Office Stationery Supplies Market Size

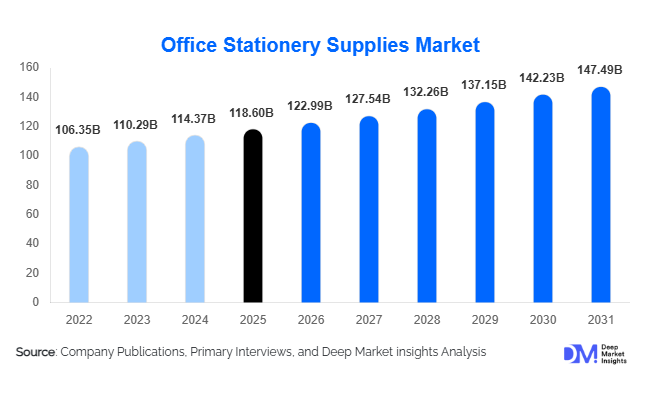

According to Deep Market Insights, the global office stationery supplies market size was valued at USD 118.6 billion in 2025 and is projected to grow from USD 122.99 billion in 2026 to reach USD 147.49 billion by 2031, expanding at a CAGR of 3.7% during the forecast period (2026–2031). The office stationery supplies market growth is supported by expanding global service-sector employment, increasing educational infrastructure investments, growth in small and medium-sized enterprises (SMEs), and the continued need for administrative documentation across corporate, government, healthcare, and educational institutions. While digital transformation has reduced dependence on certain traditional stationery categories, demand remains resilient due to regulatory requirements, workplace productivity needs, hybrid working models, and the emergence of sustainable stationery products.

Key Market Insights

- Paper-based stationery remains the largest product segment, accounting for nearly 35% of global market revenue due to sustained demand from offices, educational institutions, and government organizations.

- Sustainability is becoming a major procurement criterion, with organizations increasingly adopting recycled paper products, refillable writing instruments, and environmentally certified office supplies.

- Asia-Pacific dominates the global market, supported by large student populations, expanding office employment, and strong growth in SME formation across China, India, and Southeast Asia.

- E-commerce and digital procurement platforms are transforming purchasing behavior, enabling businesses to automate replenishment cycles and improve procurement efficiency.

- Hybrid work environments continue to create incremental demand, as employees maintain dedicated home-office workspaces requiring stationery and office supplies.

- Corporate ESG initiatives are accelerating demand for eco-friendly products, creating opportunities for manufacturers offering sustainable stationery portfolios.

Office Stationery Supplies Market Trends

Sustainable and Eco-Friendly Stationery Adoption Accelerating

Environmental sustainability has become a major purchasing consideration across both public and private organizations. Businesses are increasingly adopting recycled paper, biodegradable office products, refillable pens, and FSC-certified stationery as part of broader environmental commitments. Procurement teams are incorporating sustainability metrics into vendor selection processes, encouraging manufacturers to invest in greener product portfolios. The shift toward circular economy principles is also supporting innovation in reusable office supplies, recyclable packaging, and low-carbon production methods. Organizations pursuing ESG targets increasingly view sustainable stationery as a visible and measurable component of responsible business operations.

Digital Procurement and Smart Inventory Management Expanding

Corporate procurement is rapidly shifting toward digital purchasing platforms that provide centralized purchasing, automated replenishment, and enhanced inventory visibility. Enterprise procurement software and B2B e-commerce platforms allow organizations to streamline office supply management while reducing administrative costs. Artificial intelligence-based demand forecasting and inventory optimization tools are helping businesses minimize stockouts and excess inventory. As organizations continue digitizing procurement functions, manufacturers with strong online capabilities and direct-to-business sales channels are gaining competitive advantages.

Office Stationery Supplies Market Drivers

Growth in Global Service Sector Employment

The continued expansion of professional services, information technology, financial services, healthcare administration, and consulting industries is driving demand for office stationery products. Although workplaces have become increasingly digital, administrative functions still require a broad range of paper products, writing instruments, filing systems, and presentation materials. New office establishments and workforce expansion continue to support recurring stationery consumption across developed and emerging economies.

