Global Nodoame Market Size

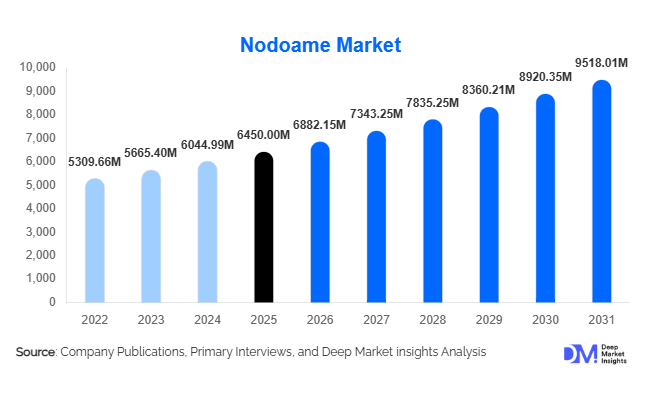

According to Deep Market Insights, the global Nodoame market size was valued at USD 6,450 million in 2026 and is projected to grow from USD 6,882.15 million in 2026 to reach USD 9,518.01 million by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The Nodoame market growth is primarily driven by rising prevalence of respiratory infections, increasing air pollution levels, growing consumer preference for OTC self-medication, and rapid expansion of herbal and immunity-boosting lozenge formulations across global markets.

Key Market Insights

- Herbal and natural formulations are gaining strong traction, with consumers shifting from medicated products to plant-based and clean-label lozenges.

- Asia Pacific dominates global demand, supported by high population density, pollution exposure, and strong pharmaceutical manufacturing ecosystems.

- E-commerce and e-pharmacy channels are rapidly expanding, improving accessibility and driving impulse OTC purchases.

- Immunity-focused lozenges are emerging as a high-growth category, driven by post-pandemic health awareness.

- Retail pharmacies remain the dominant distribution channel, accounting for the majority of global sales.

- Product innovation in flavors and sugar-free variants is significantly improving repeat consumption rates.

Nodoame market latest trends

Shift Toward Herbal and Functional Lozenges

The Nodoame market is experiencing a clear transition from synthetic medicated lozenges toward herbal, organic, and functional wellness formulations. Ingredients such as honey, ginger, eucalyptus, turmeric, and vitamin C are increasingly integrated into product formulations. This shift is being driven by consumer demand for safer, chemical-free alternatives and long-term immunity support rather than just symptomatic relief. Manufacturers are also focusing on sugar-free and diabetic-friendly variants to expand accessibility across health-conscious and elderly populations.

Digital Pharmacy and Direct-to-Consumer Expansion

The rise of online pharmacies and D2C healthcare platforms is transforming product distribution dynamics. Consumers increasingly prefer ordering OTC healthcare products online due to convenience, discounts, and wider product availability. Subscription-based wellness models and rapid delivery services are accelerating repeat purchases. This trend is particularly strong in India, China, and the United States, where digital healthcare ecosystems are rapidly maturing.

Nodoame market drivers

Rising Respiratory Health Burden

Increasing air pollution, seasonal flu outbreaks, and respiratory infections are significantly driving demand for Nodoame products globally. Urban populations exposed to poor air quality are increasingly relying on throat lozenges for quick relief. This is especially evident in densely populated regions of Asia Pacific, where pollution levels are consistently high, contributing to recurring throat irritation and cough-related conditions.

Growing OTC Self-Medication Adoption

Consumers are increasingly shifting toward self-medication for minor health issues, reducing dependency on clinical consultations for throat-related ailments. Nodoame products are widely available over the counter, making them a preferred choice for quick symptom relief. This behavioral shift is strongly supported by expanding pharmacy retail networks and rising healthcare awareness globally.

Product Innovation and Functional Enhancement

Continuous innovation in flavor profiles, delivery mechanisms, and functional ingredients is strengthening market expansion. Companies are introducing fast-dissolving, sugar-free, and immunity-enhancing lozenges that appeal to both younger and older demographics. These innovations are improving consumer engagement and increasing product lifecycle value.

Nodoame market restraints

High Price Sensitivity in Emerging Economies

Despite growing demand, price sensitivity remains a major barrier in developing regions. Low-cost local substitutes and unbranded products limit the penetration of premium global brands. This restricts margin expansion and forces companies to adopt localized pricing strategies.

