Hispanic Foods Market Size

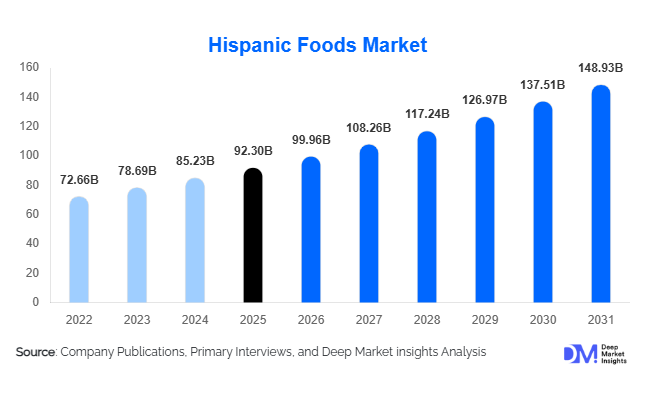

According to Deep Market Insights, the global Hispanic foods market size was valued at USD 92.3 billion in 2025 and is projected to grow from USD 99.96 billion in 2026 to reach USD 148.93 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The Hispanic foods market growth is primarily driven by the increasing global popularity of Mexican and Tex-Mex cuisines, rising demand for ethnic convenience foods, and the expansion of multicultural eating habits across developed and emerging economies. Growing consumption of tortillas, salsa, frozen burritos, taco kits, Hispanic snacks, and ready-to-eat meals is transforming Hispanic foods from a niche ethnic category into a mainstream global packaged food segment.

Food manufacturers are increasingly investing in premium, organic, and clean-label Hispanic food offerings to cater to health-conscious consumers seeking authentic flavors with improved nutritional profiles. The rapid growth of quick-service restaurants, casual dining chains, and food delivery platforms serving Hispanic-inspired menus is further accelerating category penetration globally. Retailers are also dedicating larger shelf spaces to Hispanic products due to high consumer demand and strong product turnover rates. In addition, rising Hispanic populations in North America and increasing international exposure to Latin-inspired cuisine through social media and global travel trends continue to support long-term market expansion. Emerging economies in Asia-Pacific and the Middle East are also witnessing rising demand for Mexican sauces, tortillas, dips, and frozen Hispanic foods, creating new growth avenues for multinational food manufacturers and exporters.

Key Market Insights

- Tortilla and flatbread products dominate the global Hispanic foods market, accounting for nearly 24% of total market revenue due to their versatility and mainstream global consumption.

- Mexican cuisine represents the leading cuisine category, contributing approximately 68% of overall Hispanic food demand globally.

- North America dominates the Hispanic foods market, supported by strong retail penetration, demographic demand, and mature Tex-Mex foodservice infrastructure.

- Asia-Pacific is the fastest-growing regional market, driven by rising urbanization, international food adoption, and expansion of Mexican restaurant chains.

- Frozen Hispanic foods and ready-to-eat meals are witnessing rapid growth, fueled by busy consumer lifestyles and increasing demand for convenience-oriented meal solutions.

- Clean-label, organic, and plant-based Hispanic food innovations are reshaping premium market segments globally.

Hispanic Foods Market Latest Trends

Premium and Clean-Label Hispanic Foods Gaining Popularity

Consumers are increasingly shifting toward premium Hispanic food products prepared using organic ingredients, non-GMO corn, preservative-free sauces, and minimally processed formulations. This trend is particularly visible across developed markets such as the United States, Canada, Germany, and the United Kingdom, where consumers are prioritizing healthier ethnic meal alternatives. Food manufacturers are introducing gourmet salsa variants, artisanal tortilla chips, avocado-based dips, and premium frozen meals to capture higher-margin opportunities within the category. Demand for clean-label products with transparent ingredient sourcing and sustainable packaging is also rising rapidly, encouraging brands to reformulate products and invest in eco-friendly production practices.

Expansion of Frozen and Convenience Hispanic Foods

The rapid growth of convenience-oriented lifestyles is accelerating demand for frozen Hispanic foods, microwaveable burritos, taco kits, enchiladas, and ready-to-cook meal solutions. Consumers are increasingly seeking authentic restaurant-style Hispanic meals that offer both convenience and affordability. Retail chains are therefore expanding frozen ethnic food aisles and increasing private-label Hispanic product offerings. Foodservice operators and quick-service restaurant chains are also leveraging frozen Hispanic ingredients to improve operational efficiency and reduce preparation times. Innovations in freezing technologies and packaging solutions are helping manufacturers improve shelf stability while preserving authentic flavors and textures.

