Cranberry Juice Market Size

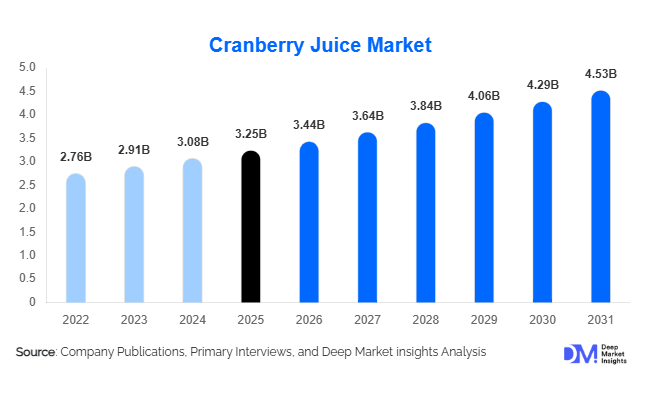

According to Deep Market Insights, the global cranberry juice market size was valued at USD 3.25 billion in 2025 and is projected to grow from USD 3.44 billion in 2026 to reach USD 4.53 billion by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The cranberry juice market growth is primarily driven by increasing consumer preference for functional beverages, rising awareness regarding urinary tract health and immunity support, growing demand for antioxidant-rich fruit-based drinks, and the expanding adoption of clean-label and organic beverage products. Manufacturers are increasingly investing in reduced-sugar formulations, premium cranberry blends, and wellness-oriented beverage innovations to capitalize on evolving consumer health preferences.

Key Market Insights

- Cranberry juice is increasingly positioned as a functional wellness beverage, supported by consumer awareness regarding antioxidant content, urinary tract health, and preventive healthcare benefits.

- Reduced-sugar and no-added-sugar formulations are gaining substantial traction, as consumers seek healthier alternatives to traditional fruit juice products.

- North America dominates the global cranberry juice market, accounting for more than half of global consumption due to strong production capabilities and established consumer awareness.

- Asia-Pacific represents the fastest-growing regional market, driven by rising disposable incomes, growing health consciousness, and expanding modern retail infrastructure.

- Organic cranberry juice products are growing significantly faster than conventional offerings, supported by increasing demand for clean-label and sustainably sourced beverages.

- E-commerce and direct-to-consumer distribution channels are reshaping market dynamics, enabling manufacturers to expand consumer reach and improve product accessibility globally.

Cranberry Juice Market Latest Trends

Functional Beverage Positioning Driving Category Expansion

Cranberry juice is increasingly being incorporated into the rapidly expanding functional beverage segment. Consumers are seeking beverages that offer measurable health benefits beyond hydration, including immune support, digestive wellness, antioxidant intake, and urinary tract health maintenance. Beverage manufacturers are responding by launching cranberry juice products fortified with vitamins, probiotics, minerals, collagen, and botanical ingredients. The trend is particularly strong among millennials and aging populations seeking preventive health solutions through daily dietary choices. Premium cranberry wellness beverages are achieving higher retail pricing and stronger brand loyalty compared to conventional juice products, helping manufacturers improve profitability while differentiating their offerings in a competitive beverage market.

Clean-Label and Organic Product Innovation Accelerating

Consumer demand for transparency and natural ingredients is reshaping product development across the cranberry juice industry. Organic cranberry juice, non-GMO formulations, preservative-free products, and sustainably sourced beverages are becoming increasingly important purchasing criteria. Manufacturers are investing heavily in organic certification, sustainable farming partnerships, recyclable packaging solutions, and transparent supply chains. Consumers are demonstrating willingness to pay premium prices for products that align with environmental sustainability and health-conscious lifestyles. This trend is particularly pronounced across North America and Europe, where regulatory support and consumer awareness regarding clean-label products continue to strengthen market adoption.

Cranberry Juice Market Drivers

Growing Consumer Focus on Preventive Healthcare

The increasing emphasis on preventive healthcare worldwide is creating substantial demand for functional beverages perceived to support overall wellness. Cranberry juice has long been associated with urinary tract health, antioxidant benefits, and immune support, making it a preferred choice among health-conscious consumers. Growing awareness regarding chronic disease prevention, healthy aging, and nutritional wellness continues to strengthen cranberry juice consumption across both developed and emerging markets. Healthcare professionals and nutrition experts increasingly encourage consumers to adopt healthier beverage alternatives, further supporting market growth.

