Black Coffee Market Size

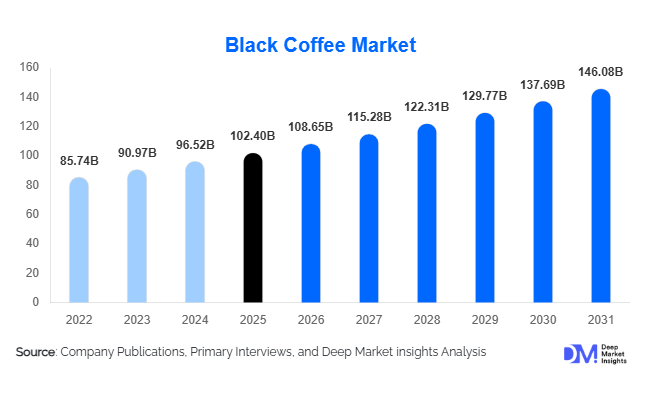

According to Deep Market Insights, the global black coffee market size was valued at USD 102.4 billion in 2025 and is projected to grow from USD 108.65 billion in 2026 to reach USD 146.08 billion by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The black coffee market growth is primarily driven by rising consumer preference for healthier beverage choices, increasing demand for premium and specialty coffee products, growing café culture across emerging economies, and expanding adoption of black coffee among fitness-conscious consumers. The market continues to benefit from strong consumption in developed economies while witnessing rapid expansion in Asia-Pacific countries where urbanization, changing lifestyles, and increasing disposable income are accelerating coffee consumption. Growing investments in specialty coffee roasting, sustainable sourcing programs, direct-to-consumer sales channels, and ready-to-drink black coffee products are further supporting market growth globally.

Key Market Insights

- Health-conscious consumers are increasingly shifting toward black coffee consumption, driven by its low-calorie profile, antioxidant content, and compatibility with fitness and wellness lifestyles.

- Specialty and premium coffee segments continue gaining market share, supported by growing demand for single-origin, artisanal, and ethically sourced coffee products.

- North America dominates the global black coffee market, accounting for approximately 31% of global revenue, led by strong consumption in the United States.

- Asia-Pacific remains the fastest-growing regional market, supported by rising demand in China, India, South Korea, Vietnam, and Indonesia.

- At-home coffee consumption continues expanding globally, driven by hybrid work models and increasing ownership of advanced coffee brewing equipment.

- Digital commerce and subscription-based coffee sales are transforming distribution channels, enabling brands to strengthen customer retention and improve profitability.

Black Coffee Market Latest Trends

Premium and Specialty Coffee Demand Accelerating

The black coffee industry is experiencing significant premiumization as consumers increasingly prioritize quality, flavor complexity, sustainability, and traceability over price. Specialty coffee products, including single-origin beans, micro-lot production, and direct-trade coffee offerings, are witnessing robust growth across North America, Europe, Japan, South Korea, and emerging urban markets in Asia-Pacific. Consumers are demonstrating greater willingness to pay premium prices for differentiated coffee experiences that offer superior taste profiles and transparent sourcing practices. Specialty coffee cafés, artisanal roasters, and independent brands are expanding globally, contributing to increased value generation across the market. In addition, certifications such as Fair Trade, Organic, and Rainforest Alliance are becoming important purchase considerations, particularly among younger demographics seeking ethically produced products.

Growth of Ready-to-Drink and Functional Black Coffee

Ready-to-drink (RTD) black coffee products are emerging as one of the fastest-growing categories within the market. Consumers increasingly seek convenient beverage options that align with busy lifestyles while maintaining health and wellness goals. Manufacturers are introducing functional black coffee products containing added protein, adaptogens, vitamins, nootropics, and natural energy-enhancing ingredients. The combination of convenience, portability, and wellness positioning is expanding black coffee consumption beyond traditional coffee-drinking occasions. RTD black coffee products are particularly popular among urban professionals, students, and fitness enthusiasts seeking healthier alternatives to carbonated soft drinks and energy beverages.

Black Coffee Market Drivers

Growing Health and Wellness Awareness

The increasing focus on preventive healthcare, fitness, and weight management is significantly driving black coffee consumption globally. Consumers are actively reducing sugar intake and replacing calorie-dense beverages with healthier alternatives. Black coffee's naturally low-calorie composition, antioxidant properties, and perceived metabolic benefits make it an attractive choice among health-conscious consumers. The growing popularity of intermittent fasting, ketogenic diets, and fitness-oriented lifestyles has further strengthened black coffee demand. As consumers become increasingly aware of the health implications associated with sugary beverages, black coffee continues gaining traction as a functional daily beverage.

