Dietary Fiber Market Size

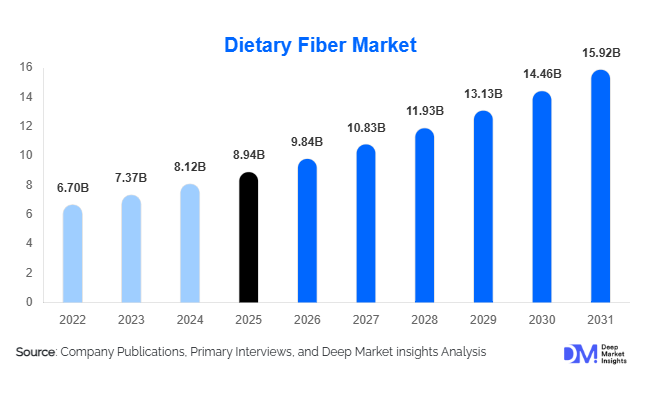

According to Deep Market Insights, the global dietary fiber market size was valued at USD 8.94 billion in 2025 and is projected to grow from USD 9.84 billion in 2026 to reach USD 15.92 billion by 2031, expanding at a CAGR of 10.1% during the forecast period (2026–2031). The dietary fiber market growth is primarily driven by increasing consumer awareness regarding digestive wellness, rising demand for functional foods and beverages, and the expanding use of fiber-enriched ingredients in nutraceuticals, pharmaceuticals, and plant-based nutrition products.

Key Market Insights

- Dietary fiber demand is increasingly shifting toward prebiotic and gut-health-focused formulations, supported by growing awareness regarding microbiome health and preventive nutrition.

- Functional food manufacturers are rapidly integrating soluble and insoluble fibers into bakery products, cereals, dairy alternatives, snacks, and beverages to support clean-label and high-fiber claims.

- North America dominates the global dietary fiber market, led by strong consumption of fortified foods and dietary supplements in the United States.

- Asia-Pacific remains the fastest-growing regional market, driven by rising health awareness, urbanization, and expanding nutraceutical industries in China and India.

- Plant-based and sugar-reduction applications are expanding rapidly, increasing demand for oat fiber, pea fiber, resistant starch, and citrus fiber ingredients.

- Technological advancements in extraction and fermentation technologies are enabling development of high-purity specialty fibers with enhanced functionality and stability.

dietary fiber market latest trends

Prebiotic and Gut Microbiome Nutrition Expansion

The growing scientific focus on gut microbiome health is significantly reshaping the dietary fiber market. Consumers are increasingly seeking products containing prebiotic fibers such as inulin, fructooligosaccharides (FOS), galactooligosaccharides (GOS), and resistant dextrin to support digestive health, immunity, and metabolic wellness. Food and nutraceutical manufacturers are responding by introducing microbiome-targeted formulations across beverages, dairy alternatives, nutritional supplements, and functional snacks. Personalized nutrition platforms and microbiome testing services are also accelerating demand for customized fiber blends designed for specific digestive and wellness outcomes. This trend is particularly strong in North America, Europe, and advanced Asian markets where preventive healthcare spending continues to rise.

Clean-Label and Plant-Based Fiber Innovations

Clean-label product development has become a major trend across the global dietary fiber industry. Consumers increasingly prefer natural, minimally processed, and plant-derived ingredients, encouraging manufacturers to expand use of oat fiber, citrus fiber, pea fiber, chicory root fiber, and resistant starches. Fiber ingredients are also gaining popularity as natural texturizers, fat replacers, and sugar-reduction solutions in plant-based foods. The rapid expansion of vegan meat alternatives, dairy substitutes, and low-calorie foods has created strong commercial opportunities for multifunctional fiber ingredients. Companies are investing heavily in sustainable extraction technologies and organic-certified fiber production to align with changing consumer preferences and environmental sustainability goals.

dietary fiber market drivers

Growing Consumer Focus on Preventive Healthcare

Rising global incidences of obesity, diabetes, cardiovascular diseases, and gastrointestinal disorders are significantly driving demand for dietary fiber products. Consumers are increasingly adopting preventive healthcare approaches, prioritizing nutrition and wellness-focused food consumption. Healthcare professionals and nutrition authorities continue promoting higher daily fiber intake to improve digestive function, support cholesterol management, regulate blood sugar levels, and aid weight management. As a result, demand for fiber-enriched cereals, nutrition bars, supplements, and beverages has accelerated globally. The increasing popularity of functional foods and wellness-oriented diets is expected to remain a major long-term growth driver for the dietary fiber market.

