Women’s Underwear Market Size

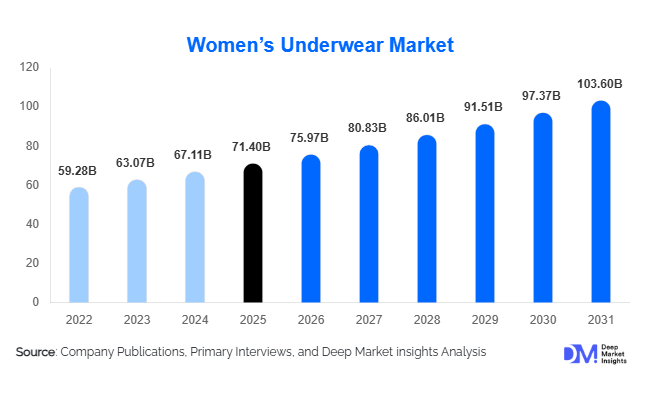

According to Deep Market Insights, the global women’s underwear market size was valued at USD 71.4 billion in 2025 and is projected to grow from USD 75.97 billion in 2026 to reach USD 103.60 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The market growth is primarily driven by rising female workforce participation, increasing demand for comfort-oriented intimate apparel, growing adoption of premium lingerie products, and rapid expansion of digital retail channels. The evolution of women’s underwear from a purely functional necessity into a fashion, wellness, and self-expression category has significantly expanded addressable market opportunities across both developed and emerging economies.

Key Market Insights

- Comfort-focused products are becoming the dominant category globally, with seamless panties, wireless bras, and bralettes witnessing strong adoption among consumers seeking all-day wearability.

- Sustainable underwear is emerging as one of the fastest-growing segments, supported by increasing consumer awareness regarding ethical sourcing, recycled fabrics, and environmentally responsible manufacturing practices.

- Asia-Pacific dominates the global market, accounting for nearly 43% of global revenue due to its large consumer base, expanding middle class, and strong manufacturing ecosystem.

- India is among the fastest-growing national markets, driven by rising disposable incomes, urbanization, and increasing penetration of organized retail and e-commerce platforms.

- Period underwear and functional intimate apparel are creating new revenue streams, attracting consumers seeking reusable, health-conscious, and sustainable alternatives.

- Technology adoption is reshaping product development, including AI-powered sizing solutions, virtual fitting technologies, seamless knitting systems, moisture-management fabrics, and antimicrobial textile innovations.

Women’s Underwear Market Trends

Growing Demand for Comfort and Everyday Wear Products

Consumer purchasing behavior has shifted significantly toward comfort-oriented underwear solutions. Wireless bras, seamless panties, bralettes, and soft-touch fabric products are increasingly replacing traditional structured underwear. Hybrid work environments, changing lifestyle preferences, and increasing awareness regarding physical comfort have accelerated this trend globally. Brands are prioritizing lightweight materials, flexible fits, and breathable fabrics that enhance all-day usability. Product launches increasingly emphasize comfort features such as tagless construction, stretch-fit technology, and moisture management capabilities. The trend is particularly strong among younger consumers who prioritize functionality alongside aesthetics, creating sustained demand across both premium and mass-market categories.

Sustainable and Eco-Friendly Underwear Gaining Momentum

Sustainability has become a key purchasing criterion across major apparel categories, including intimate wear. Manufacturers are expanding product portfolios featuring organic cotton, bamboo fibers, recycled nylon, biodegradable packaging, and ethically sourced materials. Consumers are increasingly willing to pay premium prices for environmentally responsible products that align with their personal values. Regulatory pressures regarding textile waste and carbon emissions are also encouraging brands to adopt circular manufacturing models. Several market participants are investing in traceable supply chains, closed-loop recycling systems, and water-efficient textile production technologies to strengthen their sustainability credentials and attract environmentally conscious consumers.

