Chewing Gum Market Size

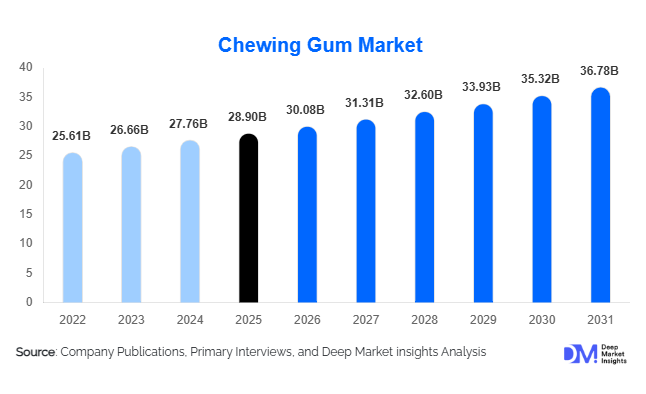

According to Deep Market Insights, the global chewing gum market size was valued at USD 28.9 billion in 2025 and is projected to grow from USD 30.08 billion in 2026 to reach USD 36.78 billion by 2031, expanding at a CAGR of 4.1% during the forecast period (2026–2031). The chewing gum market growth is being driven by increasing consumer preference for sugar-free confectionery products, rising awareness of oral health benefits, growing adoption of functional gum formulations, and expanding demand from emerging economies. Manufacturers are increasingly focusing on premiumization, clean-label ingredients, and wellness-oriented product innovations to differentiate their offerings. Functional chewing gums containing vitamins, caffeine, xylitol, nicotine replacement ingredients, and herbal extracts are transforming the category from a traditional confectionery segment into a broader wellness and lifestyle product category.

Key Market Insights

- Sugar-free chewing gum accounts for the largest share of global revenue, supported by increasing consumer awareness regarding dental health, obesity prevention, and diabetes management.

- Functional chewing gum is the fastest-growing product category, benefiting from growing demand for convenient delivery systems for vitamins, energy supplements, oral care ingredients, and smoking cessation aids.

- North America dominates the global chewing gum market, accounting for approximately 34% of global revenue due to high consumption rates and strong penetration of premium brands.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, rising disposable incomes, and expanding modern retail infrastructure across China, India, Indonesia, and Vietnam.

- Mint-flavored gum remains the leading flavor category, representing nearly 42% of global demand due to its strong association with breath freshening and oral hygiene.

- Sustainability initiatives and natural gum base innovations are reshaping product development as consumers increasingly seek environmentally responsible alternatives to synthetic gum formulations.

Chewing Gum Market Trends

Rapid Expansion of Functional and Wellness-Oriented Gum Products

The chewing gum industry is witnessing a significant shift toward functional formulations that offer benefits beyond flavor and refreshment. Consumers are increasingly seeking products that support oral health, energy enhancement, stress reduction, cognitive performance, digestive wellness, and smoking cessation. Manufacturers are responding by incorporating active ingredients such as xylitol, caffeine, vitamins, herbal extracts, probiotics, and nicotine replacement compounds into gum products. Functional gum products typically command premium pricing and generate higher profit margins compared to traditional confectionery gums. As consumer lifestyles become more health-oriented and convenience-focused, functional chewing gum is emerging as one of the industry's most important growth drivers.

Growing Adoption of Natural and Sustainable Ingredients

Environmental concerns surrounding synthetic gum bases derived from petrochemical materials are driving investment in biodegradable and plant-based alternatives. Consumers increasingly prefer products formulated with natural sweeteners such as stevia and xylitol while avoiding artificial additives. Several manufacturers are developing biodegradable gum bases using chicle and other plant-derived ingredients to address sustainability concerns. Packaging innovation is also accelerating, with companies introducing recyclable containers, paper-based packaging formats, and reduced-plastic solutions. These developments are helping brands strengthen premium positioning while aligning with evolving regulatory and consumer sustainability expectations.

