Raspberry Market Size

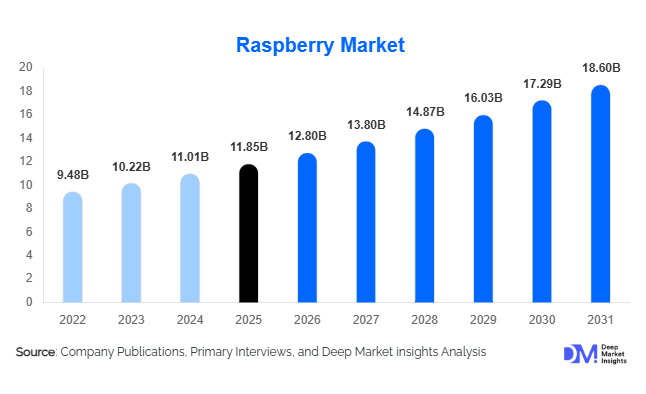

According to Deep Market Insights, the global raspberry market size was valued at USD 11.85 billion in 2025 and is projected to grow from USD 12.80 billion in 2026 to reach USD 18.60 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The raspberry market growth is primarily driven by rising consumer demand for antioxidant-rich superfruits, increasing application in functional foods and nutraceuticals, and expanding global trade of frozen and processed raspberry products supported by advanced cold chain logistics.

Key Market Insights

- Raspberry consumption is shifting toward health-oriented diets, with strong demand in low-sugar, high-fiber, and antioxidant-rich food categories.

- Frozen raspberries dominate industrial usage due to long shelf life, reduced wastage, and year-round availability for food processors.

- Europe remains the leading production hub, supported by strong cultivation in Poland, Spain, and Serbia.

- Asia-Pacific is the fastest-growing demand region, driven by rising disposable incomes and Western dietary adoption.

- Nutraceutical and functional food applications are expanding rapidly, supported by increasing demand for natural bioactive ingredients.

- Cold chain infrastructure development is transforming global trade, enabling cross-border movement of fresh and frozen raspberries.

What are the latest trends in the raspberry market?

Expansion of Functional and Clean-Label Products

The raspberry market is witnessing strong integration into functional food and clean-label product categories. Manufacturers are increasingly using raspberries in protein bars, immunity drinks, probiotic yogurts, and dietary supplements due to their high antioxidant and vitamin content. The demand for organic and pesticide-free raspberries is also rising, especially in premium retail markets across North America and Europe. This shift is encouraging producers to invest in certified organic farming practices and traceability systems, ensuring compliance with stringent food safety standards while capturing higher-margin opportunities.

Technological Advancements in Cold Chain and Processing

Technological improvements in freezing, dehydration, and IQF (Individually Quick Frozen) systems are significantly enhancing raspberry shelf life and export viability. Advanced cold storage infrastructure is reducing post-harvest losses and enabling year-round global supply. Additionally, automation in harvesting and sorting is improving efficiency and reducing labor dependency. These innovations are allowing producers to scale operations while meeting increasing global demand from food manufacturing industries.

What are the key drivers in the raspberry market?

Rising Demand for Functional and Nutrient-Dense Foods

Growing awareness of health and wellness is driving consumers toward nutrient-rich fruits such as raspberries. Their high antioxidant, fiber, and vitamin content makes them a preferred choice in preventive healthcare diets. Increasing prevalence of lifestyle diseases such as obesity and diabetes is further boosting demand for low-calorie natural food alternatives, supporting long-term market expansion.

Expansion of Food Processing and Beverage Industries

The global food processing industry is a major driver of raspberry demand, particularly in bakery, dairy, confectionery, and beverage applications. Raspberries are widely used in jams, juices, desserts, and flavored dairy products. The rise of premium and artisanal food categories is further accelerating industrial consumption, especially in developed markets.

What are the restraints for the global market?

High Production and Labor Costs

Raspberry cultivation is labor-intensive due to delicate harvesting requirements and limited mechanization options. High labor costs in developed regions significantly increase production expenses, limiting scalability and profitability for growers.

Perishability and Supply Chain Constraints

Fresh raspberries have a very short shelf life, making them highly vulnerable to spoilage and post-harvest losses. Inadequate cold storage infrastructure in developing regions further restricts global distribution efficiency and increases dependency on frozen alternatives.

What are the key opportunities in the raspberry industry?

