Black Beer Market Size

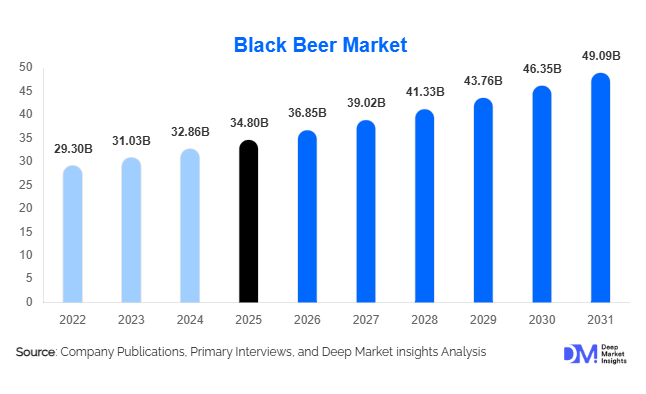

According to Deep Market Insights, the global black beer market size was valued at USD 34.8 billion in 2025 and is projected to grow from USD 36.85 billion in 2026 to reach USD 49.09 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The black beer market growth is primarily driven by the increasing consumer preference for premium alcoholic beverages, rising demand for craft and specialty beer styles, and growing adoption of dark beer variants such as stouts, porters, schwarzbiers, and specialty black ales across both mature and emerging beer markets. The market is further supported by innovation in flavor profiles, expansion of microbreweries, increasing popularity of beer tourism, and growing consumer willingness to experiment with premium and artisanal beer products. Demand remains particularly strong in Europe and North America, while Asia-Pacific is emerging as the fastest-growing region due to rising disposable incomes, urbanization, and the premiumization of alcoholic beverage consumption.

Key Market Insights

- Premium and craft black beer products are increasingly gaining market share, supported by consumer demand for authentic brewing traditions, complex flavor profiles, and premium drinking experiences.

- Stouts and specialty dark beers continue to witness strong growth, driven by innovations including coffee-infused, chocolate-flavored, barrel-aged, and nitrogen-infused variants.

- Asia-Pacific dominates global black beer consumption, accounting for nearly 40% of market demand, supported by China, Japan, South Korea, and rapidly growing consumption in India.

- India represents the fastest-growing country market, benefiting from premium beer adoption, a young consumer demographic, and increasing urban disposable income.

- Off-trade distribution channels remain dominant, with supermarkets, liquor stores, and online retail platforms accounting for more than 60% of global sales.

- Technological advancements in brewing and packaging, including nitrogen infusion systems, sustainable brewing technologies, and alcohol-free brewing processes, are reshaping product development across the market.

Black Beer Market Latest Trends

Premiumization and Specialty Flavor Innovation

The black beer industry is experiencing a significant shift toward premiumization as consumers increasingly seek distinctive and high-quality drinking experiences. Brewers are introducing specialty variants incorporating coffee, chocolate, vanilla, smoked malt, bourbon barrel aging, and nitro infusion technologies. These products command premium pricing while helping breweries differentiate themselves in an increasingly competitive beer landscape. Limited-edition releases and seasonal dark beer offerings are becoming major revenue contributors, particularly among craft breweries targeting younger consumers and beer enthusiasts. Premium black beer products often generate profit margins that are 20–40% higher than standard lager products, encouraging both multinational brewers and independent breweries to expand their dark beer portfolios.

Growth of Low-Alcohol and Non-Alcoholic Black Beer

Consumer preferences are increasingly shifting toward moderation and wellness-focused alcohol consumption. As a result, non-alcoholic and low-alcohol black beer variants are becoming one of the fastest-growing categories within the broader beer market. Advances in dealcoholization technology have significantly improved flavor retention, allowing producers to offer alcohol-free stouts and dark lagers that closely replicate traditional products. Europe, North America, Japan, and South Korea are leading adoption of this trend. Major brewers are investing heavily in non-alcoholic dark beer innovation as they seek to address changing consumer lifestyles while maintaining premium flavor experiences.

Black Beer Market Drivers

Expansion of the Global Craft Brewing Industry

The rapid growth of craft breweries worldwide has significantly contributed to the expansion of the black beer market. Craft brewers have become major innovators in dark beer categories, developing unique recipes, small-batch production methods, and experimental flavors that appeal to consumers seeking authenticity and differentiation. Thousands of microbreweries across North America, Europe, Australia, and Asia-Pacific continue to introduce new black beer products, enhancing category visibility and driving premium demand.

