Cannabis Soaked Beverage Market Size

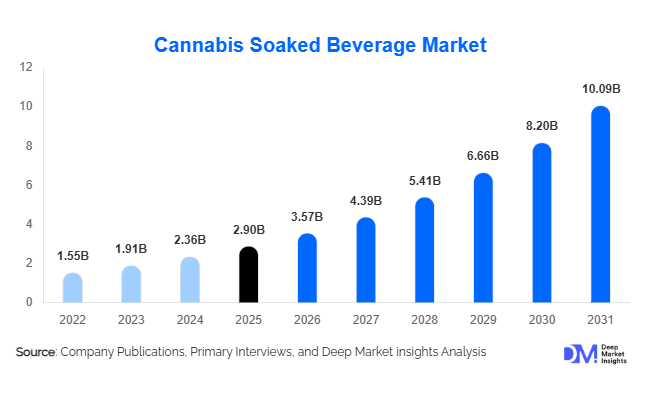

According to Deep Market Insights, the global cannabis soaked beverage market size was valued at approximately USD 2.35 billion in 2025 and is projected to grow from USD 3.57 billion in 2026 to reach USD 10.09 billion by 2031, expanding at a CAGR of 23.1% during the forecast period (2026–2031). The cannabis soaked beverage market growth is primarily driven by the increasing legalization of cannabis for both medicinal and recreational use, rising consumer preference for smoke-free cannabis consumption, and the growing popularity of functional beverages that offer relaxation, wellness, and stress-management benefits. Technological advancements in nano-emulsification and water-soluble cannabinoid formulations have significantly improved product taste, bioavailability, and onset time, making cannabis beverages increasingly appealing to mainstream consumers.

Key Market Insights

- Cannabis beverages are increasingly replacing alcoholic beverages in social settings, particularly among millennials and Gen Z consumers seeking healthier alternatives.

- CBD-infused beverages dominate the market, accounting for more than 60% of global demand due to broader regulatory acceptance and wellness-oriented applications.

- North America remains the largest market, representing nearly three-fourths of global revenues due to mature cannabis regulations and extensive product innovation.

- Asia-Pacific is expected to witness the fastest growth, supported by evolving medical cannabis regulations and rising consumer awareness regarding functional wellness products.

- Nano-emulsification technology is transforming product formulations, enabling faster absorption, enhanced bioavailability, and improved consumer experiences.

- Functional and low-dose cannabis beverages are emerging as key growth segments, appealing to first-time users and wellness-conscious consumers.

Cannabis Soaked Beverage Market Latest Trends

Low-Dose and Social Wellness Beverages Gaining Popularity

The cannabis beverage industry is witnessing strong demand for low-dose products containing less than 5 mg of THC per serving. Consumers increasingly prefer beverages that provide mild relaxation and mood enhancement without the intoxicating effects associated with higher cannabis doses. Beverage manufacturers are introducing microdose products targeted toward social occasions and alcohol substitution. This trend is particularly prominent among younger consumers who are seeking healthier and lower-calorie alternatives to alcoholic drinks. Premium cannabis mocktails, sparkling waters, and botanical infusions are increasingly being positioned as social wellness products, thereby expanding the addressable consumer base beyond traditional cannabis users.

Advanced Formulation Technologies Enhancing Consumer Experience

Manufacturers are increasingly adopting nano-emulsification and water-soluble technologies to improve cannabinoid delivery and product stability. These technologies significantly reduce onset times from more than one hour to approximately 10–20 minutes while improving taste profiles and dosage consistency. Companies are also investing heavily in flavor masking technologies and precision dosing systems to attract mainstream consumers. Functional formulations incorporating adaptogens, vitamins, electrolytes, and botanical ingredients alongside cannabinoids are becoming increasingly common, supporting the convergence of the cannabis and functional beverage industries.

Cannabis Soaked Beverage Market Drivers

Increasing Cannabis Legalization Worldwide

The expanding legalization of medical and recreational cannabis remains the most significant growth driver for the market. North America continues to lead regulatory reforms, while Europe and Latin America are gradually liberalizing cannabis regulations. New regulatory approvals are creating opportunities for manufacturers to enter previously untapped markets and expand product portfolios. Growing acceptance of cannabis consumption is also reducing social stigma and increasing consumer adoption across various demographics.