Chewing Gum Market Drivers

Increasing Consumer Focus on Oral Health

Growing awareness regarding oral hygiene and preventive dental care is significantly supporting chewing gum demand worldwide. Sugar-free chewing gums containing xylitol are increasingly recommended by dental professionals because they stimulate saliva production, reduce plaque formation, and support cavity prevention. Consumers are increasingly replacing traditional confectionery products with oral-health-oriented gum formulations, particularly in developed markets such as the United States, Japan, Germany, and the United Kingdom. This trend is expected to continue supporting long-term category expansion.

Rising Demand for Sugar-Free Confectionery Products

Increasing prevalence of obesity, diabetes, and lifestyle-related health conditions is accelerating demand for low-calorie and sugar-free confectionery products. Sugar-free chewing gum offers consumers a guilt-free alternative to traditional sweets while providing flavor and refreshment. Regulatory initiatives aimed at reducing sugar consumption across multiple countries are further supporting the transition toward sugar-free gum products. Manufacturers continue to expand their portfolios with innovative sweetener systems and improved flavor retention technologies.

Chewing Gum Market Restraints

Maturity of Developed Market Consumption

The chewing gum industry faces challenges in several mature markets where per-capita consumption has stabilized or declined. Changing consumer snacking preferences, increased competition from alternative confectionery products, and demographic shifts have constrained volume growth in certain developed economies. Manufacturers must continuously invest in innovation and premiumization strategies to maintain revenue growth despite relatively flat consumption patterns.

Volatility in Raw Material and Ingredient Costs

Price fluctuations affecting gum base materials, sweeteners, flavoring agents, packaging materials, and transportation costs continue to impact profitability. Manufacturers frequently face margin pressure due to rising input costs and competitive pricing environments. Smaller companies are particularly vulnerable to supply chain disruptions and commodity price volatility, which may limit investment in new product development and market expansion initiatives.

Chewing Gum Market Opportunities

Expansion of Functional Wellness Gum Categories

Functional chewing gum remains significantly underpenetrated relative to its growth potential. New product opportunities exist across energy supplementation, cognitive enhancement, sleep support, stress management, digestive wellness, and sports nutrition applications. As consumers increasingly seek convenient alternatives to pills and beverages, chewing gum provides an attractive delivery format. This opportunity is expected to generate substantial premium revenue growth over the next decade.

Emerging Market Growth Potential

Countries across Asia-Pacific, Latin America, the Middle East, and Africa continue to offer substantial growth opportunities due to low per-capita gum consumption levels. Expanding middle-class populations, urbanization, rising disposable incomes, and modern retail penetration are creating favorable market conditions. Localized flavor offerings, affordable packaging formats, and increased distribution coverage are expected to support accelerated market development in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.9 Billion |

| Market Size in 2026 | USD 30.08 Billion |

| Market Size in 2031 | USD 36.78 Billion |

| CAGR | 4.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sugar-free chewing gum dominates the global market, accounting for approximately 52% of total market revenue in 2025. This leadership is primarily driven by rising global health consciousness, increasing prevalence of diabetes and obesity, and strong endorsement from dental professionals who recommend sugar-free gum for improved oral hygiene and saliva stimulation. Regulatory pressure to reduce sugar consumption in several developed economies has further accelerated adoption. Continuous innovation in xylitol- and stevia-based formulations, improved flavor retention technologies, and expansion of premium sugar-free variants are strengthening its dominance in both mature and emerging markets.

Functional chewing gum is the fastest-growing product segment, supported by increasing consumer demand for convenient wellness delivery formats. Products targeting oral care, energy enhancement, smoking cessation, cognitive performance, and stress relief are gaining traction. This growth is further supported by busy urban lifestyles, rising fitness culture, and consumer preference for on-the-go supplementation. Bubble gum continues to maintain strong demand among younger consumers due to its affordability and playful appeal, while natural and organic gum products are expanding rapidly among environmentally conscious consumers seeking clean-label alternatives. Premiumization across all categories is increasing average selling prices and improving overall market profitability.

Format Insights

Pellet gum remains the leading format globally, accounting for nearly 45% of total market value. Its dominance is driven by superior convenience, portion control, and compatibility with modern resealable packaging formats such as bottles and jars. Consumers increasingly prefer pellet gum for its longer-lasting flavor release and ease of consumption in professional and social settings. Strong retail visibility and impulse purchasing behavior in convenience stores further reinforce its leadership.

