Shampoo Market Size

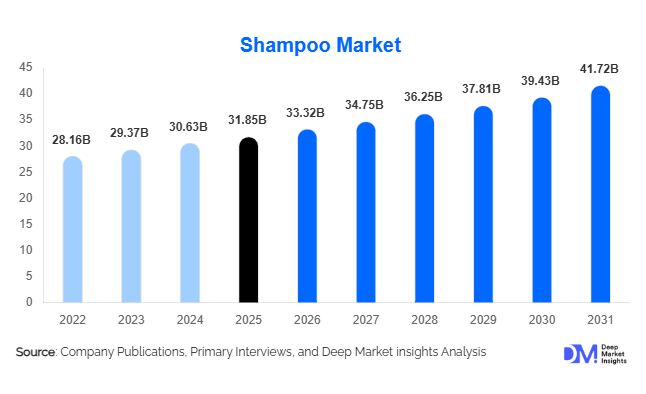

According to Deep Market Insights, the global shampoo market size was valued at USD 31.85 billion in 2025 and is projected to grow from USD 33.32 billion in 2026 to reach USD 41.72 billion by 2031, expanding at a CAGR of 4.3% during the forecast period (2026–2031). The shampoo market growth is primarily driven by rising consumer awareness regarding scalp health, increasing demand for specialized haircare solutions, growing adoption of premium and natural formulations, and expanding e-commerce penetration. The industry continues to evolve beyond basic cleansing products toward treatment-oriented formulations that address hair fall, dandruff, scalp sensitivity, color protection, hydration, and hair repair requirements.

Key Market Insights

- Scalp-health-focused shampoos are becoming a major growth category, driven by increasing consumer awareness of hair wellness and preventive haircare.

- Natural, organic, sulfate-free, and clean-label shampoos are witnessing rapid adoption, particularly among premium consumers in North America and Europe.

- Asia-Pacific dominates the global shampoo market, supported by large population bases, rising disposable incomes, and expanding urbanization.

- India and Southeast Asia represent the fastest-growing regional markets, benefiting from rising beauty expenditures and growing penetration of branded haircare products.

- E-commerce and direct-to-consumer channels are transforming market accessibility, allowing brands to target consumers through personalized recommendations and digital marketing.

- Biotechnology-based ingredients and dermatologically tested formulations are emerging as key innovation areas across premium shampoo categories.

Shampoo Market Trends

Growing Demand for Scalp Health and Therapeutic Haircare

The global shampoo industry is increasingly shifting toward scalp-health-focused solutions as consumers become more aware of the relationship between scalp condition and overall hair quality. Products formulated with probiotics, peptides, niacinamide, salicylic acid, botanical extracts, and microbiome-friendly ingredients are gaining popularity. Brands are positioning shampoos as treatment solutions rather than simple cleansing products, leading to increased demand for anti-hair-loss, anti-dandruff, anti-inflammatory, and sensitive-scalp formulations. Dermatologist-endorsed products are becoming mainstream, particularly among consumers experiencing hair thinning, stress-related hair loss, and environmental damage caused by pollution and lifestyle factors.

Premiumization and Clean Beauty Adoption

Consumers worldwide are demonstrating a willingness to spend more on premium shampoos that offer superior efficacy, ingredient transparency, and sustainability credentials. Sulfate-free, silicone-free, vegan, cruelty-free, and organic formulations are becoming standard offerings across both established brands and emerging market entrants. Sustainable packaging innovations, including refill packs, biodegradable materials, and shampoo bars, are further supporting consumer demand. Premium haircare brands are increasingly leveraging biotechnology-derived ingredients and clinically validated claims to differentiate their products, creating a higher-value product mix and stronger profit margins across the industry.

Shampoo Market Drivers

Rising Awareness of Hair Health and Personal Grooming

Consumers increasingly view haircare as an essential component of personal wellness and appearance. Rising concerns regarding hair loss, scalp irritation, dandruff, pollution-related damage, and aging hair have accelerated demand for specialized shampoos. Growing social media influence, beauty education, and professional recommendations have further encouraged consumers to adopt targeted shampoo solutions designed for specific hair and scalp conditions. This trend has expanded the premium and therapeutic shampoo segments globally.

