Paper Towels Market Size

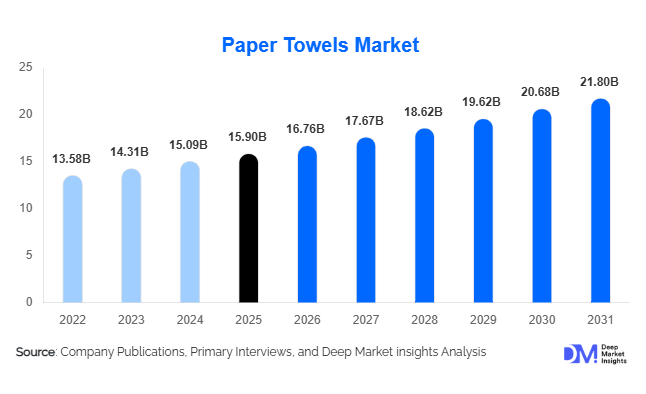

According to Deep Market Insights, the global paper towels market size was valued at USD 15.9 billion in 2025 and is projected to grow from USD 16.76 billion in 2026 to reach USD 21.80 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The paper towels market growth is primarily driven by increasing hygiene awareness across residential and commercial sectors, rising demand for disposable cleaning products, expanding healthcare and hospitality infrastructure, and the growing adoption of premium and sustainable tissue products. The market continues to benefit from long-term behavioral changes related to cleanliness and sanitation, while manufacturers are investing heavily in recycled fiber technologies, premium absorbency solutions, and environmentally responsible production methods.

Key Market Insights

- Commercial and institutional facilities account for the largest share of global demand, driven by offices, healthcare facilities, hotels, restaurants, airports, and educational institutions.

- Rolled paper towels remain the dominant product category, representing approximately 38% of global market revenue due to their widespread household and commercial usage.

- North America leads the global market, accounting for nearly 34% of total revenue, supported by high per-capita consumption and established hygiene practices.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, healthcare investments, and growing disposable income across China, India, and Southeast Asia.

- Sustainability initiatives are reshaping procurement decisions, leading to higher demand for recycled-content, FSC-certified, and bamboo-based paper towel products.

- Technological advancements in smart dispensing systems are helping commercial users reduce waste, optimize inventory management, and improve hygiene compliance.

Paper Towels Market Trends

Sustainable Fiber Adoption Accelerating Across Global Markets

Environmental concerns and corporate sustainability commitments are driving significant adoption of recycled fiber and alternative-fiber paper towels. Institutional buyers, particularly multinational corporations, healthcare providers, and hospitality chains, are increasingly integrating sustainability metrics into procurement decisions. Manufacturers are responding by expanding portfolios featuring recycled pulp, bamboo fibers, and certified sustainable wood pulp. Governments across Europe and North America continue promoting sustainable packaging and tissue products through regulatory initiatives, further encouraging the transition toward environmentally responsible paper towel solutions. As consumers become more environmentally conscious, premium eco-friendly products are expected to gain market share throughout the forecast period.

Touchless and Smart Dispensing Technologies Gaining Momentum

Commercial facilities are increasingly investing in touchless dispensing systems to improve hygiene standards and reduce paper waste. Smart dispensers equipped with sensors and IoT capabilities provide real-time monitoring of inventory levels and usage patterns, enabling facility managers to optimize maintenance schedules and reduce operating costs. Hospitals, airports, educational institutions, and hospitality facilities are among the fastest adopters of these technologies. Integration of digital monitoring capabilities is creating opportunities for manufacturers to transition from product-based business models toward service-oriented offerings that combine consumables with facility management solutions.

Paper Towels Market Drivers

Growing Global Focus on Hygiene and Sanitation

One of the strongest growth drivers for the paper towels market is the increasing emphasis on hygiene and sanitation across both residential and commercial environments. Permanent behavioral shifts following global public health events have led to higher consumption of disposable hygiene products. Healthcare facilities, schools, restaurants, and office buildings continue implementing stricter sanitation standards, resulting in consistent demand for paper towels. Increased handwashing frequency and heightened awareness of infection prevention are expected to sustain consumption growth across developed and emerging economies.