Stick gum maintains a stable presence, particularly in traditional retail environments and price-sensitive markets, while center-filled and tablet formats are witnessing accelerated growth due to product differentiation strategies and premium positioning. Innovation in texture engineering, dual-layer flavor systems, and extended-release technologies is enhancing consumer experience and supporting product diversification across all format categories.

Flavor Insights

Mint-flavored chewing gum accounts for approximately 42% of global market revenue, making it the most dominant flavor category. Its leadership is strongly supported by consumer association with breath freshening, oral hygiene, and long-lasting freshness. Peppermint and spearmint remain the most widely consumed variants due to their universal acceptance and cooling sensation profile.

Fruit flavors represent around 30% of demand and are particularly popular among younger demographics due to their sweet and diverse taste profiles. Novelty, herbal, and exotic flavors are expanding rapidly as manufacturers aim to differentiate their offerings and target premium consumer segments. Flavor innovation, including layered taste release and hybrid flavor combinations, is becoming a key competitive strategy to improve brand loyalty and repeat purchase rates.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 38% of global chewing gum sales, making them the dominant distribution channel. Their leadership is driven by strong product visibility, wide assortment availability, and consumer preference for one-stop shopping environments. Strategic product placement near checkout counters further strengthens impulse purchases.

Convenience stores remain highly important due to the impulse-driven nature of chewing gum consumption, particularly in urban areas. Online retail is the fastest-growing channel, supported by increasing e-commerce penetration, direct-to-consumer strategies, subscription-based models, and personalized product recommendations. Pharmacies and drug stores are gaining importance for functional gum products, especially those targeting oral care and smoking cessation, as consumers increasingly associate them with health-oriented purchasing decisions.

Consumer Group Insights

Adults represent the largest consumer group, accounting for approximately 47% of global demand. This segment drives strong consumption of sugar-free and functional gum products, particularly in professional and urban environments where convenience and oral freshness are prioritized. Rising awareness of preventive healthcare continues to reinforce demand among adult consumers.

Young adults represent the fastest-growing segment due to increasing adoption of wellness-oriented lifestyles, experimentation with innovative flavors, and preference for on-the-go consumption formats. Senior consumers are also contributing steadily to growth, particularly through demand for oral care and medicinal gum variants that support dental health and nicotine replacement therapies.

Explore more data points, trends and opportunities Download Free Sample Report

Chewing Gum Market Segmentations

By Product Type

- Sugar-Free Chewing Gum

- Sugared Chewing Gum

- Functional Chewing Gum

- Natural & Organic Chewing Gum

- Bubble Gum

By Format

- Pellet Gum

- Stick/Tab Gum

- Center-Filled Gum

- Tablet Gum

- Ball Gum

- Cut & Wrap Gum

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Pharmacies & Drug Stores

- Specialty Stores

- Duty-Free & Travel Retail

By Consumer Group

- Children

- Teenagers

- Young Adults

- Adults

- Senior Consumers

By End Use

- Oral Care & Dental Health

- Refreshment & Breath Freshening

- Functional Wellness

- Smoking Cessation

- Sports & Energy Consumption

Regional Insights

North America

North America accounted for approximately 34% of global chewing gum revenue in 2025, making it the largest regional market globally. The region’s dominance is underpinned by high per-capita gum consumption, deep brand penetration by leading multinational manufacturers, and strong consumer awareness regarding oral health and sugar-free alternatives. The United States remains the core revenue contributor, supported by a mature retail ecosystem, strong impulse purchase behavior at checkout counters, and continuous product innovation across sugar-free and functional gum categories. Canada also contributes steadily, particularly through rising demand for wellness-oriented and nicotine-replacement gum products.

The regional market is primarily driven by an accelerating consumer shift toward sugar-free and xylitol-based chewing gum, reinforced by widespread dental health awareness campaigns led by healthcare professionals and public health institutions. Increasing adoption of functional gum products, such as energy-boosting, nicotine replacement, and oral care gums, is expanding the category beyond traditional confectionery use. Additionally, strong e-commerce penetration and direct-to-consumer (DTC) strategies are enabling brands to strengthen customer engagement, improve product accessibility, and launch subscription-based gum offerings, further supporting long-term market expansion.

