Bell Peppers Market Size

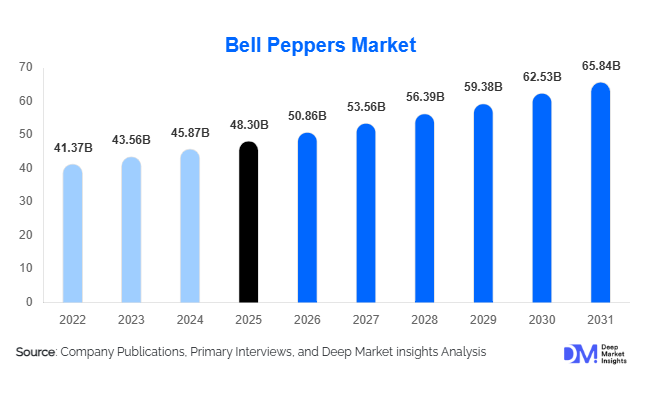

According to Deep Market Insights, the global bell peppers market size was valued at USD 48.3 billion in 2025 and is projected to grow from USD 50.86 billion in 2026 to reach USD 65.84 billion by 2031, expanding at a CAGR of 5.3% during the forecast period (2026–2031). The bell peppers market growth is primarily driven by increasing consumer preference for nutrient-rich vegetables, rising adoption of greenhouse farming, growing demand for convenience foods, and expanding utilization of bell peppers across foodservice and processed food industries globally.

Key Market Insights

- Greenhouse and hydroponic bell pepper cultivation is expanding rapidly, improving year-round production, crop quality, and supply consistency across developed and emerging markets.

- Premium colored bell peppers are witnessing faster growth than green peppers, supported by increasing consumer preference for sweeter flavor profiles and visually appealing food ingredients.

- Asia-Pacific dominates the global bell peppers market, led by strong production and consumption demand from China and India.

- Middle East & Africa is the fastest-growing regional market, driven by rising investments in controlled-environment agriculture and food security initiatives.

- Processed and convenience food applications are accelerating demand, particularly in frozen foods, ready meals, salads, sauces, and quick-service restaurants.

- Technological advancements in precision agriculture, including AI-based crop monitoring, smart irrigation, and automated greenhouse systems, are reshaping commercial bell pepper farming.

bell peppers market latest trends

Expansion of Greenhouse and Controlled-Environment Agriculture

The global bell peppers industry is increasingly shifting toward greenhouse and controlled-environment cultivation systems. Commercial growers are adopting hydroponics, vertical farming, LED-assisted cultivation, and climate-controlled greenhouses to improve yield stability, reduce pesticide usage, and ensure year-round production. Countries including the Netherlands, Canada, the United States, UAE, Saudi Arabia, and China are investing heavily in advanced greenhouse infrastructure to strengthen food security and improve agricultural efficiency. These systems also enable premium-quality production with better color consistency, extended shelf life, and lower climatic risks. Automated irrigation, sensor-based nutrient management, and AI-driven crop monitoring are becoming standard technologies across commercial greenhouse operations.

Growing Demand for Organic and Premium-Colored Bell Peppers

Consumer demand for organic and premium-colored bell peppers continues to rise globally. Red, yellow, and orange bell peppers are gaining popularity due to their sweeter taste, higher antioxidant levels, and increased use in salads, gourmet dishes, and healthy meal preparations. Organic bell peppers are witnessing particularly strong growth across North America, Europe, Japan, and urban Asia-Pacific markets as consumers increasingly prioritize pesticide-free and sustainably grown vegetables. Retailers are expanding shelf space dedicated to premium and organic produce categories, while exporters are strengthening traceability systems and sustainability certifications to meet evolving international food safety standards.

bell peppers market drivers

Rising Demand for Healthy and Functional Foods

Increasing global awareness regarding healthy eating habits and nutritional food consumption is significantly driving demand for bell peppers. Bell peppers are rich in vitamins A and C, antioxidants, dietary fiber, and bioactive compounds, making them highly attractive to health-conscious consumers. Growing preference for Mediterranean, Mexican, and Asian cuisines has further accelerated demand for bell peppers in salads, grilled dishes, pizzas, sandwiches, and ready meals. Rising urbanization and increasing disposable incomes are also encouraging consumers to incorporate fresh vegetables into daily diets, positively impacting global market expansion.

