Coconut Pudding Market Size

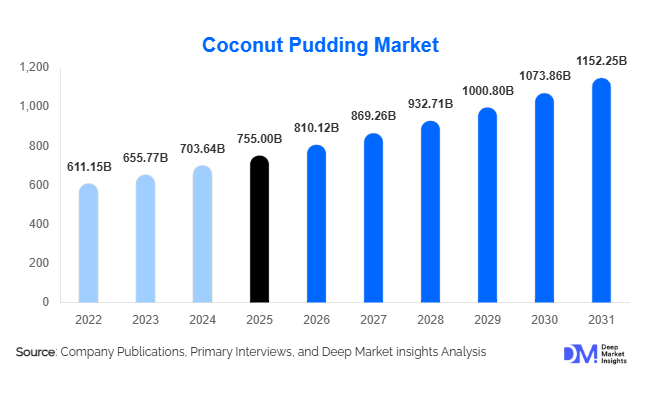

According to Deep Market Insights, the global coconut pudding market size was valued at approximately USD 755 million in 2025 and is projected to grow from USD 810 million in 2026 to reach USD 1,150 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The coconut pudding market growth is primarily driven by the rising demand for plant-based desserts, increasing consumer preference for dairy-free and lactose-free food products, and the growing popularity of premium ready-to-eat tropical desserts across both developed and emerging economies. Product innovations in organic formulations, low-sugar recipes, and functional ingredients are further strengthening the industry's growth prospects.

Key Market Insights

- Plant-based and vegan dessert consumption is reshaping the coconut pudding industry, positioning coconut-based products as a mainstream dairy alternative.

- Ready-to-eat coconut pudding cups dominate the market, supported by convenience food trends and increasing on-the-go snacking consumption.

- Asia-Pacific accounts for the largest market share, benefiting from abundant coconut production, established culinary traditions, and expanding packaged dessert consumption.

- North America remains one of the fastest-growing markets, driven by increasing demand for vegan, clean-label, and premium desserts.

- Premiumization and functional ingredient integration are accelerating product innovation, with manufacturers launching high-protein, probiotic, and reduced-sugar coconut puddings.

- E-commerce and direct-to-consumer distribution channels are expanding rapidly, enabling niche and premium brands to penetrate global markets more effectively.

Coconut Pudding Market Latest Trends

Premium and Functional Coconut Desserts Gaining Popularity

The coconut pudding market is increasingly moving toward premium and functional products that combine indulgence with health benefits. Consumers are seeking desserts made with natural ingredients, organic coconut milk, and clean-label formulations free from artificial additives and preservatives. Manufacturers are responding by introducing protein-enriched, probiotic-infused, and low-sugar coconut pudding variants that appeal to health-conscious consumers. Functional ingredients such as collagen, plant proteins, vitamins, and dietary fibers are increasingly being incorporated into coconut pudding formulations to create differentiated offerings and improve profit margins.

Expansion of Plant-Based and Dairy-Free Snacking

The rapid growth of plant-based eating patterns is significantly influencing coconut pudding demand. Consumers with lactose intolerance, vegan lifestyles, and flexitarian diets are increasingly substituting traditional dairy desserts with coconut-based alternatives. Single-serve ready-to-eat pudding cups and snack-sized products are becoming particularly popular among younger consumers and urban professionals seeking healthier convenience foods. Additionally, premium brands are introducing tropical fruit combinations and seasonal flavors to enhance product appeal and expand consumption occasions.

Coconut Pudding Market Drivers

Increasing Demand for Plant-Based Foods

The global shift toward plant-based diets has substantially increased demand for coconut-based desserts. Coconut pudding naturally aligns with vegan and lactose-free dietary requirements, making it an attractive alternative to traditional dairy puddings. Rising consumer awareness regarding digestive health and food sensitivities is expected to support long-term category expansion.

Growing Consumption of Premium Desserts

Consumers are increasingly willing to spend on premium and artisanal desserts featuring authentic ingredients and exotic flavors. Coconut pudding has benefited from premiumization trends as manufacturers introduce organic, low-sugar, and gourmet variants. Rising disposable incomes and changing eating habits in emerging economies are further accelerating demand for premium packaged desserts.

Expansion of Convenience Food Consumption

The growing preference for ready-to-eat and portable snacks has significantly increased the popularity of coconut pudding products. Single-serve packaging formats and refrigerated dessert products are witnessing strong demand from busy urban consumers seeking convenient yet indulgent food options. The expansion of modern retail and online grocery channels is further improving product accessibility.

Coconut Pudding Market Restraints

Volatility in Coconut Raw Material Prices

The coconut pudding industry is highly dependent on coconut milk and coconut cream supplies from major producing countries such as the Philippines, Indonesia, and Thailand. Weather disruptions, supply shortages, and agricultural production fluctuations often result in raw material price volatility, creating challenges for manufacturers in maintaining stable profit margins.

Limited Consumer Awareness in Certain Markets

Despite growing popularity, coconut pudding remains a relatively niche dessert category in several Western markets where consumers are more familiar with dairy puddings, yogurts, and protein desserts. Limited awareness and competition from substitute products continue to constrain broader market penetration and require significant marketing investments from industry participants.

