Thermowood Market Size

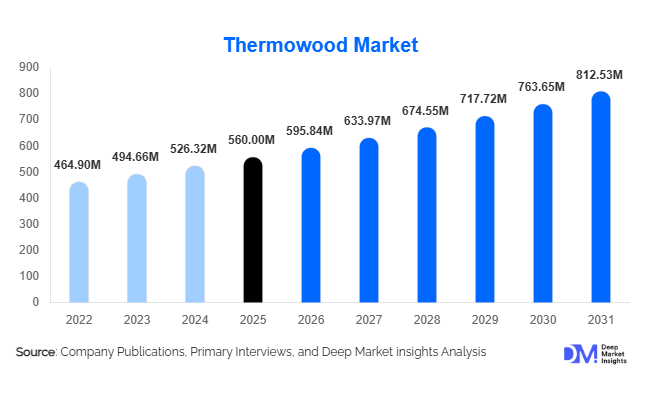

According to Deep Market Insights, the global Thermowood market size was valued at USD 560 million in 2025 and is projected to grow from USD 595.84 million in 2026 to reach USD 812.53 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The Thermowood market growth is primarily driven by increasing adoption of sustainable construction materials, rising demand for environmentally friendly alternatives to tropical hardwoods, and growing investments in green building projects worldwide. Thermally modified wood has emerged as a preferred material for exterior cladding, decking, landscaping, and architectural applications due to its superior dimensional stability, durability, and reduced maintenance requirements. Furthermore, tightening regulations on chemically treated wood products and increasing consumer preference for low-carbon construction materials are supporting long-term market expansion across both developed and emerging economies.

Key Market Insights

- Europe dominates the global Thermowood market, accounting for approximately 38% of global revenue in 2025, supported by mature sustainable construction industries and advanced wood modification technologies.

- Softwood Thermowood remains the leading product category, representing nearly 58% of global demand due to abundant raw material availability and favorable production economics.

- Decking applications account for the largest market share, contributing approximately 32% of total revenue as outdoor living spaces gain popularity worldwide.

- Asia-Pacific is the fastest-growing regional market, supported by rapid urbanization, green building initiatives, and rising demand for premium construction materials.

- Thermowood is increasingly replacing tropical hardwoods in residential and commercial construction due to sustainability concerns and stricter forestry regulations.

- Technological advancements in thermal modification systems are improving production efficiency, product consistency, and energy utilization across manufacturing facilities.

Thermowood Market Trends

Growing Replacement of Tropical Hardwoods

One of the most significant trends influencing the Thermowood market is the increasing substitution of tropical hardwood species such as Ipe, Teak, Merbau, and Cumaru. Governments, developers, and consumers are becoming increasingly concerned about deforestation, illegal logging, and the environmental impact associated with imported tropical timber. Thermowood offers comparable durability, appearance, and weather resistance while utilizing sustainably harvested local wood species. Architects and builders are increasingly specifying thermally modified wood in façade systems, decks, and public infrastructure projects as a sustainable alternative. This trend is particularly visible across Europe and North America, where environmental certification programs are influencing purchasing decisions.

Expansion of Sustainable and Low-Carbon Construction

The global construction industry is increasingly prioritizing low-carbon materials to meet climate targets and green building standards. Thermowood aligns closely with sustainability objectives because it eliminates the need for chemical preservatives while extending wood service life. Builders pursuing LEED, BREEAM, WELL, and other sustainability certifications are incorporating Thermowood into residential, commercial, and public projects. Growing investments in net-zero buildings and bio-based construction materials are expected to accelerate Thermowood adoption across both developed and emerging markets. Manufacturers are also investing in renewable energy-powered production systems to further improve product sustainability credentials.

Thermowood Market Drivers

Rising Demand for Sustainable Building Materials

Growing awareness regarding environmental sustainability is significantly driving Thermowood adoption globally. Governments, developers, and consumers are actively seeking renewable and environmentally responsible construction materials. Thermowood's chemical-free modification process and lower carbon footprint compared to synthetic materials position it as an attractive solution for sustainable construction projects. The increasing implementation of green building regulations and certification programs is expected to sustain long-term demand.