Rapid Growth of Processed and Convenience Food Industry

The expansion of frozen foods, ready-to-cook meals, packaged salads, and foodservice industries is substantially supporting bell pepper demand. Bell peppers are widely utilized across pizzas, sauces, frozen vegetables, meal kits, and snack products because of their flavor, texture, and visual appeal. The increasing penetration of quick-service restaurants and convenience-oriented consumption patterns has accelerated industrial demand for sliced, diced, roasted, and frozen peppers. Food manufacturers are also developing value-added bell pepper products including pepper purees, dried flakes, and seasoning ingredients.

bell peppers market restraints

Climatic Dependency and Supply Volatility

Bell pepper cultivation remains vulnerable to weather fluctuations, pest infestations, drought conditions, excessive rainfall, and water scarcity. Open-field cultivation systems are particularly exposed to unpredictable climatic conditions, often resulting in production losses and price volatility. Seasonal supply disruptions can impact export commitments and reduce profitability for growers and processors. Regions lacking advanced irrigation and protected farming infrastructure remain highly susceptible to climatic risks.

High Capital Investment for Advanced Cultivation Systems

Greenhouse and hydroponic cultivation require substantial investments in climate-control systems, irrigation infrastructure, automation technologies, and energy-intensive operations. Small and medium-scale farmers in developing economies often face financial constraints in adopting advanced cultivation technologies. Rising energy prices, labor shortages, and operational maintenance costs also continue to pressure profitability across commercial greenhouse farming operations. These barriers may slow technology adoption in cost-sensitive agricultural markets.

bell peppers industry key opportunities

Expansion of Export-Oriented Greenhouse Production

Export-oriented greenhouse farming represents a major growth opportunity within the global bell peppers market. Countries such as Mexico, Spain, the Netherlands, Morocco, Turkey, and India are increasingly investing in protected cultivation and cold-chain infrastructure to supply premium bell peppers to Europe, North America, and Gulf countries. Export-grade colored bell peppers generate significantly higher profit margins compared to domestic commodity produce. Retailers globally are prioritizing year-round availability, consistent quality, and traceable supply chains, creating opportunities for technologically advanced growers and exporters.

Growth in Organic and Value-Added Bell Pepper Products

The rapid expansion of organic foods and convenience-oriented products is creating strong opportunities for value-added bell pepper categories. Frozen diced peppers, roasted peppers, fresh-cut packaged vegetables, paprika extracts, sauces, and seasoning ingredients are witnessing rising demand globally. Organic bell peppers continue to command premium retail pricing due to increasing consumer preference for clean-label and sustainable food products. Food processors and agricultural companies are increasingly introducing branded premium pepper products targeting urban consumers, health-conscious households, and foodservice operators.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.30 Billion |

| Market Size in 2026 | USD 50.86 Billion |

| Market Size in 2031 | USD 65.84 Billion |

| CAGR | 5.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Green bell peppers dominate the global market, accounting for the largest share due to lower production costs, widespread culinary usage, and strong industrial demand from foodservice and processed food sectors. Red and yellow bell peppers are rapidly expanding across premium retail and export markets owing to their sweeter taste profiles, higher nutritional content, and attractive visual presentation. Orange and specialty-colored peppers remain niche but fast-growing categories, particularly within gourmet foodservice and organic retail channels. Mixed-color packaged peppers are also gaining traction in supermarkets as consumers increasingly seek visually appealing and ready-to-use fresh produce solutions.

Nature Insights

Conventional bell peppers continue to account for the majority of global production volume due to affordability and extensive open-field farming across Asia-Pacific and Latin America. However, organic bell peppers represent one of the fastest-growing segments globally, particularly across Europe and North America where consumers increasingly prioritize pesticide-free produce and sustainable farming practices. Organic cultivation is also gaining momentum in export-oriented agricultural economies seeking higher premium pricing and international market access.

Cultivation Method Insights

Open-field cultivation remains the dominant production method globally because of its large-scale adoption across China, India, Turkey, and Latin American countries. However, greenhouse cultivation is experiencing the fastest growth as growers increasingly adopt climate-controlled farming systems to improve yield consistency, minimize weather-related risks, and achieve year-round production. Hydroponic and vertical farming methods are also expanding rapidly in urban regions and water-scarce countries where agricultural efficiency and food security have become strategic priorities.