Rising Investments in Educational Infrastructure

Governments worldwide are increasing investments in schools, universities, vocational institutions, and literacy programs. Educational institutions remain among the largest consumers of notebooks, writing instruments, printing paper, filing products, and teaching materials. Rapid urbanization, growing student populations, and government-sponsored educational initiatives in Asia-Pacific, Africa, and Latin America are creating sustained demand for office and educational stationery products.

Office Stationery Supplies Market Restraints

Increasing Adoption of Paperless Workflows

The growing use of cloud-based document management systems, electronic signatures, digital collaboration tools, and enterprise content management platforms is reducing demand for traditional paper products and filing supplies. Large organizations are increasingly implementing paper reduction strategies to lower operational costs and achieve sustainability objectives. This trend poses a long-term challenge for certain stationery categories, particularly paper-intensive products.

Raw Material Price Volatility

Manufacturers face ongoing challenges from fluctuations in paper pulp, plastic resin, packaging materials, and transportation costs. Volatile input prices can compress margins and create difficulties in maintaining stable pricing structures. Global supply chain disruptions and energy cost fluctuations further contribute to production cost uncertainties, impacting profitability throughout the stationery value chain.

Office Stationery Supplies Market Opportunities

Expansion of Sustainable Product Portfolios

The increasing focus on environmental responsibility presents significant opportunities for manufacturers offering recycled paper products, biodegradable office supplies, refillable writing instruments, and low-carbon production solutions. Large corporations and government agencies are increasingly incorporating sustainability criteria into procurement decisions, creating premium market segments and long-term contractual opportunities for environmentally responsible suppliers.

Emerging Market Growth and Education Modernization Programs

Rapid economic development in countries such as India, Indonesia, Vietnam, Brazil, and Nigeria is generating substantial opportunities for stationery manufacturers. Expanding educational infrastructure, growing office employment, rising literacy rates, and increasing business registrations are driving demand for a wide range of stationery products. Public procurement programs and government-sponsored educational initiatives provide stable demand streams and long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 118.6 Billion |

| Market Size in 2026 | USD 122.99 Billion |

| Market Size in 2031 | USD 147.49 Billion |

| CAGR | 3.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Paper-based stationery emerged as the largest product segment, accounting for approximately 35% of global office stationery supplies market revenue in 2025. The segment maintains its leadership position despite increasing workplace digitization, primarily due to the continued requirement for printed documentation, record keeping, regulatory compliance, educational materials, and administrative paperwork across government agencies, educational institutions, healthcare organizations, and corporate offices. Products such as copier paper, notebooks, writing pads, envelopes, business forms, and registers remain indispensable in both developed and emerging economies. The segment is particularly supported by growing student enrollments globally, expansion of public administration functions, and increasing office employment in Asia-Pacific and Latin America.

Writing and marking instruments represent the second-largest product category, driven by recurring demand from schools, universities, offices, training centers, and professional workplaces. Premiumization trends are also supporting revenue growth as consumers increasingly prefer ergonomic pens, refillable writing instruments, and branded office supplies. Meanwhile, filing and organizational products continue to maintain stable demand in sectors such as legal services, healthcare, banking, insurance, and government administration where physical document retention remains mandatory for compliance purposes.

Eco-friendly stationery products are expected to record the fastest growth during the forecast period. Corporate sustainability initiatives, ESG procurement policies, and increasing environmental awareness are driving adoption of recycled paper, FSC-certified products, biodegradable office supplies, and refillable writing instruments. Large multinational corporations are increasingly integrating sustainability criteria into procurement contracts, creating substantial opportunities for manufacturers with environmentally responsible product portfolios.

Distribution Channel Insights

Offline distribution channels dominated the market with approximately 69% revenue share in 2025, supported by long-established procurement practices among corporations, educational institutions, and government agencies. Office supply retailers, wholesalers, contract suppliers, and business procurement networks remain the preferred purchasing channels for bulk buyers due to negotiated pricing agreements, inventory management services, and immediate product availability. Large enterprises and public-sector organizations continue to rely heavily on institutional procurement frameworks, supporting the dominance of offline distribution.