Regulatory and Compliance Constraints

Strict pharmaceutical regulations regarding ingredient approval, labeling requirements, and health claims create barriers for new product launches. Regulatory differences across regions such as Europe, North America, and Asia increase compliance costs and slow down innovation cycles.

nodoame industry key opportunities

Expansion of Herbal and Immunity-Based Product Lines

The rising global focus on preventive healthcare presents strong opportunities for herbal and immunity-boosting Nodoame products. Companies investing in vitamin-enriched and plant-based formulations are likely to capture premium market segments. This trend is further supported by increasing consumer willingness to pay higher prices for natural health products.

Growth of E-Commerce and Subscription Wellness Models

Digital healthcare platforms and subscription-based wellness services are emerging as key growth channels. These models allow companies to ensure recurring revenue streams while improving consumer retention. Rapid delivery services and personalized health product recommendations are further enhancing online sales penetration.

Emerging Markets Expansion

High-growth opportunities exist in emerging economies such as India, Indonesia, Brazil, and parts of Africa. Rising disposable income, expanding pharmacy infrastructure, and increasing healthcare awareness are driving demand. These regions also offer cost-effective manufacturing bases for global exports.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6450.00 Million |

| Market Size in 2026 | USD 6882.15 Million |

| Market Size in 2031 | USD 9518.01 Million |

| CAGR | 6.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Medicated lozenges continue to dominate the global market, holding approximately 34% share in 2025, primarily driven by strong physician endorsement, established pharmaceutical trust, and their proven efficacy in providing rapid symptomatic relief for sore throat and cough. Their leadership is further reinforced by widespread OTC availability and consumer reliance on clinically validated formulations, making them the most preferred choice across both developed and emerging markets.Herbal lozenges represent the fastest-growing product category, supported by a global shift toward natural, plant-based, and clean-label healthcare solutions. Growth is strongly driven by increasing consumer skepticism toward synthetic additives and a rising preference for traditional medicine systems such as Ayurveda and herbal therapeutics, particularly in Asia Pacific and Europe. Sugar-free lozenges are also expanding rapidly, fueled by rising diabetes prevalence, obesity concerns, and broader adoption of low-calorie lifestyles, with manufacturers increasingly reformulating products to align with metabolic health trends.Vitamin and immunity-boosting lozenges are witnessing strong momentum as preventive healthcare becomes a core consumer behavior rather than a reactive approach. This growth is primarily driven by post-pandemic health awareness, increasing air pollution exposure, and the demand for convenient daily immune support formats. Cough suppressant lozenges maintain stable demand due to seasonal influenza cycles and recurring respiratory infections, while throat-soothing variants are increasingly positioned as everyday wellness products used for hydration, voice care, and environmental irritation relief.

Application & End-Use Insights

Respiratory relief remains the largest application segment, driven by the high global incidence of sore throat, cough, and irritation caused by viral infections, environmental pollution, and seasonal allergies. This dominance is reinforced by strong OTC accessibility and physician recommendation for symptomatic management of upper respiratory conditions.Preventive wellness is emerging as the fastest-growing application, supported by a behavioral shift toward proactive health management. Consumers increasingly use lozenges not only for treatment but also for immunity reinforcement, hydration support, and daily throat protection, reflecting broader wellness-oriented consumption patterns.Occupational usage represents a stable and recurring demand base, particularly among teachers, singers, call center professionals, and public speakers, where continuous vocal strain creates sustained product need. Pediatric and geriatric adoption is also increasing, driven by improvements in flavor masking technologies, safer dosage formats, and rising healthcare accessibility, making lozenges more acceptable across sensitive age groups.

Distribution Channel Insights

Retail pharmacies remain the dominant distribution channel, accounting for approximately 46% market share, supported by strong pharmacist influence, immediate product availability, and high consumer trust in in-store recommendations. This channel leadership is further strengthened by the habitual nature of OTC healthcare purchasing behavior in both urban and semi-urban regions.Online pharmacies are the fastest-growing channel, driven by rapid digital adoption, expanding e-commerce infrastructure, and increasing consumer preference for convenience, price comparison, and home delivery. The growth is also supported by subscription-based purchasing models and targeted digital health marketing strategies.Supermarkets and convenience stores contribute significantly to impulse-driven purchases, particularly for throat-soothing and flavored variants positioned as lifestyle or wellness products. Hospital pharmacies maintain relevance for clinically recommended formulations, especially in post-treatment recovery scenarios. Direct-to-consumer brands are also gaining traction, leveraging digital-first branding, influencer marketing, and personalized wellness positioning to build recurring customer engagement.