Growth of Nutraceutical and Dietary Supplement Applications

Raspberries are increasingly used in nutraceutical formulations due to their bioactive compounds, including anthocyanins and polyphenols. Demand for natural supplements supporting immunity, digestion, and cardiovascular health is creating high-value opportunities for extract-based raspberry ingredients and powders.

Expansion of Controlled Environment Agriculture

The adoption of greenhouse farming, hydroponics, and vertical cultivation systems is enabling year-round raspberry production with higher yields and improved quality control. This is particularly beneficial in regions with unfavorable climatic conditions, reducing dependency on seasonal harvesting cycles.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.85 Billion |

| Market Size in 2026 | USD 12.80 Billion |

| Market Size in 2031 | USD 18.60 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global raspberry market is characterized by a diverse product type landscape, with frozen raspberries emerging as the dominant category, accounting for nearly 38% of total global revenue. This dominance is primarily driven by their extended shelf life, ease of storage, and suitability for large-scale industrial processing. Frozen raspberries are extensively utilized by food manufacturers, beverage companies, and dessert producers who require consistent year-round supply regardless of seasonal harvest limitations. The ability of frozen raspberries to retain their nutritional profile, color stability, and flavor integrity after processing has further strengthened their position in global supply chains, particularly in regions with high import dependency such as North America and parts of Asia-Pacific. Additionally, the growing expansion of cold chain logistics and improvements in freezing technologies such as IQF (Individually Quick Frozen) methods have significantly enhanced product accessibility and reduced wastage, reinforcing market penetration.Organic raspberries represent the fastest-growing product sub-segment globally, fueled by rising consumer awareness regarding pesticide-free agriculture, sustainability, and clean-label food trends. The demand for organic produce is especially strong in developed markets where regulatory frameworks and certification standards ensure product authenticity. Organic raspberry farming is also gaining support from government subsidies and sustainable agriculture initiatives, further encouraging producers to shift toward eco-friendly cultivation practices. This segment is expected to continue outperforming traditional categories as wellness-oriented consumption patterns intensify globally.

Application Insights

The food and beverage industry remains the largest application segment for raspberries, accounting for a significant share of global consumption. Raspberries are widely used in jams, yogurts, smoothies, baked goods, desserts, ice creams, and flavored beverages. The primary driver of this segment is the growing consumer preference for natural fruit flavors and clean-label ingredients, which has led manufacturers to replace artificial flavoring agents with real fruit inclusions. The versatility of raspberries in both sweet and functional food products has further strengthened their integration into mainstream food processing operations. Additionally, the rising demand for premium and artisanal food products has encouraged manufacturers to incorporate raspberries as a key differentiating ingredient.The nutraceutical and dietary supplement segment is experiencing rapid growth, driven by increasing consumer awareness of preventive healthcare and functional nutrition. Raspberry extracts are widely recognized for their antioxidant properties, anti-inflammatory effects, and potential metabolic health benefits. These attributes have made raspberries a popular ingredient in capsules, powders, energy supplements, and wellness drinks. The expansion of the fitness industry and rising interest in natural health boosters are key contributors to this segment’s growth. Furthermore, scientific research highlighting the bioactive compounds in raspberries has strengthened their credibility in the nutraceutical sector.The bakery and confectionery industry also plays a significant role in raspberry consumption, with demand driven by flavor innovation, seasonal product launches, and premium dessert offerings. Raspberries provide a balance of tartness and sweetness, making them ideal for enhancing product appeal. The growth of artisanal bakeries and specialty dessert shops has further expanded their usage in gourmet applications.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the distribution landscape for raspberries, particularly for fresh produce. The primary driver of this channel is consumer preference for physical product inspection, quality assurance, and immediate availability. These retail formats also benefit from strong supply chain integration and the ability to offer a wide variety of berry products under one roof. Promotional activities and seasonal discounts further enhance sales volumes in this channel, making it the backbone of fresh raspberry distribution.The foodservice and industrial procurement segment plays a crucial role in bulk raspberry consumption. Restaurants, hotels, catering services, and food manufacturers rely heavily on frozen and processed raspberries for large-scale production. The primary driver in this segment is consistent demand from the hospitality and packaged food industries, which require reliable year-round supply. Industrial buyers prioritize cost efficiency, quality consistency, and supply stability, making frozen raspberries particularly important in this channel.Specialty organic stores are gaining increasing relevance, particularly in urban and high-income markets. These stores cater to health-conscious consumers seeking premium, certified organic products. The growth driver in this segment is rising awareness of sustainable consumption and demand for traceable food sourcing.