Expansion of Foodservice, Hospitality, and Healthcare Industries

The rapid growth of foodservice establishments, hotels, hospitals, and healthcare facilities continues to drive significant demand for paper towels. Hotels, restaurants, cafes, and catering operations require large volumes of paper towels for food preparation, cleaning, and restroom maintenance. Simultaneously, healthcare facilities utilize paper towels as part of infection control and patient care protocols. Investments in hospital construction, tourism infrastructure, and hospitality development are creating long-term demand opportunities for manufacturers globally.

Paper Towels Market Restraints

Volatility in Wood Pulp and Raw Material Prices

Wood pulp remains the primary raw material used in paper towel manufacturing, making the industry highly vulnerable to fluctuations in pulp prices. Changes in forestry regulations, transportation costs, energy prices, and global supply-demand dynamics can significantly impact manufacturing costs. While premium brands can often pass increased costs to consumers, mid-tier and economy producers face margin pressure during periods of elevated raw material prices.

Environmental Concerns Associated with Disposable Products

Despite advances in sustainable manufacturing, paper towels remain disposable products that contribute to waste generation. Growing environmental awareness has encouraged some consumers and organizations to explore reusable alternatives in specific applications. Increasing regulatory scrutiny surrounding deforestation, waste management, and carbon emissions may require manufacturers to invest further in sustainable sourcing and production technologies, potentially increasing operational costs.

Paper Towels Market Opportunities

Growth of Sustainable and Premium Product Categories

The transition toward environmentally responsible products presents substantial growth opportunities for paper towel manufacturers. Demand for FSC-certified, recycled-content, compostable, and bamboo-based paper towels is growing rapidly across both consumer and institutional segments. Premium eco-friendly products command higher margins while helping organizations meet sustainability objectives. Companies that successfully balance sustainability, performance, and affordability are expected to gain competitive advantages over the coming years.

Expansion of Public Infrastructure and Institutional Facilities

Large-scale investments in healthcare facilities, airports, transportation networks, educational institutions, and commercial real estate are creating new demand centers for paper towels. Emerging economies across Asia-Pacific, the Middle East, and Latin America are expanding public sanitation infrastructure and healthcare systems, increasing consumption of institutional hygiene products. Long-term contracts with facility management providers and government agencies offer stable revenue opportunities for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.9 Billion |

| Market Size in 2026 | USD 16.76 Billion |

| Market Size in 2031 | USD 21.80 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rolled paper towels dominate the global market, accounting for approximately 38% of total revenue in 2025. Their widespread use across households, offices, restaurants, and public facilities supports strong demand globally. Standard and jumbo rolls remain particularly popular due to dispenser compatibility, ease of use, and cost efficiency. Folded paper towels represent the second-largest product category, driven primarily by institutional and commercial applications where controlled dispensing and reduced waste are priorities. Specialty paper towels featuring enhanced absorbency, decorative designs, and antimicrobial properties are gaining popularity within premium consumer segments. Industrial wiping paper towels are also experiencing growing adoption in manufacturing, automotive, and maintenance applications where durability and absorption performance are critical.

Raw Material Insights

Virgin wood pulp remains the leading raw material segment, accounting for approximately 56% of the global paper towels market revenue. Manufacturers continue to rely on virgin fibers because they offer superior softness, absorbency, and wet strength compared to alternative materials. Recycled fiber pulp represents the fastest-growing raw material category due to increasing sustainability requirements from governments, corporations, and consumers. Bamboo-based paper towels are emerging as a niche but rapidly expanding segment, particularly in North America and Europe, where environmentally conscious consumers are willing to pay premium prices for sustainable alternatives.

End-Use Insights

Commercial and institutional end users account for approximately 58% of global paper towel consumption. Offices, healthcare facilities, hotels, educational institutions, airports, and retail establishments generate substantial recurring demand due to hygiene compliance requirements. The healthcare sector remains one of the fastest-growing end-use segments, supported by expanding hospital infrastructure and infection-control protocols. Residential demand continues to grow steadily, driven by increasing household hygiene awareness and consumer preference for disposable cleaning products. Industrial manufacturing facilities are also emerging as important consumers, utilizing paper towels for equipment cleaning, maintenance operations, and contamination control procedures.

