Canned Espresso Market Size

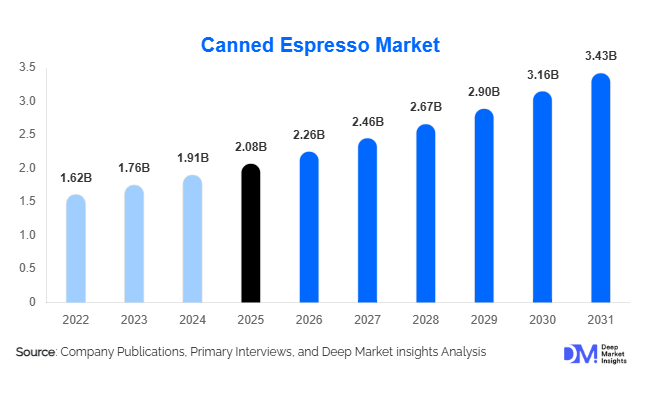

According to Deep Market Insights, the global canned espresso market size was valued at USD 2.08 billion in 2025 and is projected to grow from USD 2.26 billion in 2026 to reach USD 3.43 billion by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The canned espresso market growth is primarily driven by rising consumer demand for premium ready-to-drink (RTD) coffee beverages, increasing preference for convenient on-the-go caffeine consumption, and growing adoption of functional coffee products that combine energy enhancement with premium coffee experiences. The market is also benefiting from product innovations involving plant-based ingredients, low-sugar formulations, specialty coffee beans, and sustainable packaging solutions.

Key Market Insights

- Double-shot canned espresso products account for approximately 32% of global market revenue, making them the leading product category due to their optimal balance between caffeine content and flavor intensity.

- On-the-go consumption represents nearly 44% of total demand, supported by increasing urbanization, commuting populations, and fast-paced lifestyles.

- North America dominates the global canned espresso market with approximately 38% market share, led by strong premium coffee consumption trends in the United States.

- Asia-Pacific is the fastest-growing regional market, expanding at an estimated CAGR of over 11%, driven by growing coffee culture in China, India, South Korea, and Southeast Asia.

- Functional canned espresso beverages are gaining significant traction, incorporating ingredients such as protein, vitamins, adaptogens, nootropics, and performance-enhancing compounds.

- Sustainability initiatives are reshaping competitive positioning, with manufacturers increasingly investing in recyclable aluminum packaging, carbon-neutral sourcing, and ethically certified coffee beans.

Canned Espresso Market Latest Trends

Functional Coffee Innovation Accelerating Market Expansion

The convergence of canned espresso with the broader functional beverage sector has emerged as one of the strongest trends shaping industry growth. Manufacturers are increasingly introducing products infused with protein, collagen, vitamins, nootropics, adaptogens, and energy-supporting ingredients to meet evolving consumer demands. Consumers are increasingly seeking beverages that provide both immediate energy and long-term wellness benefits. Premium functional espresso beverages are commanding higher retail prices while generating stronger margins for producers. Brands targeting fitness enthusiasts, working professionals, and health-conscious consumers are expanding portfolios beyond traditional coffee products, positioning canned espresso as a multifunctional beverage category rather than simply a caffeine source.

Premiumization and Specialty Coffee Positioning

Consumers are increasingly demanding premium coffee experiences within ready-to-drink formats. This trend has accelerated investments in single-origin beans, specialty coffee sourcing, organic certifications, fair-trade procurement, and advanced extraction technologies. Premium canned espresso products featuring artisan roasting techniques and enhanced flavor complexity are gaining shelf space across retail channels globally. Companies are also leveraging limited-edition flavors, micro-lot coffee beans, and sustainability-focused branding to differentiate products. The trend is particularly strong among millennials and Gen Z consumers who value authenticity, transparency, and premium product experiences. As a result, specialty canned espresso products are consistently outperforming mainstream offerings in terms of revenue growth and consumer loyalty.