Women’s Underwear Market Drivers

Rising Female Workforce Participation

Increasing female employment rates across emerging and developed economies continue to support market expansion. Working women represent a major consumer segment for everyday comfort products, premium intimate apparel, and specialized functional underwear. Growing purchasing power, greater financial independence, and increasing awareness regarding product quality are driving higher spending on branded underwear. Professional women increasingly prioritize comfort, durability, and premium fabrics, contributing to market premiumization and higher average selling prices across multiple product categories.

Rapid Growth of E-Commerce and Direct-to-Consumer Sales

The expansion of online retail channels has transformed underwear purchasing behavior. E-commerce platforms enable consumers to access wider product assortments, broader size ranges, customer reviews, and personalized recommendations. Direct-to-consumer business models are allowing brands to improve customer engagement while reducing intermediary costs. Advanced technologies such as virtual fitting rooms, AI-powered size recommendations, and subscription-based purchasing models are enhancing customer retention and improving online conversion rates. Emerging markets are particularly benefiting from increased smartphone penetration and digital payment adoption.

Women’s Underwear Market Restraints

Volatility in Raw Material Prices

Fluctuations in the prices of cotton, elastane, polyester, and nylon continue to impact manufacturing costs and profitability across the industry. Global supply chain disruptions, energy cost increases, and inflationary pressures can create uncertainty regarding input costs. Manufacturers operating in highly competitive markets often face challenges passing these cost increases directly to consumers, resulting in margin pressures and pricing challenges.

Counterfeit Products and Unorganized Competition

The presence of low-cost counterfeit products and unorganized manufacturers remains a significant challenge, particularly across developing markets. These products often compete aggressively on price, creating downward pressure on branded manufacturers. Counterfeit products may also affect consumer trust and dilute brand equity, limiting premium category penetration and reducing growth opportunities for established market participants.

Women’s Underwear Market Opportunities

Expansion of Period Underwear and Functional Intimate Apparel

Period underwear has emerged as one of the fastest-growing categories within the women’s underwear industry. Consumers are increasingly adopting reusable menstrual products due to their sustainability benefits, convenience, and long-term cost savings. Additional opportunities exist within maternity, nursing, adaptive, and recovery-support underwear categories, which remain relatively underpenetrated in many markets. Specialized products designed for women's health and wellness applications are expected to generate significant future growth.

Digital Personalization and Direct-to-Consumer Growth

The increasing use of artificial intelligence, data analytics, and personalized shopping experiences presents substantial opportunities for brands. AI-powered sizing recommendations, customized product bundles, subscription programs, and targeted marketing initiatives can improve customer loyalty and increase lifetime value. Direct-to-consumer platforms also allow brands to gather valuable consumer insights, optimize inventory management, and accelerate product innovation. New entrants can leverage digital-first business models to compete effectively against established incumbents without extensive physical retail investments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 71.4 Billion |

| Market Size in 2026 | USD 75.97 Billion |

| Market Size in 2031 | USD 103.60 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Panties and briefs account for the largest share of the women’s underwear market, representing approximately 39.2% of global revenue in 2025. The segment benefits from high replacement frequency, universal consumer adoption, and strong demand across all age groups. Everyday-use categories such as bikini briefs, hipsters, seamless panties, and high-waist designs continue to drive volume growth. Bras represent the second-largest segment, supported by innovation in wireless designs, sports bras, and comfort-oriented products. Functional categories, including period underwear, shapewear, and maternity products,s are experiencing above-average growth rates as consumers increasingly seek specialized solutions tailored to specific lifestyle and wellness needs.

Material Insights

Cotton remains the leading material segment, accounting for approximately 34.8% of global market revenue. Consumers continue to favor cotton due to its breathability, comfort, affordability, and skin-friendly properties. Cotton products are particularly popular in emerging markets where comfort and value remain primary purchasing criteria. Synthetic fibers such as polyester and nylon maintain strong demand due to durability, elasticity, and performance-enhancing characteristics. Meanwhile, sustainable materials, ls including bamboo fabrics, recycled fibers, and organic cotton, are expanding rapidly as environmental considerations become increasingly important in purchasing decisions.