Rapid Expansion of Functional Foods and Nutraceuticals

The functional food and nutraceutical industries are expanding rapidly, creating sustained demand for specialty dietary fibers. Food manufacturers are increasingly incorporating soluble and insoluble fibers into bakery products, dairy alternatives, ready-to-drink beverages, sports nutrition products, and healthy snacks to improve nutritional value and support clean-label positioning. Nutraceutical companies are also launching targeted digestive wellness supplements containing prebiotic fiber blends. The growing popularity of protein-rich and low-sugar diets is further encouraging the use of fiber ingredients for texture enhancement, calorie reduction, and satiety improvement. This trend is particularly strong among health-conscious millennials and aging populations.

dietary fiber market restraints

High Processing and Specialty Ingredient Costs

Production of specialty dietary fibers such as beta-glucan, resistant starch, inulin, and fermentation-derived prebiotic ingredients requires advanced extraction technologies and strict quality standards, increasing manufacturing costs. Raw material price fluctuations involving oats, wheat, corn, and citrus fruits also create cost pressures for manufacturers. These pricing challenges can affect profitability and limit adoption of premium fiber ingredients in cost-sensitive markets.

Digestive Sensitivity and Regulatory Challenges

Excessive fiber intake may lead to digestive discomfort, bloating, or gastrointestinal sensitivity among certain consumers, creating formulation challenges for manufacturers. In addition, varying global regulations regarding nutritional labeling, fiber definitions, and health claims create compliance complexities for multinational companies. Regulatory approval processes for novel fibers and specialty ingredients can further delay commercialization and increase development costs.

dietary fiber industry key opportunities

Fiber-Based Sugar Reduction Solutions

The growing global push toward sugar reduction presents major opportunities for dietary fiber manufacturers. Governments worldwide are introducing sugar taxes, nutritional labeling mandates, and obesity-reduction initiatives, encouraging food producers to reformulate products with healthier alternatives. Dietary fibers are increasingly used as bulking agents and texture enhancers in low-sugar foods and beverages, enabling manufacturers to maintain mouthfeel and product stability while reducing calorie content. Soluble fibers such as polydextrose and resistant dextrin are witnessing strong adoption across confectionery, beverages, dairy alternatives, and bakery applications. This trend is expected to create significant long-term growth opportunities for specialty ingredient companies.

Expansion of Personalized Nutrition and Clinical Wellness

Personalized nutrition and clinical wellness applications are emerging as high-growth opportunities within the dietary fiber market. Nutraceutical companies are increasingly developing targeted fiber blends designed for digestive health, sports nutrition, metabolic health, and elderly nutrition. Advances in microbiome science and AI-driven nutritional analysis are enabling more customized dietary recommendations, accelerating demand for specialty prebiotic fibers. Clinical nutrition products targeting diabetes management, gastrointestinal disorders, and immune health are also incorporating advanced dietary fibers to improve therapeutic outcomes. These applications offer attractive premium pricing opportunities for ingredient innovators and specialty nutrition companies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.94 Billion |

| Market Size in 2026 | USD 9.84 Billion |

| Market Size in 2031 | USD 15.92 Billion |

| CAGR | 10.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Fiber Type Insights

Soluble fibers dominate the dietary fiber market, accounting for a significant share of global demand due to their strong association with digestive wellness, cholesterol management, and prebiotic functionality. Inulin, beta-glucan, and resistant dextrin are among the fastest-growing soluble fiber categories, supported by expanding use in functional beverages, dairy alternatives, and nutritional supplements. Insoluble fibers such as cellulose, wheat bran fiber, and corn bran fiber continue to maintain strong demand across bakery, cereals, and digestive health applications due to their effectiveness in supporting bowel regularity and digestive function. Functional and specialty fibers, including resistant starches and citrus fibers, are rapidly gaining popularity as manufacturers seek clean-label ingredients capable of supporting texture enhancement, sugar reduction, and calorie management in modern food formulations.

Application Insights

Food and beverage applications represent the largest segment within the dietary fiber market, driven by rising demand for fortified foods, clean-label nutrition, and healthier processed products. Bakery products, cereals, nutrition bars, dairy alternatives, and functional beverages remain major application areas for fiber ingredients. Dietary supplements are among the fastest-growing applications, supported by increasing preventive healthcare awareness and growing demand for digestive wellness products. Pharmaceutical applications are also expanding steadily, particularly in gastrointestinal therapeutics and clinical nutrition products targeting elderly populations and chronic disease management. Animal nutrition applications are emerging as an additional growth area, with fiber-enriched pet foods and livestock feed formulations gaining commercial traction.

Distribution Channel Insights

B2B ingredient supply agreements dominate the dietary fiber market, as large food and beverage manufacturers source specialty fibers directly from ingredient processors and global suppliers. Direct industrial contracts remain critical for ensuring consistent quality, regulatory compliance, and long-term pricing stability. Online retail channels are witnessing rapid growth, particularly for consumer-facing dietary supplements, fiber powders, and wellness products. Health and wellness stores, pharmacies, and specialty nutrition retailers continue expanding premium product distribution globally. Digital commerce platforms and direct-to-consumer marketing strategies are increasingly influencing purchasing behavior, particularly among younger and health-conscious consumers seeking personalized nutritional solutions.