Expansion of Functional Beverage Industry

The global functional beverage industry is experiencing robust growth, creating favorable conditions for cranberry juice manufacturers. Consumers are increasingly replacing carbonated soft drinks and sugar-laden beverages with healthier alternatives that offer nutritional benefits. Cranberry juice's naturally occurring antioxidants and wellness associations position it well within this trend. Manufacturers are introducing innovative formulations that combine cranberry juice with superfruits, vitamins, probiotics, and herbal extracts to capture greater market share within the functional beverage segment.

Rising Demand for Premium and Organic Juice Products

Premiumization continues to influence purchasing behavior across the beverage industry. Consumers are increasingly willing to pay higher prices for organic, sustainably sourced, and minimally processed juice products. Organic cranberry juice sales are growing considerably faster than conventional products, particularly among affluent urban consumers. Premium packaging, clean-label formulations, and environmentally responsible sourcing practices are contributing to higher average selling prices and stronger brand differentiation.

Cranberry Juice Market Restraints

Volatility in Cranberry Production and Raw Material Costs

Cranberry cultivation remains concentrated in a limited number of regions, primarily the United States and Canada. Weather disruptions, climate variability, pest outbreaks, and agricultural production challenges can significantly affect cranberry yields and pricing. Raw material price fluctuations impact manufacturing costs and profit margins, particularly for smaller market participants with limited sourcing flexibility. Supply chain disruptions can further create pricing instability across the global cranberry juice industry.

Consumer Concerns Regarding Sugar Content

Many conventional cranberry juice products contain added sugars to balance the fruit's naturally tart flavor profile. Rising awareness regarding obesity, diabetes, and excessive sugar consumption has increased consumer scrutiny of beverage labels. Regulatory pressure regarding sugar disclosure and taxation policies in certain markets is encouraging manufacturers to reformulate products. While reduced-sugar innovations present opportunities, the transition may increase production costs and create formulation challenges for producers seeking to maintain taste preferences.

Cranberry Juice Industry Key Opportunities

Growth of Functional Health and Nutraceutical Applications

The convergence of cranberry juice with the broader nutraceutical and functional wellness industries presents significant growth opportunities. Manufacturers can develop value-added formulations containing probiotics, immune-support ingredients, adaptogens, and clinically supported wellness compounds. Growing consumer interest in personalized nutrition and preventive healthcare is expected to accelerate demand for functional cranberry-based products. Companies capable of substantiating health claims through scientific research will likely achieve stronger competitive positioning and premium pricing advantages.

Expansion into Emerging Asia-Pacific Markets

Asia-Pacific remains substantially underpenetrated compared to North America and Europe, creating attractive growth prospects for both established players and new entrants. Countries including China, India, Japan, South Korea, and Southeast Asian markets are experiencing rising health awareness, increasing disposable incomes, and growing demand for imported premium beverages. Strategic investments in localized marketing, regional partnerships, and e-commerce distribution channels can help manufacturers capitalize on rapidly expanding consumer demand throughout the region.

Organic and Sustainable Product Development

Organic cranberry juice remains a relatively small but high-growth segment. Consumers increasingly prioritize environmentally responsible products, sustainable agriculture practices, and transparent sourcing. Companies investing in certified organic production, carbon-neutral operations, recyclable packaging, and sustainable supply chains can differentiate themselves from competitors while capturing premium consumer segments. Sustainability initiatives are also attracting greater support from retailers, institutional investors, and regulatory bodies, enhancing long-term market opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.25 Billion |

| Market Size in 2026 | USD 3.44 Billion |

| Market Size in 2031 | USD 4.53 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cranberry juice blends represent the largest product segment, accounting for approximately 56% of the global market in 2025. The leadership of this segment is primarily driven by strong consumer preference for improved taste profiles that balance the natural tartness of cranberry with sweeter fruit combinations such as apple, grape, pomegranate, and citrus. This flavor optimization strategy has significantly expanded consumer acceptance across mainstream households, particularly among younger demographics and first-time health beverage buyers. The segment also benefits from its positioning as an affordable functional beverage alternative, allowing manufacturers to achieve scale through mass retail distribution while maintaining competitive pricing. In addition, ongoing product innovation in low-sugar and no-added-sugar blends is strengthening demand among health-conscious consumers without compromising palatability.Cranberry juice cocktails continue to maintain strong traction in conventional retail channels due to their affordability, broad accessibility, and long-standing brand familiarity. Meanwhile, 100% pure cranberry juice is witnessing accelerating demand from premium and health-focused consumer groups, driven by rising awareness of antioxidant properties, urinary tract health benefits, and clean-label dietary preferences. This shift is further reinforced by growing skepticism toward added sugars and artificial flavoring in beverages. Functional ready-to-drink cranberry beverages represent the fastest-evolving subsegment, supported by rising demand for immunity-boosting, probiotic-infused, and vitamin-fortified beverages that align with global wellness trends and preventive health consumption behavior.