Distribution Channel Insights

Offline retail channels continue to dominate global sales, accounting for approximately 58.2% of market revenue. Specialty lingerie stores, department stores, and branded retail outlets remain important purchasing destinations because consumers often prefer physical fitting and product evaluation before purchase. However, online channels are rapidly gaining market share due to convenience, broader product selection, and growing confidence in virtual fitting technologies. Direct-to-consumer websites are becoming increasingly important, enabling brands to strengthen customer relationships, improve profit margins, and deliver personalized shopping experiences. Social commerce platforms and influencer-driven marketing strategies are also contributing to digital channel expansion.

Consumer Age Group Insights

Women aged 20–34 years represent the largest consumer segment, accounting for approximately 38.6% of total market demand. This demographic drives fashion trends, premiumization, and digital purchasing activity. Younger consumers are particularly receptive to innovative products such as seamless underwear, sustainable materials, and period underwear. Consumers aged 35–49 years continue to generate substantial demand for premium comfort-focused products, while mature consumers increasingly prioritize health, support, and ease of use. Growing awareness regarding body positivity and inclusive sizing is also encouraging participation across broader demographic groups.

Explore more data points, trends and opportunities Download Free Sample Report

Women’s Underwear Market Segmentations

By Product Type

- Panties & Briefs

- Bras

- Shapewear

- Thermal & Functional Underwear

- Luxury & Fashion Lingerie Sets

By Material

- Cotton

- Synthetic Fibers

- Elastane/Spandex Blends

- Modal & Bamboo Fabrics

- Silk & Satin

- Sustainable/Recycled Materials

By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

By Functionality

- Everyday Comfort

- Sports & Activewear

- Maternity

- Menstrual/Period Care

- Bridal & Occasion Wear

- Medical & Recovery Support

By Distribution Channel

- Hypermarkets & Supermarkets

- Department Stores

- Specialty Lingerie Stores

- Brand-Owned Retail Stores

- E-Commerce Marketplaces

- Direct-to-Consumer Online Stores

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global women’s underwear market, accounting for approximately 42.8% of global revenue in 2026. The region benefits from a unique combination of large population bases, expanding middle-class consumers, rising female workforce participation, increasing fashion awareness, and strong textile manufacturing capabilities. China remains the largest market within the region, supported by high domestic consumption, extensive retail networks, and the presence of major apparel manufacturing clusters that enable competitive pricing and rapid product innovation. Chinese consumers are increasingly shifting toward premium, comfort-focused, and digitally marketed underwear products, driving value growth across the market.

India represents one of the fastest-growing markets globally, supported by rapid urbanization, rising disposable incomes, growing participation of women in professional employment, and increasing penetration of organized retail and e-commerce channels. The expansion of domestic brands and increasing consumer awareness regarding product quality, hygiene, and fit are accelerating market growth. Japan and South Korea contribute significantly to premium segment revenues due to strong consumer preferences for technologically advanced fabrics, seamless construction, and functional intimate apparel. Across Southeast Asia, countries including Indonesia, Vietnam, Thailand, and the Philippines are witnessing increasing demand due to expanding middle-income populations, improving retail infrastructure, and greater exposure to international fashion trends. The region is expected to maintain the highest growth rate globally throughout the forecast period due to its favorable demographic profile and growing purchasing power.

North America

North America accounts for approximately 26.4% of global women’s underwear market revenue, with the United States representing the overwhelming majority of regional demand. Market growth is driven by high consumer spending on apparel, strong adoption of premium and luxury intimate wear, and widespread acceptance of inclusive sizing and body-positive product offerings. Consumers increasingly prioritize comfort, sustainability, and multifunctional products, supporting demand for wireless bras, seamless underwear, shapewear, and performance-focused intimate apparel.