Hispanic Foods Market Drivers

Rising Global Demand for Ethnic and Fusion Cuisine

The increasing consumer preference for ethnic cuisines and multicultural eating experiences is a major driver of the Hispanic foods market. Mexican and Tex-Mex dishes such as tacos, burritos, quesadillas, and nachos have achieved mainstream popularity globally, particularly among younger consumers seeking bold and spicy flavor profiles. Social media food trends, food tourism, and restaurant chain expansion are further increasing exposure to Hispanic cuisine. Retailers and foodservice operators are continuously expanding product portfolios to capitalize on growing consumer interest in globally inspired foods.

Rapid Expansion of Quick-Service Restaurants and Food Delivery Platforms

The growing penetration of quick-service restaurants and food delivery applications offering Hispanic-inspired menus is significantly boosting market demand. Global restaurant chains are increasingly introducing burrito bowls, tacos, nachos, enchiladas, and salsa-based products into mainstream menus. Food delivery platforms are also expanding accessibility to Hispanic meals across urban markets. This trend is strengthening upstream demand for tortillas, sauces, seasonings, frozen fillings, and ready-to-cook ingredients. International casual dining expansion across Asia-Pacific and the Middle East is further accelerating consumption of packaged Hispanic foods.

Global Market Restraints

Volatility in Agricultural Raw Material Prices

Price fluctuations in key raw materials such as corn, avocados, dairy products, peppers, and edible oils remain a major challenge for Hispanic food manufacturers. Climatic disruptions, trade restrictions, and supply chain bottlenecks can significantly impact production costs and reduce operating margins. Since several Hispanic food products rely heavily on agricultural commodities, manufacturers face difficulties maintaining stable pricing during inflationary periods. Rising transportation and cold-chain logistics costs are also adding pressure across global supply networks.

Intense Competition and Private-Label Expansion

The Hispanic foods market is becoming increasingly competitive as multinational food companies and retail chains aggressively expand private-label offerings. Smaller authentic brands often face pricing pressures and shelf-space limitations within major retail channels. Maintaining authenticity while scaling global production also remains challenging, particularly in regions where sourcing traditional ingredients can be difficult. Consumer expectations regarding flavor consistency, premium quality, and affordability continue to intensify competition within the market.

Hispanic Foods Industry Key Opportunities

Growth of Plant-Based and Health-Focused Hispanic Foods

The rising popularity of plant-based diets and healthier meal alternatives presents strong opportunities for Hispanic food manufacturers. Companies are increasingly developing vegan burritos, plant-based taco fillings, dairy-free queso dips, and low-sodium Hispanic sauces to address evolving consumer preferences. Demand for protein-rich bean-based meals, cauliflower tortillas, and organic Hispanic snacks is expanding rapidly among health-conscious urban consumers. Premium health-focused Hispanic products are expected to generate significant revenue opportunities across North America and Europe.

Expansion Through E-Commerce and International Distribution

E-commerce grocery platforms and cross-border retail distribution networks are creating new growth avenues for Hispanic food brands. Online grocery applications are helping small and mid-sized authentic Hispanic brands expand internationally without relying entirely on traditional retail infrastructure. Rising multicultural populations and increasing international food consumption across Europe, Asia-Pacific, and the Gulf countries are further supporting export-driven demand for tortillas, sauces, seasonings, and frozen Hispanic meals. Export-oriented suppliers from Mexico and the United States are expected to benefit significantly from this trend.

Product Type Insights

Tortilla and flatbread products continue to dominate the global Hispanic foods market, accounting for nearly 24% of total revenue in 2025. The leadership of this segment is primarily driven by the widespread consumption of tortillas across both traditional Hispanic cuisines and mainstream convenience foods. Corn tortillas, flour tortillas, taco shells, wraps, and flatbreads have become staple products within retail and foodservice channels due to their affordability, versatility, longer shelf life, and compatibility with multiple meal formats including tacos, burritos, quesadillas, wraps, and snack applications. Rising consumer preference for convenient meal preparation and increasing popularity of Mexican-inspired diets are further strengthening demand for tortilla-based products globally. Manufacturers are also introducing gluten-free, organic, multigrain, and low-carb tortilla variants to address evolving health-conscious consumer preferences.Frozen Hispanic foods are among the fastest-growing product categories owing to rising adoption of ready-to-eat and microwaveable meal solutions among urban consumers. Frozen burritos, enchiladas, tacos, fajitas, and Hispanic-inspired meal kits are witnessing strong demand due to busy lifestyles, increasing dual-income households, and expanding retail freezer infrastructure. The convenience offered by frozen Hispanic meals, combined with improvements in product quality and flavor preservation technologies, continues supporting strong category growth across developed and emerging markets.Meat products including chorizo, marinated beef, seasoned chicken, and Hispanic-style sausages continue gaining traction across foodservice applications as restaurants increasingly expand Latin-inspired menus. Rising demand for protein-rich convenience foods and authentic restaurant experiences is further supporting category growth. Additionally, Hispanic bakery products and desserts such as churros, tres leches cakes, empanadas, and sweet breads are increasingly penetrating mainstream retail channels due to growing consumer interest in international desserts and indulgent bakery offerings.

