Stainless Steel Cookware Market Size

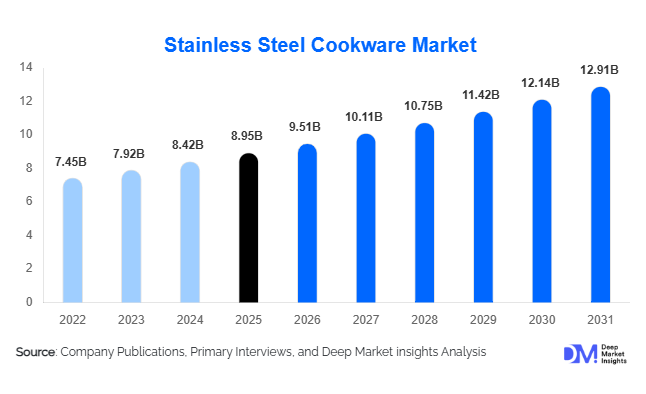

According to Deep Market Insights, the global stainless steel cookware market size was valued at USD 8.95 billion in 2025 and is projected to grow from USD 9.51 billion in 2026 to reach USD 12.91 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The stainless steel cookware market growth is primarily driven by increasing consumer preference for durable and toxin-free cookware, rising adoption of induction-compatible kitchen appliances, and strong growth in residential and commercial foodservice infrastructure globally.

Key Market Insights

- Stainless steel cookware is increasingly replacing traditional coated cookware, driven by consumer concerns regarding food safety, durability, and long-term sustainability.

- Induction-compatible cookware is experiencing rapid global adoption, particularly in Europe and the Asia-Pacific region, as governments promote energy-efficient cooking technologies.

- Asia-Pacific dominates the global market, led by strong manufacturing capabilities and rising middle-class demand in China and India.

- North America remains a major premium cookware market, supported by high spending on modular kitchens and professional-grade cookware.

- E-commerce and direct-to-consumer sales channels are revolutionizing cookware distribution, enabling brands to expand their global reach and enhance customer engagement.

- Technological innovation in tri-ply and multi-clad cookware is improving heat distribution, energy efficiency, and product differentiation across premium categories.

Stainless Steel Cookware Market Trends

Premiumization and Multi-Layered Cookware Adoption

Consumers globally are increasingly shifting toward premium cookware products that combine superior performance with long-term durability. Tri-ply and five-ply stainless steel cookware products are gaining strong traction due to improved heat conductivity, reduced cooking time, and enhanced energy efficiency. Manufacturers are investing heavily in premium product lines featuring copper or aluminum cores, ergonomic handles, scratch-resistant surfaces, and induction-compatible bases. The premium cookware trend is especially strong across North America, Western Europe, Japan, and affluent urban markets in the Asia-Pacific. Rising interest in gourmet cooking, social media-driven culinary culture, and home kitchen remodeling projects are accelerating demand for aesthetically appealing and professional-grade cookware products.

Sustainability and Eco-Friendly Manufacturing Expansion

Sustainability is becoming a major trend shaping the stainless steel cookware market. Consumers are increasingly favoring recyclable, long-lasting, and environmentally friendly cookware alternatives over disposable or chemically coated products. Stainless steel is highly recyclable and aligns with circular economy initiatives being promoted globally. Manufacturers are adopting low-carbon production technologies, recycled stainless steel sourcing, and eco-friendly packaging solutions to strengthen sustainability positioning. Companies are also emphasizing dishwasher-safe and long-lifecycle cookware designs that reduce replacement frequency and environmental waste. This sustainability-driven trend is particularly influential across Europe and North America, where environmental regulations and eco-conscious purchasing behavior continue to strengthen demand for sustainable cookware solutions.

Stainless Steel Cookware Market Drivers

Growing Consumer Preference for Healthy and Durable Cookware

Rising consumer awareness regarding food safety and chemical exposure is one of the strongest growth drivers for the stainless steel cookware market. Consumers are increasingly moving away from low-grade non-stick cookware due to concerns regarding coating degradation and toxic emissions at high temperatures. Stainless steel cookware offers a non-reactive cooking surface, corrosion resistance, and superior durability, making it highly attractive for health-conscious households. Increasing adoption of healthy cooking practices, premium kitchen upgrades, and long-term value purchasing behavior continues supporting global demand growth.

Expansion of Home Cooking and Commercial Foodservice Infrastructure

The expansion of home cooking culture and commercial foodservice industries is significantly driving market demand. Residential consumers are increasingly investing in premium cookware products due to growing culinary interest, digital cooking content, and kitchen remodeling activities. Simultaneously, restaurants, hotels, institutional kitchens, and cloud kitchens are increasing adoption of stainless steel cookware because of its durability, hygiene compliance, and lower maintenance requirements. Rapid growth in online food delivery ecosystems and hospitality infrastructure investments across Asia-Pacific and the Middle East are further accelerating commercial demand.

