Ammonium Phosphatide Market Size

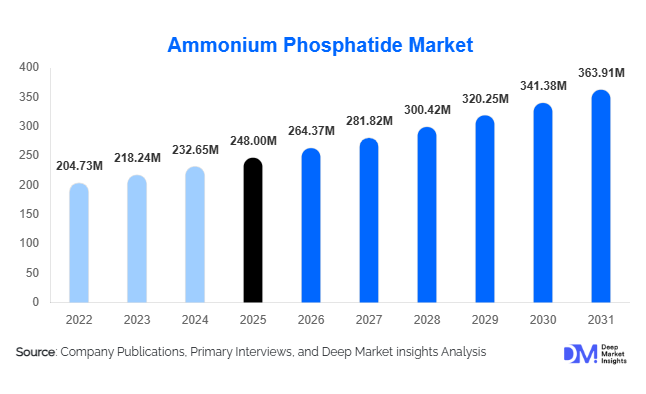

According to Deep Market Insights, theglobal ammonium phosphatide market size was valued at approximately USD 248 million in 2025 and is projected to grow from USD 264.37 million in 2026 to reach USD 363.91 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The ammonium phosphatide market growth is primarily driven by rising demand for cost-efficient emulsifiers in chocolate and confectionery manufacturing, increasing consumption of processed foods, and the growing need for formulation optimization across food processing industries. Ammonium phosphatide is widely utilized as a viscosity-reducing and emulsifying agent that enables manufacturers to reduce cocoa butter usage while maintaining product quality, making it a strategically important ingredient in confectionery production. Growing investments in food ingredient innovation, increasing adoption of plant-based emulsifier systems, and the expansion of premium food manufacturing capacities across emerging economies are further supporting market growth globally.

Key Market Insights

- Chocolate and confectionery applications account for the largest share of global demand, representing nearly 38% of the overall market due to widespread adoption by major chocolate manufacturers.

- Natural ammonium phosphatide products are gaining significant traction, supported by increasing consumer preference for clean-label, non-GMO, and plant-derived ingredients.

- Asia-Pacific dominates the global market, accounting for approximately 34% of total demand, driven by rapid growth in food processing industries across China and India.

- India is emerging as the fastest-growing national market, supported by expanding confectionery production, rising processed food consumption, and government-backed food manufacturing investments.

- Food and beverage manufacturers remain the largest end-use segment, contributing nearly 78% of total market consumption globally.

- Advanced phospholipid processing technologies are enabling manufacturers to improve product functionality, enhance emulsification performance, and expand applications into nutraceutical and specialty food formulations.

Ammonium Phosphatide Market Latest Trends

Growing Preference for Natural and Non-GMO Emulsifier Solutions

Food manufacturers are increasingly transitioning toward naturally sourced ammonium phosphatide formulations derived from sunflower, soybean, and rapeseed feedstocks. Consumer demand for clean-label products is encouraging ingredient suppliers to invest in traceable and non-GMO phospholipid production systems. Large confectionery brands are actively reformulating products to reduce reliance on synthetic additives while maintaining production efficiency. Sustainability certifications and responsible sourcing initiatives are becoming important purchasing criteria for multinational food manufacturers. This trend is particularly visible across Europe and North America, where regulatory scrutiny and consumer awareness regarding ingredient transparency continue to intensify.

Expansion of Specialty Food and Nutraceutical Applications

Beyond traditional chocolate applications, ammonium phosphatide is increasingly being incorporated into functional foods, dietary supplements, nutritional beverages, and specialty food formulations. Nutraceutical manufacturers are utilizing phospholipid-based emulsification technologies to improve ingredient stability and bioavailability. The rapid growth of health-focused consumer products is creating new demand opportunities for specialty phosphatide ingredients. Product innovation efforts are also focusing on customized emulsifier systems that combine cost optimization with enhanced nutritional functionality, enabling suppliers to access higher-margin application areas.

Ammonium Phosphatide Market Drivers

Rising Global Chocolate and Confectionery Production

The continued expansion of global chocolate consumption remains one of the strongest drivers for ammonium phosphatide demand. Manufacturers utilize ammonium phosphatide to optimize chocolate viscosity, improve processing efficiency, and reduce dependence on expensive cocoa butter. As premium and mass-market confectionery production continues to grow across Asia-Pacific, Latin America, and the Middle East, demand for cost-effective emulsification solutions is increasing correspondingly. The ingredient's ability to lower production costs without compromising product quality makes it particularly attractive during periods of cocoa price volatility.