Canned Espresso Market Drivers

Growing Demand for Convenient Premium Coffee Solutions

The increasing adoption of convenience-focused lifestyles is a major driver of canned espresso market growth. Consumers are seeking coffee products that deliver café-quality experiences without preparation time or equipment requirements. Canned espresso products address this need by offering portability, shelf stability, and consistent taste profiles. Working professionals, students, commuters, and travelers increasingly rely on RTD coffee products to support busy daily schedules. The rapid expansion of convenience stores, vending networks, quick-commerce platforms, and e-commerce channels is further improving accessibility and supporting demand growth across developed and emerging markets.

Rising Popularity of Premium and Specialty Coffee Consumption

Global coffee consumption continues to shift toward premium and specialty products as consumers become more educated about coffee origins, roasting methods, and quality attributes. This premiumization trend has significantly benefited canned espresso manufacturers that offer high-quality coffee experiences in ready-to-drink formats. Specialty coffee positioning enables companies to command higher price points while building stronger brand differentiation. Growing consumer willingness to pay for premium ingredients, sustainable sourcing, and unique flavor experiences is expected to remain a significant growth catalyst throughout the forecast period.

Expansion of Functional Energy Beverage Alternatives

Many consumers are increasingly replacing traditional energy drinks with coffee-based beverages perceived as more natural and healthier. High-caffeine canned espresso products are directly benefiting from this substitution trend. Unlike conventional energy drinks, canned espresso beverages often offer cleaner ingredient labels, lower sugar content, and stronger consumer trust associated with coffee. Functional coffee innovations are further strengthening this market transition, particularly among younger demographics and fitness-oriented consumers.

Canned Espresso Market Restraints

Volatility in Coffee Bean and Raw Material Prices

Coffee bean pricing remains highly vulnerable to climate conditions, crop yields, geopolitical developments, and commodity market fluctuations. Arabica and robusta bean shortages can significantly impact production costs and profitability for canned espresso manufacturers. In addition to coffee beans, packaging materials such as aluminum cans have experienced periodic cost inflation. These pricing pressures create challenges for producers attempting to maintain margins while remaining competitive in increasingly crowded beverage categories.

Intense Competition from Alternative Beverage Categories

The canned espresso market faces strong competition from cold brew coffee, bottled coffee beverages, energy drinks, ready-to-drink tea, functional hydration products, and freshly prepared café beverages. The growing availability of alternative caffeinated beverages forces manufacturers to continuously innovate through new flavors, packaging formats, and functional ingredients. High promotional spending and frequent product launches increase competitive intensity, particularly within mature markets such as North America and Japan.

Canned Espresso Industry Key Opportunities

Expansion Across Emerging Asia-Pacific Coffee Markets

Asia-Pacific presents one of the largest untapped opportunities for canned espresso manufacturers. Countries such as China, India, Indonesia, Thailand, Vietnam, and the Philippines are experiencing rapid growth in coffee consumption driven by urbanization, rising disposable incomes, and evolving consumer preferences. Premium coffee products remain underpenetrated relative to developed markets, creating significant opportunities for both multinational corporations and emerging regional brands. Investments in local production, distribution partnerships, and digital retail channels are expected to support long-term expansion throughout the region.

Sustainability-Led Product Differentiation

Sustainability initiatives are becoming increasingly important purchasing criteria for consumers and retailers. Manufacturers investing in recyclable aluminum packaging, ethically sourced coffee beans, carbon-neutral production processes, and fair-trade certifications are well-positioned to capture premium market segments. Retailers are also prioritizing environmentally responsible products within beverage categories. Companies that successfully align sustainability commitments with product quality and brand messaging are expected to achieve stronger customer retention and premium pricing advantages.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.08 Billion |

