Greenhouse Tomato Market Size

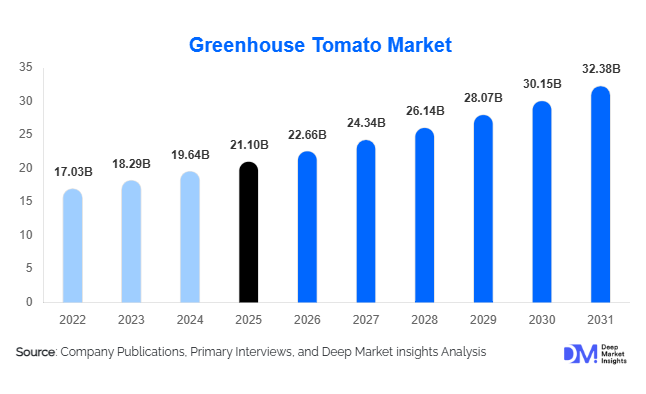

According to Deep Market Insights, the global greenhouse tomato market size was valued at USD 21.1 billion in 2025 and is projected to grow from USD 22.66 billion in 2026 to reach USD 32.38 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The greenhouse tomato market growth is primarily driven by rising demand for year-round fresh produce, increasing adoption of controlled-environment agriculture, and growing consumer preference for premium-quality, residue-controlled vegetables. Technological advancements in hydroponics, precision climate control, LED lighting, and AI-enabled greenhouse systems are further accelerating commercial greenhouse tomato production globally.

Key Market Insights

- Hydroponic greenhouse cultivation is rapidly replacing traditional soil-based farming, improving yields, reducing water usage, and enhancing crop consistency.

- Premium tomato varieties such as cherry tomatoes and vine-ripened tomatoes are witnessing strong global demand, particularly across North America and Europe.

- Europe dominates the greenhouse tomato market, supported by advanced greenhouse infrastructure and export-oriented horticulture industries.

- Asia-Pacific remains the fastest-growing region, driven by increasing investments in food security and protected cultivation technologies.

- Retail chains are increasingly prioritizing greenhouse-grown tomatoes because of stable year-round supply, superior shelf life, and improved visual quality.

- Automation and smart greenhouse technologies, including AI crop monitoring, robotic harvesting, and IoT-based irrigation systems, are transforming commercial production economics.

greenhouse tomato market latest trends

Expansion of High-Tech Hydroponic Greenhouses

Commercial greenhouse tomato cultivation is increasingly shifting toward hydroponic and precision-controlled production systems. Hydroponics enables growers to optimize nutrient delivery, improve water-use efficiency, and achieve significantly higher yields compared to conventional open-field farming. Countries such as the Netherlands, Canada, Japan, and the United States are expanding high-tech greenhouse facilities integrated with climate-control systems, AI-enabled monitoring platforms, and automated fertigation technologies. The trend is particularly strong in water-scarce regions where governments are promoting controlled-environment agriculture as part of long-term food security strategies. Modern greenhouse facilities are also integrating renewable energy systems and carbon-reduction initiatives to improve sustainability and lower long-term operating costs.

Rising Demand for Premium and Specialty Tomatoes

Consumer preference is increasingly shifting toward premium greenhouse tomato varieties including cherry tomatoes, cocktail tomatoes, vine-ripened tomatoes, and organic specialty tomatoes. Retailers are expanding shelf space for branded greenhouse produce with traceability certifications, sustainable packaging, and pesticide-controlled cultivation claims. Premium tomatoes are benefiting from rising health awareness, urban dietary changes, and demand for fresh salad ingredients. Foodservice chains and meal-kit providers are also increasing procurement of greenhouse-grown tomatoes because of consistent quality and year-round availability. Specialty greenhouse tomatoes with higher sweetness levels, improved texture, and differentiated colors are increasingly being marketed as premium fresh produce products.

greenhouse tomato market drivers

Increasing Demand for Year-Round Fresh Produce

One of the major drivers of the greenhouse tomato market is the growing consumer expectation for uninterrupted access to fresh vegetables throughout the year. Conventional tomato farming remains highly dependent on seasonal conditions and vulnerable to climate-related disruptions such as droughts, floods, and pest outbreaks. Greenhouse tomato cultivation provides stable and predictable production irrespective of external weather conditions. Supermarkets, hypermarkets, and foodservice operators increasingly rely on greenhouse-grown tomatoes to ensure supply consistency and maintain standardized product quality. Urbanization and changing dietary patterns are further supporting continuous growth in fresh tomato consumption globally.

