, and luxury dining environments introduce consumers to higher-value offerings. Growing cocktail culture and increasing consumer interest in experiential drinking occasions are expected to further support on-trade channel expansion during the forecast period.

End-Use Insights

Household consumption represents the largest end-use segment, accounting for approximately 57% of global market demand. The segment’s leadership is driven by increasing consumer preference for premium spirits consumption at home, supported by evolving lifestyle patterns, growing home entertainment trends, and rising interest in personal collections of aged spirits. Consumers are increasingly purchasing premium brandies for gifting purposes, celebratory occasions, and luxury consumption experiences, contributing to sustained demand growth across multiple markets.The hospitality sector remains the second-largest end-use category and is expected to register the fastest growth through 2031. Expanding international tourism, increasing luxury travel expenditure, growth in premium dining establishments, and the rising popularity of cocktail culture are creating favorable conditions for market expansion. Hotels, fine-dining restaurants, and upscale bars continue to utilize premium wine-distilled spirits to enhance customer experiences and differentiate their beverage offerings.Additional opportunities are emerging within food processing and culinary applications, where distilled wine spirits are increasingly incorporated into premium confectionery products, gourmet desserts, sauces, marinades, and specialty food preparations. Corporate gifting programs, luxury events, and high-end social functions are also becoming important demand generators, particularly across rapidly developing markets in Asia-Pacific where premium alcohol consumption is increasingly associated with status and social prestige.

Price Segment Insights

The premium price segment remains the leading revenue contributor, accounting for approximately 38% of total global market value. Its dominance is primarily supported by increasing consumer preference for superior product quality, extended aging characteristics, authentic production methods, and prestigious brand positioning. Growing disposable incomes, rising luxury spending, and greater consumer awareness regarding craftsmanship and product heritage continue to drive premium segment expansion across major markets worldwide.The super-premium and ultra-premium categories are expanding at an even faster pace than the broader market, benefiting from rising wealth accumulation, luxury gifting trends, and increasing demand for exclusive, limited-edition offerings. Premiumization remains one of the most influential long-term industry trends, encouraging consumers to prioritize quality and experience over quantity.Economy and standard-priced products continue to maintain significant sales volumes, particularly across developing economies where affordability and accessibility remain important purchasing considerations. However, their contribution to overall market value growth remains comparatively limited due to intense price competition, lower profit margins, and the growing consumer shift toward premium alternatives.

Explore more data points, trends and opportunities Download Free Sample Report

Distilling Wine Market Segmentations

By Product Type

- Grape-Based Distilled Wine Spirits

- Fruit-Based Distilled Wine Spirits

- Specialty Distilled Wine Spirits

By Quality Category

- VS

- VSOP

- Napoleon

- XO

- Hors d'Age

- Vintage / Reserve

- Non-Aged / Young Brandy

By Price Segment

- Economy

- Standard

- Premium

- Super Premium

- Ultra-Premium

- Luxury Collectible

By Flavor Profile

- Traditional / Unflavored

- Fruit-Infused

- Botanical-Infused

- Spice-Infused

- Barrel-Finished Variants

By Packaging Format

- Glass Bottles

- Premium Decanters

- PET Bottles

- Cans / RTD Formats

- Miniatures

Regional Insights

North America

North America accounts for approximately 29% of the global distilling wine market, making it one of the largest and most profitable regional markets. The United States dominates regional demand and represents nearly 23% of global consumption, supported by a highly developed alcoholic beverage industry and strong consumer spending on premium spirits. The region benefits from a mature retail ecosystem, widespread product availability, and a well-established culture of premium alcohol consumption.Regional growth is primarily driven by increasing demand for premium and ultra-premium spirits, rising popularity of craft cocktails, growing consumer appreciation for aged alcoholic beverages, and expanding interest in luxury drinking experiences. The continued growth of cocktail culture across urban centers has increased demand for premium cognac and brandy products in bars, restaurants, and hospitality venues. Furthermore, rising disposable incomes, strong e-commerce penetration, innovation in premium packaging, and the expansion of craft distilleries are supporting market growth. Canada contributes additional momentum through rising imports of premium wine-distilled spirits and increasing consumer interest in artisanal alcoholic beverages.