Nature Insights

Conventional cranberry juice continues to dominate the market, accounting for approximately 78% of global revenue in 2025. Its leadership is primarily supported by cost-efficient production systems, well-established agricultural supply chains, and widespread availability across both developed and emerging markets. The segment benefits from strong integration into mass retail channels, where price sensitivity remains a key purchasing driver, particularly in developing economies. Large-scale production capabilities and consistent supply stability further reinforce its dominance in global trade flows.Organic cranberry juice, while smaller in share, is experiencing significantly stronger growth momentum due to rising consumer demand for natural, non-GMO, and sustainably sourced food and beverage products. Growth is particularly strong in North America and Europe, where regulatory transparency and clean-label expectations are more advanced. The segment’s expansion is further supported by premium positioning, which allows manufacturers to command higher price points while catering to environmentally conscious consumers. Increasing investment in organic certification, sustainable farming practices, and traceable supply chains is further strengthening long-term growth prospects in this category.

Packaging Format Insights

PET bottles remain the leading packaging format, representing approximately 42% of total market demand in 2025. Their dominance is driven by cost efficiency, lightweight structure, durability, and ease of transportation, making them highly suitable for mass-market distribution. The convenience factor associated with resealable PET packaging has further strengthened consumer adoption, particularly in on-the-go consumption scenarios and household usage. Manufacturers continue to innovate with recyclable and bio-based PET solutions in response to increasing environmental regulations and sustainability expectations.Tetra Pak cartons are gaining strong traction due to their extended shelf life capabilities, reduced carbon footprint, and suitability for aseptic packaging, which preserves nutritional value without requiring preservatives. Glass bottles maintain a strong position in premium, organic, and specialty segments where product purity perception and aesthetic appeal are important purchase drivers. Aluminum cans are increasingly used in functional cranberry beverages, particularly in single-serve formats targeting convenience-oriented urban consumers. Across all formats, sustainability considerations and circular economy initiatives are increasingly shaping packaging innovation strategies.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 55% of global cranberry juice sales in 2025, maintaining their dominance due to extensive shelf visibility, strong promotional activity, and the ability to offer a wide assortment of brands and price points under one roof. These retail formats benefit from high consumer trust and habitual purchasing patterns, especially in urban and suburban areas. The in-store experience, combined with bulk purchasing opportunities, continues to reinforce their leadership position in the distribution ecosystem.E-commerce is emerging as the fastest-growing distribution channel, driven by rapid digital adoption, increasing penetration of online grocery platforms, and the expansion of direct-to-consumer beverage brands. This growth is further supported by subscription-based delivery models and personalized nutrition offerings. Specialty health stores continue to play a critical role in premium and organic product distribution, benefiting from their curated product assortments and health-focused positioning. Foodservice channels, including hotels, cafés, and institutional buyers, remain an important demand base, particularly for bulk procurement and functional beverage applications. The growing emphasis on omnichannel retail strategies is enabling manufacturers to enhance consumer reach and strengthen brand engagement across multiple purchasing touchpoints.

Application Insights

Direct beverage consumption remains the largest application segment, accounting for approximately 63% of the global market in 2025. This dominance is primarily driven by household consumption patterns where cranberry juice is positioned as a functional daily beverage associated with urinary tract health, hydration, and antioxidant benefits. The segment benefits from strong repeat purchase behavior and widespread retail availability across both premium and value categories.Functional beverage applications are expanding rapidly, supported by increasing consumer interest in immunity support, digestive health, and holistic wellness. Manufacturers are actively incorporating added vitamins, minerals, probiotics, and botanical extracts to enhance product differentiation. Nutraceutical applications are also gaining traction as cranberry concentrates and powders are increasingly used in dietary supplements and preventive health formulations. Food processing and pharmaceutical applications, while smaller in scale, are steadily growing, particularly in clinical nutrition, medical beverages, and functional food formulations targeting specific health conditions.