However, online distribution channels are witnessing the fastest growth rate globally as businesses increasingly adopt digital procurement solutions. Enterprise procurement platforms, B2B e-commerce marketplaces, and direct-to-business purchasing portals are improving purchasing efficiency while reducing procurement costs. The growth of remote work and distributed workforce models has further accelerated online stationery purchasing. Manufacturers are increasingly implementing omnichannel strategies that combine traditional retail presence with digital procurement capabilities to enhance customer engagement, strengthen brand visibility, and improve operational efficiency.

Enterprise Size Insights

Large enterprises accounted for approximately 42% of global office stationery supplies consumption in 2025, making them the largest customer segment. Their dominance is driven by extensive administrative operations, geographically dispersed office networks, centralized procurement systems, and large employee populations that require consistent replenishment of stationery products. Multinational corporations, financial institutions, technology companies, consulting firms, and government contractors generate significant recurring demand for paper products, writing instruments, filing systems, and presentation materials.

Medium-sized enterprises continue to represent a rapidly growing customer base, particularly across emerging economies where industrialization, urbanization, and entrepreneurship are driving business formation. Meanwhile, small enterprises and microbusinesses are increasingly utilizing digital procurement platforms and subscription-based purchasing models, creating new opportunities for stationery suppliers to reach previously fragmented customer segments. The growth of startup ecosystems and professional service firms across Asia-Pacific and Latin America is expected to further expand demand from SME customers during the forecast period.

End-Use Industry Insights

Corporate offices remained the largest end-use segment, accounting for approximately 31% of global market demand in 2025. The segment's leadership is supported by sustained demand from financial services, information technology, consulting, telecommunications, legal services, and professional service industries. Despite increasing digitalization, businesses continue to require office stationery for internal communication, client documentation, presentations, employee onboarding, and administrative functions. The continued expansion of the global services sector is expected to support stable long-term demand.

Educational institutions represent the fastest-growing end-use segment globally. Rising student populations, increasing literacy rates, government investments in educational infrastructure, and the establishment of new schools and universities across developing economies are driving significant demand for notebooks, writing instruments, paper products, and classroom supplies. Countries such as India, Indonesia, Vietnam, Nigeria, and Brazil continue to invest heavily in educational development programs, creating substantial growth opportunities for stationery manufacturers.

Healthcare facilities are emerging as another high-growth end-use sector due to expanding healthcare infrastructure, increasing patient volumes, and extensive documentation requirements. Additionally, co-working spaces and home-office environments continue to generate incremental demand as hybrid working models become a permanent feature of the global workplace ecosystem.

Explore more data points, trends and opportunities Download Free Sample Report

Office Stationery Supplies Market Segmentations

By Product Type

- Paper-Based Stationery

- Writing & Marking Instruments

- Filing & Organization Supplies

- Desk & Workspace Supplies

- Adhesives & Fastening Products

- Presentation & Meeting Supplies

- Mailing & Shipping Stationery

- Printing Consumables

- Eco-Friendly & Sustainable Stationery

By Distribution Channel

- Offline Retail

- Online Sales

By Enterprise Size

- Large Enterprises

- Medium Enterprises

- Small Enterprises

- Micro Businesses

By End Use

- Corporate Offices

- Government & Public Administration

- Educational Institutions

- Healthcare Facilities

- BFSI Sector

- Legal & Professional Services

- Manufacturing Facilities

- Co-working Spaces

- Home Offices

Regional Insights

North America

North America accounted for approximately 24% of global office stationery supplies market revenue in 2025, with the United States representing the largest contributor. Demand is primarily driven by the region's extensive corporate sector, highly developed service economy, large educational infrastructure, and significant government administrative spending. The United States continues to generate strong stationery consumption through financial services, healthcare administration, legal services, and professional consulting industries. Increasing adoption of premium office products, sustainable stationery solutions, and digitally integrated procurement systems is further supporting market growth. Canada contributes stable demand through its public education system and government sector, while Mexico benefits from expanding manufacturing activity, business services growth, and increasing SME formation. Key growth drivers include corporate procurement modernization, hybrid work adoption, growth in professional services employment, and increasing sustainability-focused purchasing policies.