Cuisine Type Insights

Mexican cuisine remains the dominant cuisine segment within the global Hispanic foods market, contributing approximately 68% of total market value in 2025. The segment’s leadership is primarily driven by strong global consumer familiarity with tacos, burritos, enchiladas, nachos, fajitas, and salsa products, which have transitioned from ethnic specialties into mainstream meal choices across multiple regions. The rapid expansion of Mexican quick-service restaurants, growing retail availability of Mexican meal kits, and increasing demand for bold and spicy flavors continue supporting long-term market dominance. In addition, continuous innovation in sauces, seasonings, tortillas, and frozen Mexican meals is further enhancing product accessibility among international consumers.Caribbean and South American Hispanic cuisines are gradually gaining traction as consumers increasingly seek differentiated ethnic flavor experiences beyond traditional Mexican offerings. Products inspired by Cuban, Brazilian, Peruvian, and Argentine cuisines are expanding in premium retail and specialty food channels. Growing consumer interest in authentic international recipes, regional spices, grilled meats, and tropical flavors is creating new growth opportunities for manufacturers.Fusion Hispanic cuisine combining Latin flavors with Asian, Mediterranean, and American culinary styles is emerging as an important innovation segment within the market. Food manufacturers and restaurant operators are increasingly launching hybrid menu concepts such as Korean tacos, Latin-inspired burgers, spicy Hispanic noodles, and Mediterranean burrito bowls to attract younger consumers seeking culinary experimentation and social media-driven food experiences.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the Hispanic foods market, accounting for nearly 42% of global sales in 2025. The leading position of this segment is driven by strong product visibility, broad consumer accessibility, and expanding shelf space dedicated to tortillas, sauces, frozen Hispanic meals, snacks, and seasonings. Large retail chains continue expanding ethnic food sections in response to rising multicultural food demand and high inventory turnover rates associated with Hispanic food products. Strategic promotional campaigns, private-label product launches, and partnerships with Hispanic food manufacturers are further contributing to segment growth.Online retail is emerging as one of the fastest-growing distribution channels due to increasing adoption of digital grocery shopping platforms and direct-to-consumer food delivery services. Consumers are increasingly purchasing specialty Hispanic ingredients, imported sauces, frozen meals, and snack products through e-commerce channels due to wider product availability and convenience. Subscription meal kits and online ethnic grocery platforms are also contributing to market expansion.Specialty Hispanic stores continue playing a critical role in maintaining demand for authentic imported products and regional flavor varieties. These stores remain important for consumers seeking traditional ingredients, locally sourced spices, premium sauces, and culturally authentic food products that may not be widely available in mainstream retail outlets.

End-Use Insights

Household retail consumption represents the largest end-use segment in the Hispanic foods market, contributing nearly 57% of total market demand in 2025. The dominance of this segment is primarily driven by increasing consumer preference for preparing Hispanic-inspired meals at home using taco kits, tortillas, sauces, frozen meals, seasonings, and ready-to-cook ingredients. Rising home cooking trends, growing exposure to international cuisines through digital media, and the affordability of Hispanic meal preparation continue supporting strong retail consumption globally.Quick-service restaurants and foodservice operators are among the fastest-growing end-use segments due to rising global demand for tacos, burrito bowls, quesadillas, nachos, and Latin-inspired convenience meals. Restaurant chains are increasingly expanding Hispanic menu offerings to capitalize on consumer demand for flavorful and customizable dining experiences. The rapid growth of food delivery applications and cloud kitchens specializing in Mexican and Tex-Mex cuisines is also accelerating foodservice demand.Institutional catering providers, hotels, airlines, and corporate cafeterias are increasingly integrating Hispanic-inspired menu options to cater to evolving multicultural consumer preferences. The incorporation of tortillas, salsa products, Hispanic rice dishes, and grilled meat preparations into institutional foodservice menus is supporting additional market growth opportunities.Growing export demand for foodservice-grade tortillas, frozen Hispanic meals, sauces, and seasoning products is further strengthening overall market expansion. International distributors and hospitality operators are increasingly sourcing Hispanic food products to meet rising global consumer demand for authentic ethnic cuisine experiences.