Increasing Demand for Processed and Convenience Foods

Urbanization, changing lifestyles, and rising disposable incomes are driving consumption of processed food products worldwide. Bakery products, fillings, dairy products, spreads, and ready-to-eat foods increasingly require emulsifier systems to maintain texture, consistency, and shelf stability. Ammonium phosphatide provides manufacturers with formulation flexibility while supporting large-scale industrial production requirements. This growing processed food ecosystem continues to create a stable demand base for phospholipid ingredients globally.

Ammonium Phosphatide Market Restraints

Volatility in Vegetable Oil and Phospholipid Feedstock Prices

Ammonium phosphatide production depends significantly on soybean, sunflower, and rapeseed processing streams. Fluctuations in agricultural commodity markets can directly impact raw material availability and production economics. Rising feedstock costs may compress manufacturer margins and create pricing uncertainty across supply chains. Suppliers must continuously optimize sourcing strategies to mitigate raw material cost risks.

Competition from Alternative Emulsifier Technologies

Alternative emulsifiers, including lecithin, mono- and diglycerides, and other phospholipid-based systems, continue to compete for market share across food applications. Some food manufacturers maintain long-established formulations based on competing ingredients, limiting conversion opportunities. Overcoming formulation inertia and demonstrating superior cost-performance benefits remain key challenges for ammonium phosphatide suppliers.

Ammonium Phosphatide Industry Key Opportunities

Emerging Market Food Manufacturing Expansion

Rapid industrialization of food production across India, China, Indonesia, Vietnam, Saudi Arabia, and Brazil presents substantial opportunities for ammonium phosphatide suppliers. Investments in chocolate manufacturing, bakery production, and processed food facilities are increasing ingredient consumption requirements. Local production partnerships, technical service centers, and regional supply networks can help market participants capitalize on growing demand. As multinational food brands expand manufacturing footprints across emerging economies, adoption of advanced emulsifier technologies is expected to accelerate.

Development of Premium Functional Ingredient Solutions

The growing nutraceutical and functional food industries create opportunities for manufacturers to develop high-performance phospholipid systems tailored for health-focused applications. Functional beverages, dietary supplements, meal replacements, and specialty nutrition products increasingly require advanced emulsification capabilities. Companies that invest in customized formulations, enhanced phospholipid purity, and application-specific ingredient platforms can access higher-value market segments and improve profitability. This diversification beyond traditional confectionery applications is expected to become a significant growth avenue over the coming decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 248.00 Million |

| Market Size in 2026 | USD 264.37 Million |

| Market Size in 2031 | USD 363.91 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The natural ammonium phosphatide segment dominates the global ammonium phosphatide market, accounting for approximately 62% of total market revenue in 2025. The segment’s leadership is primarily driven by the accelerating global preference for clean-label, plant-derived, and non-GMO food ingredients. Food and beverage manufacturers are increasingly incorporating naturally sourced phosphatides into product formulations to align with evolving consumer expectations regarding transparency, sustainability, and ingredient authenticity. Growing regulatory scrutiny of food additives across major markets has further encouraged the adoption of naturally derived emulsification solutions. In addition, the expansion of premium confectionery, bakery, and specialty nutrition products continues to support demand for natural ammonium phosphatide. While natural variants maintain market leadership, synthetic ammonium phosphatide remains relevant in cost-sensitive industrial applications and large-scale food processing environments where formulation consistency, functional performance, and economic efficiency are critical purchasing factors. The ongoing transition toward sustainable sourcing practices, coupled with increasing investments in natural ingredient innovation, is expected to further strengthen the dominance of the natural product segment throughout the forecast period.

Form Insights

The liquid form segment represents the largest share of the global ammonium phosphatide market, accounting for approximately 54% of global demand in 2025. The leading position of the segment is primarily attributed to its superior processing efficiency and ease of integration into large-scale food manufacturing operations. Liquid ammonium phosphatide enables accurate dosing, rapid dispersion, and consistent blending during production, making it particularly valuable in chocolate manufacturing and confectionery processing applications. Its ability to improve production efficiency while reducing processing complexity has made it the preferred choice among industrial food producers. Furthermore, increasing automation within food processing facilities continues to support the adoption of liquid formulations. Powder and granular forms are gaining traction in applications requiring extended shelf life, easier transportation, and improved storage stability, particularly in regions with complex supply chain requirements. Paste formulations continue to serve specialized industrial applications where customized rheological properties and formulation flexibility are required.

