Toys Market Size

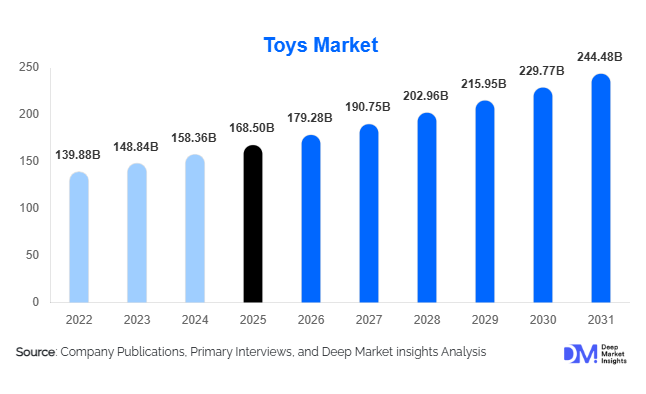

According to Deep Market Insights, the global toys market size was valued at USD 168.5 billion in 2025 and is projected to grow from USD 179.28 billion in 2026 to reach USD 244.48 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The toys market growth is primarily driven by increasing consumer spending on educational and developmental toys, rising demand for licensed and collectible products, expanding e-commerce penetration, and the growing integration of smart technologies into children’s entertainment products.

Key Market Insights

- Educational and STEM toys are witnessing strong global demand, supported by rising parental focus on cognitive development, coding literacy, and experiential learning.

- Licensed toys linked to movies, gaming franchises, anime, and streaming platforms are driving premium product sales, particularly among collectors and adult consumers.

- North America dominates the global toys market, led by strong consumer spending, premium product adoption, and a mature entertainment licensing ecosystem.

- Asia-Pacific remains the fastest-growing regional market, driven by rising middle-class incomes, urbanization, and increasing online retail penetration in China and India.

- Sustainable and eco-friendly toys are rapidly gaining traction, with manufacturers increasingly adopting recyclable plastics, wooden materials, and biodegradable packaging.

- Technological integration, including AI-enabled toys, AR/VR experiences, app-connected products, and interactive learning systems, is transforming the future of the toys industry.

Toys Market Trends

Rise of Educational and STEM-Based Toys

Educational and STEM-based toys are becoming one of the fastest-growing segments within the global toys market. Parents increasingly prioritize products that combine entertainment with cognitive development, problem-solving, creativity, and digital literacy. Robotics kits, coding toys, science experiment kits, and engineering-based construction systems are witnessing strong demand across North America, Europe, China, India, and Southeast Asia. Schools and educational institutions are also integrating STEM toys into learning programs, further accelerating market growth. Manufacturers are increasingly collaborating with edtech platforms and digital learning providers to create hybrid physical-digital learning experiences. This trend is expected to continue as governments and educational bodies place greater emphasis on early-age technological literacy and experiential learning models.

Growing Popularity of Smart and Connected Toys

The adoption of smart connected toys is reshaping the toys market globally. AI-powered interactive toys, voice-enabled learning devices, AR/VR-based gaming systems, and app-connected products are becoming increasingly mainstream. These products enhance engagement by offering personalization, interactive storytelling, adaptive learning, and gamified experiences. Technology integration is especially popular among digitally native younger consumers and tech-savvy parents seeking educational value alongside entertainment. Companies are increasingly monetizing smart toys through subscription-based digital ecosystems, downloadable content, and companion mobile applications. As connectivity infrastructure improves globally and consumer comfort with digital products rises, connected toys are expected to become a major long-term revenue category within the market.

Toys Market Drivers

Increasing Consumer Spending on Child Development Products

Rising disposable incomes and growing awareness regarding early childhood development are significantly driving the toys market. Parents increasingly view toys as developmental tools that support creativity, motor skills, emotional intelligence, and educational outcomes. Educational toys, Montessori systems, sensory toys, and interactive learning products are witnessing strong demand globally. This trend is particularly prominent among urban middle-income households in North America, Europe, China, and India, where consumers are willing to spend more on premium and educational play experiences. The increasing participation of children in structured learning environments is further supporting demand for developmental toys.

Expansion of Entertainment Licensing and Franchise Merchandising

The growing influence of movies, gaming franchises, anime, sports brands, and streaming content has become a major growth driver for the toys industry. Licensed toys linked to blockbuster films, gaming ecosystems, and digital entertainment platforms generate strong seasonal and recurring demand. Popular entertainment properties continue driving sales of action figures, collectibles, plush toys, and premium construction systems. Adult collectors and fandom-driven consumers are additionally contributing to market growth by purchasing premium licensed merchandise and nostalgia-based products. Entertainment licensing enables manufacturers to maintain strong pricing power and sustained consumer engagement across multiple product categories.

