Pump Feeders Market Size

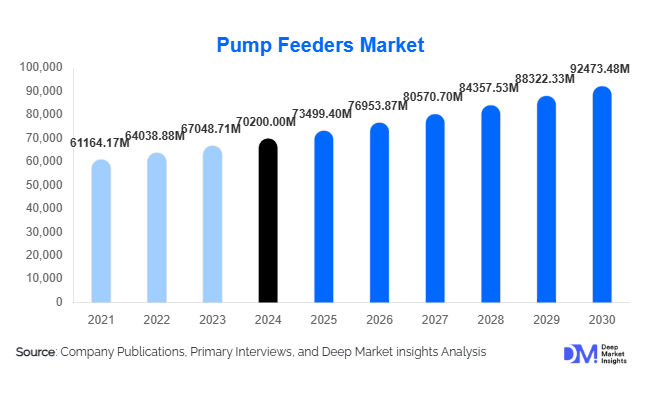

According to Deep Market Insights, the global pump feeders market size was valued at USD 70,200.00 million in 2025 and is projected to grow from USD 73,499.40 million in 2026 to reach USD 92,473.48 million by 2031, expanding at a CAGR of 4.7% during the forecast period (2026–2031). The pump feeders market growth is driven by rapid industrial automation, rising investments in water and wastewater treatment infrastructure, and increasing demand for precision material dosing across chemical, mining, food, and pharmaceutical industries.

Key Market Insights

- Gravimetric pump feeders dominate demand globally, supported by their high dosing accuracy and strong adoption across pharmaceuticals, chemicals, and water treatment applications.

- Asia-Pacific is the largest and fastest-growing region, driven by rapid infrastructure expansion, industrial manufacturing growth, and the rising need for water treatment modernization.

- Water and wastewater treatment represent the single largest end-use industry, contributing nearly 29% of total 2025 demand.

- Smart feeders with IoT-based monitoring and automated calibration are quickly gaining traction as industries shift toward predictive maintenance and real-time process optimization.

- Energy-efficient and corrosion-resistant pump feeders are in high demand due to strict environmental regulations and the rising cost of industrial compliance.

- Top global OEMs hold around 32–35% of the market, creating a moderately concentrated competitive environment dominated by technological innovation.

Pump Feeders Market Trends

Digitalization and Smart Feeding Technologies

Industries worldwide are rapidly integrating smart pump feeder systems that incorporate automated calibration, flow sensors, and real-time feedback loops. These digital enhancements provide higher accuracy, predictive maintenance capabilities, and lower operational downtime. IoT-connected feeders are being adopted within chemical, pharmaceutical, and water treatment plants, enabling remote monitoring of dosing rates, material flow, and wear conditions. Manufacturers are increasingly embedding AI-based analytics into feeder control systems to improve reliability, reduce wastage, and enhance energy efficiency. As industrial automation accelerates globally, digital pump feeders have become a key differentiator in large-scale processing environments.

Shift Toward Energy-Efficient and Eco-Compliant Designs

Rising global focus on sustainability is influencing pump feeder design. Industries seek feeders that minimize chemical overuse, reduce power consumption, and comply with environmental standards such as EPA regulations, EU REACH, and emerging ZLD (Zero Liquid Discharge) policies. Manufacturers are integrating high-efficiency motors, optimized flow paths, and corrosion-resistant alloys that extend equipment life and reduce operational emissions. This trend is especially strong in water treatment and chemical plants, where precision dosing directly affects environmental outcomes.

Pump Feeders Market Drivers

Growth in Global Water and Wastewater Treatment Projects

Water scarcity, stricter purification standards, and rapid urbanization are pushing governments and industries to expand wastewater treatment capacity. Pump feeders are critical for chemical dosing, pH correction, coagulation, and sludge handling. Spending on desalination plants in the Middle East, wastewater upgrades in the U.S., and large-scale municipal water missions in Asia are driving strong, sustained demand for automated feeding systems.

Industrial Automation and Process Efficiency Requirements

Across chemicals, pharmaceuticals, plastics, and food processing, manufacturers are optimizing production lines to achieve higher consistency and lower operating costs. Pump feeders enable precise, controlled dosing essential for quality assurance. Rising adoption of Industry 4.0 technologies further accelerates demand for smart gravimetric and volumetric feeders with real-time monitoring, error detection, and integrated PLC systems.

Pump Feeders Market Restraints

High Installation and Maintenance Costs

Advanced pump feeders, particularly gravimetric and IoT-enabled systems, require significant initial investment and skilled servicing. Small and medium-scale manufacturers in developing regions often prefer low-cost manual alternatives. Maintenance of feeders used in corrosive chemical and slurry environments adds further cost burden.

Raw Material Price Volatility

Feeders require stainless steel, nickel-based alloys, engineering plastics, and composite polymers, all subject to global commodity price fluctuations. Variability in raw material prices affects production costs and can delay procurement decisions for large industrial projects.

Pump Feeders Market Opportunities

Water Treatment Infrastructure Expansion

Emerging markets in Asia, Africa, and Latin America are rapidly scaling municipal and industrial water treatment capacity. Chemical dosing, disinfectant injection, and sludge management rely heavily on pump feeders, creating long-term opportunities. Desalination growth in the Middle East further strengthens market expansion.

