Plastic Pallets Market Size

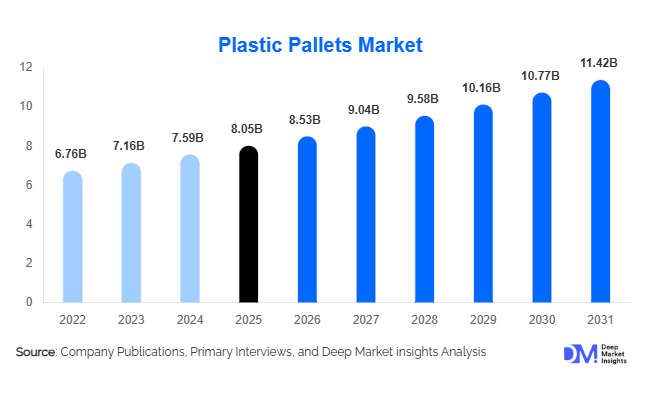

According to Deep Market Insights, the global plastic pallets market size was valued at USD 8.05 billion in 2025 and is projected to grow from USD 8.53 billion in 2026 to reach USD 11.42 billion by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The plastic pallets market growth is primarily driven by increasing adoption of automated warehousing systems, growing demand for hygienic material handling solutions in food and pharmaceutical industries, and rising preference for reusable and sustainable logistics equipment. As global supply chains continue to modernize, plastic pallets are increasingly replacing conventional wooden pallets due to their durability, moisture resistance, longer service life, and compatibility with automated handling technologies.

Key Market Insights

- Reusable plastic pallets account for more than 70% of market demand, driven by sustainability initiatives and lifecycle cost advantages over wooden alternatives.

- HDPE-based pallets dominate material consumption, representing nearly 68% of total market revenue due to superior durability, impact resistance, and chemical stability.

- Asia-Pacific leads the global market, accounting for approximately 38% of global demand, supported by manufacturing expansion and logistics infrastructure investments.

- India and Southeast Asia are among the fastest-growing markets, benefiting from industrialization, export growth, and warehouse modernization.

- Food & Beverage remains the largest end-use segment, accounting for approximately 23% of global market revenues in 2025.

- Smart pallet technologies, including RFID-enabled tracking, IoT integration, and warehouse automation compatibility, are emerging as major innovation areas.

Plastic Pallets Market Trends

Growing Adoption of Recycled Plastic Pallets

Sustainability objectives across industries are accelerating the adoption of recycled plastic pallets. Manufacturers are increasingly utilizing recycled HDPE and polypropylene resins to reduce production costs and environmental impact while meeting corporate ESG commitments. Large retailers, food manufacturers, and logistics companies are implementing circular economy strategies that prioritize reusable and recyclable material handling products. Recycled-content pallets are becoming particularly popular in Europe and North America, where environmental regulations and sustainability reporting requirements continue to intensify. Several pallet manufacturers are investing in closed-loop recycling programs that recover end-of-life pallets and convert them into new products, reducing dependence on virgin polymers and strengthening long-term supply chain sustainability.

Automation-Compatible Pallets Becoming Industry Standard

The rapid expansion of warehouse automation and Industry 4.0 logistics is increasing demand for dimensionally consistent plastic pallets. Automated storage and retrieval systems (ASRS), robotic fulfillment centers, conveyor systems, and autonomous guided vehicles require pallets with uniform specifications and high structural integrity. Plastic pallets provide superior compatibility compared to wooden alternatives, making them increasingly preferred in highly automated facilities. Manufacturers are introducing lightweight designs, reinforced structures, and embedded RFID technologies to improve traceability and warehouse efficiency. As global investments in automated logistics continue to rise, demand for automation-grade plastic pallets is expected to accelerate significantly during the forecast period.

Plastic Pallets Market Drivers

Expansion of E-Commerce and Modern Warehousing

The continued growth of e-commerce and omnichannel retailing is driving substantial investments in warehouses, fulfillment centers, and distribution networks worldwide. Plastic pallets provide operational advantages through enhanced durability, reduced maintenance requirements, and compatibility with high-speed logistics systems. Major retailers and third-party logistics providers are increasingly standardizing plastic pallet usage to improve supply chain efficiency and reduce long-term operating costs.

