Printing & Writing Paper Market Size

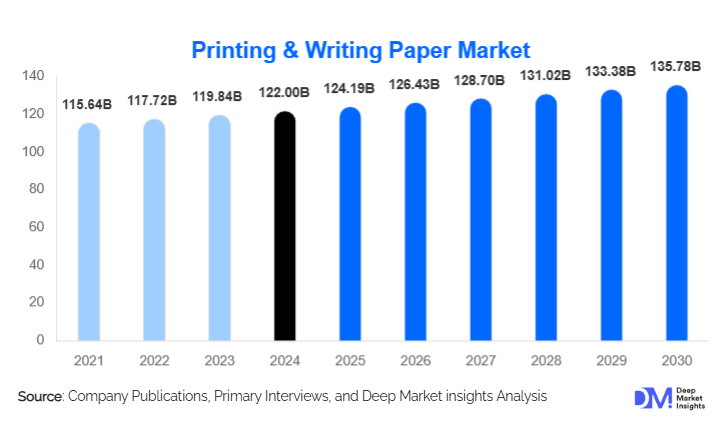

According to Deep Market Insights, the global printing and writing paper market size was valued at USD 122 billion in 2025 and is projected to grow from USD 124.19 billion in 2026 to reach USD 135.78 billion by 2031, expanding at a CAGR of 1.80% during the forecast period (2026–2031). Market growth is anchored by rising paper consumption in emerging economies, steady demand from education and office sectors, and expanding adoption of sustainable, recycled, and specialty paper grades that command higher margins. Despite global digitization trends, the market remains resilient due to sustained commercial printing needs, institutional consumption, and increasing production of eco-friendly paper products.

Key Market Insights

- Uncoated writing & copier paper continues to lead global consumption, driven by education, corporate, and government demand.

- Recycled and sustainably certified papers are the fastest-growing categories, supported by ESG commitments and regulatory pressure.

- Asia-Pacific dominates global consumption, accounting for more than half of global printing & writing paper demand.

- North America and Europe show stable but slow growth, with a concentration in premium, specialty, and eco-friendly paper types.

- Digital-printing-optimized papers are rising as businesses shift to short-run, high-quality digital print applications.

- Industry consolidation and mill modernization are reshaping cost structures and competitive positioning globally.

Hotel Toiletries Market Trends

Shift Toward Premium, Specialty & High-Value Papers

Global manufacturers are increasingly focusing on high-margin, specialty, and premium-grade papers to offset declining volumes in commodity printing paper. These include textured writing paper, cotton-based fine paper, luxury stationery, designer notebooks, art papers, coated premium media for catalogs, and brand-oriented commercial print materials. The premiumization trend is reinforced by rising global disposable income, corporate branding initiatives, and demand from boutique publishers and luxury packaging producers. Specialty paper segments remain resilient to digital disruption because they serve tactile, high-end, and experience-driven use cases where printed physical quality is essential.

Sustainable & Recycled Paper Adoption Accelerating

Environmental regulations, deforestation controls, and corporate sustainability mandates are pushing global buyers toward recycled fiber, FSC/PEFC-certified, and low-carbon paper products. Recycled writing and printing papers have seen double-digit growth in Europe, North America, and parts of Asia as governments implement green procurement standards. Mills are investing in advanced de-inking technology, high-yield recycled pulp, water-efficient processes, and renewable energy. This shift is fundamentally reshaping global pulp sourcing and positioning sustainability as a core competitive differentiator in the market.

Hotel Toiletries Market Drivers

Growing Demand from Education and Institutional Sectors

Expanding school enrollments, rising literacy rates, and increasing adoption of printed educational materials in emerging markets continue to support large-scale demand for writing and printing papers. Exercise books, notebooks, worksheets, examination papers, and school stationery account for a substantial portion of total paper consumption in Asia, Africa, and Latin America. Government-funded education programs further reinforce stable baseline demand.

Commercial Printing & Corporate Documentation Needs

Despite the digitization of communication, businesses worldwide continue to rely on printed brochures, reports, forms, marketing collateral, and operational documents. Commercial print houses require large volumes of coated, uncoated, and specialty papers, particularly in advertising, retail, and FMCG sectors. The rise of short-run digital printing further strengthens the need for high-quality, digitally optimized papers.

Rising Sustainability Awareness & Recycled Paper Consumption

Corporate ESG mandates, eco-label requirements, and consumer pressure for environmentally responsible products are driving robust demand for recycled and sustainably sourced fibers. Governments are adopting mandatory green procurement standards, accelerating market expansion for eco-friendly writing and printing papers. Mills that offer certified sustainable products experience higher customer loyalty and stronger pricing power.

Hotel Toiletries Market Restraints

Digitalization and Declining Print Media Consumption

The migration to digital communication, online documentation, and electronic publishing continues to erode demand for newspapers, magazines, and traditional printing applications. This structural decline particularly affects coated and newsprint-related segments in mature markets. The shift to e-learning and digital workflow tools further challenges traditional writing and printing paper categories.

High Raw Material and Compliance Costs

Fluctuating pulp prices, rising energy costs, and increasingly strict environmental compliance obligations elevate production costs for mills. Modernizing or retrofitting aging facilities requires significant capital expenditure, which can be prohibitive for smaller mills. Such cost pressures reduce profitability in commodity paper grades and accelerate mill consolidation worldwide.