Expansion of Outdoor Living and Landscaping Projects

Investments in residential outdoor spaces, commercial landscaping, hospitality developments, and recreational infrastructure continue to increase worldwide. Thermowood offers superior dimensional stability, moisture resistance, and aesthetic appeal, making it highly suitable for decking, pergolas, fencing, boardwalks, and outdoor furniture applications. The growing popularity of outdoor living environments is creating strong demand across residential and commercial sectors.

Regulatory Shift Away from Chemically Treated Wood

Several countries have introduced restrictions on traditional wood preservatives due to environmental and health concerns. Thermowood provides a viable alternative by enhancing wood durability through heat treatment rather than chemical additives. This regulatory transition is encouraging builders, municipalities, and infrastructure developers to adopt thermally modified wood products in place of conventional treated lumber.

Thermowood Market Restraints

Higher Product Costs Compared to Conventional Lumber

Thermowood products typically command premium prices due to specialized processing equipment, energy-intensive manufacturing procedures, and stringent quality control requirements. Although lifecycle maintenance costs are generally lower, higher upfront costs can discourage adoption among budget-sensitive customers. This remains a key challenge, particularly in developing markets where price considerations strongly influence purchasing decisions.

Limited Market Awareness in Emerging Economies

While Thermowood has achieved strong market penetration across Europe and parts of North America, awareness remains relatively low in many emerging regions. Architects, contractors, distributors, and consumers often lack familiarity with the performance benefits and lifecycle advantages associated with thermally modified wood. Educational initiatives and demonstration projects will be necessary to accelerate adoption rates in these markets.

Thermowood Market Opportunities

Green Building and Net-Zero Construction Initiatives

Global commitments toward carbon neutrality are creating substantial opportunities for Thermowood manufacturers. Governments are introducing incentives for sustainable construction materials, while developers are increasingly prioritizing low-carbon building solutions. Thermowood manufacturers capable of providing environmental product declarations, FSC certification, and traceable sourcing are well-positioned to capitalize on this growing demand. Public infrastructure projects focused on sustainability also represent an attractive growth avenue.

Growth of Outdoor Infrastructure Development

Significant investments in public parks, waterfront developments, urban beautification programs, and recreational infrastructure are creating new opportunities for Thermowood applications. Municipal governments increasingly prefer durable and environmentally friendly materials for boardwalks, pedestrian pathways, outdoor seating, and landscape structures. These projects provide manufacturers with long-term, high-volume demand opportunities.

Expansion into Premium Hospitality and Wellness Projects

The hospitality sector is increasingly incorporating Thermowood into luxury resorts, eco-lodges, wellness centers, and spa facilities. Its natural appearance, durability, and resistance to moisture make it particularly suitable for sauna construction, outdoor leisure areas, and architectural cladding. Growing investments in tourism infrastructure across the Asia-Pacific and the Middle East are expected to generate additional demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 560 Million |

| Market Size in 2026 | USD 595.84 Million |

| Market Size in 2031 | USD 812.53 Million |

| CAGR | 6.40% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Softwood Thermowood dominates the market, accounting for approximately 58% of global revenue in 2025. Pine and spruce remain the most commonly modified species due to their widespread availability, cost efficiency, and favorable thermal treatment characteristics. Softwood Thermowood is extensively utilized in decking, cladding, fencing, and landscaping applications where dimensional stability and weather resistance are critical. Hardwood Thermowood, particularly thermally modified ash and oak, represents a premium segment with growing demand in architectural applications, outdoor furniture, and luxury construction projects. Although hardwood products command higher prices, they continue to gain popularity among architects seeking premium aesthetics and enhanced durability.