Explore more data points, trends and opportunities Download Free Sample Report

Nodoame Market Segmentations

By Product Type

- Medicated Lozenges

- Herbal / Natural Lozenges

- Sugar-Free Lozenges

- Vitamin & Immunity Lozenges

- Cough Suppressant Lozenges

- Throat Soothing Candy Lozenges

By Formulation Type

- Hard Lozenges

- Soft Chewable Lozenges

- Fast-Dissolving Tablets

- Dual-Layer Lozenges

By Distribution Channel

- Retail Pharmacies & Drug Stores

- Hospital Pharmacies

- Supermarkets & Hypermarkets

- Online E-commerce Platforms

- Convenience Stores

By End User

- Adults

- Pediatric Population

- Geriatric Population

- Occupational Users

Regional Insights

Asia Pacific

Asia Pacific leads the global market with approximately 38% share in 2025, driven by a combination of high population density, elevated air pollution levels, and strong pharmaceutical manufacturing ecosystems across China, India, Japan, and Southeast Asia. The region’s dominance is further supported by increasing urbanization and rising respiratory health concerns linked to environmental factors.India is emerging as a key consumption and export hub due to strong OTC accessibility, cost-effective production capabilities, and growing health awareness among urban populations. China drives both large-scale production and domestic consumption, supported by integrated supply chains and expanding retail pharmacy penetration. Japan contributes through high-quality, innovation-driven formulations, particularly in medicated and functional wellness segments.

North America

North America accounts for approximately 27% of the global market, with the United States as the primary growth engine due to a highly developed OTC healthcare ecosystem and strong consumer trust in branded pharmaceutical products. Growth in this region is driven by high incidence of seasonal respiratory illnesses, widespread self-medication practices, and strong retail pharmacy networks.Demand is particularly driven by sugar-free, immunity-enhancing, and premium formulations, reflecting a broader shift toward preventive health and functional wellness. Product innovation and branding strategies emphasizing clinically backed benefits also play a key role in sustaining regional growth.

Europe

Europe holds nearly 22% market share, supported by strong demand in Germany, the United Kingdom, and France. The region’s growth is driven by strict regulatory frameworks that favor clean-label, herbal, and organic formulations, alongside rising consumer awareness of ingredient transparency.Increasing preference for plant-based remedies and natural therapeutic solutions is a key growth driver, particularly in Western Europe, where consumers actively seek alternatives to synthetic pharmaceuticals. Well-established healthcare systems and pharmacist-led recommendations further reinforce steady market expansion.

Latin America

Latin America, led by Brazil and Mexico, is experiencing steady growth driven by improving pharmacy infrastructure, expanding urban healthcare access, and rising awareness of OTC self-care products. The increasing prevalence of respiratory conditions linked to urban pollution and climate variability further supports demand.Market growth is also driven by affordability-focused product positioning and the gradual expansion of international and regional brands into pharmacy retail networks.

Middle East & Africa

The Middle East & Africa region is in an emerging growth phase, supported by rapid urbanization, increasing respiratory health challenges, and rising healthcare investments. Gulf countries such as the UAE and Saudi Arabia are driving demand for premium OTC healthcare products, supported by high purchasing power and modern retail pharmacy systems.In Africa, growth is primarily driven by expanding pharmacy networks, improving healthcare accessibility, and increasing consumer awareness of self-medication practices. The region’s long-term potential is strengthened by ongoing healthcare infrastructure development and rising population growth.

Key Players in the Nodoame Market

- Yami

- Reckitt

- Procter & Gamble

- Kenvue

- Mondelez International

- Lotte Corporation

- Ricola AG

- Nestlé Health Science

- Perfetti Van Melle

- Himalaya Wellness

- Cipla

- Dr. Reddy’s Laboratories

- Johnson & Johnson Consumer Health (legacy OTC portfolio)

- Glenmark Pharmaceuticals

- Pfizer Consumer Healthcare (legacy OTC portfolio)