Stainless Steel Cookware Market Restraints

Volatility in Stainless Steel and Nickel Prices

Raw material price volatility remains a major challenge for cookware manufacturers globally. Stainless steel cookware production depends heavily on steel, nickel, chromium, and aluminum prices, which are subject to geopolitical tensions, mining supply disruptions, and energy market fluctuations. Rising metal costs directly increase manufacturing expenses and compress profit margins for manufacturers. Premium cookware brands often pass on higher costs to consumers, but entry-level manufacturers face significant pricing pressure in highly competitive markets.

Intense Competition from Unorganized and Low-Cost Manufacturers

The global stainless steel cookware market remains highly fragmented, with strong competition from regional and unorganized manufacturers, especially in developing economies. Low-cost producers often compete aggressively on price, limiting profit margins for branded players. Counterfeit cookware products and inconsistent quality standards in certain emerging markets also create challenges for organized manufacturers. In addition, product commoditization within economy cookware categories makes differentiation difficult, requiring continuous innovation in design, branding, and technology.

Stainless Steel Cookware Market Opportunities

Rising Adoption of Induction Cooking Systems

The increasing global adoption of induction cooking technology presents a major growth opportunity for stainless steel cookware manufacturers. Governments and utility providers are promoting induction cooktops because of their energy efficiency and lower carbon emissions. Induction cooking systems require magnetic cookware compatibility, directly supporting demand for stainless steel products. Manufacturers capable of offering affordable induction-ready cookware collections are expected to benefit significantly from replacement demand across residential kitchens, particularly in Europe, China, India, and North America.

Growth of Premium and Smart Kitchen Ecosystems

The rapid expansion of premium kitchen ecosystems and modular home designs is creating strong opportunities for technologically advanced cookware products. Consumers increasingly prefer cookware that integrates with modern kitchen aesthetics while offering enhanced cooking performance. Premium stainless steel cookware with stackable designs, ergonomic features, multi-layer construction, and dishwasher-safe compatibility is gaining popularity among urban households. Manufacturers are also leveraging direct-to-consumer platforms, social media marketing, and chef collaborations to target affluent consumers seeking premium culinary experiences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.95 Billion |

| Market Size in 2026 | USD 9.51 Billion |

| Market Size in 2031 | USD 12.91 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pots and pans dominate the stainless steel cookware market, accounting for nearly 41% of global revenue in 2025. Frying pans, sauté pans, and stock pots remain the most widely purchased cookware products due to their versatility across residential and commercial cooking applications. Cookware sets are gaining significant traction among urban consumers because they provide uniform aesthetics, bundled value pricing, and compatibility across modern kitchen systems. Pressure cookers continue witnessing strong demand in Asia-Pacific, particularly in India, where stainless steel pressure cookers remain essential household kitchen products. Specialty cookware products such as woks, Dutch ovens, and grill pans are also expanding steadily due to growing international culinary adoption and home gourmet cooking trends.

Material Composition Insights

18/10 stainless steel cookware leads the market, contributing nearly 36% of global revenues because of its superior corrosion resistance, polished appearance, and premium performance characteristics. Tri-ply and multi-clad cookware segments are among the fastest-growing categories, driven by rising consumer demand for improved heat distribution and professional-grade cooking performance. Stainless steel cookware with aluminum or copper cores is increasingly popular among premium consumers and commercial kitchens due to enhanced thermal conductivity. Entry-level 18/0 cookware continues maintaining strong demand in price-sensitive markets because of affordability and mass-market accessibility.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel for stainless steel cookware, accounting for nearly 40% of total market sales. Consumers continue preferring physical retail stores for cookware purchases because of direct product inspection, bundled offers, and brand comparison opportunities. However, online retail and direct-to-consumer channels are witnessing the fastest growth globally. E-commerce platforms are transforming cookware sales through digital product demonstrations, influencer marketing, competitive pricing, and wider product accessibility. Brand-owned online stores are increasingly enabling manufacturers to improve margins, strengthen customer engagement, and launch premium product collections directly to consumers.

End-Use Insights

Residential households represent the largest end-use segment in the stainless steel cookware market, accounting for nearly 67% of global demand in 2025. Urbanization, rising disposable income, and increasing investments in modular kitchens continue supporting residential cookware purchases globally. Commercial foodservice is the fastest-growing end-use segment, driven by expansion in restaurants, hotels, cloud kitchens, and institutional catering operations. Stainless steel cookware is increasingly preferred in commercial kitchens because of durability, hygiene compliance, and compatibility with high-temperature cooking environments. Healthcare institutions, educational facilities, and corporate cafeterias are also emerging as important institutional buyers of industrial-grade cookware products.