Application Insights

Decking remains the largest application segment, accounting for approximately 32% of the global Thermowood market in 2025. Growing investments in residential outdoor spaces and commercial hospitality projects continue to drive demand. Cladding and façade systems represent the second-largest application category, supported by increasing adoption of sustainable architectural materials. Flooring applications are expanding steadily due to the material's dimensional stability and attractive appearance. Sauna construction remains a niche but high-value segment, particularly across Nordic countries, Central Europe, and luxury wellness facilities globally. Outdoor furniture and garden structures are also emerging as important applications due to growing consumer preference for sustainable outdoor products.

End-Use Industry Insights

Residential construction represents the largest end-use segment, contributing approximately 46% of global Thermowood demand. Homeowners increasingly utilize Thermowood for decking, fencing, exterior cladding, pergolas, and landscaping projects. Commercial construction continues to demonstrate strong growth, driven by office developments, hotels, retail centers, and institutional buildings seeking sustainable construction materials. Public infrastructure projects, including boardwalks, parks, waterfront developments, and recreational facilities, are becoming increasingly important demand generators. Furniture manufacturing and landscape architecture sectors are also expanding their utilization of thermally modified wood due to durability and environmental benefits.

Distribution Channel Insights

Building material distributors account for the largest share of Thermowood sales, representing approximately 41% of global distribution. These distributors provide inventory management, technical expertise, and established contractor relationships that facilitate product adoption. Direct sales to developers, architects, and construction firms remain significant, particularly for large-scale commercial and infrastructure projects. Specialty wood dealers continue to play an important role in premium residential markets, while online sales channels are gradually expanding as digital procurement becomes more common within the construction industry.

Explore more data points, trends and opportunities Download Free Sample Report

Thermowood Market Segmentations

By Product Type

- Softwood Thermowood

- Hardwood Thermowood

By Application

- Decking

- Cladding & Facades

- Flooring

- Doors & Windows

- Interior Wall & Ceiling Panels

- Outdoor Furniture

- Garden Structures

- Saunas & Wellness Facilities

- Fencing

- Marine & Waterfront Structures

- Other Architectural Applications

By End-Use Industry

- Residential Construction

- Commercial Construction

- Public Infrastructure

- Furniture Manufacturing

- Landscape & Outdoor Living

- Marine Construction

By Distribution Channel

- Direct Sales to Contractors & Developers

- Building Material Distributors

- Timber Merchants

- Specialty Wood Dealers

- E-commerce & Online Platforms

Regional Insights

Europe

Europe remains the largest Thermowood market globally, accounting for approximately 38% of total revenue in 2025. Finland, Sweden, Estonia, Germany, and the United Kingdom are the primary contributors to regional demand and production. Strong environmental regulations, advanced forestry industries, and widespread adoption of sustainable construction materials continue to support market growth. Finland serves as a major global production hub, exporting Thermowood products to North America, Asia-Pacific, and the Middle East.

North America

North America represents approximately 27% of global market revenue, led primarily by the United States. Increasing replacement of pressure-treated lumber and tropical hardwoods is driving demand across residential and commercial applications. The region's growing focus on sustainable construction and outdoor living environments continues to support Thermowood adoption. Canada is also emerging as an important producer and consumer of thermally modified wood products.

Asia-Pacific

Asia-Pacific accounts for approximately 22% of global demand and represents the fastest-growing regional market, with an estimated CAGR exceeding 8% through 2031. China, Japan, Australia, South Korea, and New Zealand are driving growth through increasing investments in green buildings, urban development, and premium residential construction. Rising disposable incomes and growing awareness of sustainable materials are expected to accelerate regional demand.

Latin America

Latin America contributes approximately 6% of global market revenue. Brazil, Chile, and Mexico are the primary consumers of Thermowood products within the region. Demand is supported by infrastructure modernization initiatives, growing tourism investments, and increasing awareness of sustainable construction materials. Although market penetration remains relatively low, long-term growth prospects remain favorable.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of global market demand. Luxury hospitality projects, tourism infrastructure, and premium residential developments are driving adoption across the UAE, Saudi Arabia, Qatar, and South Africa. Thermowood's ability to withstand challenging climatic conditions makes it particularly attractive for exterior applications in the region.