| By Product Type | By Cuisine Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America dominates the global Hispanic foods market, accounting for approximately 46% of total revenue in 2025. The region’s leadership is primarily driven by the large Hispanic population base, strong consumer familiarity with Mexican cuisine, and the highly developed Tex-Mex restaurant ecosystem across the United States and Canada. The United States remains the largest country market globally, contributing nearly 39% of worldwide Hispanic food consumption due to extensive retail penetration, high demand for convenience foods, and widespread availability of tortillas, sauces, frozen meals, and snack products across mainstream supermarkets and foodservice channels.Growth across North America is further supported by rising multicultural food consumption trends, increasing demand for authentic ethnic flavors, and continued expansion of quick-service restaurant chains offering Hispanic-inspired menu items. Consumers are increasingly seeking organic tortillas, clean-label salsa products, plant-based Hispanic meals, and premium frozen offerings, encouraging manufacturers to invest in product innovation. Canada is also witnessing rising demand for frozen Hispanic foods, premium dips, and ready-to-cook Tex-Mex meal kits due to changing urban lifestyles and growing international food exposure.

Europe

Europe accounts for nearly 17% of global Hispanic foods demand, led by the United Kingdom, Germany, France, and Spain. Regional market growth is primarily driven by increasing exposure to international cuisines, rising popularity of convenience foods, and growing influence of social media food trends among younger consumers. Mexican-inspired meals, tortilla chips, salsa products, wraps, and ready-to-eat Tex-Mex offerings are becoming increasingly popular across supermarkets, restaurants, and casual dining chains.Retailers throughout Europe are rapidly expanding ethnic food aisles while introducing private-label Hispanic products to capitalize on growing consumer demand for affordable international meal options. The expansion of online grocery platforms and food delivery services is further supporting accessibility of Hispanic food products across urban markets. Younger consumers are particularly contributing to demand growth within premium, fusion, and health-focused Hispanic food categories, including organic tortillas, vegan burritos, and clean-label sauces.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market and is projected to expand at a CAGR exceeding 10% during the forecast period. The region’s rapid growth is primarily driven by urbanization, rising disposable incomes, westernization of food consumption patterns, and the aggressive expansion of international foodservice chains across major metropolitan areas. Countries including China, Japan, South Korea, India, and Australia are witnessing increasing consumption of tortillas, salsa products, frozen burritos, taco kits, and Tex-Mex restaurant offerings.The growth of modern retail infrastructure, rising popularity of international cuisines among younger consumers, and increasing social media influence are encouraging experimentation with Hispanic foods throughout the region. Expanding tourism, international travel exposure, and the proliferation of global restaurant franchises are also accelerating adoption of Mexican and Tex-Mex cuisine. In addition, increasing demand for convenient ready-to-eat meals and premium snack products is creating favorable opportunities for Hispanic food manufacturers within Asia-Pacific markets.

Latin America

Latin America accounts for approximately 22% of global Hispanic foods market revenue, with Mexico serving as both a leading producer and consumer of Hispanic food products. The region benefits from strong cultural familiarity with tortillas, sauces, seasonings, beans, and traditional Hispanic meal formats. Mexico continues functioning as a major export hub for tortillas, salsa products, frozen meals, spices, and Tex-Mex ingredients supplied to North America and Europe.Regional market growth is further supported by increasing urbanization, expansion of organized retail channels, and rising consumer demand for packaged convenience foods. Brazil and Argentina are experiencing growing adoption of Mexican-inspired snacks, sauces, and frozen meal products due to changing urban consumption habits and increasing international food exposure. Expanding foodservice infrastructure and rising popularity of casual dining chains are also supporting broader regional market penetration.

Middle East & Africa

The Middle East & Africa region is gradually emerging as a promising growth market for Hispanic foods, particularly across the UAE, Saudi Arabia, and South Africa. Regional demand is being driven by rising tourism activity, expanding expatriate populations, increasing westernization of food preferences, and the rapid growth of international restaurant chains offering Tex-Mex and Mexican-inspired menu options.Premium supermarkets, hospitality operators, and foodservice providers across Gulf countries are increasingly integrating tortillas, salsa products, frozen burritos, taco kits, and Hispanic sauces into retail and dining offerings to cater to younger urban consumers and international visitors. Rising disposable incomes, growing demand for convenience foods, and expansion of modern retail infrastructure are further supporting market growth across the region. In addition, increasing exposure to global food trends through digital platforms and international travel is encouraging broader consumer acceptance of Hispanic cuisine throughout the Middle East and Africa.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Hispanic Foods Market

- Gruma

- Conagra Brands

- General Mills

- Campbell Soup Company

- PepsiCo

- Hormel Foods

- Kraft Heinz

- B&G Foods

- Sigma Alimentos

- Hain Celestial

- Ajinomoto

- Nestlé

- Unilever

- Mission Foods

- Tyson Foods