| Market Size in 2026 | USD 2.26 Billion |

| Market Size in 2031 | USD 3.43 Billion |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Based on product type, the global canned espresso market is segmented into single-shot espresso, double-shot espresso, triple-shot and extra-strength espresso, espresso with milk, plant-based milk espresso, and functional espresso beverages. Among these, double-shot canned espresso dominates the global market, accounting for approximately 32% of total revenue in 2025. The segment’s leadership is primarily driven by its ability to deliver an optimal balance between caffeine intensity, flavor richness, and convenience, making it highly attractive to working professionals, students, commuters, and consumers seeking sustained energy without the excessive caffeine content associated with stronger formulations. Growing consumer preference for premium ready-to-drink (RTD) coffee beverages that combine convenience with authentic coffee experiences continues to strengthen demand for double-shot variants across both developed and emerging markets.Espresso with milk continues to represent a substantial share of global demand due to its broader consumer appeal, smoother taste profile, and accessibility among consumers transitioning from traditional coffee beverages to RTD formats. The segment benefits from strong demand among consumers seeking a less intense espresso experience while maintaining convenience and premium quality. Meanwhile, plant-based milk espresso products are witnessing robust growth as vegan, lactose-free, and flexitarian dietary preferences become increasingly mainstream. Rising consumer awareness regarding sustainability, animal welfare, and digestive health is encouraging the adoption of oat, almond, soy, and coconut-based espresso beverages.Functional espresso beverages infused with protein, vitamins, adaptogens, nootropics, collagen, and other wellness-focused ingredients represent one of the most dynamic and fastest-growing product categories within the market. Demand is being driven by consumers seeking multifunctional beverages that provide energy, cognitive support, nutritional benefits, and productivity enhancement in a single convenient format. As health-conscious consumption patterns continue to evolve globally, manufacturers are increasingly investing in innovation and product diversification within the functional espresso category.

Flavor Profile Insights

Based on flavor profile, the canned espresso market is categorized into original espresso, vanilla, mocha, caramel, seasonal and limited-edition flavors, and specialty flavors. Original espresso remains the leading flavor segment, accounting for approximately 38% of global market revenue in 2025. The dominance of this segment is driven by growing consumer preference for authentic coffee experiences that emphasize bean quality, roast characteristics, and natural flavor complexity rather than heavily sweetened beverage formulations. The premiumization trend within the coffee industry continues to support demand for original espresso products, particularly among coffee enthusiasts and specialty coffee consumers.Seasonal and limited-edition flavor offerings are becoming increasingly important for product differentiation and brand engagement. Manufacturers frequently introduce holiday-inspired, region-specific, and limited-run flavors to generate consumer excitement, encourage trial purchases, and stimulate repeat buying behavior. These offerings also enable brands to strengthen customer loyalty and maintain relevance in an increasingly competitive marketplace.Specialty flavors inspired by desserts, international coffee traditions, exotic ingredients, and premium culinary trends are contributing significantly to category innovation and premiumization. Growing consumer interest in unique taste experiences and artisanal beverage offerings is encouraging manufacturers to expand their flavor portfolios and target niche consumer segments seeking differentiated coffee products.

Distribution Channel Insights

Based on distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, e-commerce platforms, specialty coffee retailers, foodservice outlets, and vending machines. Supermarkets and hypermarkets account for approximately 35% of global canned espresso sales, making them the leading distribution channel in 2025. The segment’s dominance is driven by extensive product visibility, strong promotional capabilities, wide geographic reach, and consumers’ preference for one-stop shopping experiences. The ability of large retail chains to offer extensive product assortments, competitive pricing, and premium shelf placement continues to support market leadership.E-commerce platforms are emerging as one of the fastest-growing distribution channels within the market. Growth is supported by expanding direct-to-consumer strategies, subscription-based purchasing models, personalized product recommendations, and the rapid development of quick-commerce delivery services. Online channels also provide manufacturers with valuable consumer insights while enabling broader access to premium and niche product offerings.Specialty coffee retailers and foodservice operators continue to play a vital role in premium product positioning and consumer education. These channels help introduce innovative products, support brand credibility, and attract consumers seeking specialty coffee experiences. Meanwhile, vending machines are experiencing renewed growth due to advancements in smart retail technologies, digital payment systems, and automated beverage dispensing solutions that enhance accessibility and convenience.