Distribution Channel Insights

Hypermarkets and supermarkets remain the dominant distribution channel, accounting for approximately 41% of global sales. Consumers frequently purchase paper towels as part of routine grocery shopping, making modern retail outlets the preferred purchasing channel. Wholesale clubs and institutional procurement networks play a significant role in commercial purchasing, particularly among hospitality and healthcare operators. E-commerce represents the fastest-growing channel, supported by subscription purchasing models, bulk ordering options, and increasing consumer preference for online shopping. Manufacturers are also strengthening direct-to-business sales channels to secure long-term institutional contracts and improve customer retention.

Explore more data points, trends and opportunities Download Free Sample Report

Paper Towels Market Segmentations

By Product Type

- Rolled Paper Towels

- Folded Paper Towels

- Boxed Paper Towels

- Kitchen Paper Towels

- Industrial Wiping Paper Towels

- Specialty Paper Towels

By Raw Material

- Virgin Wood Pulp

- Recycled Fiber Pulp

- Blended Fiber Pulp

- Bamboo-Based Fiber

- Alternative Sustainable Fibers

By Ply Structure

- Single Ply

- Double Ply

- Triple Ply and Above

By End User

- Residential Households

- Foodservice & Hospitality

- Healthcare Facilities

- Commercial Offices

- Educational Institutions

- Industrial Manufacturing Facilities

- Retail Establishments

- Transportation & Public Infrastructure Facilities

By Distribution Channel

- Hypermarkets & Supermarkets

- Convenience Stores

- Wholesale Clubs

- Specialty Retail Stores

- Online Retail/E-Commerce

- Institutional/B2B Procurement

Regional Insights

North America

North America accounts for approximately 34% of the global paper towel market revenue, making it the largest regional market. The United States alone contributes nearly 28% of global demand due to high household consumption, strong commercial usage, and widespread adoption of premium tissue products. Canada also represents a mature market with stable demand supported by healthcare and institutional sectors. Sustainability initiatives and premium product innovation continue to drive growth throughout the region.

Europe

Europe represents approximately 30% of global market revenue and remains one of the most advanced markets for sustainable paper towel products. Germany, the United Kingdom, France, Italy, and Spain are the largest consumers within the region. Strict environmental regulations and strong consumer awareness regarding sustainability have accelerated adoption of recycled-content and certified products. Europe also leads the global market in sustainable procurement practices among institutional buyers.

Asia-Pacific

Asia-Pacific accounts for approximately 25% of global demand and is projected to be the fastest-growing regional market through 2031. China remains the largest regional consumer, while India is expected to record the highest growth rate due to rapid urbanization, expanding healthcare infrastructure, and rising disposable income. Growing foodservice, hospitality, and retail sectors across Southeast Asia are further contributing to regional market expansion.

Latin America

Latin America represents approximately 6% of global market revenue, with Brazil, Mexico, and Argentina serving as the primary demand centers. Increasing urbanization, retail modernization, and rising hygiene awareness are supporting market growth. Investments in healthcare and hospitality infrastructure are expected to generate additional demand across the region during the forecast period.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of global revenue and is emerging as an attractive growth market. Saudi Arabia, the UAE, South Africa, and Turkey are among the largest consumers. Significant investments in tourism, healthcare facilities, transportation infrastructure, and commercial real estate continue to support demand growth. Rising hygiene standards and government-led infrastructure development initiatives are expected to further strengthen regional consumption.

Key Players in the Paper Towels Market

- Kimberly-Clark Corporation

- Procter & Gamble

- Essity AB

- Georgia-Pacific LLC

- Sofidel Group

- WEPA Group

- Kruger Products

- Cascades Inc.

- Hengan International Group

- Vinda International Holdings

- Metsä Tissue

- Industrie Cartarie Tronchetti S.p.A.

- Asaleo Care

- Hayat Kimya

- Clearwater Paper Corporation