Expansion of Premium Haircare Products

Premiumization remains one of the strongest drivers shaping the shampoo market. Consumers are shifting away from generic products toward formulations containing keratin, argan oil, amino acids, botanical extracts, collagen, and advanced conditioning agents. Professional salon-inspired shampoos are experiencing increased adoption as consumers seek salon-quality results at home. Premium products generate significantly higher margins for manufacturers, encouraging continuous investments in product innovation and brand positioning.

Shampoo Market Restraints

Volatility in Raw Material and Packaging Costs

The shampoo industry remains exposed to fluctuations in surfactant prices, specialty chemicals, fragrances, preservatives, packaging materials, and transportation costs. Rising costs can place pressure on manufacturers' margins, particularly within price-sensitive emerging markets where passing cost increases directly to consumers may not always be feasible. Manufacturers continue investing in supply chain optimization and local sourcing strategies to mitigate these challenges.

Market Saturation in Developed Economies

Many developed markets such as the United States, Canada, Western Europe, Japan, and Australia have reached high levels of shampoo penetration. As a result, volume growth opportunities are limited, forcing companies to compete primarily through innovation, premiumization, and marketing initiatives. Intense competition among established brands creates challenges for both incumbent manufacturers and new market entrants attempting to gain market share.

Shampoo Market Opportunities

Expansion of Natural and Organic Haircare

The increasing consumer preference for clean-label personal care products presents significant opportunities for shampoo manufacturers. Organic, herbal, sulfate-free, and plant-based shampoos continue gaining traction among consumers seeking safer and environmentally responsible products. Companies capable of offering certified organic formulations, transparent ingredient sourcing, and sustainable manufacturing practices are well-positioned to capture premium market segments and expand their customer base globally.

Emerging Market Premiumization

Rapid economic development in countries such as India, Indonesia, Vietnam, Brazil, Mexico, and South Africa is creating substantial growth opportunities. Rising disposable incomes, urbanization, and increasing beauty awareness are encouraging consumers to upgrade from basic haircare products to specialized and premium formulations. Manufacturers are leveraging localized products, affordable premium pricing strategies, and smaller package formats to improve market penetration while simultaneously expanding premium offerings for affluent urban consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 31.85 Billion |

| Market Size in 2026 | USD 33.32 Billion |

| Market Size in 2031 | USD 41.72 Billion |

| CAGR | 4.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Regular or daily-use shampoos continue to dominate the global market, accounting for approximately 29% of total revenue due to their broad consumer appeal and high purchase frequency. Anti-dandruff shampoos represent one of the largest specialized categories, supported by increasing scalp health awareness and widespread prevalence of dandruff-related concerns. Hair fall control shampoos are experiencing strong growth, particularly across Asia-Pacific markets where consumers increasingly seek preventive haircare solutions. Moisturizing and repair shampoos are benefiting from rising incidences of hair damage caused by chemical treatments, heat styling, and environmental stressors. Meanwhile, dry shampoos and sulfate-free formulations are emerging as high-growth segments due to changing lifestyles and increasing demand for convenience-oriented and clean-label products.

Ingredient Category Insights

Natural and botanical shampoos account for the largest share within the specialty ingredient segment, representing approximately 24% of global shampoo sales. Consumers increasingly prefer formulations containing aloe vera, tea tree oil, coconut oil, rosemary, argan oil, and other plant-derived ingredients. Sulfate-free and paraben-free shampoos are rapidly gaining adoption among health-conscious consumers seeking gentler alternatives to conventional products. Vegan and cruelty-free formulations are becoming increasingly important purchasing considerations, particularly among younger demographics in North America and Europe. Protein- and keratin-based shampoos continue expanding due to their perceived effectiveness in strengthening damaged hair and improving overall hair quality.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 39% of global shampoo sales due to extensive product availability and strong consumer accessibility. Pharmacies and drug stores continue performing well in medicated and therapeutic shampoo categories, where professional recommendations influence purchasing decisions. Specialty beauty retailers maintain strong positions within premium product segments. E-commerce represents the fastest-growing distribution channel, driven by product variety, convenience, personalized recommendations, subscription models, and direct-to-consumer marketing strategies. Manufacturers are increasingly investing in digital platforms and omnichannel strategies to strengthen consumer engagement and improve conversion rates.