Rising Demand for Premium Alcoholic Beverages

Consumers are increasingly trading up from mainstream beer products to premium and super-premium offerings. Black beer styles are often associated with craftsmanship, heritage brewing techniques, and higher-quality ingredients, making them particularly attractive within premium beverage portfolios. Higher disposable incomes and changing consumption habits among millennials and Generation Z consumers are supporting sustained demand growth globally. Premium dark beer products also benefit from stronger customer loyalty and higher average transaction values.

Black Beer Market Restraints

Declining Alcohol Consumption in Mature Markets

Several developed beer markets, including Germany, Japan, the United Kingdom, and the United States, are experiencing gradual declines in per-capita alcohol consumption due to health-conscious lifestyles and moderation trends. While premium black beer continues to outperform mainstream beer categories, lower overall alcohol consumption may constrain long-term volume growth in mature markets.

Volatility in Raw Material and Production Costs

Black beer production requires specialty roasted malts, premium barley, hops, energy-intensive brewing processes, and often longer maturation periods. Volatility in agricultural commodity prices, packaging costs, and energy expenses can significantly impact brewery profitability. Smaller breweries are particularly vulnerable to fluctuations in input costs, which may limit expansion and innovation efforts.

Black Beer Industry Key Opportunities

Expansion into Emerging Premium Beer Markets

Emerging economies such as India, Vietnam, Thailand, Mexico, Brazil, Colombia, and South Africa represent substantial growth opportunities for black beer manufacturers. While traditional lagers continue to dominate beer consumption in these markets, rising urbanization and growing middle-class populations are creating demand for premium imported and craft beer styles. Companies entering these markets early can establish strong brand recognition and secure premium positioning before competition intensifies.

Growth of Alcohol-Free and Functional Dark Beer

The increasing popularity of healthier lifestyle choices presents a significant opportunity for brewers to develop alcohol-free, low-calorie, and functional black beer products. Innovations involving added vitamins, botanical ingredients, natural flavors, and wellness-focused positioning are expected to create new consumer segments. These products appeal to health-conscious consumers who seek premium taste experiences without traditional alcohol consumption patterns.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 34.80 Billion |

| Market Size in 2026 | USD 36.85 Billion |

| Market Size in 2031 | USD 49.09 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dark lager remains the largest product segment, accounting for approximately 41.5% of the global black beer market in 2025. Its market leadership is supported by broad consumer acceptance, balanced roasted flavor profiles, smooth drinkability, and strong compatibility with mainstream beer consumption occasions. Dark lagers appeal to both traditional beer consumers and new entrants to the category, enabling widespread adoption across mature and emerging markets. The segment also benefits from large-scale production capabilities of major breweries, extensive retail availability, and competitive pricing strategies that support high-volume sales. Growing consumer preference for flavorful yet approachable beer styles continues to reinforce demand for dark lager products across supermarkets, bars, restaurants, and convenience retail channels.Stouts represent the fastest-growing product category within the global black beer industry. Rising consumer interest in premiumization, flavor experimentation, and craft brewing innovation has accelerated demand for specialty stout offerings. Coffee stouts, chocolate stouts, milk stouts, oatmeal stouts, and nitro stouts are gaining significant traction among consumers seeking richer taste experiences and differentiated product offerings. Increasing availability of seasonal releases, limited-edition variants, and barrel-aged stouts has further strengthened the segment's growth trajectory. Porter beers continue to maintain a loyal consumer base among craft beer enthusiasts due to their balanced roasted malt characteristics and historical brewing heritage. Meanwhile, specialty black beer categories, including Black IPA, smoked dark beers, imperial dark ales, and barrel-aged variants, are witnessing rapid expansion as breweries focus on product innovation, premium positioning, and experiential consumption trends. Continued investment in flavor innovation and small-batch production is expected to support long-term growth across specialty black beer categories.

Alcohol Content Insights

Standard-alcohol black beer products containing between 3.5% and 6.5% ABV dominate the market with approximately 67% market share in 2025. This segment benefits from its ability to deliver a balance between flavor intensity, sessionability, and responsible consumption, making it suitable for a broad range of consumers and drinking occasions. The widespread availability of standard-strength dark lagers, stouts, and porters across both on-trade and off-trade channels continues to support segment leadership. Regulatory acceptance, lower taxation in certain markets compared to higher-alcohol products, and strong consumer familiarity further contribute to its dominant position.The primary growth driver for the alcohol-content segment landscape is the rapidly expanding demand for low-alcohol and alcohol-free black beer products. Increasing health consciousness, moderation-focused lifestyles, wellness trends, and changing drinking habits among younger consumers are encouraging breweries to invest in non-alcoholic and reduced-alcohol product development. Technological improvements in brewing processes have enabled manufacturers to preserve the flavor complexity of traditional black beers while reducing alcohol content, improving consumer acceptance. At the same time, high-alcohol variants such as imperial stouts, double stouts, and specialty craft releases continue to attract premium consumers seeking richer flavor profiles, exclusivity, and higher-value drinking experiences.