Rapid Adoption of Controlled-Environment Agriculture

The increasing adoption of controlled-environment agriculture technologies is significantly accelerating greenhouse tomato market expansion. Commercial growers are investing heavily in AI-enabled crop management systems, automated irrigation platforms, robotic harvesting technologies, and IoT-based climate monitoring. High-tech greenhouses can deliver substantially higher yields per square meter while minimizing water usage and reducing pesticide dependency. Governments across Asia-Pacific, Europe, and the Middle East are supporting greenhouse infrastructure investments through subsidies, grants, and agricultural modernization programs. Precision agriculture integration is enabling growers to improve operational efficiency while reducing labor intensity and crop losses.

greenhouse tomato market restraints

High Initial Infrastructure and Operating Costs

Greenhouse tomato production remains highly capital intensive due to the significant investment required for greenhouse structures, automation systems, irrigation infrastructure, LED lighting, and climate-control technologies. Smaller growers in developing regions often face financial barriers when transitioning from conventional farming to commercial greenhouse production. Long payback periods and financing limitations continue to restrict broader market penetration, particularly among small and medium-scale agricultural operators.

Energy Cost Volatility and Labor Challenges

Modern greenhouse facilities require substantial energy consumption for heating, cooling, lighting, and environmental control operations. Fluctuating electricity and natural gas prices significantly impact production economics, particularly in colder regions where year-round climate control is essential. In addition, labor shortages and rising wages across developed agricultural economies are increasing operating costs for greenhouse operators. Many companies are being forced to accelerate automation investments to offset labor dependency while maintaining production efficiency and profitability.

greenhouse tomato industry key opportunities

Expansion of Greenhouse Farming in Water-Stressed Regions

The growing focus on food security and water conservation presents substantial opportunities for greenhouse tomato producers globally. Countries across the Middle East, North Africa, and Asia-Pacific are investing heavily in hydroponic and climate-controlled greenhouse systems to reduce dependence on imported vegetables. Saudi Arabia, the UAE, and Qatar are actively supporting controlled-environment agriculture projects through public-private partnerships and agricultural sustainability initiatives. These investments are creating strong demand for greenhouse technologies, precision irrigation systems, and large-scale commercial tomato cultivation infrastructure.

Growth of Organic and Premium Tomato Segments

Organic greenhouse tomatoes and premium specialty varieties represent one of the fastest-growing opportunities within the global market. Consumers are increasingly willing to pay premium prices for pesticide-controlled, sustainably grown, and traceable fresh produce. Retailers are introducing branded greenhouse tomato offerings with organic certifications, environmentally friendly packaging, and locally sourced positioning. Premium cherry tomatoes, cocktail tomatoes, and snack-sized tomato products are gaining strong traction among health-conscious urban consumers. This trend allows greenhouse operators to improve profit margins and differentiate products in highly competitive retail markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21.10 Billion |

| Market Size in 2026 | USD 22.66 Billion |

| Market Size in 2031 | USD 32.38 Billion |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Tomato Type Insights

Cherry tomatoes represent the leading tomato type segment globally, accounting for nearly 31% of greenhouse tomato market revenue in 2025. The segment benefits from increasing demand for healthy snacking products, salads, and premium packaged produce. Tomatoes-on-the-vine and vine-ripened beefsteak tomatoes continue to gain popularity among retail consumers because of their superior appearance, freshness, and flavor consistency. Roma and plum tomatoes maintain strong demand across food processing applications, including sauces, purees, and ready-to-cook meals. Specialty greenhouse tomatoes, including colored and high-brix varieties, are emerging as high-margin niche products targeting premium retail and gourmet foodservice channels. Organic greenhouse tomatoes are also witnessing accelerated adoption due to rising consumer preference for sustainable and residue-controlled produce.

Cultivation Technology Insights

Hydroponic greenhouse cultivation dominates the market with approximately 46% share of global revenue in 2025. Hydroponic systems enable precise nutrient management, lower water consumption, and improved productivity compared to soil-based cultivation methods. Substrate-based cultivation using coco peat and rockwool is also gaining traction among commercial greenhouse operators due to improved root-zone control and disease management. Aeroponic and aquaponic greenhouse systems remain emerging technologies but are attracting increasing investment because of their potential to optimize resource utilization and support sustainable urban agriculture initiatives. High-tech integrated cultivation systems are becoming increasingly important for large-scale greenhouse operators seeking operational efficiency and export-grade crop consistency.

Greenhouse Structure Insights

Glass greenhouses account for the largest share of commercial greenhouse tomato production due to superior light transmission, durability, and compatibility with automation technologies. Venlo greenhouse systems remain widely adopted across Europe because of their efficiency in climate management and high-yield tomato cultivation. Polycarbonate and polyethylene greenhouses continue to witness strong demand in emerging economies due to lower installation costs and scalability advantages. Tunnel greenhouse structures are gaining popularity among small and medium-sized growers seeking affordable protected cultivation solutions. Vertical integrated greenhouse systems are also emerging in urban farming applications, particularly in North America and Asia-Pacific, where land availability constraints are driving innovation in controlled-environment agriculture.