Growing Demand for Smoke-Free Cannabis Consumption

Consumers are increasingly shifting toward smoke-free and discreet cannabis consumption methods. Cannabis beverages provide controlled dosing, ease of consumption, and improved convenience compared to smoking and vaping products. The beverage format also attracts first-time users and wellness-oriented consumers who may not be comfortable with traditional cannabis products. This trend has substantially broadened the consumer base and contributed to the rapid growth of infused beverage categories.

Rising Consumer Preference for Functional Wellness Products

The functional beverage industry is experiencing significant growth globally, and cannabis beverages are benefiting from this trend. Consumers increasingly seek products that support relaxation, stress reduction, sleep enhancement, and overall well-being. CBD-infused beverages, in particular, have gained popularity among health-conscious consumers due to their perceived therapeutic benefits and non-intoxicating nature.

Cannabis Soaked Beverage Market Restraints

Regulatory Fragmentation and Compliance Challenges

The regulatory landscape governing cannabis beverages varies considerably across countries and states, creating significant compliance challenges for manufacturers. Restrictions on THC content, packaging, labeling, and marketing continue to complicate market expansion and increase operational costs.

High Production and Manufacturing Costs

The production of cannabis beverages requires specialized extraction technologies, extensive laboratory testing, and advanced formulation techniques. High compliance requirements and quality assurance standards increase manufacturing expenses and may limit profitability, particularly for smaller market participants.

Cannabis Soaked Beverage Industry Key Opportunities

Alcohol Replacement and Social Consumption Trends

One of the largest opportunities in the market lies in the increasing substitution of alcohol with cannabis beverages. Younger consumers increasingly prefer products that provide relaxation without the adverse health effects associated with alcohol consumption. Premium cannabis mocktails, sparkling beverages, and low-dose products are emerging as attractive alternatives in social settings. Beverage manufacturers that successfully position cannabis products as social wellness beverages are expected to capture substantial market share in the coming years.

Expansion into Newly Legalized Markets

Several countries and regions are progressively liberalizing cannabis regulations, creating substantial opportunities for market participants. Germany's cannabis reforms, expanding medical cannabis access across Europe, and evolving regulations in Latin America and Asia-Pacific are expected to significantly increase market demand. Early market entrants are likely to benefit from first-mover advantages, including brand recognition and distribution network development.

Functional and Personalized Cannabis Beverages

The integration of cannabinoids with vitamins, adaptogens, nootropics, and herbal ingredients represents a significant opportunity for product differentiation. Personalized formulations targeting sleep, energy, focus, recovery, and stress management are expected to create new revenue streams and attract wellness-oriented consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.90 Billion |

| Market Size in 2026 | USD 3.57 Billion |

| Market Size in 2031 | USD 10.09 Billion |

| CAGR | 23.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Non-alcoholic cannabis beverages dominate the global market, accounting for nearly 69% of total revenues in 2025, primarily driven by their alignment with health-conscious consumption trends and expanding legalization frameworks. Cannabis-infused sparkling waters represent the leading product category within this segment, supported by their low-calorie profile, clean-label positioning, and strong appeal among first-time and wellness-oriented consumers seeking a familiar beverage format with functional benefits. The growth of sparkling waters is further reinforced by rapid product innovation, improved flavor masking technologies, and increasing retail placement in both cannabis dispensaries and mainstream beverage channels where permitted. Cannabis teas and functional wellness beverages are also gaining traction as consumers increasingly prioritize hydration combined with relaxation, stress relief, and sleep support benefits. Cannabis-infused alcoholic beverages remain a niche but emerging category, largely constrained by regulatory limitations, although they are gradually expanding in select hybrid markets where cannabinoid-alcohol combinations are permitted. Functional wellness shots and premium cannabis mocktails are emerging as high-margin subsegments, driven by urban consumers seeking sophisticated, on-the-go consumption formats that integrate seamlessly into modern wellness lifestyles.