Function Insights

Emulsification remains the largest functional segment, representing approximately 43% of the total market in 2025. The segment's dominance is driven by the critical role ammonium phosphatide plays in improving oil-water compatibility, enhancing product stability, and maintaining consistent texture characteristics across a wide range of food applications. Growing demand for high-quality confectionery products, bakery formulations, and processed foods continues to support the widespread use of ammonium phosphatide as an effective emulsifying agent. Manufacturers increasingly rely on advanced emulsification technologies to improve product quality while optimizing production costs and formulation efficiency. Viscosity reduction represents the second-largest functional category, particularly within chocolate processing applications where enhanced flow properties enable lower cocoa butter utilization, improved production throughput, and significant cost savings. Additional functions including crystallization control, dispersion enhancement, and stabilization are witnessing growing adoption across specialty foods, functional nutrition products, and innovative food formulations, further expanding the market's functional scope.

Application Insights

Chocolate and compound coatings constitute the largest application segment, accounting for approximately 38% of global market demand in 2025. The segment maintains its leading position due to the indispensable role ammonium phosphatide plays in optimizing chocolate processing efficiency and reducing formulation costs. Manufacturers utilize the ingredient to lower cocoa butter requirements while maintaining desirable texture, viscosity, appearance, and sensory attributes. The continued expansion of global chocolate consumption, premium confectionery offerings, and innovative chocolate-based products remains a key driver supporting segment growth. Beyond chocolate applications, bakery products, confectionery items, dairy formulations, fillings, creams, and spreads continue to generate substantial demand. Growing consumer interest in convenience foods, premium indulgence products, and functional nutrition solutions is encouraging manufacturers to incorporate advanced emulsifier systems across a broader range of applications. As food companies increasingly focus on formulation optimization and cost efficiency, the adoption of ammonium phosphatide is expected to expand beyond traditional confectionery markets.

End-Use Industry Insights

Food and beverage manufacturing remains the dominant end-use industry, accounting for approximately 78% of total ammonium phosphatide consumption in 2025. The segment’s leadership is primarily driven by the substantial global demand for confectionery, bakery, processed foods, dairy products, and specialty nutrition formulations. The worldwide confectionery industry, valued at more than USD 250 billion annually, continues to represent the largest source of ammonium phosphatide consumption due to the ingredient’s effectiveness in improving product quality and processing efficiency. Increasing consumer demand for premium food products, clean-label formulations, and enhanced sensory experiences is further strengthening market penetration within the food sector. Nutraceutical manufacturing represents the fastest-growing end-use segment, supported by rising health awareness, growing consumption of dietary supplements, and increasing demand for functional ingredients. Pharmaceutical formulations, animal nutrition products, and personal care applications are also emerging as attractive growth opportunities as manufacturers explore the broader functionality of phospholipid-based ingredients across multiple industries.

Distribution Channel Insights

Direct sales channels account for nearly 68% of global market revenue in 2025, making them the leading distribution segment. The dominance of direct sales is primarily driven by the highly business-to-business nature of the ammonium phosphatide industry, where product consistency, supply reliability, and technical collaboration are critical factors in procurement decisions. Large food manufacturers typically establish long-term supply agreements with ingredient producers to ensure uninterrupted supply, customized technical support, quality assurance, and formulation expertise. Direct engagement between suppliers and end-users also facilitates product innovation and process optimization, strengthening customer relationships. Specialty ingredient distributors continue to play an important role in serving small and medium-sized food processors that require flexible purchasing arrangements and localized support. Meanwhile, the increasing digitalization of industrial procurement processes is contributing to the gradual emergence of online sourcing platforms, which are improving purchasing transparency, operational efficiency, and supplier accessibility across global markets.