Consumer Group Insights

Women remain the largest consumer segment, accounting for approximately 57% of global shampoo demand. Higher product usage frequency, greater adoption of specialized formulations, and stronger engagement with premium haircare routines contribute to segment dominance. Men's grooming products are expanding steadily as male consumers become increasingly focused on hair health, scalp care, and personal appearance. Children's and baby shampoos continue benefiting from growing parental preference for mild, hypoallergenic, and dermatologist-tested formulations. Unisex products are also gaining traction as brands simplify product portfolios and focus on scalp-health positioning rather than gender-specific marketing.

Explore more data points, trends and opportunities Download Free Sample Report

Shampoo Market Segmentations

By Product Type

- Regular/Daily Use Shampoo

- Anti-Dandruff Shampoo

- Hair Fall Control Shampoo

- Moisturizing/Hydrating Shampoo

- Repair & Damage Control Shampoo

- Volumizing Shampoo

- Color Protection Shampoo

- Clarifying/Deep Cleansing Shampoo

- Baby Shampoo

- Medicated/Therapeutic Shampoo

- 2-in-1 Shampoo & Conditioner

- Dry Shampoo

- Sulfate-Free Shampoo

- Organic/Natural/Herbal Shampoo

By Ingredient Category

- Synthetic Formulation Shampoo

- Natural & Botanical Shampoo

- Organic Certified Shampoo

- Sulfate-Free Shampoo

- Silicone-Free Shampoo

- Paraben-Free Shampoo

- Vegan Shampoo

- Protein/Keratin-Based Shampoo

By Hair Type

- Normal Hair

- Dry Hair

- Oily Hair

- Curly Hair

- Straight Hair

- Chemically Treated Hair

- Colored Hair

- Sensitive Scalp Hair

By Consumer Group

- Men

- Women

- Children/Babies

- Unisex

By Price Category

- Economy

- Mid-Range

- Premium

- Luxury/Professional Salon Grade

Regional Insights

Asia-Pacific

Asia-Pacific dominated the global shampoo market in 2025, accounting for approximately 39% of total market revenue. The region is expected to remain the largest and fastest-growing market throughout the forecast period. China represents the largest regional market, contributing nearly 13% of global demand, followed by India with approximately 8% market share. Japan, South Korea, Indonesia, Thailand, Vietnam, and the Philippines also represent significant consumption centers. The region's dominance is primarily driven by its large population base, rapid urbanization, rising disposable incomes, and increasing consumer awareness regarding personal grooming and hair health. Growing middle-class populations across India, China, and Southeast Asia are upgrading from unbranded products to premium and specialized shampoo formulations. In addition, the widespread availability of affordable sachet packaging has significantly improved product penetration in developing economies.

Country-specific growth drivers vary across the region. In China, premiumization, scalp-health awareness, and demand for anti-hair-loss products continue to fuel market expansion. India is experiencing strong growth due to rising rural penetration, increasing female workforce participation, and growing demand for herbal and ayurvedic haircare products. Japan and South Korea are leading innovation in premium, dermatologist-tested, and functional shampoos, while Southeast Asian countries are benefiting from expanding retail infrastructure, increasing internet penetration, and rapid growth in e-commerce beauty sales. The region is also witnessing increasing demand for natural, sulfate-free, and environmentally sustainable formulations as consumers become more ingredient-conscious.

North America

North America accounted for approximately 28% of global shampoo market revenue in 2025, making it the second-largest regional market. The United States dominates regional demand and contributes nearly 24% of global market consumption, while Canada represents a mature but steadily growing market. The region's growth is primarily supported by strong consumer spending on personal care products, high adoption of premium haircare solutions, and increasing demand for scientifically validated formulations. Consumers increasingly seek shampoos that address specific concerns such as scalp sensitivity, hair thinning, color protection, hydration, and anti-aging haircare. As a result, premium and therapeutic shampoo categories continue to outperform conventional products.