Consumer Age Group Insights

Based on consumer age group, the canned espresso market is segmented into 18–24 years, 25–34 years, 35–44 years, 45–54 years, and 55 years and above. Consumers aged 25–34 years represent the largest customer segment within the global canned espresso market. The leadership of this demographic is primarily attributed to strong purchasing power, busy lifestyles, high workforce participation, and a willingness to spend on premium convenience beverages. This consumer group demonstrates strong affinity for premium RTD coffee products that offer convenience, functional benefits, and café-quality experiences in portable formats.Consumers aged 35–44 years remain significant contributors to overall market revenue due to established workplace consumption habits and a growing preference for premium and specialty coffee products. Demand within this segment is supported by increasing focus on convenience, product quality, and premium ingredients that align with professional lifestyles.Older consumer groups increasingly favor low-sugar, organic, clean-label, and specialty coffee formulations that support broader health and wellness objectives. Growing awareness regarding nutrition, ingredient transparency, and sustainable sourcing is encouraging manufacturers to develop products tailored to the preferences of mature consumers. As a result, companies are increasingly refining product positioning, packaging formats, and flavor portfolios to address the unique needs of each age demographic.

End-Use Insights

Based on end use, the market is segmented into individual consumers, corporate offices, hospitality venues, fitness centers and sports facilities, and educational institutions. Individual consumers account for approximately 72% of global canned espresso demand, making them the dominant end-use segment in 2025. The segment’s leadership is driven by growing consumer preference for convenient, premium, and ready-to-drink coffee solutions that fit increasingly fast-paced lifestyles. Rising demand among professionals, students, commuters, and remote workers continues to support strong consumption volumes across both developed and emerging markets.Hospitality venues, including hotels, airports, railway stations, travel centers, and entertainment facilities, are rapidly expanding canned espresso offerings to meet rising demand for premium grab-and-go beverages. Increasing travel activity and consumer preference for convenient refreshment options are supporting growth within this segment.Fitness centers and sports facilities are emerging as attractive growth areas due to increasing consumer preference for coffee-based energy solutions as alternatives to traditional energy drinks. Growing awareness of caffeine’s role in athletic performance, endurance, and mental focus is further supporting demand. Educational institutions are also expanding canned espresso availability as universities and colleges seek to accommodate evolving beverage preferences among students, faculty, and staff.

Explore more data points, trends and opportunities Download Free Sample Report

Canned Espresso Market Segmentations

By Product Type

- Single-Shot Canned Espresso

- Double-Shot Canned Espresso

- Triple-Shot & Extra-Strength Canned Espresso

- Espresso with Milk

- Espresso with Plant-Based Milk

- Black Unsweetened Espresso

- Sweetened Espresso

- Functional Espresso

By Flavor Profile

- Original Espresso

- Vanilla

- Mocha/Chocolate

- Caramel

- Hazelnut

- Seasonal/Limited Edition Flavors

- Other Specialty Flavors

By Sugar Formulation

- Regular Sugar

- Reduced Sugar

- Sugar-Free/Zero-Calorie

By Caffeine Content

- Standard Caffeine

- High-Caffeine

- Decaffeinated

By Ingredient Positioning

- Conventional

- Organic

- Fair Trade Certified

- Specialty Coffee/Single-Origin

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 38% of global canned espresso revenue in 2025. The region’s leadership is supported by high per-capita coffee consumption, a well-established ready-to-drink beverage industry, strong consumer purchasing power, and widespread availability of premium coffee products across modern retail channels. The United States dominates regional demand with nearly 82% of North American consumption, benefiting from a mature coffee culture, strong brand presence, extensive convenience retail infrastructure, and growing consumer interest in functional and premium RTD coffee beverages.Regional growth is being driven by increasing demand for convenient caffeine solutions among busy professionals, rising adoption of premium and specialty coffee products, growing consumer preference for clean-label and functional beverages, and continuous product innovation by leading beverage manufacturers. Expansion of e-commerce channels, subscription-based beverage purchasing, and the increasing popularity of high-protein and wellness-focused coffee beverages are further supporting market growth. Canada continues to exhibit strong demand for specialty coffee products, while Mexico is emerging as a promising growth market due to rapid urbanization, expanding middle-class populations, and evolving coffee consumption habits.