Europe

Europe remains the largest regional market, accounting for approximately 39% of global market value. The region serves as the historical center of wine-distilled spirit production and consumption, with France maintaining its position as the leading producer and exporter of premium cognac and armagnac. Spain and Italy continue to support strong domestic consumption while also functioning as major export centers for international markets. Germany and the United Kingdom represent significant import markets characterized by high consumer demand for premium alcoholic beverages and well-developed retail infrastructure.Regional growth is driven by strong export demand for premium European spirits, the presence of globally recognized heritage brands, increasing international appreciation for geographically protected products, and continued premiumization across both domestic and export markets. Europe also benefits from centuries-old production expertise, strict quality standards, and protected geographical indication systems that reinforce product authenticity and brand value. Expanding tourism activity, luxury hospitality demand, and increasing consumer interest in aged and collectible spirits further contribute to sustained regional market growth.

Asia-Pacific

Asia-Pacific accounts for approximately 22% of the global market and represents the fastest-growing regional market, with expected growth exceeding 8.5% annually through 2031. China remains the largest regional market, accounting for nearly 12% of global demand, while India is emerging as one of the fastest-growing countries worldwide. Japan, South Korea, Vietnam, and Australia continue to contribute significantly to regional expansion through evolving consumer preferences and increasing premium spirit consumption.The region’s rapid growth is being driven by rising disposable incomes, accelerating urbanization, expansion of middle-class populations, increasing westernization of drinking habits, and growing consumer willingness to purchase premium imported spirits. Rising luxury consumption and gifting culture, particularly in China and Southeast Asia, are creating substantial opportunities for premium brandy producers. Additionally, expanding tourism, growth in premium hospitality infrastructure, increasing exposure to global beverage trends, and the rapid development of modern retail and e-commerce channels are supporting sustained market expansion throughout the region.

Latin America

Latin America accounts for approximately 6% of global market demand, with Brazil and Mexico representing the region’s largest consumer markets. Demand for premium imported wine-distilled spirits continues to strengthen as economic development supports rising consumer purchasing power and changing consumption patterns. Major metropolitan areas are witnessing increasing adoption of premium alcoholic beverages among younger professionals and affluent consumers.Regional growth is driven by expanding middle-class populations, increasing urbanization, growing awareness of international premium spirit brands, and the steady expansion of hospitality and tourism industries. The development of modern retail infrastructure and rising demand for premium lifestyle products are further supporting market penetration. Additionally, increasing participation in social drinking occasions and premium cocktail consumption is creating favorable conditions for long-term market growth across key regional economies.

Middle East & Africa

The Middle East & Africa region accounts for approximately 4% of global market value. South Africa remains the leading producer and consumer within the region, benefiting from a well-established brandy production industry, favorable grape cultivation conditions, and strong domestic consumption. The United Arab Emirates continues to serve as a key luxury consumption center and one of the world's most important duty-free retail hubs for premium alcoholic beverages.Regional growth is supported by increasing tourism activity, substantial investments in hospitality and entertainment infrastructure, rising luxury consumption among affluent consumers, and the continued expansion of premium retail environments across Gulf countries. Growing international visitor arrivals, development of high-end hotels and resorts, and increasing demand for imported luxury spirits are strengthening market opportunities throughout the region. In Africa, improving economic conditions, expanding urban populations, and the gradual premiumization of alcoholic beverage consumption are expected to contribute to future market expansion.

Key Players in the Distilling Wine Market

- LVMH (Hennessy)

- Rémy Cointreau

- Emperador Inc.

- Diageo plc

- E. & J. Gallo Winery

- Pernod Ricard

- Suntory Global Spirits

- Stock Spirits Group

- Torres Brandy

- Osborne Group

- Tilaknagar Industries

- Yantai Changyu Pioneer Wine

- Becle SAB

- Distell Group

- Camus Cognac