Expansion of Global Café Culture

The rapid expansion of coffee chains and independent cafés continues to drive market growth worldwide. International brands and local specialty coffee operators are increasing investments in emerging economies, particularly across Asia-Pacific and the Middle East. Café culture is becoming deeply integrated into urban lifestyles, creating demand for premium black coffee beverages and specialty brewing methods. Increased consumer exposure to espresso-based black coffee, pour-over coffee, cold brew, and single-origin offerings is encouraging more frequent consumption and higher spending across the market. The proliferation of modern coffee shops is also educating consumers about quality, roasting techniques, and coffee origins.

Black Coffee Market Restraints

Volatility in Green Coffee Bean Prices

One of the most significant challenges facing the black coffee industry is fluctuating green coffee bean prices. Climate variability, extreme weather events, drought conditions, and crop diseases in major producing countries such as Brazil and Vietnam can significantly affect coffee yields and supply availability. These factors contribute to substantial price volatility, creating margin pressures for roasters, retailers, and foodservice operators. Rising input costs often force companies to increase retail prices, which may affect consumption patterns in price-sensitive markets.

Climate Change and Supply Chain Risks

Coffee cultivation remains highly sensitive to environmental conditions. Climate change is altering growing regions, affecting crop productivity, and increasing the frequency of extreme weather events. Sustainability requirements and environmental regulations are also increasing operational costs across the value chain. Producers must invest in climate-resilient farming practices, water conservation technologies, and sustainable agricultural methods to ensure long-term supply security. These challenges create uncertainty regarding future coffee production and industry profitability.

Black Coffee Industry Key Opportunities

Expansion Across Emerging Asia-Pacific Markets

Asia-Pacific represents the most significant growth opportunity within the global black coffee market. Countries including China, India, Vietnam, Indonesia, Thailand, and the Philippines are witnessing rapid growth in coffee consumption due to urbanization, rising disposable incomes, and westernization of consumer preferences. Coffee penetration remains substantially lower than mature markets, creating considerable headroom for future growth. International coffee chains, specialty roasters, and packaged coffee manufacturers continue investing aggressively across the region to capture emerging demand. Localized product offerings, regional roasting facilities, and digital sales channels are expected to support long-term market expansion.

Technology-Enabled Direct-to-Consumer Coffee Models

Digital commerce is creating substantial opportunities for coffee brands to improve customer engagement and profitability. Subscription-based coffee delivery services, AI-driven personalization platforms, and mobile commerce applications are helping companies build direct relationships with consumers. These models generate valuable consumer insights while reducing dependence on traditional retail channels. Companies adopting advanced analytics, customer loyalty programs, and automated replenishment services can enhance retention rates and strengthen recurring revenue streams. Technology-driven direct-to-consumer strategies are becoming increasingly important competitive differentiators across the industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 102.40 Billion |

| Market Size in 2026 | USD 108.65 Billion |

| Market Size in 2031 | USD 146.08 Billion |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Format Insights

The black coffee market is segmented by product format into ground black coffee, whole bean coffee, instant black coffee, coffee pods and capsules, and ready-to-drink (RTD) black coffee. Among these, ground black coffee continues to dominate the global market, accounting for approximately 34% of total revenue in 2025. The segment’s leadership is primarily driven by its affordability, widespread retail availability, ease of preparation, and compatibility with a broad range of brewing methods including drip coffee makers, French presses, pour-over systems, and espresso machines. Its strong presence across supermarkets, hypermarkets, convenience stores, and online channels further supports sustained consumer adoption. In addition, the growing preference for at-home coffee consumption and daily routine coffee drinking continues to reinforce demand for ground black coffee across both developed and emerging economies.Coffee pods and capsules continue expanding steadily, supported by rising adoption of single-serve brewing systems in households and workplaces. Consumers increasingly value the convenience, consistency, portion control, and minimal preparation time offered by pod-based formats. Premium coffee brands are further strengthening the segment through expanded flavor portfolios, sustainable capsule innovations, and compatibility with a growing range of brewing machines.Ready-to-drink black coffee is emerging as one of the fastest-growing product categories globally. Growth is being fueled by increasing demand for convenient, on-the-go beverages, particularly among younger consumers and urban professionals. Rising interest in functional beverages, cold brew coffee, low-calorie refreshment options, and premium packaged drinks is accelerating category adoption. Product innovation in areas such as organic formulations, clean-label ingredients, enhanced caffeine content, and functional health benefits continues to support strong growth prospects for RTD black coffee worldwide.