Hotel Toiletries Market Opportunities

High-Margin Specialty & Premium Paper Expansion

Demand for textured writing paper, luxury stationery, fine art paper, and bespoke corporate communication materials is increasing globally. These segments are insulated from digital substitution and allow manufacturers to capture premium margins. As gifting, branding, and boutique publishing grow, the specialty paper segment will continue expanding, offering strong opportunities for new entrants and existing producers.

Growth Potential in Emerging Markets

Asia-Pacific, Africa, and Latin America present major long-term opportunities due to rising literacy, population growth, rapid industrialization, and expansion of SME businesses. Local production units that reduce import dependence can gain a significant competitive advantage. Educational institutions, government departments, and corporate enterprises in these regions continue to increase their paper consumption, driving sustained growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 122 Billion |

| Market Size in 2026 | USD 124.19 Billion |

| Market Size in 2031 | USD 135.78 Billion |

| CAGR | 1.80% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Uncoated writing and copier paper dominate the market, accounting for roughly 40–45% of global revenue in 2025. These papers serve daily writing, printing, and documentation needs in schools, offices, and households. Coated papers represent around 15–20% of the market, driven by demand from commercial printing, catalogs, and promotional materials. Specialty and premium-grade papers, including textured and cotton-based varieties, represent a smaller share but are the fastest-growing due to premiumization, digital-print optimization, and sustainability preferences.

Application Insights

Education remains the largest application segment, supported by growing school populations and the continued reliance on physical learning materials in developing regions. Corporate and office applications maintain strong demand due to the persistent need for printed documents, copier paper, and administrative stationery. Commercial printing applications, catalogs, brochures, leaflets, and advertising materials continue to be major consumers of coated and specialty paper. New applications in luxury packaging inserts, boutique publishing, and premium gifting are rapidly emerging.

Distribution Channel Insights

Wholesale channels dominate due to high-volume purchases by corporate buyers, print houses, and educational institutions. Retail distribution, through office supply stores and stationery outlets, remains strong in both developed and emerging markets. Online B2B platforms and e-commerce distribution are rapidly growing for small businesses, freelancers, home offices, and specialty paper buyers. Manufacturers increasingly invest in direct-to-consumer (D2C) channels for premium stationery and customized paper products.

End-Use Insights

Educational institutions, corporate offices, and commercial printers represent the primary end-users. Education-driven consumption in Asia and Africa ensures a steady baseline demand. Corporate sectors in North America and Europe continue to adopt specialty, sustainable, and premium paper for branding and documentation. Emerging new users include luxury packaging manufacturers, boutique publishers, artisanal stationery brands, and digital printing specialists. Export-driven demand for premium and sustainable papers is rising as countries expand high-end packaging and branding requirements.

Explore more data points, trends and opportunities Download Free Sample Report

Printing & Writing Paper Market Segmentations

By Product Type

- Uncoated Writing & Copier Paper

- Coated Paper (Coated Woodfree, Gloss/Matte)

- Specialty & Premium Paper (Textured, Cotton-Based, Art Paper)

- Newsprint & Publication Paper

By Application

- Education Materials (Notebooks, Exercise Books)

- Corporate & Office Documentation

- Commercial Printing (Catalogs, Brochures, Advertising)

- Publishing (Books, Magazines, Journals)

- Luxury & Specialty Printing (Stationery, Packaging Inserts)

By Distribution Channel

- Wholesale / Bulk Distributors

- Retail Stores (Stationery, Office Supply)

- Online B2B & E-commerce Platforms

- Direct Sales to Corporations and Institutions

By Raw Material Type

- Virgin Fiber Paper

- Recycled Fiber Paper

- Alternative/Non-Wood Fiber Paper

Regional Insights

North America

North America accounts for 20–25% of the global market value in 2025. The region maintains a strong demand for premium and eco-friendly paper categories. Commercial printing, corporate documentation, and specialty applications remain major segments. Sustainability regulations and recycling mandates are reshaping product portfolios, with U.S. and Canadian buyers prioritizing certified and low-carbon papers.

Europe

Europe contributes 15–20% of global demand and remains at the forefront of sustainable paper adoption. Consumers and institutions prefer FSC/PEFC-certified products, recycled paper, and eco-friendly printing media. Western Europe shows strong demand for specialty, premium, and artisanal-quality papers, especially in Germany, the U.K., France, and the Nordics.

Asia-Pacific

Asia-Pacific dominates the global market with a 50–55% share in 2025. China and India lead consumption due to large populations, expanding education systems, and fast-growing SME sectors. Southeast Asia, Indonesia, Vietnam, and Malaysia continue to expand commercial printing and office stationery use. APAC also represents the fastest-growing region overall.

Latin America

Latin America holds a smaller but rising share, supported by expanding educational enrollment and increasing corporate sectors in Brazil, Argentina, Mexico, and Chile. Demand is shifting toward mid-range and eco-friendly paper grades as regulatory frameworks strengthen.

Middle East & Africa

MEA markets, South Africa, Nigeria, Kenya, UAE, and Saudi Arabia, are rapidly increasing their writing and printing paper consumption. Education, government documentation, and corporate paperwork drive volume. UAE and Saudi Arabia import large quantities of premium and specialty paper, while Africa remains one of the fastest-growing markets for writing and office paper.

Key Players in the Printing & Writing Paper Market

- International Paper Company

- UPM-Kymmene Corporation

- Mondi Group

- Stora Enso

- Sappi Limited

- Nippon Paper Industries

- Oji Holdings Corporation

- WestRock

- Domtar Corporation

- Georgia-Pacific LLC

- Smurfit Kappa Group

- DS Smith

- Pratt Industries

- Sonoco Products Company

- Great Little Box Company Ltd.