Application Insights

Household consumption remains the leading application segment for bell peppers globally, supported by rising healthy eating trends and increasing usage in home-cooked meals. The foodservice industry represents another major application area due to extensive use of peppers in pizzas, salads, sandwiches, grilled dishes, and international cuisines. Processed food manufacturers are significantly increasing utilization of frozen, dried, roasted, and diced peppers within ready meals, snack foods, sauces, and convenience products. Emerging applications in nutraceuticals, natural food colorants, and functional food ingredients are also creating additional market opportunities.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the bell peppers market distribution landscape due to strong cold-chain infrastructure, broad product availability, and growing consumer preference for organized retail. Wholesale markets continue to play a major role in emerging economies, particularly for fresh produce trade. Online grocery platforms are rapidly gaining popularity across urban regions as consumers increasingly prefer home delivery of fresh vegetables and premium organic produce. Direct-to-foodservice supply channels are also expanding as restaurants and institutional buyers seek reliable year-round sourcing partnerships with commercial growers.

End-Use Insights

Residential consumers account for a substantial share of global bell pepper demand, driven by increasing awareness regarding nutrition and fresh vegetable consumption. Commercial foodservice operators including quick-service restaurants, hotels, and catering companies represent another major end-use segment due to extensive usage of bell peppers across international cuisines and convenience foods. Food manufacturers are increasingly incorporating peppers into frozen foods, packaged salads, meal kits, and seasoning products. Nutraceutical companies are also emerging as niche end users due to growing interest in antioxidant-rich vegetable extracts and functional food ingredients.

Explore more data points, trends and opportunities Download Free Sample Report

Bell Peppers Market Segmentations

Mastronardi Produce

Nature Fresh Farms

Mucci Farms

Pure Flavor

Del Fresco Pure

Rijk Zwaan

Syngenta Group

Bayer Crop Science

Enza Zaden

Village Farms International

Regional Insights

North America

North America accounted for nearly 18% of the global bell peppers market in 2025, driven primarily by strong retail consumption, expanding greenhouse production, and rising demand from foodservice operators. The United States remains the largest regional consumer market due to high consumption of fresh vegetables, frozen foods, and convenience meals. Mexico plays a critical role as a leading exporter of bell peppers into North America because of favorable climatic conditions and lower production costs. Canada is witnessing substantial growth in hydroponic and greenhouse farming, particularly across Ontario and British Columbia, to strengthen domestic year-round supply capabilities.

Europe

Europe represented approximately 24% of global market revenue in 2025 and remains a leading producer of premium greenhouse-grown bell peppers. The Netherlands and Spain dominate regional exports due to advanced greenhouse infrastructure, precision agriculture technologies, and efficient cold-chain logistics. Germany, France, and the United Kingdom represent major import and consumption markets where demand for organic and sustainably produced vegetables continues to rise. European consumers increasingly prioritize traceable, pesticide-free produce, supporting growth in premium bell pepper categories.

Asia-Pacific

Asia-Pacific dominates the global bell peppers market with nearly 45% share of global revenue in 2025. China remains the world’s largest producer and consumer due to extensive cultivation acreage and rising urban demand for fresh vegetables. India is emerging as a major growth market driven by expanding greenhouse cultivation, increasing organized retail penetration, and rising consumption among urban households. Japan and South Korea remain premium import-oriented markets with strong demand for high-quality greenhouse-grown peppers. Southeast Asian countries including Thailand and Vietnam are also witnessing rising demand from foodservice and processed food industries.

Latin America

Latin America continues to strengthen its position as a key export-oriented production hub for bell peppers. Mexico remains one of the world’s largest exporters supplying North American retail and foodservice industries year-round. Brazil and Peru are expanding commercial pepper cultivation due to favorable climatic conditions and rising processed food demand. Chile and Argentina continue to support export supply chains for premium and off-season pepper production. Investments in greenhouse farming and export logistics are improving the region’s international competitiveness.

Middle East & Africa

Middle East & Africa is the fastest-growing regional market, supported by rising investments in controlled-environment agriculture and food security programs. Saudi Arabia and the UAE are heavily investing in hydroponics, vertical farming, and greenhouse cultivation to reduce import dependence and improve local food production. Israel remains a global leader in irrigation technology and desert farming innovation. South Africa and Egypt continue to serve as important regional production centers, while supermarket expansion and changing dietary patterns are accelerating fresh vegetable consumption across the region.

Key Players in the Bell Peppers Market

- Mastronardi Produce

- Nature Fresh Farms

- Mucci Farms

- Pure Flavor

- Del Fresco Pure

- Rijk Zwaan

- Syngenta Group

- Bayer Crop Science

- Enza Zaden

- Limagrain

- Takii & Co.

- East-West Seed

- Dalsem Greenhouse Projects

- Village Farms International

- Lipman Family Farms