Europe

Europe accounts for approximately 23% of global canned espresso demand and represents one of the most established coffee consumption markets worldwide. Germany, the United Kingdom, France, Italy, and Spain remain the primary revenue-generating countries within the region. Strong coffee traditions, increasing premiumization, and rising consumer demand for convenience-oriented beverage formats continue to support market expansion.Regional growth is driven by growing demand for sustainably sourced coffee products, increasing consumer preference for organic and fair-trade beverages, rising adoption of premium RTD coffee formats, and heightened focus on ethical sourcing practices. Consumers across Western and Northern Europe increasingly prioritize product quality, traceability, and environmental responsibility when making purchasing decisions. Additionally, expanding urban lifestyles, busy work schedules, and the growing popularity of grab-and-go beverage consumption are accelerating demand for canned espresso products across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of global market revenue and represents the fastest-growing regional market, expanding at an estimated CAGR exceeding 11% during the forecast period. The region benefits from a rapidly expanding consumer base, increasing urbanization, rising disposable incomes, and significant shifts in beverage consumption preferences toward premium coffee products. Japan remains the world's largest canned coffee market and contributes more than one-third of regional demand, supported by a deeply established vending machine culture and long-standing consumer acceptance of canned coffee products.Regional growth is being fueled by increasing coffee adoption among younger consumers, rapid expansion of café culture, rising exposure to Western beverage trends, growing demand for premium convenience beverages, and expanding retail and e-commerce infrastructure. China continues to experience substantial growth due to increasing coffee consumption among urban professionals and middle-income consumers. India is emerging as the fastest-growing national market, supported by rising disposable incomes, expanding café chains, growing awareness of specialty coffee, and increasing demand for convenient energy beverages. South Korea, Australia, Indonesia, Thailand, Vietnam, and other Southeast Asian markets continue to provide significant opportunities as coffee consumption becomes increasingly mainstream across the region.

Latin America

Latin America accounts for approximately 6% of global canned espresso revenue and presents attractive long-term growth potential due to its strong coffee heritage and expanding RTD beverage sector. Brazil remains the largest market within the region, supported by high coffee consumption levels, growing demand for premium beverages, and increasing product innovation among domestic and international brands.Regional growth is driven by rising urbanization, increasing disposable incomes, expanding modern retail networks, growing awareness of premium ready-to-drink coffee products, and changing consumer lifestyles that favor convenient beverage solutions. Mexico and Argentina are also contributing significantly to regional expansion as younger consumers increasingly adopt premium coffee products and international beverage trends. Improved product availability across supermarkets, convenience stores, and online retail channels is expected to further strengthen market penetration throughout the forecast period.

Middle East & Africa

The Middle East & Africa region represents approximately 4% of global canned espresso demand and is gradually emerging as a promising market for premium ready-to-drink coffee products. The United Arab Emirates and Saudi Arabia serve as key growth centers due to strong consumer spending on premium beverages, expanding café culture, and well-developed modern retail infrastructure. South Africa remains an important market within the African region, supported by increasing consumer interest in specialty coffee products.Regional growth is being driven by rapid urbanization, rising disposable incomes, growing influence of Western coffee consumption trends, expanding convenience retail networks, and increasing demand for premium on-the-go beverage options. Investments in modern retail development, growth in travel and tourism activities, and rising penetration of international coffee brands are creating favorable conditions for market expansion. Additionally, younger consumer populations and increasing adoption of premium lifestyle products are expected to support sustained demand growth across the region over the coming years.

Key Players in the Canned Espresso Market

- Starbucks Corporation

- Suntory Holdings

- Nestlé SA

- La Colombe Coffee Roasters

- Black Rifle Coffee Company

- High Brew Coffee

- Super Coffee

- Peet's Coffee

- illycaffè

- UCC Ueshima Coffee

- Costa Coffee

- Blue Bottle Coffee

- Chameleon Organic Coffee

- Stumptown Coffee Roasters

- Westrock Coffee