Coconut Pudding Industry Key Opportunities

Expansion of Plant-Based Dessert Portfolios

The rapid expansion of the global plant-based food industry presents substantial opportunities for coconut pudding manufacturers. Major food companies are increasingly incorporating dairy-free desserts into their product portfolios to address growing consumer demand for vegan and lactose-free alternatives. Coconut pudding is particularly well positioned because of its natural plant-based characteristics and compatibility with clean-label trends. New entrants can capitalize on this opportunity by introducing organic, fortified, and premium coconut dessert offerings targeting health-conscious consumers.

Emerging Market Growth and Premiumization

Rising disposable incomes and urbanization in countries such as India, Indonesia, Vietnam, Brazil, and Saudi Arabia are creating significant opportunities for packaged dessert manufacturers. Increasing penetration of supermarkets, convenience stores, and e-commerce platforms is enabling premium dessert brands to access previously underserved consumer segments. Manufacturers are also benefiting from growing demand for indulgent tropical desserts among younger demographics and middle-income consumers.

Functional and Nutritional Product Innovation

The increasing consumer preference for foods that provide additional health benefits is encouraging innovation in coconut pudding formulations. Functional ingredients such as probiotics, plant proteins, collagen, and vitamins are being incorporated into products to address consumer demand for healthier indulgence. This trend provides opportunities for manufacturers to differentiate their products, command premium pricing, and improve overall profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 755.00 Billion |

| Market Size in 2026 | USD 810.12 Billion |

| Market Size in 2031 | USD 1152.25 Billion |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ready-to-eat coconut pudding products dominate the global landscape, accounting for approximately 58% of total market revenue. This leadership is primarily driven by accelerating urbanization, increasingly busy consumer lifestyles, and the rising demand for convenient, indulgent yet portion-controlled dessert options. The segment benefits strongly from retail-ready packaging innovations and expanding chilled dessert assortments across modern trade channels. Refrigerated coconut pudding variants continue to gain momentum within the premium dessert category, supported by superior sensory appeal, fresher taste perception, and growing consumer willingness to pay for higher-quality indulgence experiences. Shelf-stable coconut pudding products are particularly important in emerging economies where limited cold-chain infrastructure and price sensitivity encourage longer shelf-life formats, enabling broader geographic penetration. Instant and powdered coconut pudding mixes are expanding steadily, driven by increased at-home baking trends, foodservice customization needs, and demand for flexible preparation formats, while frozen coconut pudding desserts, though still niche, are emerging rapidly in developed markets due to innovation in plant-based frozen indulgence and expanding gourmet dessert culture.

Formulation Insights

Conventional coconut pudding formulations continue to lead the global market with nearly 68% share, largely due to their established manufacturing base, cost efficiency, and widespread consumer familiarity. Their dominance is further reinforced by strong retail penetration and consistent demand across both developed and developing economies. However, structural shifts in dietary preferences are accelerating the growth of vegan and organic formulations, which are emerging as the fastest-growing category within the segment. This growth is primarily driven by rising lactose intolerance awareness, increasing adoption of plant-based lifestyles, and heightened consumer scrutiny regarding ingredient transparency and sustainability. Reduced-sugar and functional coconut pudding variants are also gaining traction as premium offerings, supported by growing health consciousness, government initiatives targeting sugar reduction, and consumer interest in desserts that offer added nutritional or functional benefits such as digestive health or clean-label positioning.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, contributing approximately 42% of global sales, supported by their extensive product assortments, strong merchandising capabilities, and high consumer footfall that encourages impulse purchasing behavior. These outlets continue to serve as the primary access point for both mass-market and premium coconut pudding products, particularly in urban and semi-urban regions. Convenience stores also play a critical role in driving incremental demand, especially in densely populated urban centers where on-the-go consumption and single-serve packaging formats align with fast-paced lifestyles. The fastest-growing distribution channel is online retail and direct-to-consumer platforms, which are being propelled by digital adoption, expanding e-grocery ecosystems, and increasing consumer preference for home delivery convenience. These channels also enable brands to deploy targeted marketing strategies, subscription models, and personalized product offerings, which are strengthening customer retention and accelerating premium product penetration across diverse consumer segments.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for nearly 61% of global demand, supported by the growing trend of at-home indulgence and increasing availability of premium packaged dessert options. The shift toward home-based consumption has been reinforced by evolving eating habits, greater exposure to global cuisines, and rising demand for convenient yet high-quality dessert experiences that can be enjoyed without preparation complexity. The foodservice sector, which includes cafés, hotels, restaurants, and quick-service establishments, represents the fastest-growing end-use category, driven by menu diversification strategies and the increasing incorporation of coconut-based desserts into gourmet and health-oriented offerings. This growth is further supported by tourism expansion, rising experiential dining trends, and the popularity of plant-based dessert menus. Institutional demand from schools, hospitals, and corporate cafeterias is also gradually expanding, particularly in Asia-Pacific and the Middle East, where dietary diversification programs and large-scale catering needs are creating sustained long-term consumption opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Coconut Pudding Market Segmentations