Packaging Format Insights

Cans have emerged as the leading packaging format, accounting for approximately 58.2% of total black beer sales in 2025. The segment's dominance is primarily driven by consumer preference for convenience, portability, product freshness, and sustainability. Aluminum cans offer superior protection against light exposure and oxidation, helping preserve the flavor integrity of dark beer products throughout distribution and storage. Their lightweight nature reduces transportation costs and supports environmental sustainability initiatives through improved recyclability. Growing outdoor consumption, e-commerce distribution, and multipack purchasing patterns have further accelerated the adoption of canned black beer products across global markets.Glass bottles continue to hold a significant position, particularly within premium, imported, and specialty beer categories where packaging aesthetics and brand heritage remain important purchasing factors. Draught and keg formats maintain strong demand within bars, pubs, restaurants, hotels, and brewery taprooms, where consumers increasingly seek fresh and experiential consumption occasions. Multipack formats are also experiencing steady growth as retailers and manufacturers focus on increasing household consumption, value-oriented purchases, and product trial opportunities. Continued innovation in sustainable packaging solutions is expected to remain a key competitive factor across all packaging categories.

Distribution Channel Insights

Off-trade channels account for approximately 60.3% of global black beer sales in 2025, making them the dominant route to market. Supermarkets, hypermarkets, liquor retail chains, convenience stores, specialty beer retailers, and online platforms collectively drive substantial sales volumes by offering broad product availability, competitive pricing, and convenient purchasing experiences. The expansion of organized retail infrastructure across emerging economies and increasing consumer preference for at-home consumption have strengthened off-trade channel performance. The rapid growth of e-commerce platforms, direct-to-consumer sales models, and digital alcohol delivery services has further expanded market accessibility and purchasing convenience.The leading growth driver within distribution channels is the accelerating adoption of digital retail and e-commerce platforms. Consumers increasingly prefer online purchasing due to wider product selection, personalized recommendations, home delivery convenience, and access to specialty products that may not be available through traditional retail outlets. Despite off-trade dominance, on-trade channels including bars, pubs, restaurants, hotels, breweries, and taprooms continue to play a critical role in category development by introducing consumers to new products, facilitating premium experiences, and supporting brand engagement. Craft breweries increasingly leverage taproom experiences, tasting events, and brewery tourism to strengthen customer loyalty and encourage product discovery.

Consumer Category Insights

Premium consumers represent the largest customer segment, accounting for approximately 46% of global market value in 2025. These consumers prioritize product quality, authenticity, brewing craftsmanship, flavor complexity, and brand heritage over price considerations. The segment benefits from the ongoing premiumization trend across the global alcoholic beverages industry, where consumers increasingly seek differentiated products that offer superior taste experiences and perceived value. Premium black beer offerings, including specialty stouts, craft porters, barrel-aged variants, and limited-edition releases, continue to command higher margins and attract affluent consumers.The primary growth driver across consumer categories is the sustained global premiumization of beer consumption. Rising disposable incomes, growing consumer sophistication, and increasing interest in artisanal beverages are encouraging consumers to trade up from mainstream beer products to premium and craft alternatives. Super-premium and craft beer consumers are driving significant demand for innovative black beer styles, while mass-market consumers continue to support volume growth through dark lagers and mainstream stouts. As consumers place greater emphasis on quality, authenticity, and unique flavor experiences, premium and super-premium black beer categories are expected to outperform the broader beer market over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Black Beer Market Segmentations