Distribution Channel Insights

Supermarkets and hypermarkets dominate greenhouse tomato distribution globally, accounting for nearly 38% of total market sales in 2025. Organized retail chains increasingly prioritize greenhouse-grown tomatoes because of their stable year-round availability, standardized quality, and lower spoilage rates. Foodservice distributors remain important buyers, particularly across North America and Europe, where premium greenhouse tomatoes are widely used in restaurants, hotels, and institutional catering. Online grocery platforms are rapidly emerging as a significant sales channel for packaged greenhouse produce, supported by increasing consumer adoption of digital food retailing. Wholesale produce markets and export trading companies continue to play a critical role in international greenhouse tomato supply chains.

End-Use Insights

Fresh consumption applications represent the largest end-use segment, contributing nearly 63% of greenhouse tomato market demand globally. Rising consumer preference for healthy eating habits, fresh salads, and nutrient-rich meal ingredients is supporting long-term demand growth. Foodservice and hospitality applications are expanding steadily due to increasing use of premium tomatoes in quick-service restaurants, cafes, gourmet dining establishments, and ready-to-eat food preparations. Food processing industries also remain important consumers of greenhouse-grown tomatoes, particularly for sauces, canned products, frozen meals, and convenience foods. Institutional catering and retail packaged produce applications are increasingly incorporating greenhouse tomatoes because of quality consistency and longer shelf life advantages.

Explore more data points, trends and opportunities Download Free Sample Report

Greenhouse Tomato Market Segmentations

NatureSweet Ltd.

Mastronardi Produce Ltd.

Village Farms International Inc.

Mucci Farms

Pure Flavor Farms

AppHarvest Inc.

Red Sun Farms

Windset Farms

Agro Care Group

Houweling’s Group

Regional Insights

North America

North America accounted for approximately 27% of global greenhouse tomato market revenue in 2025. The United States remains a major consumer market driven by rising demand for locally grown fresh vegetables, premium produce, and organic food products. Canada has developed one of the world’s most advanced greenhouse tomato industries, particularly in Ontario and British Columbia, supported by high-tech greenhouse infrastructure and export capabilities. Mexico continues to dominate greenhouse tomato exports to the United States because of favorable climate conditions, lower labor costs, and strong trade connectivity. Retail demand for premium cherry tomatoes and vine-ripened products remains particularly strong across the region.

Europe

Europe remains the dominant regional market, accounting for nearly 34% of global greenhouse tomato revenue in 2025. The Netherlands continues to lead technologically advanced greenhouse cultivation with extensive use of hydroponics, AI-driven climate management, and export-focused horticulture systems. Spain remains a major producer supplying tomatoes across European retail markets during winter seasons. Germany, France, Italy, and the United Kingdom maintain strong import demand for premium greenhouse tomatoes, particularly organic and specialty varieties. European sustainability regulations and energy-efficient greenhouse initiatives are accelerating adoption of climate-smart cultivation technologies across the region.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing greenhouse tomato market through 2031, supported by increasing food security investments and urbanization. China is rapidly expanding protected agriculture infrastructure under national agricultural modernization programs. Japan remains a high-value market emphasizing precision-controlled greenhouse production and premium tomato varieties. India is witnessing rising greenhouse adoption under government horticulture development schemes, while South Korea and Australia continue investing in sustainable commercial greenhouse farming. Increasing demand for high-quality vegetables among urban middle-class populations is supporting strong regional market expansion.

Latin America

Latin America is strengthening its position within global greenhouse tomato production and exports. Mexico remains the leading producer and exporter within the region, supplying substantial greenhouse tomato volumes to North American markets. Brazil and Chile are increasingly investing in protected cultivation systems to improve domestic vegetable supply and reduce weather-related production risks. Favorable climate conditions and relatively lower labor costs continue to support commercial greenhouse expansion across several Latin American countries.

Middle East & Africa

The Middle East & Africa region is witnessing increasing investment in greenhouse tomato production due to water scarcity concerns and food security priorities. Saudi Arabia and the UAE are rapidly expanding hydroponic and climate-controlled greenhouse projects to reduce dependence on imported vegetables. Israel continues to lead greenhouse technology innovation, particularly in drip irrigation and precision agriculture systems. South Africa is also emerging as a growing commercial greenhouse market serving modern retail and hospitality industries. Government-backed sustainability programs across the region are expected to accelerate future greenhouse cultivation investments.

Key Players in the Greenhouse Tomato Market

- NatureSweet Ltd.

- Mastronardi Produce Ltd.

- Village Farms International Inc.

- Mucci Farms

- Pure Flavor Farms

- AppHarvest Inc.

- Red Sun Farms

- Windset Farms

- Agro Care Group

- Houweling’s Group

- Del Fresco Pure

- SUNSET Produce

- Gotham Greens

- Jingpeng International

- Richel Group