Increasing Demand for Hygienic Material Handling Solutions

Food processing, pharmaceutical manufacturing, and healthcare logistics industries require contamination-free transportation and storage systems. Plastic pallets offer resistance to moisture, pests, mold, and bacterial growth, making them highly suitable for regulated environments. Strict food safety regulations and pharmaceutical compliance standards continue to drive replacement demand for plastic pallets globally. Growing vaccine distribution networks, biologics manufacturing, and cold-chain logistics are further strengthening demand from healthcare applications.

Plastic Pallets Market Restraints

Higher Initial Purchase Costs Compared to Wooden Pallets

Despite offering superior lifecycle economics, plastic pallets require significantly higher upfront investment than traditional wooden pallets. Small and medium-sized enterprises often prioritize lower acquisition costs, limiting adoption rates in cost-sensitive markets. The price differential remains one of the primary barriers to broader penetration, particularly in developing economies where capital expenditure budgets remain constrained.

Volatility in Raw Material Prices

Plastic pallet manufacturing relies heavily on petrochemical-based resins such as HDPE and polypropylene. Fluctuations in crude oil prices, supply chain disruptions, and resin shortages can significantly impact manufacturing costs and profit margins. Manufacturers must continuously manage procurement strategies and pricing structures to mitigate the effects of resin market volatility, which remains a key challenge for industry participants.

Plastic Pallets Market Opportunities

Expansion of Circular Economy and Sustainable Logistics Programs

Governments and multinational corporations are increasingly implementing sustainability initiatives aimed at reducing waste and improving resource efficiency. Plastic pallets align well with these objectives due to their reusability, recyclability, and long operational lifespan. Manufacturers capable of offering high recycled-content products, take-back programs, and closed-loop recycling systems are expected to benefit significantly from growing sustainability investments across logistics and manufacturing industries.

Emerging Market Manufacturing and Export Growth

Rapid industrialization in countries such as India, Vietnam, Indonesia, Saudi Arabia, and Mexico is creating substantial demand for advanced material handling equipment. Export-oriented industries including pharmaceuticals, electronics, automotive components, chemicals, and food processing increasingly require durable pallets that comply with international shipping standards. Plastic pallets eliminate phytosanitary treatment requirements associated with wood pallets, making them attractive for export supply chains. Establishing regional production facilities in these high-growth markets presents significant opportunities for both existing manufacturers and new entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.05 Billion |

| Market Size in 2026 | USD 8.53 Billion |

| Market Size in 2031 | USD 11.42 Billion |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

HDPE pallets dominate the market, accounting for approximately 68% of total revenues in 2025. Their superior strength, impact resistance, moisture tolerance, and chemical stability make them the preferred choice across food processing, pharmaceutical, and industrial applications. Polypropylene pallets represent the second-largest segment, benefiting from lightweight properties and enhanced dimensional stability. Recycled plastic pallets are experiencing the fastest growth as companies pursue sustainability objectives and seek lower-carbon logistics solutions. Growing investments in recycled resin technologies are expected to further expand this segment's market share during the forecast period.

Structural Design Insights

Nestable plastic pallets account for approximately 43% of global demand and represent the largest structural design segment. Their ability to reduce storage space requirements and lower transportation costs makes them highly attractive for retail distribution, export logistics, and warehouse operations. Rackable pallets continue to gain market share due to rising adoption within automated warehouses and high-density storage facilities. Stackable and hygienic solid-deck pallets remain important segments, particularly in pharmaceutical, food processing, and cleanroom environments where hygiene and product protection are critical operational requirements.

Manufacturing Process Insights

Injection molded plastic pallets hold the leading position with approximately 52% market share due to their superior structural consistency, scalability, and cost efficiency in high-volume production. Injection molding enables manufacturers to produce highly precise pallet designs suitable for automated material handling environments. Blow molded pallets are increasingly used in heavy-duty applications requiring enhanced impact resistance and durability. Thermoformed and rotational molded pallets serve specialized applications where lightweight construction, custom dimensions, or unique performance characteristics are required.