Coffee Bean Type Insights

Based on coffee bean type, the market is categorized into Arabica, Robusta, Arabica-Robusta blends, and specialty or single-origin coffee varieties. Arabica black coffee dominates the global market, accounting for approximately 61% of total revenue in 2025. The segment’s leading position is primarily driven by strong consumer preference for smoother flavor profiles, lower bitterness levels, pleasant aroma characteristics, and superior cup quality. Arabica beans are extensively used across premium, specialty, and gourmet coffee categories, making them the preferred choice among consumers seeking higher-quality coffee experiences. Growing demand for premiumization, specialty beverages, and ethically sourced coffee products continues to strengthen Arabica's market leadership.Arabica-Robusta blends continue gaining popularity as manufacturers seek to balance taste quality, caffeine intensity, and pricing competitiveness. These blends enable producers to achieve greater consistency while meeting diverse consumer preferences across different markets. The growing popularity of espresso-based beverages and value-premium product offerings is further supporting segment growth.Specialty and single-origin coffees are witnessing rapid expansion as consumers increasingly prioritize authenticity, traceability, sustainability, and unique regional flavor characteristics. Growing awareness of coffee origins, direct-trade sourcing practices, and premium coffee craftsmanship is encouraging consumers to explore differentiated products. The expansion of specialty coffee shops, artisan roasters, and educational coffee experiences is expected to further strengthen demand for specialty and single-origin offerings during the forecast period.

Distribution Channel Insights

The black coffee market is distributed through supermarkets and hypermarkets, specialty coffee stores, online retail channels, direct-to-consumer platforms, and foodservice establishments. Supermarkets and hypermarkets remain the leading distribution channel, accounting for approximately 32% of global sales in 2025. The segment’s dominance is driven by extensive product assortments, strong consumer foot traffic, competitive pricing strategies, convenient product accessibility, and the ability to compare multiple brands within a single shopping destination. Retail chains also support market growth through promotional campaigns, private-label offerings, and expanding shelf space dedicated to coffee products.Online retail channels are experiencing robust growth as consumers increasingly purchase coffee through e-commerce platforms, digital marketplaces, and subscription-based services. Convenience, wider product availability, personalized recommendations, recurring delivery options, and access to niche specialty brands are supporting channel expansion. The growing influence of digital commerce and mobile shopping is expected to further accelerate online coffee sales over the coming years.Direct-to-consumer sales models are becoming increasingly important for coffee manufacturers and specialty roasters seeking stronger customer engagement, improved profit margins, and greater control over brand positioning. Subscription programs, customized coffee selections, and direct sourcing narratives are helping brands build long-term consumer loyalty.Foodservice distribution continues to represent a major sales channel due to expanding demand from cafés, restaurants, hotels, corporate offices, educational institutions, and hospitality establishments. Increasing consumer preference for premium coffee experiences outside the home and the expansion of global café chains continue to support sustained growth across the foodservice segment.

End-Use Insights

Based on end use, the market is segmented into residential consumers, cafés and coffee chains, hotels and restaurants, corporate offices, and institutional establishments. Residential consumers represent the largest end-use segment, accounting for approximately 48% of total market value in 2025. The segment’s leadership is primarily driven by increasing home brewing adoption, rising consumption of premium coffee products, growing investment in household coffee equipment, and changing consumer preferences toward café-quality experiences at home. The expansion of e-commerce channels and subscription coffee services has further improved accessibility to premium black coffee products for household consumers.Cafés and coffee chains represent the fastest-growing end-use category and are projected to expand at a CAGR exceeding 7% during the forecast period. Growth is supported by the rapid expansion of specialty coffee chains, increasing consumer demand for premium coffee experiences, rising urbanization, and the growing popularity of coffee shops as social and professional gathering spaces. Continuous menu innovation and premium beverage offerings are further strengthening segment growth.Corporate offices are emerging as important growth contributors as employers increasingly invest in premium workplace beverage programs to enhance employee satisfaction, productivity, and workplace amenities. The growing adoption of bean-to-cup systems and premium coffee solutions within office environments is supporting demand across this segment.Institutional demand from transportation services, airlines, airports, universities, healthcare facilities, and government organizations is also expanding steadily. These sectors are increasingly incorporating premium coffee offerings to improve customer experiences and service quality, creating additional growth opportunities across the global black coffee market.