Cannabinoid Composition Insights

CBD-dominant beverages accounted for approximately 63% of global demand in 2025, maintaining their leadership position due to their non-psychoactive properties, broad regulatory acceptance, and strong association with wellness and relaxation use cases. The dominance of CBD formulations is further supported by their versatility across consumer segments, including first-time users, wellness-focused consumers, and medical patients seeking non-intoxicating alternatives. THC-infused beverages represent the second-largest category and are expanding steadily, driven by increasing legalization and growing consumer preference for controlled, discreet, and smoke-free recreational experiences. Balanced THC:CBD formulations are gaining momentum as they offer a synergistic effect that appeals to consumers seeking both therapeutic benefits and mild psychoactive effects, particularly in stress relief and mood enhancement applications. Minor cannabinoid beverages, including CBG and CBN-based products, remain an emerging frontier, with growing investment in sleep-support and recovery-focused formulations that target specialized wellness needs and premium positioning within the functional beverage landscape.

Distribution Channel Insights

Licensed cannabis dispensaries accounted for approximately 43% of global revenues in 2025 and continue to dominate distribution due to strict regulatory frameworks governing cannabinoid products in most legal markets. Their leadership is reinforced by controlled product access, consumer education, and curated product assortments that enhance trust and compliance. E-commerce and direct-to-consumer platforms are among the fastest-growing channels, driven by increasing digital adoption, regulatory relaxation in select jurisdictions, and consumer preference for discreet and convenient purchasing experiences. Specialty wellness stores and pharmacies are expanding their presence in the CBD beverage segment as demand for functional health products increases, particularly among consumers seeking non-recreational applications of cannabinoids. Supermarkets and convenience stores are expected to play a significantly larger role in the long term as regulatory normalization progresses, enabling broader mainstream acceptance and improved product accessibility for mass-market consumers.

Consumer Type Insights

Recreational consumers remain the largest end-user group, supported by expanding legalization and growing cultural acceptance of cannabis-infused beverages as a social and lifestyle-oriented alternative to traditional alcoholic drinks. The dominance of this segment is reinforced by increasing product availability, improved taste profiles, and the rising popularity of controlled-dose consumption formats. Wellness-oriented consumers represent one of the fastest-growing segments, driven by heightened awareness of stress management, sleep improvement, and natural health solutions, with CBD beverages playing a central role in daily wellness routines. Medical cannabis consumers continue to contribute stable demand, particularly in regions with established medical cannabis frameworks, where beverages are increasingly used for pain management, anxiety reduction, and chronic condition support. First-time users are also a key growth driver, as beverages are widely perceived as more approachable, familiar, and easier to dose compared to traditional cannabis consumption methods, significantly lowering barriers to entry.

End-Use Insights

Household consumption accounts for approximately 55% of global demand, supported by the growing trend of at-home wellness routines and recreational consumption, particularly in regions with established legalization. The dominance of this segment is driven by convenience, privacy, and the increasing integration of cannabis beverages into relaxation and self-care practices. Hospitality and food-service applications represent one of the fastest-growing end-use categories, fueled by the emergence of cannabis lounges, infused dining experiences, and experiential consumption venues that are reshaping social beverage culture in legalized markets. Wellness centers and spas are increasingly incorporating CBD beverages into holistic treatment programs, leveraging their calming and recovery-enhancing properties to complement therapeutic services. Medical and therapeutic applications are also expanding steadily, supported by growing clinical research and increasing physician acceptance of cannabinoid-based interventions for pain, anxiety, and sleep-related disorders, further strengthening the role of beverages as a functional delivery format in healthcare contexts.