Europe

Europe holds approximately 27% of the global chewing gum market share, with major demand concentrated in Germany, the United Kingdom, France, Italy, and Spain. The region benefits from strong regulatory frameworks encouraging reduced sugar consumption, high consumer preference for clean-label and natural ingredients, and increasing adoption of environmentally sustainable packaging solutions. Germany leads the regional market in terms of volume and value, while Eastern European countries are gradually emerging as new growth contributors due to rising retail penetration and increasing disposable incomes.

Market expansion in Europe is strongly supported by government regulations and public health policies aimed at reducing sugar intake, which continue to accelerate demand for sugar-free chewing gum. Rising consumer preference for natural, organic, and plant-based formulations is also reshaping product innovation strategies. In addition, sustainability consciousness is driving demand for biodegradable gum bases and recyclable packaging formats. The growing role of pharmacies and drug stores in distributing functional gum products, particularly for oral health and smoking cessation, further strengthens category penetration across the region.

Asia-Pacific

Asia-Pacific represents approximately 25% of global chewing gum revenue and is the fastest-growing regional market, with a projected CAGR exceeding 5.5% through 2031. Key markets include China, India, Japan, South Korea, and Indonesia. Japan remains a leader in product innovation, particularly in functional and premium chewing gum categories, while China and India are driving large-scale volume growth supported by expanding consumer bases and rising disposable incomes. Increasing urbanization and retail modernization are significantly improving product availability across both metropolitan and semi-urban regions.

The region’s strong growth is driven by the rapid expansion of the middle-class population, increasing urbanization, and rising exposure to Western lifestyle consumption patterns. Modern retail infrastructure development, including supermarkets, convenience stores, and organized retail chains, is significantly improving product accessibility. The growing influence of younger demographics is also fueling demand for flavored, affordable, and innovative gum formats. Furthermore, the rapid expansion of e-commerce platforms and mobile-first shopping behavior is accelerating product penetration, particularly in emerging economies such as India and Southeast Asia.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, is experiencing steady growth in the chewing gum market, supported by favorable demographic trends and increasing retail modernization. The region is characterized by a young population base and a strong preference for fruit-flavored and affordable chewing gum variants. Global manufacturers are increasingly tailoring their product offerings to suit regional taste preferences and price sensitivity, which is improving accessibility and driving volume growth across urban and semi-urban markets.

Growth in Latin America is primarily driven by rising urbanization, increasing penetration of convenience stores and modern retail formats, and strong demand for low-cost flavored gum products. Aggressive marketing and distribution expansion by global brands are further strengthening market visibility. In addition, the expansion of organized retail and improved supply chain networks is enhancing product availability across remote regions. Youth-driven consumption patterns and impulse buying behavior remain key structural growth enablers for the region.

Middle East & Africa

The Middle East & Africa region is witnessing steady expansion, with key growth markets including Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria. The region benefits from a young and rapidly growing population base, increasing disposable incomes in urban centers, and rising exposure to international consumer brands. Gulf Cooperation Council (GCC) countries, in particular, are driving premium segment demand due to high purchasing power and strong preference for imported confectionery products.

Market growth in the region is driven by accelerating urbanization, expansion of modern retail infrastructure such as supermarkets and hypermarkets, and increasing consumer preference for imported and premium chewing gum brands. Rising awareness of oral hygiene and increasing demand for sugar-free and functional gum products are further supporting category expansion. Additionally, growing youth demographics and increasing tourism activity in GCC countries are contributing to higher consumption of impulse-based confectionery products, strengthening long-term market potential.

Key Players in the Chewing Gum Market

- Mars Incorporated

- Mondelez International

- Perfetti Van Melle

- Lotte Corporation

- Cloetta AB

- Meiji Holdings

- Grupo Arcor

- Orkla ASA

- Ford Gum & Machine Company

- Concord Confections

- Gerrit J. Verburg Company

- Simply Gum

- Peppersmith

- Rev Gum

- Tree Hugger Gum