Cocoa Butter Equivalent (CBE) Market Size

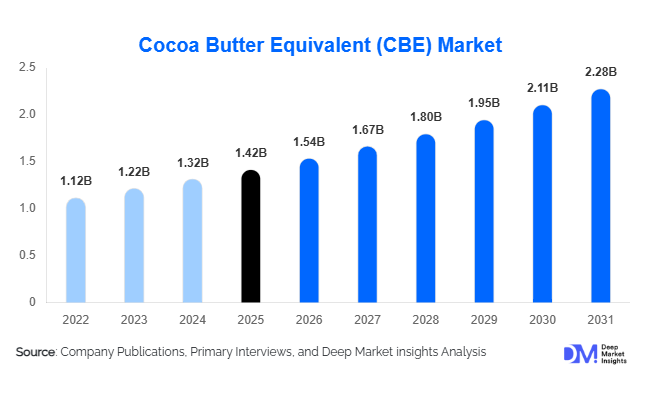

According to Deep Market Insights, the global cocoa butter equivalent (CBE) market size was valued at USD 1.42 billion in 2025 and is projected to grow from USD 1.54 billion in 2026 to reach USD 2.28 billion by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The cocoa butter equivalent market growth is primarily driven by increasing global chocolate consumption, rising demand for cost-effective confectionery formulations, and the expanding use of specialty vegetable fats in bakery, cosmetics, and pharmaceutical applications.

Key Market Insights

- Cocoa butter equivalents are increasingly replacing conventional cocoa butter in industrial chocolate manufacturing, helping manufacturers reduce formulation costs while maintaining texture, gloss, and melting characteristics.

- Sustainable and RSPO-certified specialty fats are gaining strong traction globally, as multinational confectionery companies prioritize ethical sourcing and environmentally responsible supply chains.

- Europe dominates the global CBE market, supported by strong chocolate manufacturing industries in Germany, Belgium, Switzerland, and the Netherlands.

- Asia-Pacific remains the fastest-growing regional market, driven by rising chocolate consumption, rapid urbanization, and growing processed food demand across China, India, Indonesia, and Southeast Asia.

- Industrial confectionery manufacturers account for the largest share of demand, particularly in compound chocolates, coatings, bakery fillings, and heat-resistant chocolate products.

- Technological advancements in enzymatic interesterification and specialty fat fractionation are enabling the development of customized, trans-fat-free, and premium-performance cocoa butter alternatives.

Cocoa Butter Equivalent Market Latest Trends

Sustainable Specialty Fat Sourcing Becoming Industry Standard

Sustainability has become one of the most influential trends shaping the cocoa butter equivalent market. Global chocolate manufacturers are increasingly demanding RSPO-certified palm oil, traceable shea butter, and ethically sourced vegetable fats to align with environmental, social, and governance (ESG) objectives. Consumers are becoming more conscious about deforestation, carbon emissions, and ethical sourcing practices associated with vegetable oil production, forcing manufacturers to strengthen supply-chain transparency. Specialty fat producers are therefore investing heavily in traceability systems, sustainable plantation partnerships, and low-carbon refining technologies. Companies are also adopting circular manufacturing models and renewable energy integration in production facilities to reduce environmental impact. Sustainable sourcing has evolved from a niche differentiator into a mainstream procurement requirement among global confectionery brands.

Customized Heat-Resistant Chocolate Formulations Expanding Rapidly

Demand for heat-resistant and climate-stable chocolate products is accelerating globally, particularly in Asia-Pacific, the Middle East, and Latin America. Cocoa butter equivalents are increasingly being used to improve melting resistance and product stability in warm climates where traditional cocoa butter formulations face logistical and storage limitations. Manufacturers are developing highly customized triglyceride blends using advanced fractionation and enzymatic processing technologies to optimize melting profiles, hardness, and gloss retention. This trend is supporting the expansion of premium compound chocolates, bakery coatings, and confectionery exports into tropical regions. In addition, foodservice operators and packaged snack manufacturers are increasingly preferring specialty fats that deliver longer shelf life, easier processing, and better transportation resilience without compromising consumer sensory expectations.

Cocoa Butter Equivalent Market Drivers

Rising Cocoa Price Volatility Supporting Alternative Fat Adoption

Fluctuating cocoa prices and supply-chain disruptions in major cocoa-producing countries are significantly driving the adoption of cocoa butter equivalents globally. Climate variability, crop diseases, and geopolitical instability in West African cocoa-producing regions have increased procurement uncertainty for chocolate manufacturers. As a result, industrial confectionery companies are increasingly integrating specialty vegetable fats into formulations to stabilize production costs while maintaining consistent product quality. Cocoa butter equivalents provide economic flexibility and reduce exposure to volatile raw material markets, particularly for compound chocolates and coated confectionery products. This cost optimization advantage is becoming increasingly critical for manufacturers operating in price-sensitive mass-market confectionery segments.