End-Use Industry Insights

The food manufacturing industry remains the largest end-use sector for dietary fibers, driven by growing consumer demand for fortified foods, digestive wellness products, and plant-based nutrition. Beverage manufacturers are increasingly integrating soluble fibers into ready-to-drink functional beverages and meal replacement products. Nutraceutical companies represent one of the fastest-growing end-use industries due to increasing demand for preventive healthcare supplements and personalized wellness solutions. Pharmaceutical companies are also expanding usage of specialty fibers in clinical nutrition products and gastrointestinal health formulations. The animal feed industry is gradually emerging as a new application area, particularly in premium pet nutrition products emphasizing digestive health and balanced nutrition.

Explore more data points, trends and opportunities Download Free Sample Report

Dietary Fiber Market Segmentations

By Fiber Type

- Soluble Fiber

- Insoluble Fiber

- Functional & Specialty Fiber

By Source

- Cereals & Grains

- Fruits & Vegetables

- Legumes & Pulses

- Nuts & Seeds

- Microbial & Synthetic Sources

By Form

- Powder

- Granules

- Liquid

- Capsules/Tablets

- Sachets & Premixes

By Application

- Food & Beverage

- Dietary Supplements

- Pharmaceuticals

- Animal Feed

- Personal Care & Cosmetics

By Functionality

- Digestive Health Support

- Weight Management

- Blood Glucose Regulation

- Cholesterol Reduction

- Prebiotic Functionality

- Texture Enhancement & Fat Replacement

- Sugar Reduction Support

Regional Insights

North America

North America accounts for the largest share of the global dietary fiber market, supported by strong consumer awareness regarding digestive wellness, obesity management, and preventive nutrition. The United States dominates regional demand due to high consumption of functional foods, nutritional supplements, and fiber-fortified beverages. Consumers increasingly prefer clean-label and plant-based products containing natural fiber ingredients such as oat fiber, pea fiber, and resistant starch. Canada is also witnessing growing demand for premium wellness products and organic nutritional ingredients. Strong regulatory support for nutritional labeling and sugar reduction initiatives continues to strengthen regional market expansion.

Europe

Europe represents a major market for dietary fibers, driven by strict food labeling regulations and increasing consumer preference for functional nutrition products. Germany, France, the United Kingdom, and the Netherlands remain key contributors to regional demand. European consumers show strong interest in digestive health, clean-label products, and sustainable nutrition, encouraging adoption of prebiotic fibers and plant-based ingredients. The region also remains a major producer and exporter of chicory-derived inulin and specialty functional fibers. Growing vegan food consumption and sugar-reduction initiatives continue accelerating demand for multifunctional dietary fiber ingredients across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for dietary fibers, supported by rapid urbanization, rising disposable incomes, and increasing health awareness. China leads regional demand due to expanding functional food manufacturing and strong growth in the nutraceutical industry. India is witnessing rising consumption of fortified foods and preventive healthcare supplements, supported by growing middle-class health consciousness and government nutrition initiatives. Japan remains an important market for digestive wellness products and advanced functional ingredients, while South Korea and Australia are showing strong demand for premium dietary supplements and clean-label nutrition products. Expanding food processing industries and increasing healthcare spending are expected to sustain strong regional growth.

Latin America

Latin America is experiencing moderate but steady growth in the dietary fiber market, led by Brazil and Mexico. Rising obesity rates, expanding processed food industries, and growing awareness regarding digestive wellness are encouraging higher consumption of fiber-enriched foods and beverages. Brazil also represents an important agricultural producer for plant-based raw materials used in dietary fiber manufacturing. Nutritional supplement adoption is increasing steadily across urban populations, creating additional opportunities for functional food and nutraceutical companies operating in the region.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for functional nutrition and preventive healthcare products. The UAE and Saudi Arabia are leading regional consumption due to rising healthcare spending, urban lifestyle changes, and growing demand for imported premium wellness products. South Africa represents a developing market for fortified packaged foods and dietary supplements. Increasing investments in healthcare infrastructure, rising obesity concerns, and growing consumer awareness regarding nutrition are expected to support long-term dietary fiber market growth across the region.

Key Players in the Dietary Fiber Market

- Kerry Group

- Ingredion Incorporated

- Tate & Lyle

- Roquette Frères

- Cargill

- ADM

- Beneo

- IFF

- SunOpta

- Cosucra

- Südzucker Group

- Nexira

- Fiberstar

- Taiyo International

- Lonza