Toys Market Restraints

Rising Competition from Digital Entertainment

One of the major challenges facing the toys market is the increasing popularity of digital entertainment platforms such as mobile gaming, streaming services, social media, and online video content. Children are spending greater amounts of time on smartphones, tablets, and gaming devices, reducing engagement with traditional physical toys. This trend is especially impacting conventional toy categories that lack digital integration or interactive features. Manufacturers are therefore under growing pressure to innovate continuously and integrate technology-driven experiences into their product portfolios.

Supply Chain Volatility and Raw Material Cost Fluctuations

The toys industry remains highly dependent on global manufacturing and supply chain networks, particularly across Asia-Pacific. Rising shipping costs, geopolitical tensions, tariffs, and fluctuations in plastic resin and electronic component prices continue impacting operational costs and profitability. Supply chain disruptions can lead to inventory shortages, delayed product launches, and pricing pressures, especially during peak holiday seasons. Smaller manufacturers often face additional challenges in maintaining compliance with evolving international safety and sustainability regulations, which further increases production complexity and costs.

Toys Market Opportunities

Expansion of Sustainable and Eco-Friendly Toys

Growing consumer awareness regarding environmental sustainability is creating major opportunities within the eco-friendly toys segment. Parents increasingly prefer products made from recycled plastics, FSC-certified wood, organic fabrics, and biodegradable materials. Governments and retailers are also encouraging sustainable manufacturing practices through stricter environmental standards and packaging regulations. Companies investing in low-carbon manufacturing, recyclable packaging, and environmentally responsible sourcing are gaining stronger consumer trust and premium positioning. Sustainable toy collections are particularly gaining traction in Europe and North America, where environmentally conscious purchasing behavior continues to rise.

Growth of the Adult Collector and “Kidult” Segment

The emergence of adult toy consumers, commonly referred to as “kidults,” is becoming one of the most profitable opportunities within the global toys market. Adult consumers are increasingly purchasing collectible figurines, premium construction sets, anime merchandise, tabletop games, and nostalgia-driven products linked to childhood franchises. This segment offers higher margins, repeat purchasing behavior, and strong brand loyalty. Social media communities, gaming culture, and entertainment franchises are accelerating collector demand globally. Manufacturers are increasingly developing premium product lines specifically targeted toward adult hobbyists and collectors, significantly expanding the addressable market beyond traditional child-focused demographics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 168.5 Billion |

| Market Size in 2026 | USD 179.28 Billion |

| Market Size in 2031 | USD 244.48 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Building and construction toys dominate the global toys market, accounting for a significant share of overall revenues due to their strong educational value, repeat purchasing behavior, and cross-generational appeal. Premium construction systems linked to entertainment franchises continue witnessing strong demand among both children and adult collectors. Educational and STEM toys are among the fastest-growing categories, driven by increasing emphasis on learning-based play experiences. Dolls and accessories remain highly popular globally, particularly in emerging markets, while action figures and collectibles continue benefiting from movie, gaming, and anime licensing partnerships. Outdoor and sports toys are also witnessing growing demand as parents increasingly encourage physical activity and reduced screen time among children.

Application Insights

Educational applications represent one of the largest and fastest-growing segments within the toys market. STEM kits, coding systems, robotics platforms, and developmental learning toys are increasingly integrated into schools, daycare centers, and homeschooling environments. Entertainment-focused applications linked to movies, gaming ecosystems, and streaming platforms continue driving substantial global demand for licensed products and collectibles. Therapy and special education applications are also expanding, with sensory toys, interactive learning devices, and cognitive development products increasingly used in autism support and occupational therapy. Additionally, family entertainment and tabletop gaming applications are experiencing renewed popularity, supported by growing demand for social and collaborative indoor activities.

Distribution Channel Insights

Online retail and e-commerce platforms are rapidly transforming the global toys industry by enabling wider product accessibility, personalized recommendations, and direct consumer engagement. Digital channels are becoming the fastest-growing distribution segment, particularly in Asia-Pacific and North America, where mobile commerce and social-commerce adoption continue rising. Specialty toy stores maintain strong market relevance due to curated shopping experiences, exclusive products, and in-store demonstrations. Hypermarkets and supermarkets continue dominating mass-market toy sales because of high consumer footfall and seasonal promotional campaigns. Direct-to-consumer channels are also expanding as manufacturers increasingly invest in branded e-commerce platforms, subscription models, and digital marketing strategies to strengthen customer relationships and improve margins.