Europe

Europe represented approximately 22% of global market demand in 2025, led by Germany, the United Kingdom, France, Italy, and Spain. The region benefits from a mature corporate environment, extensive government administration infrastructure, and strong educational systems that support stable stationery consumption. Germany remains the largest market due to its large industrial and business services sectors, while the United Kingdom generates substantial demand from financial services, legal firms, and educational institutions.

The strongest growth driver across Europe is the region's leadership in sustainability and circular economy initiatives. Corporate ESG commitments, strict environmental regulations, and public procurement policies are accelerating demand for recycled paper products, refillable writing instruments, and environmentally certified office supplies. Furthermore, rising investments in digital procurement systems and workplace modernization programs continue to support market expansion.

Asia-Pacific

Asia-Pacific dominated the global office stationery supplies market with approximately 39% market share in 2025 and is expected to remain the fastest-growing regional market through 2031. China accounts for roughly 16% of global demand due to its vast workforce, extensive educational network, and strong manufacturing sector. India contributes approximately 7% of global market revenue and is projected to record the highest growth rate among major countries owing to expanding office employment, rapid SME formation, growing educational enrollment, and government initiatives supporting domestic manufacturing and education.

Japan and South Korea continue to drive demand for premium stationery products, while Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are experiencing robust growth due to urbanization, rising literacy rates, and expanding business activity. Australia contributes through its strong corporate sector and educational institutions. Key regional growth drivers include rapid economic development, expanding middle-class populations, increasing business registrations, rising education expenditure, growth of the services sector, and substantial government investments in administrative and educational infrastructure.

Latin America

Latin America accounted for approximately 8% of global office stationery supplies demand in 2025, with Brazil and Mexico serving as the region's largest markets. Demand growth is supported by expanding educational infrastructure, increasing workforce participation, rising business registrations, and ongoing investments in public administration systems. Brazil continues to dominate regional consumption due to its large student population and extensive government procurement programs.

Mexico benefits from industrial expansion, nearshoring investments, and growth in professional services industries, while countries such as Colombia, Chile, and Argentina are witnessing gradual increases in office employment and educational spending. Government-led literacy programs and educational modernization initiatives remain important contributors to long-term market growth throughout the region. Primary growth drivers include educational investment, SME development, urbanization, public-sector procurement programs, and the continued expansion of service-based industries.

Middle East & Africa

The Middle East and Africa accounted for approximately 7% of global market revenue in 2025, with Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria emerging as key demand centers. The region is experiencing increasing demand for office stationery supplies due to expanding government administration functions, educational development initiatives, and rising private-sector investment.

In the Gulf Cooperation Council countries, economic diversification programs such as Saudi Vision 2031 and the UAE's knowledge-economy initiatives are supporting growth in professional services, education, healthcare, and administrative industries. South Africa remains a major regional market due to its developed corporate sector and educational infrastructure, while Nigeria and Egypt are benefiting from population growth, rising school enrollments, and expanding business activity. Key regional growth drivers include government modernization programs, economic diversification strategies, increasing educational investments, workforce expansion, and rising demand for administrative infrastructure across both public and private sectors.

Key Players in the Office Stationery Supplies Market

- ACCO Brands Corporation

- Newell Brands Inc.

- Kokuyo Co., Ltd.

- BIC Group

- Faber-Castell AG

- Staedtler Mars GmbH

- Schwan-STABILO Group

- Hamelin Group

- Pentel Co., Ltd.

- 3M Company

- Pilot Corporation

- Mitsubishi Pencil Company (Uni)

- Maped Group

- Navneet Education Limited

- ITC Classmate