Expansion of Processed Confectionery and Bakery Industries

The rapid expansion of global processed food industries is accelerating demand for specialty fats across confectionery, bakery, and frozen dessert applications. Industrial chocolate manufacturers are increasingly utilizing CBEs because they offer enhanced processing flexibility, reduced tempering complexity, and superior heat stability compared to conventional cocoa butter. The bakery industry is also adopting cocoa butter alternatives in fillings, icings, coatings, and wafer creams due to their smooth texture and improved shelf-life performance. Rising consumption of packaged snacks, premium desserts, and convenience foods across emerging economies is creating strong long-term demand for specialty vegetable fats globally.

Global Market Restraints

Regulatory Restrictions on Cocoa Butter Equivalent Usage

One of the key restraints affecting the cocoa butter equivalent market is the variation in regulatory standards governing specialty fat usage in chocolate products. Different countries maintain different permissible inclusion limits and labeling requirements for CBEs in confectionery formulations. European regulations allow limited usage percentages in chocolate products, while several countries enforce stricter disclosure norms regarding cocoa butter substitution. These regulatory inconsistencies create formulation complexities and export-related challenges for multinational manufacturers operating across multiple markets. Compliance with varying food safety and labeling standards also increases operational costs for specialty fat producers.

Volatility in Vegetable Oil and Shea Butter Prices

The cocoa butter equivalent market remains highly sensitive to fluctuations in palm oil, shea butter, and other specialty vegetable fat prices. Supply-chain disruptions, sustainability-driven plantation restrictions, weather-related crop issues, and geopolitical uncertainty can significantly impact raw material availability and pricing. Since specialty fat manufacturing relies heavily on agricultural commodities, unexpected changes in raw material costs can compress profit margins and reduce pricing stability for downstream confectionery manufacturers. In addition, sustainability certifications and traceability requirements may further increase sourcing expenses, particularly for premium-grade CBEs used in high-end chocolate applications.

Cocoa Butter Equivalent Industry Key Opportunities

Expansion of Premium Compound Chocolate Manufacturing

The rapid growth of premium and mid-range compound chocolate products presents a major opportunity for cocoa butter equivalent manufacturers. Emerging economies such as China, India, Brazil, Indonesia, and Vietnam are witnessing increasing demand for affordable premium confectionery products among urban middle-class consumers. Manufacturers are increasingly utilizing CBEs to replicate premium cocoa butter functionality while improving production economics. This opportunity is particularly significant for suppliers capable of offering customized fat blends tailored to regional climate conditions and sensory preferences. As chocolate consumption continues to expand globally, demand for specialty fats optimized for premium compound formulations is expected to accelerate significantly.

Growing Applications in Cosmetics and Pharmaceuticals

The cosmetics and pharmaceutical industries are emerging as attractive growth opportunities for the cocoa butter equivalent market. Specialty vegetable fats are increasingly being incorporated into lipsticks, body lotions, creams, soaps, and pharmaceutical suppositories due to their stable melting behavior, smooth texture, and plant-based composition. Rising consumer preference for natural and sustainable cosmetic ingredients is driving demand for vegetable fat-derived emollients that offer improved oxidative stability and enhanced skin-feel properties. Pharmaceutical manufacturers are also exploring specialty fats for temperature-stable medicinal delivery systems. Diversification into non-confectionery applications is expected to reduce market dependency on chocolate demand cycles while expanding revenue opportunities for specialty fat manufacturers globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.42 Billion |

| Market Size in 2026 | USD 1.54 Billion |

| Market Size in 2031 | USD 2.28 Billion |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cocoa butter equivalents remain the dominant product category, accounting for nearly 46% of the global market share in 2025. Shea-based and palm mid-fraction CBEs are particularly preferred due to their close compatibility with cocoa butter triglyceride structures and their ability to deliver premium gloss, snap, and melting characteristics in confectionery products. Cocoa butter replacers and cocoa butter substitutes are also witnessing increasing demand in compound chocolate and bakery coating applications because of their lower cost and improved processing flexibility. Heat-resistant specialty fat blends are gaining traction in tropical markets where conventional cocoa butter formulations face storage and transportation challenges. Manufacturers are increasingly developing customized CBE formulations tailored to specific climatic conditions and end-use applications.

Application Insights

Confectionery applications dominate the cocoa butter equivalent market, contributing approximately 62% of total global demand in 2025. Chocolate coatings, compound chocolates, chocolate spreads, and filled confectionery products remain the primary application areas due to the extensive use of specialty fats in industrial chocolate manufacturing. Bakery and frozen dessert applications are also expanding steadily as manufacturers increasingly use CBEs in icings, fillings, wafers, pastries, and ice cream coatings to improve texture and shelf-life performance. Cosmetic applications are emerging rapidly, particularly in plant-based skincare and lip-care formulations where specialty vegetable fats offer enhanced emollient functionality. Pharmaceutical usage is also gradually increasing in medicinal coatings and suppository formulations requiring stable melting characteristics.

Distribution Channel Insights

Direct B2B supply agreements dominate the distribution structure of the cocoa butter equivalent market, as large confectionery manufacturers typically procure specialty fats through long-term industrial contracts. Ingredient distributors also play an important role, particularly in emerging markets where mid-sized bakery and confectionery manufacturers rely on regional specialty ingredient suppliers. Online industrial ingredient platforms are gradually expanding as digital procurement systems become more common within the food processing industry. Specialty fat manufacturers are increasingly strengthening direct customer relationships through technical consulting services, formulation support, and customized product development programs. Supply-chain integration and reliable sourcing partnerships remain key competitive factors within global distribution networks.