Explore more data points, trends and opportunities Download Free Sample Report

Ammonium Phosphatide Market Segmentations

By Product Type

- Natural Ammonium Phosphatide

- Synthetic Ammonium Phosphatide

By Form

- Liquid

- Paste

- Powder

- Granular

By Function

- Emulsification

- Viscosity Reduction

- Crystallization Control

- Wetting & Dispersion

- Stabilization

- Release Agent Function

By Application

- Chocolate & Compound Coatings

- Bakery Products

- Confectionery Products

- Dairy Products

- Ice Cream & Frozen Desserts

- Fillings & Creams

- Margarine & Spreads

- Instant Food Mixes

- Beverage Systems

- Pharmaceuticals

- Nutraceuticals

- Animal Feed

- Cosmetics & Personal Care

- Industrial Formulations

By End-Use Industry

- Food & Beverage Manufacturing

- Pharmaceutical Industry

- Nutraceutical Industry

- Animal Nutrition Industry

- Personal Care & Cosmetics Industry

- Industrial Chemicals Industry

Regional Insights

Asia-Pacific

Asia-Pacific leads the global ammonium phosphatide market, accounting for approximately 34% of total market revenue in 2025. The region's dominance is supported by its rapidly expanding food processing industry, strong confectionery manufacturing base, and increasing consumption of processed and convenience foods. China accounts for nearly 14% of global demand, benefiting from large-scale chocolate, bakery, and confectionery production as well as continuous investments in food manufacturing modernization. India contributes approximately 7% of global consumption and is projected to register the fastest growth rate globally, exceeding 8% CAGR through 2031, supported by rising urbanization, growing middle-class spending, increasing packaged food consumption, and expanding domestic food processing capacity. Japan and South Korea continue to generate significant demand for premium food ingredients, specialty emulsifiers, and high-value confectionery products. Additional regional growth drivers include favorable government initiatives supporting food manufacturing, increasing foreign direct investment in the food and beverage sector, expanding organized retail networks, and rising consumer preference for premium and clean-label food products.

Europe

Europe accounts for approximately 31% of global market demand, making it the second-largest regional market. Germany represents the largest national market within Europe, contributing around 8% of global consumption due to its well-established confectionery, bakery, and food processing industries. The United Kingdom, France, Italy, Belgium, and the Netherlands remain significant consumers, supported by strong chocolate manufacturing infrastructure and high demand for advanced food ingredient solutions. Regional growth is being driven by increasing adoption of natural and sustainable food additives, stringent food quality regulations, and growing consumer demand for clean-label products. Europe also remains a global leader in specialty food innovation, encouraging manufacturers to develop premium formulations that require advanced emulsification technologies. Continuous investments in sustainable phospholipid sourcing, ingredient traceability, and environmentally responsible production practices are further supporting market expansion across the region.

North America

North America holds approximately 22% of the global ammonium phosphatide market, led by the United States, which accounts for nearly 18% of worldwide demand. The region benefits from a highly developed food processing sector, advanced manufacturing technologies, and strong demand for premium confectionery and bakery products. Growth is increasingly supported by rising consumer preference for natural ingredient systems, clean-label food formulations, and healthier processed food alternatives. The expanding nutraceutical and dietary supplement industry is creating additional opportunities for phospholipid-based ingredients due to their functional and formulation benefits. Manufacturers across the region continue to invest in product innovation, operational efficiency, and premium food categories, further stimulating demand. Canada remains an important secondary market, supported by growing specialty food production, increasing health and wellness trends, and expanding demand for value-added food ingredients.

Latin America

Latin America represents approximately 7% of global market demand in 2025, with Brazil serving as the region's largest market. The market is benefiting from increasing consumption of confectionery products, expanding urban populations, and rising demand for packaged and processed foods. Brazil's large food manufacturing industry continues to drive substantial demand for emulsifier technologies used in bakery, confectionery, and dairy applications. Mexico and Argentina are also contributing significantly to regional growth through expanding food processing activities and increasing investments in manufacturing infrastructure. Additional growth drivers include improving retail penetration, rising disposable incomes, growing demand for premium food products, and increasing adoption of cost-efficient formulation technologies that enhance production performance while maintaining product quality.

Middle East & Africa

The Middle East & Africa account for approximately 6% of global market revenue in 2025. Although relatively smaller in size, the region is expected to witness steady growth supported by ongoing diversification of food manufacturing activities and rising investments in domestic food production capabilities. Saudi Arabia and the United Arab Emirates are emerging as attractive growth markets due to increasing investments in food processing infrastructure, expanding premium confectionery consumption, and government initiatives aimed at strengthening food security and local manufacturing capacity. South Africa remains the largest Sub-Saharan market, benefiting from a well-developed food processing sector and growing demand for specialty food ingredients. Additional regional growth drivers include rapid urbanization, changing dietary patterns, rising demand for convenience foods, expansion of modern retail channels, and increasing adoption of advanced food processing technologies across both domestic and export-oriented food industries.