The region has also become a global leader in direct-to-consumer retailing, subscription-based purchasing models, and digitally native underwear brands. Advanced e-commerce infrastructure, high internet penetration, and the adoption of AI-powered sizing technologies have accelerated online purchasing behavior. Demand for sustainable underwear products made from organic cotton, recycled fibers, and ethically sourced materials continues to increase, particularly among younger demographics. In addition, strong product innovation, celebrity-backed brands, and premium lifestyle positioning are driving category expansion. Canada contributes additional growth through rising demand for sustainable products and premium intimate apparel, further strengthening the region’s market outlook.

Europe

Europe accounts for approximately 22.3% of global market revenue and remains one of the most mature and premium-focused regions within the women’s underwear industry. Germany, the United Kingdom, France, Italy, and Spain collectively represent the majority of regional demand. European consumers demonstrate strong preferences for high-quality fabrics, superior craftsmanship, sustainability, and ethical sourcing practices, creating favorable conditions for premium and luxury underwear manufacturers.

The primary growth driver across Europe is the increasing emphasis on sustainable fashion and environmental responsibility. Consumers actively seek products manufactured using organic cotton, recycled materials, and environmentally friendly production methods. Regulatory initiatives promoting sustainable textile production and circular economy principles are further encouraging manufacturers to innovate. Western European markets continue to witness strong demand for premium lingerie, shapewear, and fashion-oriented underwear products, while Eastern European countries are benefiting from rising disposable incomes and increasing retail modernization. The growing popularity of e-commerce platforms and direct-to-consumer brands is also expanding product accessibility throughout the region. Europe is expected to remain a key market for premiumization and sustainable product innovation during the forecast period.

Latin America

Latin America represents approximately 5.4% of global women’s underwear demand, with Brazil and Mexico serving as the largest regional markets. Market growth is supported by increasing female workforce participation, improving economic conditions, expanding middle-class populations, and rising consumer expenditure on personal apparel products. Brazilian consumers have historically demonstrated strong demand for lingerie and intimate apparel, making the country one of the most developed underwear markets within the region.

The rapid growth of e-commerce and social commerce platforms is improving product accessibility and enabling international brands to reach previously underserved consumers. Fashion-conscious younger populations are increasingly adopting premium underwear products, while organized retail expansion is supporting greater availability of branded offerings. Mexico is benefiting from rising urbanization, expanding retail infrastructure, and increasing consumer exposure to global fashion trends. Additionally, improvements in digital payment systems and logistics networks are enhancing online purchasing activity across the region. Despite economic volatility in certain countries, growing consumer awareness regarding quality, comfort, and brand value is expected to sustain long-term market growth.

Middle East & Africa

The Middle East and Africa account for approximately 3.1% of global market revenue, representing the smallest but increasingly attractive regional market. Growth is being driven by rising disposable incomes, expanding retail infrastructure, increasing fashion consciousness, and ongoing urbanization across key economies. Saudi Arabia and the United Arab Emirates lead regional demand, supported by high purchasing power, premium lifestyle preferences, and strong penetration of international apparel brands.

Government-led economic diversification initiatives, particularly under programs such as Saudi Vision 2031, are encouraging retail sector development and increasing consumer spending on lifestyle products. E-commerce adoption is growing rapidly throughout the Gulf Cooperation Council countries, enabling broader access to premium and international underwear brands. In Africa, South Africa remains the largest market due to its relatively developed retail sector and established consumer base. Egypt, Nigeria, and Kenya are emerging as attractive growth markets due to increasing urban populations and rising middle-class spending. Growing awareness of personal hygiene, comfort-focused apparel, and premium product offerings is expected to support long-term market expansion across the region. While market penetration remains lower than in developed regions, improving economic conditions and retail modernization present substantial future growth opportunities.

Key Players in the Women’s Underwear Market

- Hanesbrands Inc.

- Victoria’s Secret & Co.

- PVH Corp.

- Jockey International Inc.

- Triumph International

- Wacoal Holdings Corp.

- Calzedonia Group

- Chantelle Group

- MAS Holdings

- Hunkemöller International

- Marks & Spencer Group plc

- La Perla Global Management

- SKIMS

- Aerie

- Naked Brand Group