End-Use Industry Insights

The retail beverage industry remains the largest end-use sector, accounting for approximately 60% of total market demand. Its leadership is supported by strong consumer preference for ready-to-drink functional beverages, increasing retail penetration, and continuous product diversification by major beverage manufacturers. Brand-driven marketing and health positioning strategies further reinforce demand across retail environments.The functional beverage industry represents the fastest-growing end-use segment, driven by rising consumer focus on preventive healthcare, immunity enhancement, and lifestyle-oriented nutrition. Nutraceutical companies are increasingly incorporating cranberry-derived ingredients into capsules, powders, and fortified formulations, expanding the ingredient’s application scope beyond beverages. Pharmaceutical usage is also increasing, particularly in products targeting urinary tract health and anti-inflammatory benefits. Additionally, food manufacturing companies are utilizing cranberry juice concentrates in sauces, snacks, and fortified food products, reflecting growing cross-category application potential.

Explore more data points, trends and opportunities Download Free Sample Report

Cranberry Juice Market Segmentations

By Product Type

- 100% Pure Cranberry Juice

- Cranberry Juice Blends

- Cranberry Juice Cocktails

- Cranberry Juice Concentrates

- Ready-to-Drink Functional Cranberry Beverages

By Nature

- Conventional Cranberry Juice

- Organic Cranberry Juice

By Sweetening Profile

- Unsweetened

- Naturally Sweetened

- Artificially Sweetened / Low-Calorie

By Packaging Format

- PET Bottles

- Glass Bottles

- Tetra Pak / Carton Packaging

- Aluminum Cans

- Bag-in-Box Packaging

- Bulk Industrial Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health & Organic Stores

- Online Retail / E-commerce

- Foodservice & HoReCa Distribution

- Direct-to-Consumer (DTC)

Regional Insights

North America

North America remains the dominant regional market, accounting for approximately 51% of global cranberry juice consumption in 2025. The region’s leadership is strongly supported by established cranberry cultivation ecosystems, particularly in the United States, where nearly 44% of global demand is generated. A key growth driver is the deep-rooted consumer awareness of cranberry’s health benefits, especially related to urinary tract health and antioxidant properties. High disposable income levels, mature retail infrastructure, and strong penetration of functional beverages further reinforce regional dominance. Continuous product innovation, particularly in low-sugar and fortified beverages, is also accelerating premiumization trends across the market.

Europe

Europe accounts for approximately 25% of global market revenue, with strong demand concentrated in Germany, the United Kingdom, France, Italy, and the Netherlands. Regional growth is driven by increasing consumer preference for organic, clean-label, and sustainably produced beverages, reflecting broader environmental and health-conscious purchasing behavior. Germany leads the region due to its strong functional beverage culture and advanced retail ecosystem. Sustainability regulations, coupled with growing demand for natural health products, are encouraging manufacturers to adopt transparent sourcing and eco-friendly production practices, thereby enhancing market competitiveness.

Asia-Pacific

Asia-Pacific accounts for approximately 15% of the global market and represents the fastest-growing regional segment, with projected growth exceeding 8% CAGR through 2031. The region’s expansion is driven by rising disposable incomes, rapid urbanization, and increasing awareness of functional health beverages. China leads demand due to expanding middle-class consumption and growing interest in imported wellness products. India is emerging as a high-growth market supported by shifting dietary preferences and rising health consciousness. Japan, South Korea, and Australia continue to show stable demand, supported by premium beverage consumption trends. The rapid expansion of e-commerce platforms and modern retail formats is further accelerating product accessibility across urban and semi-urban areas.

Latin America

Latin America accounts for approximately 6% of global market demand, with Brazil and Mexico serving as the primary consumption hubs. Market growth is driven by expanding middle-class populations, increasing awareness of functional beverages, and gradual lifestyle shifts toward healthier consumption patterns. Premiumization trends are becoming more visible in urban centers, while imported cranberry juice products continue to dominate due to limited regional production capacity. Rising retail modernization and expanding supermarket penetration are further supporting category growth across the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 3% of global market revenue. Growth is primarily concentrated in the United Arab Emirates, Saudi Arabia, and South Africa, where demand is supported by rising health awareness and increasing preference for imported premium beverages. The expansion of modern retail infrastructure and hospitality sectors is further contributing to market development. In addition, increasing disposable incomes and a growing focus on preventive healthcare are expected to strengthen long-term demand for functional and premium cranberry juice products across the region.

Key Players in the Cranberry Juice Market

- Ocean Spray Cranberries

- Lassonde Industries

- PepsiCo

- The Coca-Cola Company

- Welch Foods

- R.W. Knudsen Family

- Lakewood Organic

- Old Orchard Brands

- Dynamic Health Laboratories

- Fruit d'Or

- Decas Cranberry Products

- Atoka

- Happy Day

- Trader Joe's

- Biedronka