End-Use Industry Insights

Food and beverage remains the largest end-use industry, contributing approximately 23% of global plastic pallet demand. The sector relies heavily on hygienic material handling systems that comply with stringent food safety regulations. Pharmaceuticals represent the fastest-growing segment, supported by rising biologics production, vaccine distribution, and cold-chain logistics investments. Retail and e-commerce continue to generate significant demand due to expanding fulfillment center networks and warehouse automation initiatives. Automotive, chemicals, electronics, and industrial manufacturing sectors also contribute substantial demand, particularly in export-oriented economies where durable logistics equipment is essential for efficient supply chain operations.

Explore more data points, trends and opportunities Download Free Sample Report

Plastic Pallets Market Segmentations

By Material Type

- High-Density Polyethylene (HDPE)

- Polypropylene (PP)

- Low-Density Polyethylene (LDPE)

- Recycled Plastic Resins

- Other Engineering Plastics

By Structural Design

- Nestable Plastic Pallets

- Rackable Plastic Pallets

- Stackable Plastic Pallets

- Export/One-Way Plastic Pallets

- Hygienic/Solid-Deck Plastic Pallets

- Drum Plastic Pallets

By Manufacturing Process

- Injection Molded Plastic Pallets

- Blow Molded Plastic Pallets

- Thermoformed Plastic Pallets

- Rotational Molded Plastic Pallets

By Deck Configuration

- Open Deck Plastic Pallets

- Closed Deck Plastic Pallets

By Load Capacity

- Light Duty (<1 Ton)

- Medium Duty (1–2 Tons)

- Heavy Duty (>2 Tons)

By Reusability

- Reusable Plastic Pallets

- Single-Use/Export Plastic Pallets

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Chemicals & Petrochemicals

- Retail & E-commerce

- Logistics & Warehousing

- Automotive

- Electronics & Electricals

- Agriculture & Fresh Produce

- Consumer Goods & FMCG

- Industrial Manufacturing

By Distribution Model

- Direct Sales

- Pallet Pooling & Rental Services

- Distributor/Channel Sales

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global plastic pallets market with approximately 38% share in 2025. China remains the largest country market due to its massive manufacturing base, export activities, and logistics infrastructure investments. India is emerging as one of the fastest-growing markets globally, supported by industrialization, warehousing expansion, and government-led manufacturing initiatives. Japan and South Korea maintain strong demand from automotive, electronics, and industrial sectors, while Southeast Asia continues to benefit from growing foreign direct investment and supply chain diversification strategies.

North America

North America accounts for approximately 28% of global market demand, led primarily by the United States. Warehouse automation investments, pharmaceutical manufacturing growth, and mature logistics infrastructure continue to support plastic pallet adoption. Canada contributes demand through food processing, agriculture exports, and industrial manufacturing activities, while Mexico benefits from growing automotive exports and increasing integration within North American supply chains.

Europe

Europe represents approximately 26% of global market revenues. Germany leads regional demand due to its strong industrial manufacturing base and extensive export network. France, the United Kingdom, Italy, Spain, and Benelux countries continue to witness steady growth driven by sustainability initiatives, food processing activities, and advanced logistics infrastructure. European regulations promoting circular economy practices are accelerating adoption of reusable and recycled plastic pallets across the region.

Latin America

Latin America accounts for approximately 5% of global demand, with Brazil representing the largest market. Agricultural exports, food processing industries, and manufacturing expansion continue to support demand growth. Mexico also plays an increasingly important role due to its growing automotive and industrial export sectors.

Middle East & Africa

The Middle East and Africa region accounts for approximately 3% of global market revenues but is expected to record one of the fastest growth rates during the forecast period. Saudi Arabia and the UAE are investing heavily in logistics infrastructure, industrial diversification, and warehousing capacity expansion. South Africa remains the largest market in Sub-Saharan Africa, supported by manufacturing, mining, and retail distribution activities.

Key Players in the Plastic Pallets Market

- ORBIS Corporation

- Schoeller Allibert

- Cabka Group

- Craemer Holding

- Rehrig Pacific Company

- Monoflo International

- Greystone Logistics

- IPL Plastics

- Bekuplast GmbH

- Q-Pall

- Faber Halbertsma Group

- Nefab Group

- Loscam

- Brambles Limited

- TranPak Inc.