Age Group Insights

Children aged 5–10 years account for the largest share of global toy demand due to high spending on educational products, construction toys, gaming systems, and licensed entertainment merchandise. Preschool children represent another important segment, particularly for developmental and sensory toys focused on early learning outcomes. Teenagers are increasingly driving demand for gaming-linked collectibles, advanced robotics kits, and hobby-oriented products. The adult collector segment is emerging as one of the fastest-growing age categories globally, fueled by nostalgia-driven purchases, anime culture, premium collectibles, and fandom-based consumption. Older consumers increasingly view toys as lifestyle, hobby, and collectible products rather than solely children’s entertainment items.

Explore more data points, trends and opportunities Download Free Sample Report

Toys Market Segmentations

By Product Type

- Action Figures & Collectibles

- Dolls & Accessories

- Building & Construction Toys

- Educational & STEM Toys

- Games & Puzzles

- Outdoor & Sports Toys

- Infant & Preschool Toys

- Plush Toys

- Electronic & Smart Toys

- Arts & Crafts Toys

- Vehicles & Remote-Control Toys

- Role Play & Pretend Play Toys

By Material

- Plastic Toys

- Wooden Toys

- Metal Toys

- Fabric/Textile Toys

- Bio-based & Sustainable Material Toys

By Age Group

- Infants (0–2 Years)

- Preschool (3–5 Years)

- Children (6–8 Years)

- Pre-teens (9–12 Years)

- Teenagers (13–17 Years)

- Adults & Collectors

By Distribution Channel

- Online Retail & E-commerce

- Specialty Toy Stores

- Hypermarkets & Supermarkets

- Department Stores

- Discount Stores

- Direct-to-Consumer Channels

By Technology Integration

- Traditional/Mechanical Toys

- Battery-operated Toys

- Smart Connected Toys

- AR/VR-enabled Toys

- AI-powered Interactive Toys

Regional Insights

North America

North America remains the largest regional toys market, accounting for approximately 40% of global revenues in 2025. The United States dominates regional demand due to high disposable incomes, strong consumer spending on premium products, and a mature entertainment licensing ecosystem. Educational toys, collectibles, construction systems, and franchise-linked merchandise are particularly popular among U.S. consumers. Canada is also witnessing increasing demand for sustainable and STEM-focused toys, supported by strong retail penetration and high awareness regarding child development products.

Europe

Europe represents a highly mature and innovation-driven toys market led by Germany, the United Kingdom, France, Italy, and Spain. European consumers increasingly prioritize sustainability, safety standards, and educational value when purchasing toys. Wooden toys, eco-friendly materials, and Montessori-based learning products are particularly popular across the region. The United Kingdom continues witnessing strong growth in online toy retail and collectible gaming merchandise, while Germany remains a leading hub for premium educational toys and manufacturing innovation.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market globally, accounting for nearly 29% of total revenues in 2025. China remains both the world’s largest toy manufacturing hub and one of the largest consumer markets. Rising middle-class incomes, urbanization, and expanding digital commerce ecosystems are accelerating toy demand across the region. India is emerging as one of the fastest-growing toy markets due to favorable demographics, government manufacturing initiatives, and rising spending on educational products. Japan and South Korea continue driving premium demand for anime collectibles, gaming-linked toys, and high-quality electronic products.

Latin America

Latin America is witnessing stable growth led by Brazil and Mexico. Increasing retail modernization, rising urban middle-class populations, and expanding access to international toy brands are supporting regional market development. Consumers in the region are increasingly showing interest in affordable educational toys, outdoor products, and licensed entertainment merchandise. However, economic volatility and inflationary pressures remain challenges affecting premium product penetration across several countries.

Middle East & Africa

The Middle East & Africa region is gradually emerging as a promising growth market for premium and educational toys. The UAE and Saudi Arabia are leading regional demand due to high disposable incomes, growing mall-based retail infrastructure, and increasing preference for premium international brands. South Africa remains the largest sub-Saharan toys market, supported by rising organized retail penetration and expanding middle-income consumer groups. Demand for educational and technology-integrated toys is also increasing across urban centers in the region.

Key Players in the Toys Market

- LEGO Group

- Mattel

- Hasbro

- Bandai Namco Holdings

- Spin Master

- MGA Entertainment

- Tomy Company

- VTech Holdings

- Jazwares

- Funko

- Ravensburger

- Playmobil

- Melissa & Doug

- Jakks Pacific

- Moose Toys