Explore more data points, trends and opportunities Download Free Sample Report

Cannabis Soaked Beverage Market Segmentations

By Cannabinoid Composition

- THC-Dominant Beverages

- CBD-Dominant Beverages

- Balanced THC:CBD Beverages

- Minor Cannabinoid Beverages

By Product Type

- Cannabis-Infused Sparkling Water

- Cannabis-Infused Carbonated Soft Drinks

- Cannabis Tea and Herbal Drinks

- Cannabis Coffee and Ready-to-Drink Coffee

- Cannabis Energy Drinks

- Cannabis Sports and Recovery Drinks

- Cannabis Juices and Smoothies

- Cannabis Functional Wellness Shots

- Cannabis Mocktails and Cocktail Mixers

- Cannabis Alcoholic Beverages

By Functional Positioning

- Relaxation and Stress Relief

- Sleep and Recovery

- Pain Management

- Mood Enhancement

- Social Consumption and Recreation

- Energy and Focus

- General Wellness and Preventive Health

By Source of Cannabis Extract

- Hemp-Derived Beverages

- Marijuana-Derived Beverages

By Formulation Technology

- Nano-Emulsified Beverages

- Water-Soluble Formulations

- Conventional Oil-Based Infusions

- Encapsulated Cannabinoid Technology

Regional Insights

North America

North America accounted for approximately 74% of global cannabis beverage revenues in 2025, maintaining its dominance due to early legalization, strong consumer awareness, and highly developed product innovation ecosystems. The United States leads regional growth, driven by expanding state-level legalization, a mature retail infrastructure, and continuous investment in beverage formulation technologies that improve taste, stability, and dosing precision. Canada also plays a significant role, supported by its federally regulated cannabis market, well-established supply chains, and early adoption of infused beverage products. Growth in the region is further driven by increasing mainstream retail acceptance, strong venture capital investment in cannabis innovation, and evolving consumer preferences toward smoke-free and wellness-oriented consumption formats.

Europe

Europe accounted for approximately 10% of global revenues in 2025 and is emerging as a high-potential growth region driven by progressive regulatory reforms and rising consumer interest in CBD-based wellness products. Germany leads regional expansion due to ongoing cannabis policy reforms, increasing medical cannabis adoption, and growing acceptance of functional cannabinoid beverages. The United Kingdom, Switzerland, and the Netherlands are also witnessing strong demand growth, particularly in CBD-infused beverages positioned within wellness, relaxation, and lifestyle segments. Regional growth is primarily driven by increasing regulatory clarity, expanding retail availability, and rising consumer awareness of plant-based wellness alternatives, supported by a strong pharmaceutical and health-focused retail ecosystem.

Asia-Pacific

Asia-Pacific currently accounts for around 7% of global demand but is projected to record the fastest growth rate over the forecast period, driven by gradual regulatory liberalization and increasing consumer awareness of cannabinoid-based wellness products. Australia and Thailand are leading markets due to progressive medical cannabis frameworks and expanding clinical acceptance of cannabinoid therapies. Emerging markets such as India, Japan, and South Korea are witnessing rising interest in functional wellness beverages as middle-class populations expand and disposable incomes increase. Regional growth is strongly supported by a shift toward preventive healthcare, increasing demand for natural wellness solutions, and growing investment in cannabinoid research and product development, positioning Asia-Pacific as a key long-term expansion hub.

Latin America

Latin America accounted for approximately 6% of global revenues in 2025, with growth driven by favorable agricultural conditions, evolving regulatory environments, and increasing investment in cannabis cultivation and processing infrastructure. Brazil, Mexico, and Colombia are emerging as key markets, supported by expanding medical cannabis frameworks and growing interest in export-oriented production capabilities. Regional growth is further fueled by cost-efficient production advantages, rising domestic acceptance of cannabinoid wellness products, and increasing participation from global cannabis companies seeking scalable cultivation and manufacturing bases.

Middle East & Africa

The Middle East and Africa represented nearly 3% of global demand in 2025, with growth concentrated in medically regulated and research-driven markets. Israel leads the region due to its advanced medical cannabis research ecosystem and strong pharmaceutical integration of cannabinoid-based therapies. South Africa is also emerging as a key market supported by progressive medical cannabis regulations and growing interest in therapeutic applications. Regional growth is driven by increasing clinical research investment, gradual regulatory liberalization in select countries, and expanding recognition of cannabinoid-based treatments in pain management and chronic disease care, creating a foundation for long-term market development.

Key Players in the Cannabis Soaked Beverage Market

- Canopy Growth Corporation

- Tilray Brands Inc.

- Curaleaf Holdings Inc.

- Trulieve Cannabis Corp.

- Green Thumb Industries Inc.

- Aurora Cannabis Inc.

- Cronos Group Inc.

- Village Farms International Inc.

- SNDL Inc.

- Jones Soda Co.

- Keef Brands

- Cann Social Tonics

- Vertosa Inc.

- Organigram Holdings Inc.

- Aphria Inc.