Explore more data points, trends and opportunities Download Free Sample Report

Black Coffee Market Segmentations

By Product Format

- Whole Bean Black Coffee

- Ground Black Coffee

- Instant Black Coffee

- Coffee Pods & Capsules

- Ready-to-Drink (RTD) Black Coffee

By Coffee Bean Type

- Arabica Black Coffee

- Robusta Black Coffee

- Arabica-Robusta Blends

- Specialty & Single-Origin Black Coffee

By Roast Level

- Light Roast Black Coffee

- Medium Roast Black Coffee

- Dark Roast Black Coffee

By Nature

- Conventional Black Coffee

- Organic Black Coffee

- Certified Sustainable Black Coffee

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Coffee Stores

- Online Retail/E-commerce

- Direct-to-Consumer Subscription Platforms

- Foodservice Distribution

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 31% of global black coffee revenue in 2025. The region’s market leadership is supported by a deeply established coffee culture, high per-capita coffee consumption, widespread availability of premium coffee products, and strong consumer purchasing power. The United States alone contributes nearly 26% of worldwide demand, driven by a mature specialty coffee industry, growing demand for organic and ethically sourced products, and continuous product innovation across premium and functional coffee categories. Rising adoption of ready-to-drink coffee, increasing demand for cold brew products, and expanding subscription-based coffee services further support market growth. Canada also contributes significantly through increasing specialty coffee consumption, growing café penetration, and rising consumer interest in sustainable and premium coffee offerings. Advanced retail infrastructure, strong foodservice networks, and high levels of disposable income continue to position North America as a key revenue-generating region.

Europe

Europe accounts for approximately 29% of global market revenue and remains one of the world's most mature coffee-consuming regions. Regional growth is driven by exceptionally high per-capita coffee consumption, strong café traditions, increasing demand for premium and specialty coffee products, and growing consumer awareness regarding sustainability and ethical sourcing practices. Germany serves as the largest coffee importer and processing hub within Europe, while Italy continues to shape global coffee culture through its long-standing espresso heritage. France, the United Kingdom, Spain, and the Netherlands contribute substantially to regional demand through strong retail and foodservice consumption. The growing popularity of specialty roasters, organic coffee products, fair-trade certifications, and premium home brewing equipment continues to support market expansion. Additionally, strong consumption levels across Nordic countries reinforce Europe’s position as a major global market for black coffee.

Asia-Pacific

Asia-Pacific accounted for approximately 23% of global market share in 2025 and is expected to record the fastest growth throughout the forecast period. The region’s expansion is driven by rapid urbanization, rising disposable incomes, westernization of consumer lifestyles, growing café culture, and increasing awareness of premium coffee products. China represents the most attractive growth market, supported by expanding coffee shop chains, a growing middle-class population, and increasing acceptance of coffee as a daily beverage. India is witnessing strong growth due to rising purchasing power, expanding specialty coffee networks, growing youth populations, and increasing demand for convenient beverage options. Japan and South Korea remain highly developed markets characterized by innovation, premium product consumption, and strong demand for ready-to-drink coffee formats. Vietnam and Indonesia continue strengthening their positions as both major coffee-producing nations and rapidly expanding consumer markets. Rising investments from international coffee brands and the proliferation of digital foodservice platforms are expected to further accelerate regional market growth.

Latin America

Latin America contributes approximately 9% of global black coffee revenue and continues to benefit from its strong coffee production heritage. Regional growth is supported by increasing domestic coffee consumption, expanding urban populations, rising middle-class incomes, and growing consumer interest in premium and specialty coffee products. Brazil dominates regional demand while maintaining its position as the world's largest coffee producer. Increasing café culture, product premiumization, and growing awareness of specialty coffee varieties are supporting market expansion throughout the country. Mexico, Colombia, Chile, and Argentina are also witnessing steady growth driven by urbanization, evolving consumer preferences, and improving purchasing power. Greater availability of specialty coffee products, expanding local roasting industries, and rising tourism-related coffee consumption are creating additional opportunities across the region.

Middle East & Africa

The Middle East and Africa account for approximately 8% of global market revenue and represent an increasingly attractive growth region. Market expansion is being driven by rapid urbanization, rising disposable incomes, growing youth populations, expanding café chains, and increasing consumer interest in premium coffee experiences. The United Arab Emirates and Saudi Arabia are emerging as major consumption hubs due to strong specialty coffee adoption, luxury hospitality development, and increasing investments in premium foodservice establishments. Turkey continues to maintain a strong coffee-drinking tradition while incorporating modern specialty coffee concepts. South Africa remains one of the region’s most developed coffee markets, supported by growing urban consumer demand and expanding retail availability. Across Africa, increasing domestic coffee consumption, rising middle-class populations, and investments in value-added coffee processing are supporting market development. The expansion of specialty coffee retail, international coffee chains, and premium hospitality infrastructure is expected to sustain long-term growth across the region.

Key Players in the Black Coffee Market

- Nestlé

- JDE Peet's

- Starbucks Corporation

- Luigi Lavazza S.p.A.

- Tchibo GmbH

- Keurig Dr Pepper

- Massimo Zanetti Beverage Group

- illycaffè S.p.A.

- UCC Holdings Co., Ltd.

- Strauss Group Ltd.

- Tata Consumer Products Limited

- Luckin Coffee Inc.

- Costa Coffee

- Tim Hortons

- Café de Coral Coffee Division