Another major growth driver is the rapid expansion of direct-to-consumer (D2C) brands and e-commerce channels, which enable personalized product recommendations and subscription-based purchasing models. Sustainability trends are also influencing purchasing decisions, with consumers showing strong preference for refillable packaging, clean-label ingredients, vegan formulations, and cruelty-free certifications. Furthermore, the growing multicultural population in the United States is increasing demand for specialized products designed for curly, textured, and ethnic hair types, creating new growth opportunities for manufacturers.

Europe

Europe represented approximately 24% of global shampoo market demand in 2025, with Germany, the United Kingdom, France, Italy, and Spain serving as the region's largest markets. The European market is characterized by high consumer awareness regarding ingredient safety, sustainability, and product performance. One of the strongest growth drivers in Europe is the increasing preference for organic, vegan, natural, and environmentally sustainable haircare products. Consumers are willing to pay premium prices for products that offer transparency regarding ingredient sourcing, ethical manufacturing, and environmental impact. Consequently, sulfate-free, silicone-free, and biodegradable shampoo formulations are experiencing significant growth across the region.

Stringent regulatory standards governing cosmetic ingredients and product labeling further support market expansion by increasing consumer confidence. Germany continues to lead demand for natural and organic personal care products, while the United Kingdom is witnessing strong growth in premium salon-quality haircare. France remains a major center for luxury beauty products and innovation, while Southern European markets are benefiting from growing demand for moisturizing and repair-focused shampoos designed to address climate-related hair concerns. The region is also experiencing increased adoption of sustainable packaging solutions, supporting premium product positioning and long-term market growth.

Latin America

Latin America accounted for approximately 6% of global shampoo market revenue in 2025, with Brazil serving as the region's largest and most influential market. Mexico and Argentina are also important contributors to regional demand. The region benefits from one of the highest levels of consumer engagement with beauty and personal care products globally. Haircare routines are deeply embedded within consumer lifestyles, resulting in relatively high per-capita shampoo consumption compared to several other emerging regions. Brazilian consumers, in particular, are highly focused on hair aesthetics, driving strong demand for hair repair, moisturizing, anti-frizz, and treatment-based formulations.

Market growth is supported by increasing urbanization, rising disposable incomes, and expanding availability of branded haircare products through modern retail and digital commerce channels. The growing popularity of salon treatments and chemically treated hair has increased demand for specialized shampoos designed for color protection, keratin maintenance, and damage repair. In addition, international manufacturers continue expanding their presence across Latin America through localized product offerings tailored to regional hair textures and climate conditions.

Middle East & Africa

The Middle East and Africa collectively accounted for approximately 3% of global shampoo market demand in 2025. While the region currently represents a relatively smaller share of global revenue, it is expected to experience steady growth throughout the forecast period. Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria represent the largest and most attractive markets within the region. Market expansion is primarily driven by rapid urbanization, population growth, rising disposable incomes, and increasing consumer awareness regarding personal grooming. The Middle East, particularly the Gulf Cooperation Council (GCC) countries, benefits from high purchasing power and strong demand for premium international beauty brands. Consumers increasingly seek luxury haircare products, salon-grade formulations, and specialized treatments designed to address hair damage caused by harsh climatic conditions and frequent styling practices.

In Africa, expanding retail infrastructure and improving product accessibility are contributing to market growth. Countries such as South Africa and Nigeria are witnessing increasing demand for shampoos formulated for textured and curly hair types, while multinational manufacturers continue introducing affordable product variants to increase market penetration. Growth in e-commerce platforms, rising beauty awareness among younger consumers, and ongoing investments by global personal care companies are expected to further strengthen regional demand over the coming years.

Key Players in the Shampoo Market

- Procter & Gamble

- Unilever

- L'Oréal

- Henkel

- Kao Corporation

- Shiseido

- Amway

- Natura &Co

- Beiersdorf

- Johnson & Johnson

- Revlon

- Oriflame

- The Estée Lauder Companies

- Davines

- Moroccanoil