Smart and Connected Pump Feeders

The shift toward sensor-integrated feeders capable of predictive maintenance, remote monitoring, and real-time automated dosing provides major growth potential. Manufacturers offering SCADA/DCS-compatible feeders will capture high-value industrial and municipal clients seeking enhanced reliability and efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 70200 Million |

| Market Size in 2026 | USD 73499.40 Million |

| Market Size in 2031 | USD 92473.48 Million |

| CAGR | 4.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Gravimetric pump feeders lead the market with a 32% share, driven by high precision and widespread adoption in regulated industries such as pharmaceuticals and chemicals. Volumetric feeders remain popular for general industrial use, offering cost-effectiveness and durability. Peristaltic feeders are gaining traction in water treatment due to their contamination-free operation, while diaphragm feeders dominate corrosive chemical dosing applications. Centrifugal and piston feeders serve niche requirements in slurry and high-pressure feeding environments, particularly within mining and construction sectors.

Application Insights

Water and wastewater treatment is the dominant application, contributing nearly 29% of global demand, driven by the need for accurate chemical dosing and sludge handling. Chemical processing is another major segment, requiring feeders for acids, catalysts, solvents, and specialty compounds. The mining sector shows strong growth due to slurry handling and mineral processing needs. Food & beverage and pharmaceuticals increasingly rely on precision feeders for hygienic, accurate, and contamination-free dosing systems. New applications in renewable energy processing, battery materials, and hydrogen electrolysis are emerging growth avenues.

Distribution Channel Insights

Direct OEM sales dominate with 55% market share, reflecting industrial buyers’ preference for reliable equipment, warranties, customization, and integrated service packages. Engineering procurement contractors (EPCs) serve large-scale industrial projects, especially in water treatment, oil & gas, and chemicals. Online industrial platforms are gaining traction for standardized feeder purchases, though adoption remains strongest in the mid- and low-capacity feeder segments.

End-User Insights

Water and wastewater treatment plants represent the largest end-user category, driven by global infrastructure expansion. Chemical and petrochemical industries demand feeders for critical dosing of corrosive liquids and catalysts. Mining, construction, pharmaceuticals, food & beverage, and pulp & paper industries represent additional high-growth sectors, each relying on controlled feeding processes to ensure quality and regulatory compliance. New end-use categories are emerging in renewable energy, advanced materials, and EV battery manufacturing, where precise chemical dosing is essential.

Explore more data points, trends and opportunities Download Free Sample Report

Pump Feeders Market Segmentations

By Feeder Type

- Volumetric Pump Feeders

- Gravimetric Pump Feeders

- Centrifugal Pump Feeders

- Piston/Plunger Pump Feeders

- Diaphragm Pump Feeders

- Peristaltic Pump Feeders

By Feeding Mechanism

- Continuous Feeders

- Batch Feeders

- Micro-Dosing Feeders

- Macro-Dosing Feeders

By Pumping Material

- Liquids

- Slurries & Suspensions

- Powders & Granules

- Corrosive & Hazardous Chemicals

By End-Use Industry

- Water & Wastewater Treatment

- Chemical Processing

- Mining & Minerals

- Food & Beverage

- Pharmaceuticals & Biotechnology

- Pulp & Paper

- Cement & Construction Materials

- Oil & Gas

- Power Generation

By Distribution Channel

- Direct OEM Sales

- Engineering Procurement Contractors (EPCs)

- Online Industrial Platforms

Regional Insights

North America

North America accounts for around 23% of global demand, led by the U.S. chemical, pharmaceutical, and water treatment industries. Significant investment in municipal water infrastructure and strict EPA compliance continue to support pump feeder adoption. Canada’s mining sector also contributes to steady demand for slurry-capable feeders.

Europe

Europe holds 21% of the market, with strong adoption driven by Germany, France, and Italy. Strict environmental regulations and advanced manufacturing ecosystems support the use of high-precision gravimetric feeders. The region is a leader in sustainability-focused dosing solutions and IoT-enabled feeder adoption.

Asia-Pacific

Asia-Pacific is the largest region, commanding 38% of the global share and showing the fastest growth. China and India dominate due to industrial expansion and massive water treatment investments. Japan and South Korea drive demand for highly engineered, automated feeding systems used in advanced manufacturing, semiconductors, and pharmaceuticals.

Latin America

Latin America holds around 8% of the market share, with Brazil, Mexico, and Chile leading demand. Mining operations in Chile and industrial expansions in Brazil support strong growth in slurry and chemical feeding applications.

Middle East & Africa

MEA accounts for around 10% of demand, driven by large-scale desalination plants, petrochemical expansions, and mining activities. Saudi Arabia, UAE, and Qatar dominate regional spending, while South Africa contributes significantly through mining and industrial applications.

Key Players in the Pump Feeders Market

- NETZSCH

- Watson-Marlow Fluid Technology

- Grundfos

- SEEPEX

- IDEX Corporation

- Verder Group

- SPX FLOW

- ProMinent

- Milton Roy

- LEWA GmbH

- WAMGROUP

- Coperion

- Schlumberger (Chemical Injection Systems)

- Dover Corporation

- Vogelsang