By Product Type

- Ready-to-Eat (RTE) Coconut Pudding Cups

- Refrigerated Coconut Pudding

- Shelf-Stable Coconut Pudding

- Instant/Powder Coconut Pudding Mixes

- Frozen Coconut Pudding Desserts

By Formulation

- Conventional Coconut Pudding

- Organic Coconut Pudding

- Vegan/Plant-Based Coconut Pudding

- Reduced Sugar/No Added Sugar Coconut Pudding

- Functional/Fortified Coconut Pudding

By Flavor Profile

- Original Coconut

- Coconut-Vanilla

- Coconut-Chocolate

- Coconut-Fruit Blends

- Premium and Seasonal Flavors

By Packaging Type

- Single-Serve Cups

- Multi-Pack Cups

- Pouches

- Tubs and Family Packs

- Foodservice Bulk Packaging

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Food Stores

- Online Retail and E-commerce

- Direct-to-Consumer (DTC)

- Foodservice Distributors

Regional Insights

Asia-Pacific

Asia-Pacific leads the global coconut pudding market with approximately 41% of global revenue in 2025, supported by a combination of strong raw material availability, deep-rooted cultural affinity for coconut-based desserts, and rapid expansion of modern retail infrastructure. The region’s dominance is further reinforced by rising disposable incomes, urbanization-driven dietary shifts, and growing demand for packaged and convenience-oriented dessert products. China remains a key contributor, accounting for nearly 13% of global demand, with growth driven by premiumization of dessert consumption, rapid expansion of e-commerce grocery platforms, and increasing adoption of Western-style dessert formats. India is emerging as one of the fastest-growing markets, fueled by a young population base, increasing health awareness, lactose-free dietary preferences, and strong retail expansion across tier-1 and tier-2 cities. Southeast Asian countries such as Thailand, Indonesia, and the Philippines also serve as both strong consumption markets and critical production hubs, benefiting from abundant coconut cultivation, established export ecosystems, and growing processed food industries that support regional and global supply chains.

North America

North America accounts for approximately 24% of global market revenue, with the United States representing the largest share of regional demand. Growth in this region is strongly driven by the widespread adoption of plant-based diets, increasing prevalence of lactose intolerance, and a rising consumer shift toward healthier indulgent dessert alternatives. The premium ready-to-eat segment is particularly strong, supported by innovation in clean-label formulations, organic positioning, and functional dessert offerings. Canada is also experiencing steady expansion, driven by increasing multicultural food influence, rising awareness of dairy-free nutrition, and broader availability of vegan dessert options across mainstream retail and specialty health stores. The region’s strong cold-chain logistics infrastructure and high consumer spending power further support the penetration of refrigerated and premium coconut pudding variants.

Europe

Europe contributes approximately 22% of global demand, with strong growth underpinned by consumer preference for organic, sustainable, and clean-label food products. Major consumption centers such as Germany, the United Kingdom, and France are witnessing rising demand driven by expanding vegan populations, increasing interest in plant-based indulgence, and growing acceptance of tropical flavors within mainstream dessert categories. Regulatory emphasis on sugar reduction and ingredient transparency is also encouraging innovation in healthier coconut pudding formulations, including reduced-sugar and fortified variants. Additionally, European consumers are increasingly drawn to ethically sourced and environmentally sustainable packaging, which is pushing manufacturers to adopt greener production and supply chain practices while enhancing brand differentiation in a highly competitive market.

Latin America

Latin America accounts for nearly 6% of global demand, with Brazil and Mexico leading regional consumption. Market expansion is strongly influenced by rapid urbanization, rising disposable incomes, and increasing exposure to global dessert trends. Coconut-based products benefit from strong consumer acceptance due to the region’s familiarity with tropical flavors and longstanding culinary integration of coconut in traditional foods. Growth is further supported by expanding modern retail networks and the gradual shift from homemade desserts to packaged convenience foods, particularly among urban middle-class consumers seeking affordable indulgence and ready-to-eat options.

Middle East & Africa

The Middle East and Africa collectively represent approximately 7% of global market revenue, with growth driven by rising premium food consumption, expanding tourism activity, and increasing diversification of dietary preferences. The United Arab Emirates and Saudi Arabia are leading regional markets, supported by strong hospitality sectors, high per capita spending on premium desserts, and growing demand for international and plant-based food offerings. South Africa is emerging as a key growth market within Africa, benefiting from improving retail infrastructure, rising health awareness, and gradual adoption of dairy-free and vegan food products. Across the region, expanding expatriate populations and increasing exposure to global food cultures are further accelerating demand for innovative coconut-based dessert products.

Key Players in the Coconut Pudding Market

- Danone

- The Kraft Heinz Company

- The Coconut Collaborative

- Kozy Shack Enterprises

- House Foods Group

- Healthy Traditions

- Jellico Food

- Nantong Litai Jianlong Food

- Xiamen Jinhua Hezuo Foods

- Jiashibo

- GLOBAL FORSUCCESS

- Hey Boo

- Thai Coconut Public Company

- Schwan's Company

- General Mills