End-Use Industry Insights

Industrial chocolate manufacturing represents the largest end-use segment within the cocoa butter equivalent market, accounting for nearly 48% of global consumption. Large confectionery manufacturers prefer CBEs because they reduce tempering complexity, improve heat resistance, and optimize production costs while maintaining desirable sensory properties. Bakery processing industries are also witnessing increasing demand for specialty fats in cream fillings, coated snacks, cookies, and pastries. The cosmetics and personal care sector is among the fastest-growing end-use industries, supported by rising demand for natural plant-based emollients and sustainable skincare ingredients. Pharmaceutical applications are gradually emerging as manufacturers seek stable vegetable fat-based excipients for medicinal delivery systems and temperature-sensitive formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Cocoa Butter Equivalent (CBE) Market Segmentations

By Product Type

- Cocoa Butter Equivalents (CBE)

- Cocoa Butter Replacers (CBR)

- Cocoa Butter Substitutes (CBS)

- Specialty Blended Vegetable Fats

By Source Oil/Fat

- Palm Oil

- Shea Butter

- Sal Fat

- Kokum Butter

- Mango Kernel Oil

- Illipe Fat

- Coconut Oil

- Palm Kernel Oil

By Application

- Confectionery

- Bakery & Desserts

- Dairy & Frozen Desserts

- Snacks & Convenience Foods

- Cosmetics & Personal Care

- Pharmaceuticals

By Processing Technology

- Fractionation

- Hydrogenation

- Interesterification

- Enzymatic Modification

- Blending & Formulation

By Distribution Channel

- Direct B2B Supply Contracts

- Ingredient Distributors

- Specialty Fat Suppliers

- Online Industrial Ingredient Platforms

Regional Insights

North America

North America accounts for approximately 22% of the global cocoa butter equivalent market, led primarily by the United States. Strong industrial confectionery production, growing demand for compound chocolates, and rising packaged snack consumption continue to support regional market growth. The U.S. remains a major consumer of specialty fats for bakery coatings, frozen desserts, and chocolate spreads. Mexico is emerging as an important regional manufacturing hub due to increasing confectionery exports and cost-efficient food processing infrastructure. Demand for clean-label and trans-fat-free specialty fats is also growing steadily across North America.

Europe

Europe dominates the global cocoa butter equivalent market with nearly 34% market share in 2025. Germany, Belgium, Switzerland, France, and the Netherlands remain key chocolate manufacturing centers with extensive demand for premium specialty fats. Germany leads regional consumption because of its strong industrial confectionery exports and advanced food processing industry. Belgium and Switzerland continue to drive innovation in premium chocolates requiring highly customized cocoa butter-compatible formulations. Sustainability regulations and strong consumer preference for ethically sourced ingredients are further accelerating adoption of certified specialty fats across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 9% during the forecast period. China and India are witnessing rapid growth in chocolate consumption due to urbanization, rising disposable incomes, and westernized dietary trends. Indonesia and Malaysia serve as major specialty fat production hubs because of their integrated palm oil industries and strong refining infrastructure. Japan and South Korea continue to contribute significantly to premium confectionery demand, particularly for high-quality chocolates and bakery applications. Expanding retail penetration and growing processed food manufacturing are expected to sustain long-term regional growth.

Latin America

Latin America represents a steadily growing market led by Brazil, Argentina, and Colombia. Brazil remains the largest regional consumer due to strong domestic confectionery demand and increasing industrial bakery production. The region is also benefiting from rising packaged snack consumption and improving retail distribution infrastructure. Manufacturers are increasingly utilizing cocoa butter equivalents in affordable premium chocolate products targeted at middle-income consumers. Export-oriented confectionery manufacturing is gradually supporting additional demand for specialty fats across Latin America.

Middle East & Africa

The Middle East & Africa region is experiencing rising demand for heat-resistant chocolate formulations and specialty confectionery fats. UAE and Saudi Arabia are major importers of premium confectionery ingredients due to expanding foodservice industries and strong luxury confectionery consumption. South Africa remains an important regional manufacturing center for bakery and chocolate products. In Africa, growing urbanization and rising processed food demand are gradually expanding industrial chocolate manufacturing capabilities. Climate conditions across the region also increase demand for CBEs that provide enhanced product stability during transportation and storage.

Key Players in the Cocoa Butter Equivalent Market

- Cargill Incorporated

- Bunge Global SA

- Fuji Oil Holdings Inc.

- AAK AB

- Wilmar International Limited

- Musim Mas Holdings

- IOI Corporation Berhad

- Mewah International Inc.

- Olam International

- 3F Industries Ltd.

- Intercontinental Specialty Fats Sdn. Bhd.

- Nisshin OilliO Group Ltd.

- ADM

- Premium Vegetable Oils Sdn. Bhd.

- Efko Group