By Product Type

- Dark Lager

- Stout

- Porter

- Dark Ale

- Specialty Black Beer

By Alcohol Content

- Non-Alcoholic

- Low Alcohol

- Standard Alcohol

- High Alcohol

By Packaging Format

- Cans

- Glass Bottles

- Draught/Keg

- Multipack & Variety Packs

By Brewing Scale

- Macrobrewery Production

- Regional Brewery Production

- Craft Brewery Production

- Microbrewery Production

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Liquor Retail Chains

- Specialty Beer Stores

- Online Retail

- Bars & Pubs

- Restaurants

- Hotels

- Breweries & Taprooms

- Entertainment Venues

Regional Insights

Asia-Pacific

Asia-Pacific represents the largest regional market, accounting for approximately 39.5% of global demand in 2025. China remains the largest country market due to its extensive beer consumption base, expanding middle-class population, and growing interest in premium alcoholic beverages. Japan and South Korea demonstrate strong demand for imported stouts, craft dark beers, and premium specialty offerings, supported by highly developed beverage markets and increasing consumer willingness to experiment with new beer styles. India is emerging as one of the fastest-growing markets globally, driven by rising disposable incomes, rapid urbanization, expanding legal drinking-age populations, and increasing adoption of premium alcoholic beverages. Australia contributes significantly through its mature craft brewing ecosystem and strong consumer acceptance of dark beer products.The primary driver of regional growth in Asia-Pacific is the rapid premiumization of beer consumption supported by rising disposable incomes and expanding urban middle-class populations. Growing exposure to international beer styles, increasing craft brewery investments, expanding modern retail networks, and rising demand for premium alcoholic beverages are accelerating black beer adoption across both developed and emerging markets. Digital retail expansion and changing consumer preferences toward differentiated drinking experiences are further supporting regional market growth.

Europe

Europe accounts for approximately 31% of the global black beer market and remains the historical center of dark beer production and consumption. Ireland leads global stout consumption, supported by strong domestic demand and extensive export activity. Germany dominates dark lager production, benefiting from centuries-old brewing traditions and strong domestic consumption patterns. The United Kingdom remains a major market for porters, stouts, and craft dark beer innovations, while Belgium, Poland, and the Czech Republic continue to support regional demand through established brewing cultures and growing craft beer sectors.The key driver of growth in Europe is the region's strong brewing heritage combined with the expansion of premium and craft beer consumption. Consumers increasingly seek authentic, locally brewed, and specialty dark beer products that emphasize quality, provenance, and traditional brewing methods. Growing demand for craft beverages, brewery tourism, premium product innovation, and the resurgence of heritage beer styles continue to support market expansion across the region.

North America

North America accounts for approximately 21% of global market share in 2025. The United States contributes nearly 80% of regional demand and serves as a global innovation hub for craft stouts, porters, barrel-aged dark beers, and experimental brewing techniques. Strong craft brewery penetration, premiumization trends, and consumer interest in unique flavor profiles continue to support category growth. Canada also contributes significantly through rising premium beer consumption, increasing craft brewery activity, and growing consumer demand for locally produced specialty beers.The leading driver of regional growth is the continued expansion of the craft beer industry and consumer demand for innovative premium beer products. Increasing experimentation with ingredients, flavor profiles, aging techniques, and limited-edition releases is encouraging consumers to explore dark beer categories. Strong brewery innovation, high consumer spending on premium beverages, and a well-developed distribution infrastructure continue to strengthen North America's position within the global black beer market.

Latin America

Latin America represents approximately 5% of global demand, with Brazil and Mexico accounting for the majority of regional consumption. Rising urbanization, increasing premium beer adoption, and expanding hospitality sectors are supporting demand for both imported and locally produced black beer products. Growing consumer awareness of craft brewing, expanding retail availability, and increasing participation of domestic breweries in specialty beer production are contributing to category development throughout the region.The primary regional growth driver is the gradual shift toward premium alcoholic beverages among expanding middle-income consumer groups. Rising disposable incomes, growing tourism activity, increasing exposure to international beer brands, and the development of local craft brewing industries are creating favorable conditions for black beer market expansion. Investments in hospitality infrastructure and modern retail channels are further supporting regional demand growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 3.5% of global market demand in 2025. South Africa remains the largest market due to its well-established brewing industry, relatively mature beer culture, and growing premium beer segment. Tourism-driven consumption in selected Gulf countries and increasing urban demand in Nigeria and other developing markets are contributing to market expansion. Although the region currently represents a smaller share of global demand, it offers significant long-term growth potential.The key growth driver across the Middle East & Africa region is the expanding premium alcoholic beverage consumer base supported by urbanization and rising disposable incomes in select markets. Growth in tourism, increasing availability of imported and premium beer products, expansion of modern retail infrastructure, and changing consumer preferences toward higher-quality beverages are gradually strengthening demand for black beer products. As economic development and premium beverage adoption continue to increase, the region is expected to present attractive opportunities for market participants over the forecast period.

Key Players in the Black Beer Market

- Diageo

- Anheuser-Busch InBev

- Heineken N.V.

- Carlsberg Group

- Molson Coors Beverage Company

- Asahi Group Holdings

- Kirin Holdings

- Suntory Holdings

- Boston Beer Company

- D.G. Yuengling & Son

- Sierra Nevada Brewing Company

- Deschutes Brewery

- Founders Brewing

- BrewDog

- Royal Unibrew