Price Range Insights

Mid-range stainless steel cookware dominates the market with nearly 45% share due to its balance between affordability and branded quality perception. Consumers increasingly prefer mid-range cookware that combines durability with modern design features. Premium cookware categories are witnessing faster growth rates, especially across developed markets, due to rising consumer willingness to invest in long-lasting kitchen products. Luxury and chef-grade cookware products are expanding strongly among affluent consumers, culinary enthusiasts, and hospitality businesses seeking professional cooking performance and superior aesthetics.

Explore more data points, trends and opportunities Download Free Sample Report

Stainless Steel Cookware Market Segmentations

By Product Type

- Pots

- Pans

- Pressure Cookers

- Casseroles & Dutch Ovens

- Steamers & Multi-cook Vessels

- Bakeware

- Specialty Cookware

- Cookware Sets

By Material Composition

- 18/10 Stainless Steel

- 18/8 Stainless Steel

- 18/0 Stainless Steel

- Tri-ply Stainless Steel

- Five-ply & Multi-clad Stainless Steel

- Stainless Steel with Aluminum Core

- Stainless Steel with Copper Core

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Kitchenware Stores

- Department Stores

- Online Retail/E-commerce

- Brand-owned Retail Stores

- Direct-to-consumer Channels

By End User

- Residential Households

- Restaurants

- Hotels & Resorts

- Cloud Kitchens

- Institutional Kitchens

- Hospitals & Educational Facilities

Regional Insights

Asia-Pacific

Asia-Pacific dominates the stainless steel cookware market with approximately 39–40% share of global revenue in 2025. China remains the world’s largest manufacturing and consumption hub due to integrated stainless steel supply chains, rising middle-class consumption, and extensive domestic appliance demand. India is emerging as one of the fastest-growing markets globally, supported by urbanization, rising household income, growth in modular kitchens, and increasing penetration of branded cookware products. Japan and South Korea continue representing strong premium cookware markets with high demand for technologically advanced and aesthetically refined cookware collections. Southeast Asia is also witnessing steady demand growth due to expanding retail infrastructure and rising urban population.

North America

North America accounts for nearly 17–18% of global market demand and remains a key premium cookware consumption region. The United States dominates regional revenues because of strong consumer spending on kitchen remodeling, high penetration of branded cookware, and rising adoption of induction-compatible products. Commercial foodservice infrastructure across the U.S. remains a major contributor to cookware demand. Canada also demonstrates strong market growth due to increasing preference for sustainable and long-lasting cookware products among environmentally conscious consumers.

Europe

Europe contributes approximately 28–30% of global stainless steel cookware revenues and remains one of the most mature premium cookware markets worldwide. Germany, France, Italy, and the United Kingdom represent the largest regional markets. European consumers strongly prioritize recyclable and sustainable cookware products, supporting long-term stainless steel cookware demand. The region is also witnessing rapid adoption of induction cooking systems in response to energy efficiency initiatives and changing household appliance preferences. Italy remains a major manufacturing center for premium cookware brands, while Germany leads regional consumption of professional-grade kitchen products.

Latin America

Latin America accounts for nearly 7–8% of the global market, led primarily by Brazil and Mexico. Rising urbanization, expanding retail penetration, and increasing preference for modern kitchenware products are supporting regional demand growth. Brazilian consumers are increasingly adopting branded cookware products as disposable incomes improve. Mexico is witnessing rising demand due to expansion in organized retail and e-commerce channels. However, currency volatility and import dependence continue creating pricing challenges across several Latin American economies.

Middle East & Africa

The Middle East & Africa region contributes nearly 5% of global demand and is experiencing steady growth driven by hospitality investments and rising premium housing development. GCC countries including Saudi Arabia and the UAE are witnessing strong demand for premium cookware products due to luxury lifestyle trends and expanding tourism infrastructure. South Africa remains the largest Sub-Saharan African market because of stronger urban retail networks and rising middle-class consumption. Commercial cookware demand is also increasing steadily across hotels, restaurants, and institutional kitchens throughout the region.

Key Players in the Stainless Steel Cookware Market

- Groupe SEB

- Meyer Corporation

- All-Clad

- Zwilling J.A. Henckels

- Cuisinart

- Calphalon

- Fissler

- Le Creuset

- KitchenAid

- Tramontina

- TTK Prestige

- Hawkins Cookers

- Vinod Cookware

- WMF Group

- BergHOFF