End-Use Analysis

The food processing industry remains the dominant end-use sector for raspberries globally, driven by strong demand from dairy, bakery, beverage, and confectionery manufacturers. The key growth driver is the scalability and consistency required in industrial food production, where raspberries are used as flavoring agents, fillings, and natural color enhancers. The increasing shift toward natural ingredients and reduction of artificial additives has further accelerated raspberry adoption in processed food manufacturing.Nutraceutical companies represent a high-growth end-use segment, leveraging raspberry bioactive compounds for dietary supplements and functional health products. The main driver is the rising global focus on preventive healthcare, immunity enhancement, and natural wellness solutions. Raspberries are increasingly incorporated into formulations targeting cardiovascular health, weight management, and metabolic balance.Export-driven demand remains highly significant, particularly in Europe and North America, where industrial buyers depend on imported frozen raspberries to maintain year-round production cycles. Global trade integration, improved logistics infrastructure, and growing international demand for berry-based products are key factors supporting this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Raspberry Market Segmentations

By Product Type

- Fresh Raspberries

- Frozen Raspberries

- Processed Raspberries

- Organic Raspberries

By Application

- Food & Beverage

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Foodservice & Hospitality Usage

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / E-commerce

- Specialty Organic Stores

- Foodservice & Industrial Procurement

By End Use

- Household Consumption

- Food Processing Industry

- Nutraceutical Industry

- Cosmetics & Personal Care Industry

By Cultivation Type

- Open Field Cultivation

- Greenhouse Cultivation

- Hydroponic & Controlled Environment Farming

Regional Insights

Europe

Europe holds the largest share of the global raspberry market at approximately 34%, supported by strong domestic production, advanced agricultural practices, and established export networks. Major producing countries such as Poland, Spain, and Serbia play a critical role in supplying both fresh and frozen raspberries to global markets. The primary growth drivers in Europe include favorable climatic conditions, high labor efficiency in berry cultivation, and strong demand from food processing industries. Additionally, the region benefits from a well-developed cold chain infrastructure and stringent quality standards that enhance global competitiveness. Increasing consumer preference for organic and sustainably sourced fruits further strengthens market expansion across Western and Northern Europe.

North America

North America accounts for nearly 29% of global raspberry demand, led by the United States and Canada. The key drivers in this region include strong health-conscious consumer behavior, widespread use of raspberries in dietary supplements, and robust demand from the processed food industry. The United States is a major importer of frozen raspberries, which are used extensively in smoothies, bakery products, and packaged foods. Rising trends in plant-based diets and clean-label consumption are further accelerating market growth. Additionally, expanding retail chains and advanced distribution networks ensure consistent product availability across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, rapid urbanization, and increasing exposure to Western dietary patterns. Countries such as China, India, and Japan are witnessing growing demand for imported raspberries in premium retail, hospitality, and foodservice sectors. The primary growth drivers include expanding middle-class populations, increasing health awareness, and the growing popularity of smoothie culture and dessert innovation. Improved cold chain logistics and rising e-commerce penetration are also enabling wider accessibility of both fresh and frozen raspberries across urban centers.

Latin America

Latin America, particularly Chile and Mexico, plays a strategic role in global raspberry exports. The region benefits from favorable climatic conditions that allow for counter-seasonal production, making it a crucial supplier during off-peak harvesting periods in the Northern Hemisphere. The main drivers of growth include increasing investment in berry cultivation, expansion of export-oriented agriculture, and improving trade agreements with major importing regions. Chile, in particular, has developed a strong reputation for high-quality berry exports, supported by advanced farming techniques and efficient logistics infrastructure.

Middle East & Africa

The Middle East & Africa region is an emerging market for raspberries, driven primarily by rising demand in premium retail, hospitality, and tourism sectors. The key growth drivers include increasing disposable incomes, expanding luxury hotel chains, and growing awareness of healthy dietary choices. The United Arab Emirates and Saudi Arabia are leading import markets due to their strong reliance on imported fresh and frozen fruits. In Africa, gradual improvements in retail infrastructure and urbanization are expected to support long-term market expansion, although consumption levels remain relatively modest compared to other regions.

Key Players in the Global Raspberry Market

- Driscoll's

- Dole plc

- Naturipe Farms

- BerryWorld Group

- Wish Farms

- Sun Belle Inc.

- Hortifrut

- Agroberries

- Greenyard NV

- Ardo

- Berry Gardens Ltd

- Planasa

- Altar Produce

- Mastronardi Produce

- BerryFresh